The Euro’s Death Wish

Authored by Alasdair Macleod via GoldMoney.com,

Last week’s Goldmoney article explained the Fed’s increasing commitment to dollar hyperinflation. This week’s article examines the additional issues facing the euro and the Eurozone.

More nakedly than is evidenced by other major central banks, the ECB through its system of satellite national central banks is now almost solely committed to financing national government debts and smothering over the consequences. The result is a commercial banking system both highly leveraged and burdened with overvalued government debt secured only by an implied ECB guarantee.

The failings of this statist control system have been covered up by a pass-the-parcel any collateral goes €10 trillion plus repo market, which with the TARGET2 settlement system has concealed the progressive accumulation of private sector bad debts ever since the first Eurozone crisis hit Spain in 2012.

These distortions can only continue so long as interest rates are suppressed beneath the zero bound. But rising interest rates globally are now a certainty — only officially unrecognised by central bankers — so there can only be two major consequences. First, the inevitable Eurozone economic recession (now being given an extra push through renewed covid restrictions) will send debt-burdened government deficits which are already high soaring, requiring an accelerated pace of inflationary financing by the ECB. And second, the collapse of the bloated repo market, which is to be avoided at all costs, will almost certainly be triggered.

This article attempts to clarify these issues. It is hardly surprising that for the ECB raising interest rates is not an option. Therefore, the recent weakness of the euro on the foreign exchanges marks only the start of a threat to the euro system, the outcome of which will be decided by the markets, not the ECB.

Introduction

The euro, as it is said of the camel, was designed by a committee. Unlike the ship of the desert the euro and its institutions will not survive — we can say that with increasing certainty considering current developments. Instead of evolving as demanded by its users, the euro has become even more of a state control mechanism than the other major currencies, with the exception, perhaps, of China’s renminbi. But for all its faults, the Chinese state at least pays attention to the economic demands of its citizens to guide it in its management of the currency. The commissars in Brussels along with national politicians seem to be blind to the social and economic consequences of drifting into totalitarianism, where people are forced into new lockdowns and in some cases are being forced into mandatory covid vaccinations.

The ECB in Frankfurt has also ignored the economic consequences of its actions and has just two priorities intact from its inception: to finance member governments by inflationary means and to suppress or ignore all evidence of the consequences.

The ECB’s founding was not auspicious. Before monetary union socialistic France relied on inflationary financing of government spending while Germany did not. The French state was interventionist while Germany fostered its mittelstand with sound money. The compromise was that the ECB would be in Frankfurt (the locational credibility argument won the day) while its first true president, after Wim Duisenberg oversaw its establishment and cut short his presidency, would be French: Jean-Claude Trichet. Membership qualifications for the Eurozone were set out in the Maastricht treaty, and then promptly ignored to let in Italy. They were ignored again to let in Greece, which in terms of ease of doing business ranked lower than both Jamaica and Columbia at the time. And now the Maastricht rules are ignored by everyone.

Following the establishment of the ECB the EU made no attempt to tackle the divergence between fiscally responsible Germany with similarly conservative northern states, and the spendthrift southern PIGS. Indeed, many claimed a virtue in that Germany’s savings could be deployed for the benefit of investment in less advanced member nations, a belief insufficiently addressed by the Germans at the time. The ECB presided over the rapidly expanding balance sheets of the major banks which in the early days of the euro made them fortunes arbitraging between Germany’s and the PIGs’ converging bond yields. The ECB was seemingly oblivious to the rapid balance sheet expansion with which came risks spiralling out of control. To be fair, the ECB was not the only major central bank unaware of what was happening on the banking scene ahead of the great financial crisis, but that does not absolve it from responsibility.

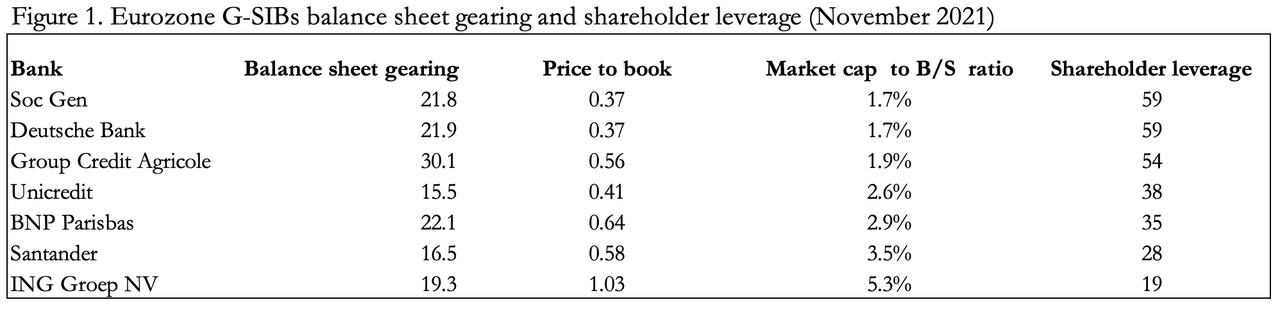

The ECB and its banking regulator (the European Banking Authority — EBA) has done nothing since the Lehman failure to reduce banking risk. Figure 1 shows current leverages for the Eurozone’s global systemically important banks, the G-SIBs. Doubtless, there are other lesser Eurozone banks with even higher balance sheet ratios, the failure of any of which threatens the Eurosystem itself.

Even these numbers don’t tell the whole story. Most of the credit expansion has been into government debt aided and abetted by Basel regulations, which rank government debt as the least risky balance sheet asset, irrespective whether it is German or Italian. Throughout the PIGS, private sector bad debts have been rated as “performing” by national regulators so that they can be used as collateral against loans and repurchase agreements, depositing them into the amorphous TARGET2 settlement system and upon other unwary counterparties.

Figure 2 shows the growth of M1 narrow money, which has admittedly not been as dramatic as in the US dollar’s M1. But the translation of bank lending into circulating currency in the Eurozone is by way of government borrowing without stimulation cheques. It is still progressing, Cantillon-like, through the monetary statistics. And they will almost certainly increase substantially further on the back of the ongoing covid pandemic, as state spending rises, tax revenues fall, and budget deficits soar. Bear in mind that the new covid lockdowns currently being implemented will knock the recent anaemic recovery firmly on the head and drive the Eurozone into a new slump. There can be no doubt that M1 for the euro area is set to increase significantly from here, particularly since the ECB is now nakedly a machine for inflationary financing.

In the US’s case, rising interest rates, which the Fed is keen to avoid, will undermine the US stock market with knock-on economic effects. In the Eurozone, rising interest rates will undermine spendthrift governments and the entire commercial banking system.

Government debt creation out of control

The table below shows government spending for leading Eurozone states as a proportion of their GDP last year, ranked from highest government spending to GDP to lowest (column 1). The US is included for comparison.

Some of the increase in government spending relative to their economies was due to significant falls in GDP, and some of it due to increased spending. The current year has seen a recovery in GDP, which will have not yet led to a general improvement in tax revenues, beyond sales taxes. And now, much of Europe faces new covid restrictions and lockdowns which are emasculating any hopes of stabilising government debt levels.

The final column in the table adjusts government debt to show it relative to the tax base, which is the productive private sector upon which all government spending, including borrowing costs and much of inflationary financing, depends. This is a more important measure than the commonly quoted debt to GDP ratios in the second column. The sensitivity to and importance of maintaining tax income becomes readily apparent and informs us that government debt to private sector GDP is potentially catastrophic. As well as the private sectors’ own tax burden, through their taxes and currency debasement they are having to support far larger obligations than generally realised. Productive citizens who don’t feel they are on a treadmill going ever faster for no purpose are lacking awareness.

These are the dynamics of national debt traps which only miss one element to trigger them: rising interest rates. Instead, they are being heavily suppressed by the ECB’s deposit rate of minus 0.5%. The market is so distorted that the nominal yield on France’s 5-year bond is minus 0.45%. In other words, a nation with a national debt that is so high as to be impossible to stabilise without the necessary political will to do so is being paid to borrow. Greece’s 5-year bond yields a paltry 0.48% and Italy’s 0.25%. Welcome to the mad, mad world of Eurozone government finances.

The ECB’s policy failure

It is therefore unsurprising that the ECB is resisting interest rate increases despite producer and consumer price inflation taking off. Consumer price inflation across the Eurozone is most recently recorded at 4.1%, making the real yield on Germany’s 5-year bond minus 4.67%. But Germany’s producer prices for October rose 18.4% compared with a year ago. There can be no doubt that producer prices will feed into consumer prices, and that rising consumer prices have much further to go, fuelled by the acceleration of currency debasement in recent years.

Therefore, in real terms, not only are negative rates already increasing, but they will go even further into record territory due to rising producer and consumer prices. It is also the consequence of all major central banks’ accelerated expansion of their base currencies, particularly since March 2020. Unless it abandons the euro to its fate on the foreign exchanges altogether, the ECB will be forced to raise its deposit rate very soon, to offset the euro’s depreciation. And given the sheer scale of previous monetary expansion, which is driving its loss of purchasing power, euro interest rates will have to rise considerably to have any stabilising effect.

But even if they increased only into modestly positive territory, the ECB would have to quicken the pace of its monetary creation just to keep Eurozone member governments afloat. The foreign exchanges will quickly recognise the situation, punishing the euro if the ECB fails to raise rates and punishing it if it does. But it won’t be limited to cross rates against other currencies, which to varying degrees face similar dilemmas, but measured against prices for commodities and essential products. Arguably, the euro’s rerating on the foreign exchanges has already commenced.

The ECB is being forced into an impossible situation of its own making. Bond yields have started to rise or become less negative, threatening to bankrupt the whole Eurozone network as the trend continues, and inflicting mark-to-market losses on highly leveraged commercial banks invested in government bonds. Furthermore, the Euro system’s network of national central banks is like a basket of rotten apples. It is the consequence not just of a flawed system, but of policies first introduced to rescue Spain from soaring bond yields in 2012. That was when Mario Draghi, the ECB’s President at the time said he was ready to do whatever it takes to save the euro, adding, “Believe me, it will be enough”.

It was then and its demise was deferred. The threat of intervention was enough to drive Spanish bond yields down (currently minus 0.24% on the 5-year bond!) and is probably behind the complacent thinking in the ECB to this day. But as the other bookend to Draghi’s promise to deploy bond purchasing programmes, Lagarde’s current intervention policy is of necessity far larger and more destabilising. And then there is the market problem: the ECB now acts as if it can ignore it for ever.

It wasn’t always like this. The euro started with the promise of being a far more stable currency replacement for national currencies, particularly the Italian lira, the Spanish peseta, the French franc, and the Greek drachma. But the first president of the ECB, Wim Duisenberg, resigned halfway during his term to make way for Jean-Claude Trichet, who was a French statist from the École Nationale d’Administration and a career civil servant. His was a political appointment, promoted by the French on a mixture of nationalism and a determination to neutralise the sound money advocates in Germany. To be fair to Trichet, he resisted some of the more overt pressures for inflationism. But then things had not yet started to go wrong on his watch.

Following Trichet, the ECB has pursued increasingly inflationist policies. Unlike the Bundesbank which closely monitored the money supply and paid attention to little else, the ECB adopted a wide range of economic indicators, allowing it to shift its focus from money to employment, confidence polls, long-term interest rates, output measures and others, allowing a fully flexible attitude to money. The ECB is now intensely political, masquerading as an independent monetary institution. But there is no question that it is subservient to Brussels and whose primary purpose is to ensure Eurozone governments’ profligate spending is always financed; “whatever it takes”. The private sector is now a distant irrelevance, only an alternative source of government revenue to inflation, the delegated responsibility of compliant national central banks, who take their orders from the economically remote ECB.

It is an arrangement that will eventually collapse through currency debasement and economic breakdown. Prices rising to multiples of the official CPI target and the necessary abandonment by the ECB of the euro in the foreign exchanges in favour of interest rate suppression now threaten the ability of the ECB to finance in perpetuity increasing government deficits.

The ECB, TARGET2 and the repo market

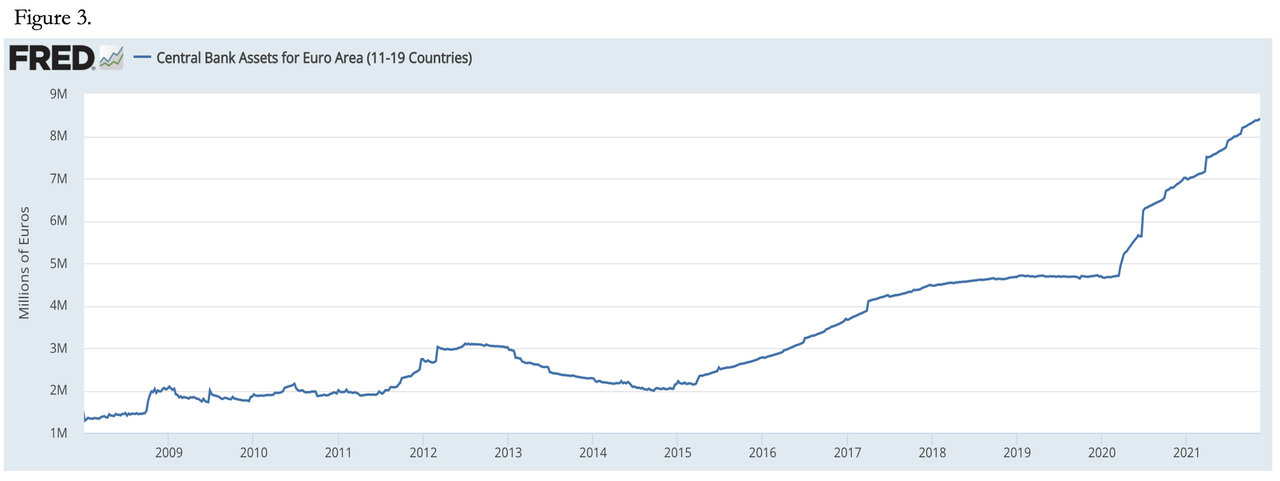

Figure 3 shows how the Eurozone’s central bank balance sheets have grown since the great financial crisis. The growth has virtually matched that of the Fed, increasing to $9.7 trillion equivalent against the Fed’s $8.5 trillion, but from a base about $700bn higher.

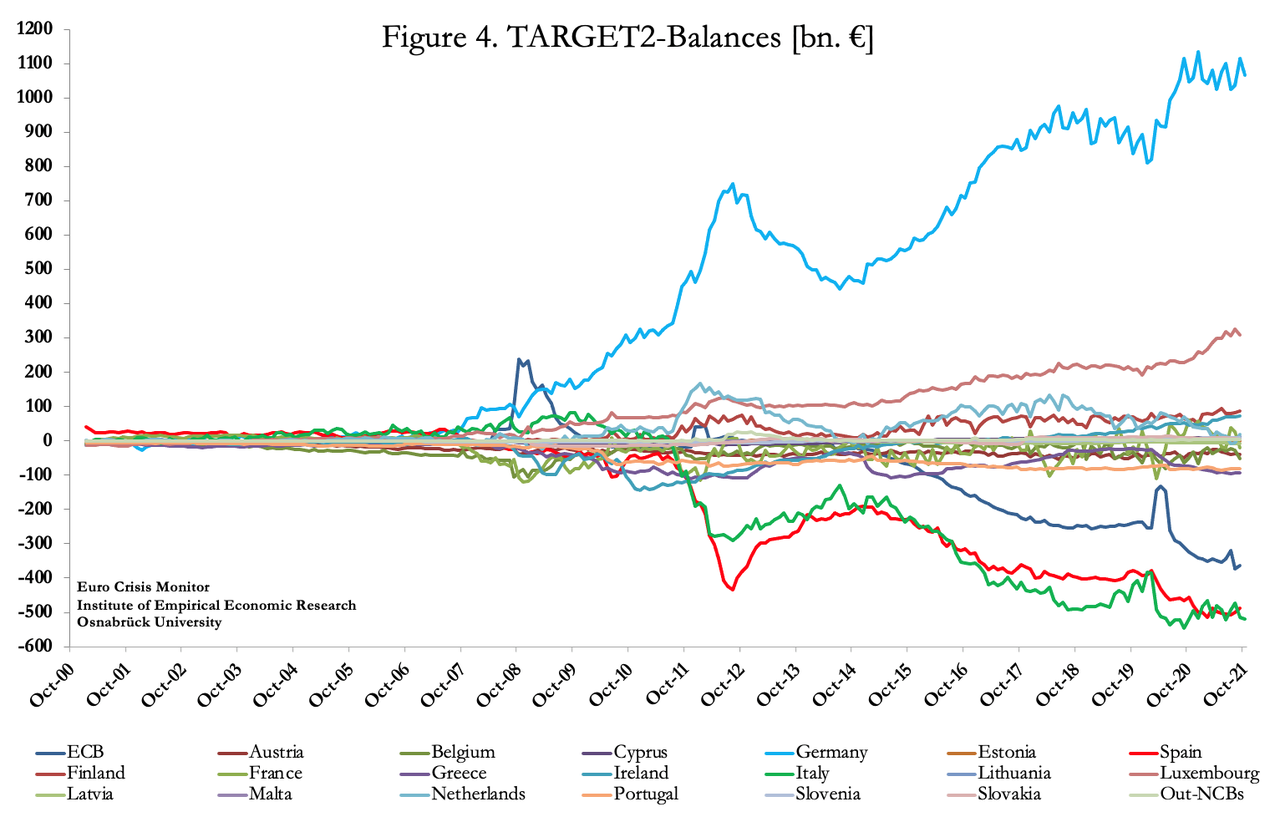

While they are reflected in central bank assets, TARGET2 imbalances are an additional complication, which are shown in the Osnabrück University chart reproduced in Figure 4. Points to note are that Germany is owed €1,067bn. The ECB collectively owes the national central banks (NCBs) €364bn. Italy owes €519bn, Spain €487bn and Portugal €82bn.

The effect of the ECB deficit, which arises from bond purchases conducted on its behalf by the national central banks, is to artificially reduce the TARGET2 balances of debtors in the system to the extent the ECB has bought their government bonds and not paid the relevant national central bank for them.

The combined debts of Italy and Spain to the other national central banks is about €1 trillion. In theory, these imbalances should not exist. The fact that they do and that from 2015 they have been increasing is due partly to accumulating bad debts, particularly in Portugal, Italy, Greece, and Spain. Local regulators are incentivised to declare non-performing bank loans as performing, so that they can be used as collateral for repurchase agreements with the local central bank and other counterparties. This has the effect of reducing non-performing loans at the national level, encouraging the view that there is no bad debt problem. But much of it has merely been removed from national banking systems and lost in both the euro system and the wider repo market.

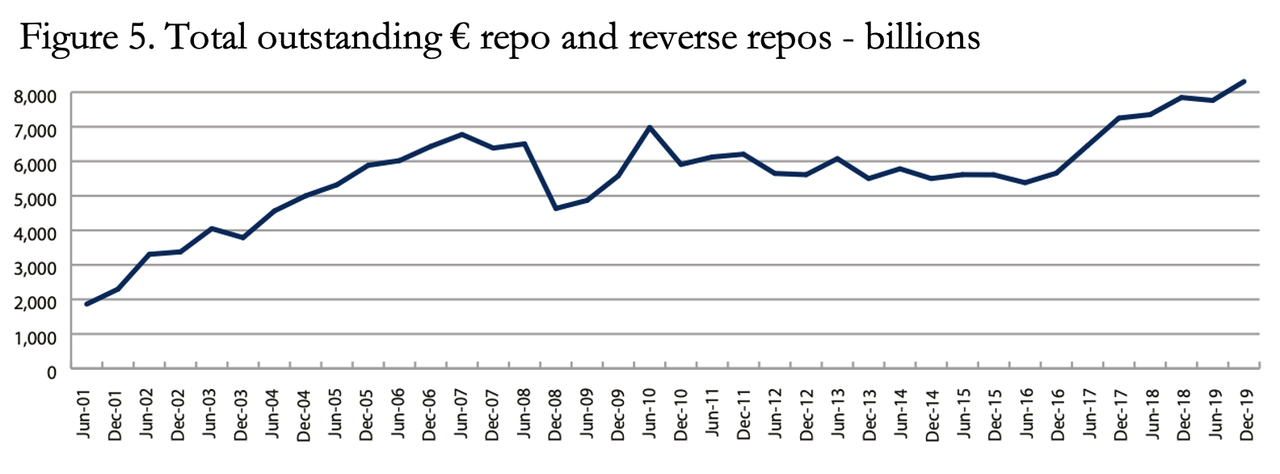

Demand for collateral against which to obtain liquidity has led to significant monetary expansion, with the repo market acting not as a marginal liquidity management tool as is the case in other banking systems, but as an accumulating supply of raw money. This is shown in Figure 4, which is the result of an ICMA survey of 58 leading institutions in the euro system.

The total for this form of short-term financing grew to €8.31 trillion in outstanding contracts by December 2019. The collateral includes everything from government bonds and bills to pre-packaged commercial bank debt. According to the ICMA survey, double counting, whereby repos are offset by reverse repos, is minimal. This is important when one considers that a reverse repo is the other side of a repo, so that with repos being additional to the reverse repos recorded, the sum of the two is a valid measure of the size of the market outstanding. The value of repos transacted with central banks as part of official monetary policy operations were not included in the survey and continue to be “very substantial”. But repos with central banks in the ordinary course of financing are included.

Today, even excluding central bank repos connected with monetary policy operations, this figure probably exceeds €10 trillion, allowing for the underlying growth in this market and when one includes participants beyond the 58 dealers in the survey. An interesting driver of this market is negative interest rates, which means that the repayment of the cash side of a repo (and of a reverse repo) can be less than its initial payment. By tapping into central bank cash through a repo it gives a commercial bank a guaranteed return. This must be one reason that the repo market in euros has grown to be considerably larger than it is in the US.

This consideration raises the question as to the consequences of the ECB’s deposit rate being forced back into positive territory. It is likely to substantially reduce a source of balance sheet funding for commercial banks as repos from national central banks no longer offer negative rate funding. They would then be forced to sell balance sheet assets, which would drive all negative bond yields into positive territory, and higher. Furthermore, the contraction of bank credit implied by the withdrawal of repo finance will almost certainly have the knock-on effect of triggering a widespread banking liquidity crisis in a banking cohort with such high balance sheet gearing.

There is a further issue over collateral quality. While the US Fed only accepts very high-quality securities as repo collateral, with the Eurozone’s national banks and the ECB almost anything is accepted — it had to be when Greece and other PIGS were bailed out. High quality debt represents most of the repo collateral and commercial banks can take it back onto their balance sheets. But the hidden bailouts of Italian banks by taking dodgy loans off their books could not continue to this day without them being posted as repo collateral rolled into the TARGET2 system and into the wider commercial repo network.

The result is that the repos that will not be renewed by commercial counterparties are those whose collateral is bad or doubtful. We have no knowledge how much is involved. But given the incentive for national regulators to have deemed them creditworthy so that they could act as repo collateral, the amounts will be considerable. Having accepted this dodgy collateral, national central banks will be unable to reject them for fear of triggering a banking crisis in their own jurisdictions. Furthermore, they are likely to be forced to accept additional repo collateral rejected by commercial counterparties.

In short, in the bloated repo market there are the makings of the next Eurozone banking crisis. The numbers are far larger than the central banking system’s capital. And the tide will rapidly ebb on them with rising interest rates.

Inflation and interest rate outlook

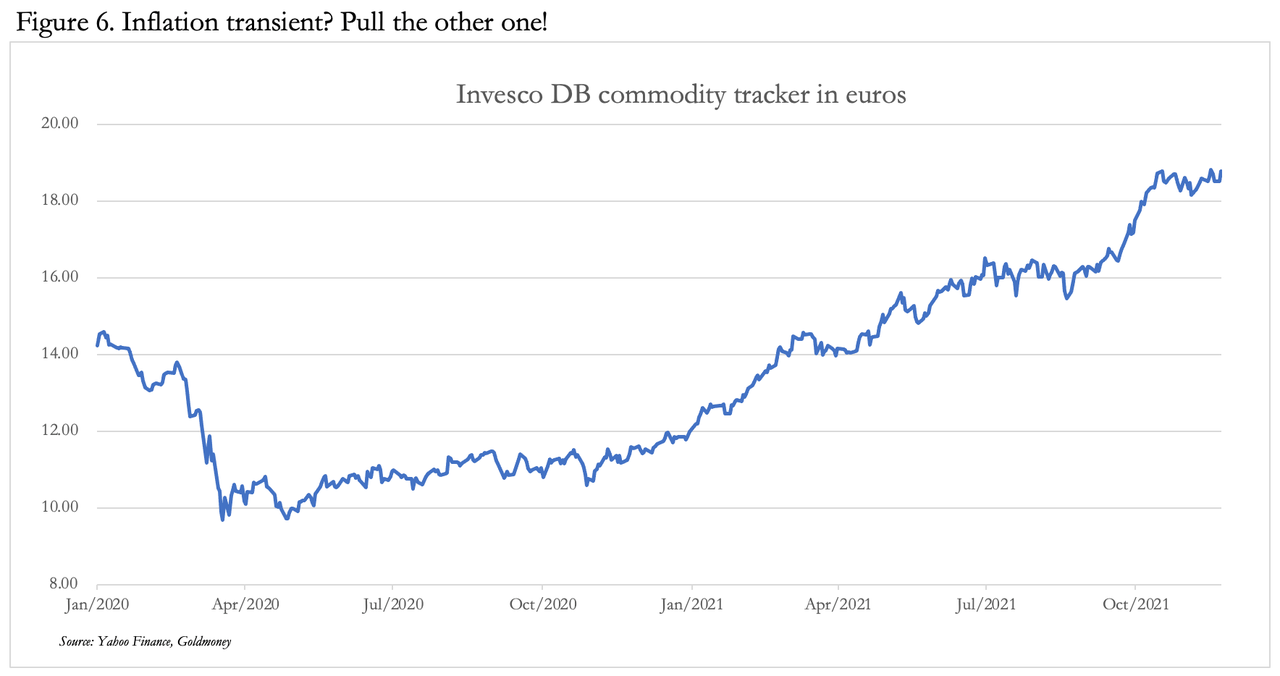

Starting with input prices, the commodity tracker in Figure 6 illustrates the rise in commodity and energy prices in euros, ever since the US Fed went “all in” in early 2020. To these inputs we can add soaring shipping costs, logistical disruption, and labour shortages — in effect all the problems seen in other jurisdictions. Additionally, this article demonstrates that not only is the ECB determined not to raise interest rates, but it simply cannot afford to. Being on the edge of a combined government funding crisis and with a possible collapse in the repo market taking out the banking system, the ECB is paralyzed with fear.

That being so, we can expect further weakness in the euro exchange rate. And the commodity tracker in Figure 6 shows that when commodity prices break out above their current consolidation phase, they will likely push alarmingly higher in euros at least. The ECB’s dilemma over choosing inflationary financing or saving the currency is about to get considerably worse. And for probable confirmation of mounting fear over the situation in Frankfurt, look no further than the resignation of the President of the Bundesbank, who has asked the Federal President to dismiss him early for personal reasons. It was all very polite, but a high-flying, sound money man such as Jens Weidmann is unlikely to just want to spend more time with his family. That he can no longer act as a restraint on the ECB’s inflationism is clear, and more than any outsider he will be acutely aware of the coming crisis.

Let us hope that Weidmann will be available to pick up the pieces and reintroduce a gold-backed mark.

Tyler Durden

Sun, 11/28/2021 – 07:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com