4.3 Trillion Reasons To Be Nervous Into Friday’s Option Expiration

It’s not the economy; it’s the positioning, stupid.

That’s the clear message from Goldman Sachs and SpotGamma as traders ready themselves for a tumultuous week navigating the implicit volatility of tomorrow’s Fed statement, dot-plot, and press conference as turbo-taper-talk is expected, ahead of a very significant options expiration on Friday.

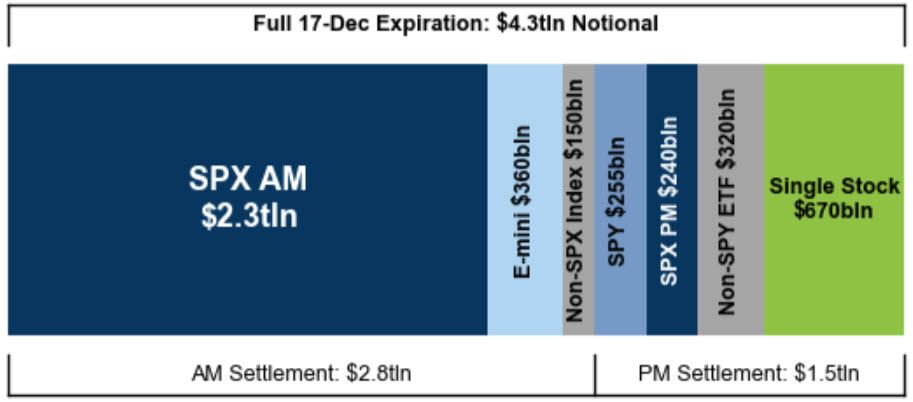

$4.3tln notional of equity options (referencing over 8% of the Russell 3000’s market cap) are expiring (including $2.3tln of SPX quarterly options, $360bln of options on SPX E-mini futures, $255bln of SPY options, and $670bln of single stock options).

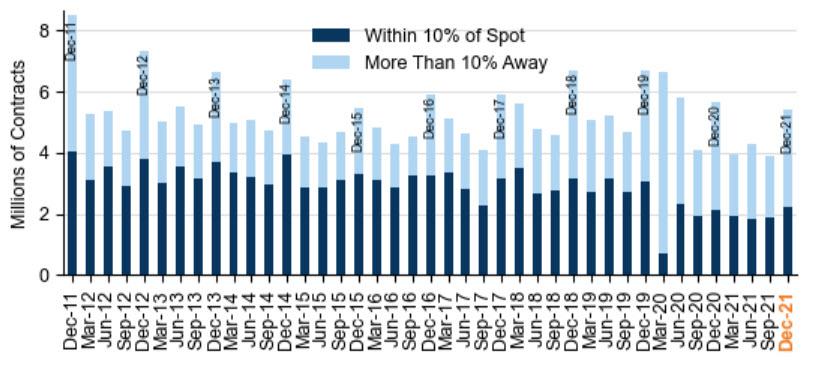

This has historically been the most active week of the option trading year.

The Dec-2021 OpEx has less total open interest than last December’s expiration did, but more of its open interest is near the money than last year’s was. While this is the smallest December expiration in at least a decade, but larger than just about all non-December expirations.

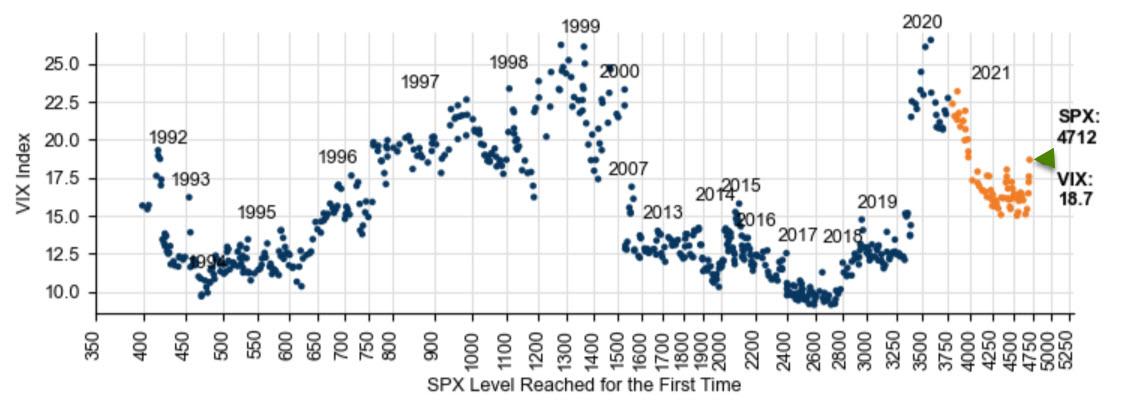

As Goldman notes, elevated volatility over the past month has brought the highest index option volumes of the year, leaving extra positioning slightly below the current spot level following the SPX hitting a new all-time high.

Even when the SPX hit a new all-time high on Friday (10-Dec), the VIX was at its highest for a record-SPX day since the index hit 3975 in March – consistent with an environment of elevated macro risk.

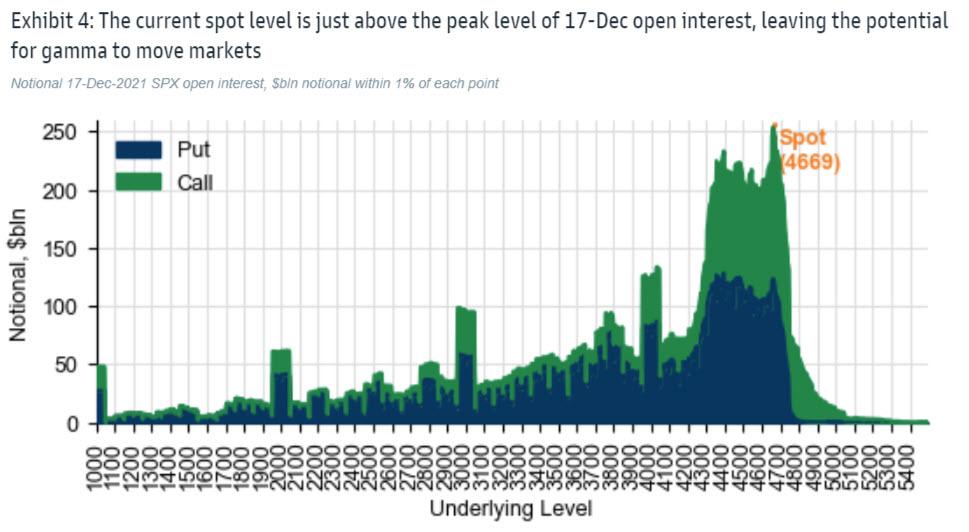

In Goldman’s view, the prevailing high volatility risk premium this year is an indication that investors have been net purchasers of index options, leaving a short “street” gamma position that can help volatility remain elevated this week.

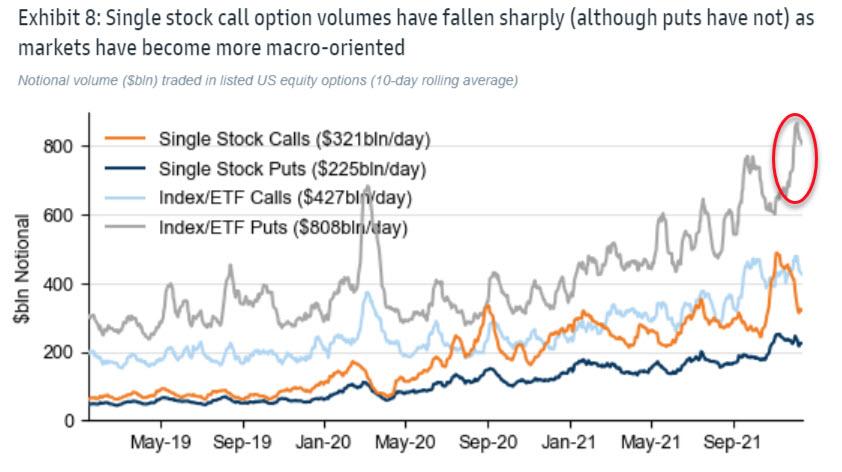

As SpotGamma concludes, single stock volatility remains quite high even as volumes have subsided modestly in recent months.

The sharp negative performance of many stocks is drawing out large put volumes, creating highly concentrated negative gamma in the 12/17 expiration.

For the top 50 stocks with high options volumes, investors traded $196bn in puts on the average day over the past month, up 40% relative to the prior year. TSLA, HD, PFE, AMD and SE are among the high market cap stocks where put volumes were up more than 80% relative to the prior year.

We have nothing constructive to offer about the FOMC meeting itself, or the markets reaction to the event. However, what seems apparent is that the Fed will trigger a “release” of flows tied to a large amount of very short dated negative gamma.

The idea here that we cannot shake is that we generally view the expiration of large put positions as a bullish catalyst (dealers unwind short stock hedges).

Stocks falling farther into 12/17 drives that negative put gamma higher which could lead to a large short (hedge) cover rally into Christmas.

If you recall back to December of 2018 the markets had been dropping sharply into December OPEX. The Monday after OPEX was Christmas Eve, with these infamous headlines:

Despite that doom, the market rallied ~5% from Xmas Eve into 2018 year end.

SpotGamma’s clear point here is that positioning matters, and the current positioning is quite negative but that is heavily tied to 12/17 expiration. Either a bullish Fed and/or OPEX could trigger a violent rally that is purely a function of puts positions unwinding.

Tyler Durden

Tue, 12/14/2021 – 15:05

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com