The Unraveling

Authored by Sven Henrich via NorthmanTrader.com,

Investors are ignoring two big elephants in the room. While we see yet again a positive reaction to the latest Fed meeting with new all time highs in the $ES futures contract things are far from well, indeed things have already been unraveling beneath the surface for a while. A potential Santa rally notwithstanding storm clouds are not only gathering but they are already all around us. I suggest paying close attention, despite the expected upcoming holiday lull.

First off and most importantly: The Fed was NOT hawkish yesterday despite what you hear in the media.

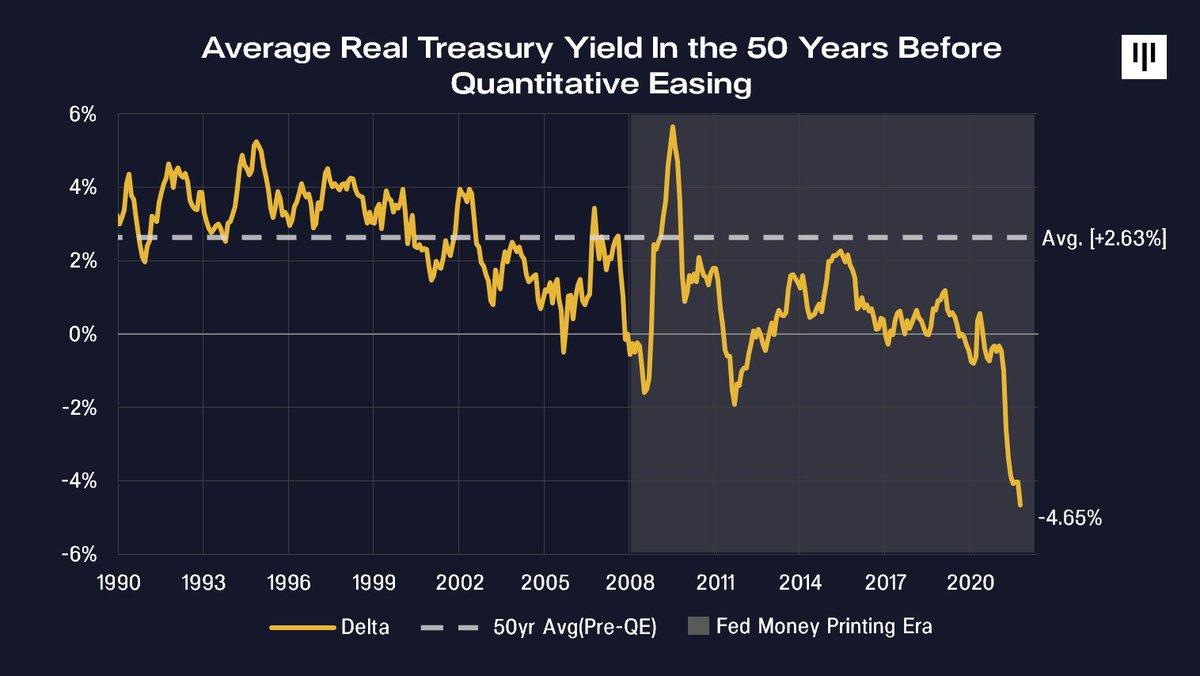

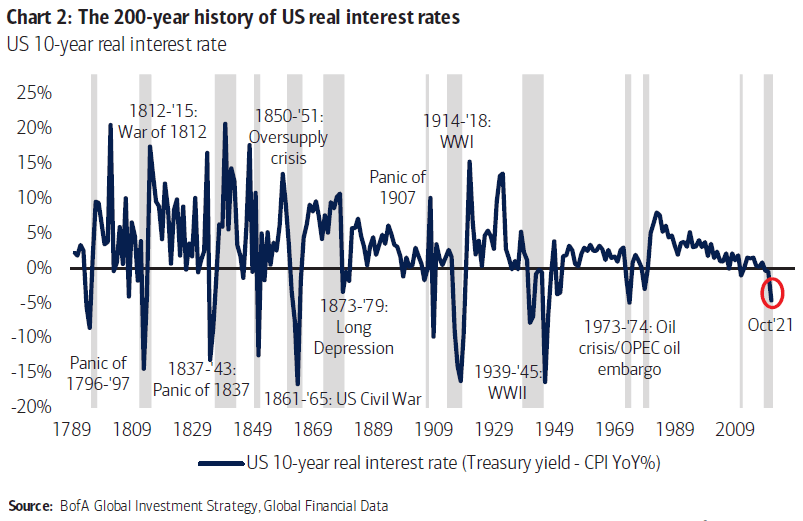

Context: For months on end they insisted that inflation was transitory, then as inflation kept surprising them to the upside they finally retired it and yesterday Powell said that now risk is that inflation is becoming persistent. The policy response to 6.7% CPI and 9.6% PPI? Absolutely nothing in the here and now. In December they are continuing asset purchases and it’s not until January that they will accelerate taper which means they will continue to expand the balance sheet. In addition they will continue to run full negative real rates even with 3 supposed rate hikes next year, for anyway you look at it this is where we are:

Under which economic theory or construct do you fight inflation with real negative rates? I know of none and I suspect neither does the Fed. So the Fed is overtly risking that inflation is becoming entrenched with a weak response and that can be a big problem. I know so because Powell has said so himself in 2018:

“recent research highlights two particularly important cases in which doing too little comes with higher costs than doing too much. The first case is when attempting to avoid severely adverse events such as a financial crisis or an extended period with interest rates at the effective lower bound.21 In such situations, the famous words “We will do whatever it takes” will likely be more effective than “We will take cautious steps toward doing whatever it takes.” The second case is when inflation expectations threaten to become unanchored. If expectations were to begin to drift, the reality or expectation of a weak initial response could exacerbate the problem.”

So why the weak response that sparked the market rally yesterday?

Because of 4 distinct ‘puts’ the Fed and Powell issued yesterday.

First, the most important: Powell admitting yesterday that he is putting market reaction ahead of anything else. When asked why they are not ending asset purchase immediately his response speaks volumes:

![]()

“Markets can be sensitive to it.” That is a direct admission that they don’t want to upset markets and that they are putting market consideration ahead of what might be the right economic policy, ie. fight inflation. It’s also a big admission that they know the balance sheet impacts asset prices which is of course exactly what the ECB’s Schnabel said the other day:

And we know this because I’ve been highlighting it for months. The S&P 500 is in essence a Fed balance sheet tracker and today we again see new highs on what surely will be a new record high on the Fed’s balance sheet. 13 months in a row, tit for tat and equity pullbacks tend to occur when the Fed’s balance sheet temporarily pulls back only to end as soon as the balance sheet cranks right back up, an exercise I advertised in advance during the early December pullback:

Come and see, come and see: As I suggested last week (see tweet above) the Fed’s balance sheet rose again between last Thursday and this Wednesday and took $SPX right back up with it.

I rest my case. pic.twitter.com/qh8bXbRF3l— Sven Henrich (@NorthmanTrader) December 9, 2021

In this sense the S&P 500 has been nothing but a Fed balance sheet tracker. Yet in process the bubble has gotten so large even Powell had to acknowledge the obvious:

Powell: Asset valuations, I’m going very superficial here, but asset valuations are elevated.

YOU THINK? pic.twitter.com/ossdL0TrRJ

— Sven Henrich (@NorthmanTrader) December 15, 2021

I repeat: The asset bubble is so large it is now the biggest threat to the economy should it blow up, hence they can’t afford a major sell off although ironically it would be the quickest way to stop inflation in its track.

The second put was in the Fed statement itself:

“The Committee judges that similar reductions in the pace of net asset purchases will likely be appropriate each month, but it is prepared to adjust the pace of purchases if warranted by changes in the economic outlook. The Federal Reserve’s ongoing purchases and holdings of securities will continue to foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.”

Translated: As soon as there is any trouble, i.e. markets selling off, we will immediately stop the taper. This is the Powell pivot advertised in advance and markets know this. They know all this talk means nothing as Powell is ready to flip on a dime, like he did in 2018. In other words: We will intervene as soon as there is a market correction. See a 10%-20% correction and all rate hike talk dies and QE continues or gets expanded again. And of course if Omicron poses a problem that will serve as an excuse as well. Markets know this and hence they don’t take Powell all that serious when it comes to tapering, raising rates or anything else. They bet on Powell caving as soon as there is any real market trouble. After all the 2018 Powell pivot still in fresh memory.

The third put was Powell’s insistence to point out that even if they end QE the Fed will remain highly accommodative which is proving the earlier point: They are not serious in fighting inflation. To fight inflation you have to be non accommodative, i.e. tightening and they’re not doing that for at least months on end and only if market don’t drop. Rather Powell and team appear to intrinsically believe inflation will soon peak. And while that may be the case consumers will still be left holding the bag for the damage is already apparent and will in many case not reverse at all:

We’re sorry your rent has gone up 20% this year but we won’t raise it by more than 3 % next year, so you see, inflation was just transitory.

— Sven Henrich (@NorthmanTrader) December 15, 2021

The 4th put is the simple fact that now in front of Santa seasonality they are still going pedal to the metal and therefore none of the mechanics have changed and this gives everyone the excuse to go balls in deep to chase year end performance.

Take these 4 puts together and voila, vertical panic rally to the upside and new all time highs in overnight today:

Which brings me to other big elephant in the room:

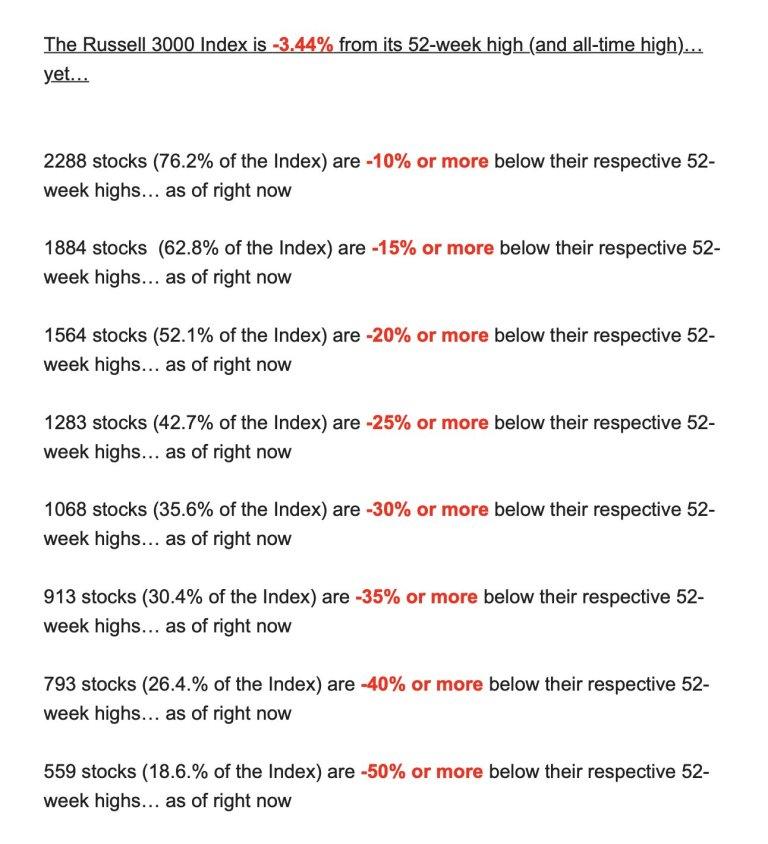

Bear market in stocks bull market in indices.

— Sven Henrich (@NorthmanTrader) December 3, 2021

Be absolutely clear: While main indices are making new all time highs & give the appearance of a raging bull market underneath there already is a raging bear market in individual stocks ( via Carter Worth):

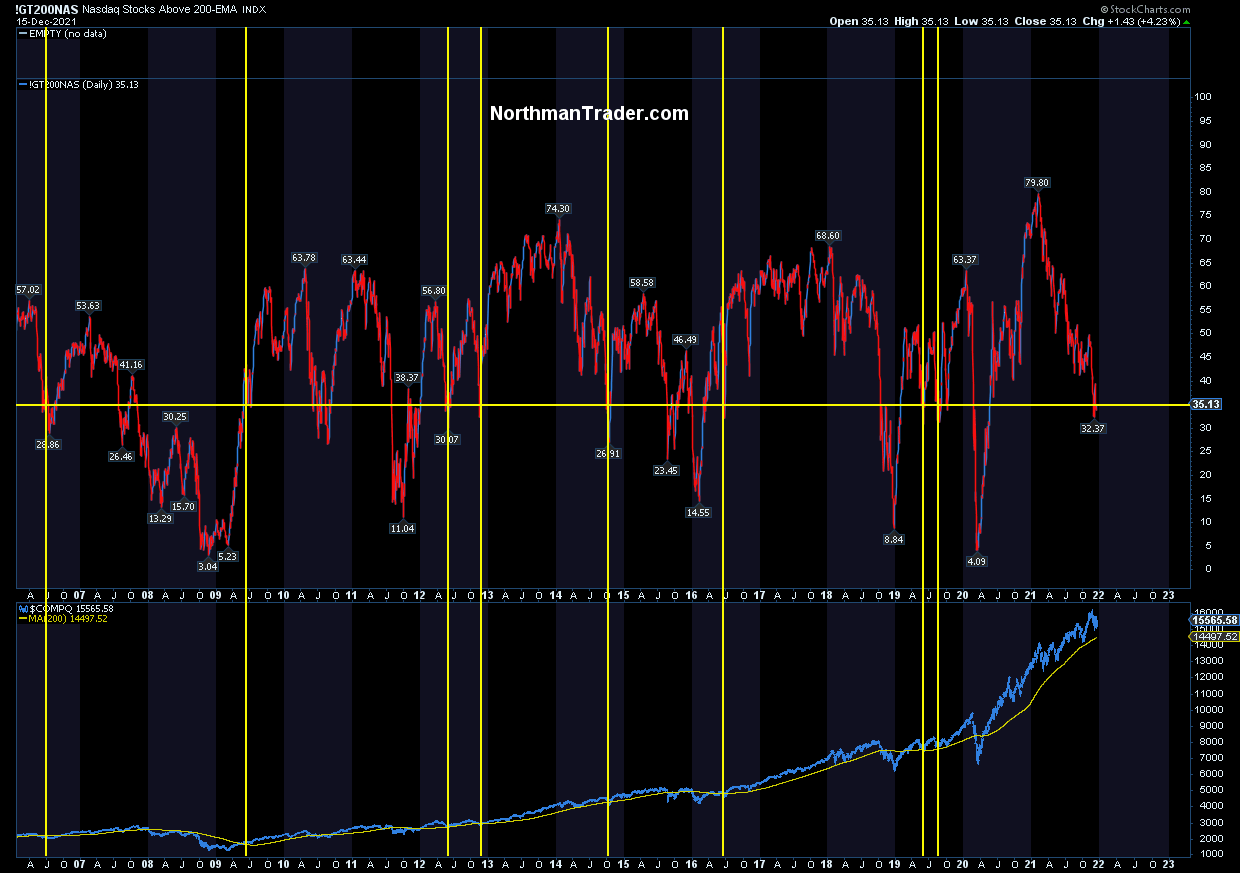

We see it in the almighty Nasdaq where 65% components are trading below the 200 daily moving average:

If the fab 5 were trading below their 200 day moving average people would already be talking about a bear market and be begging for more intervention.

No, the big cap tech stocks are masking all the damage beneath and this market is dependent on these stocks not correcting.

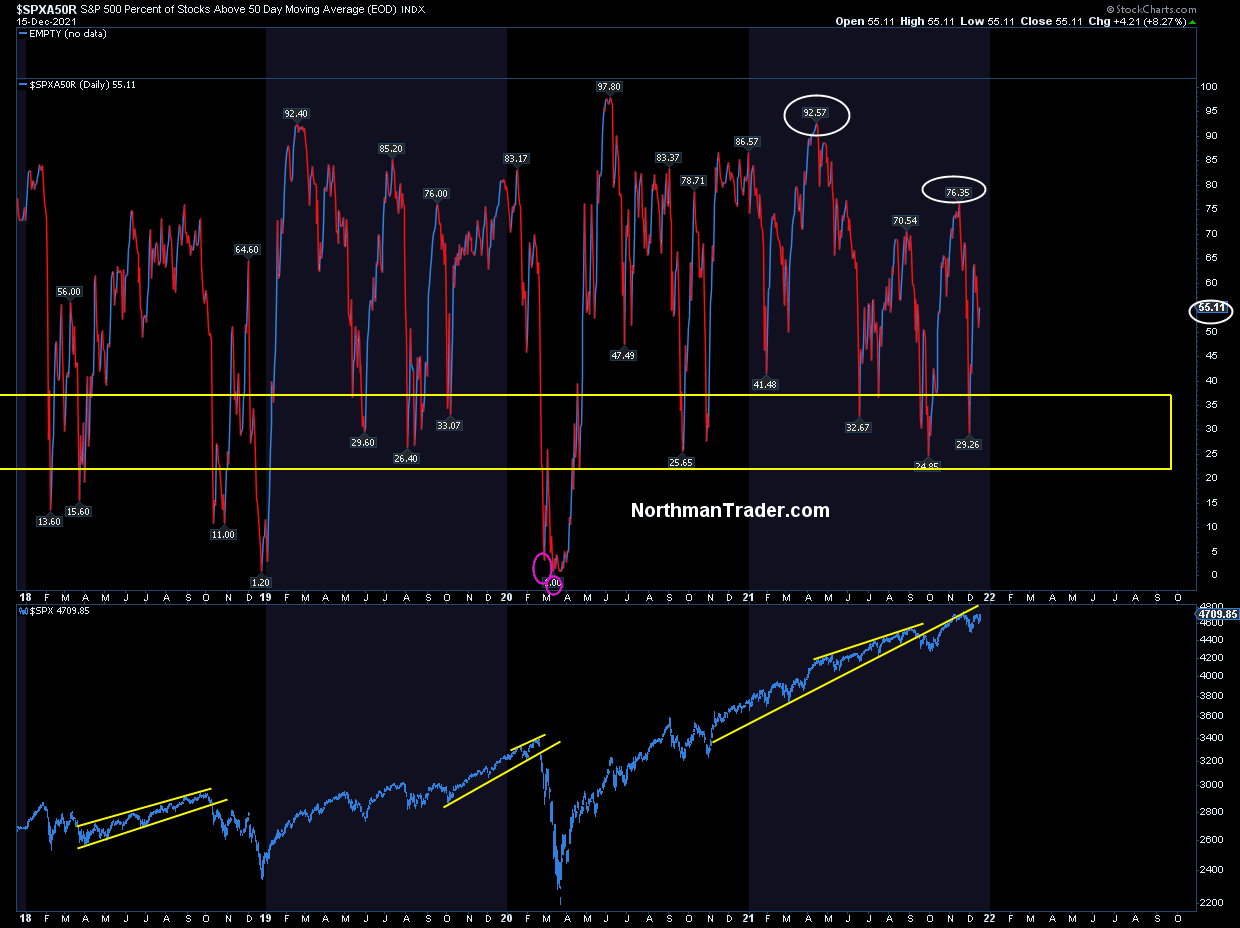

And this divergence is also very notable in the S&P as new highs show ever fewer stoke exhibiting strength.

45% of components are below their 50 day moving average:

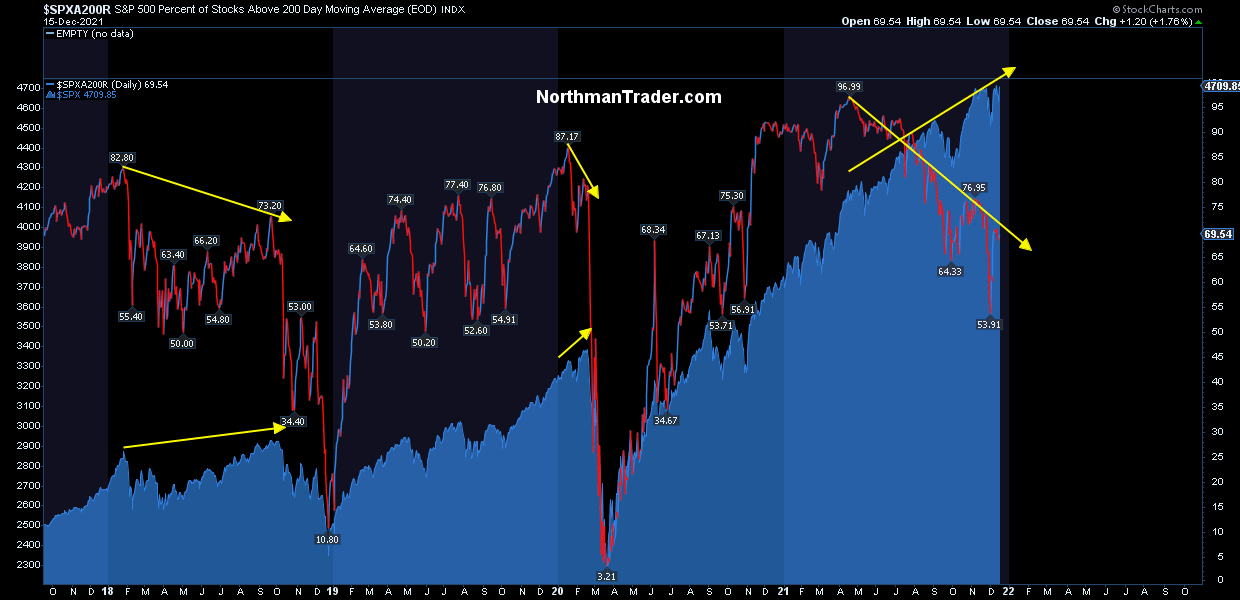

30% are below their 200 day moving average the weakest reading this year yet reflecting a trend that began early in the year.

Indeed it was in February when the Spac and ARKK craze peaked. Many IPos this year such as $HOOD are trading disaster zones seeing early buyers getting absolutely crushed.

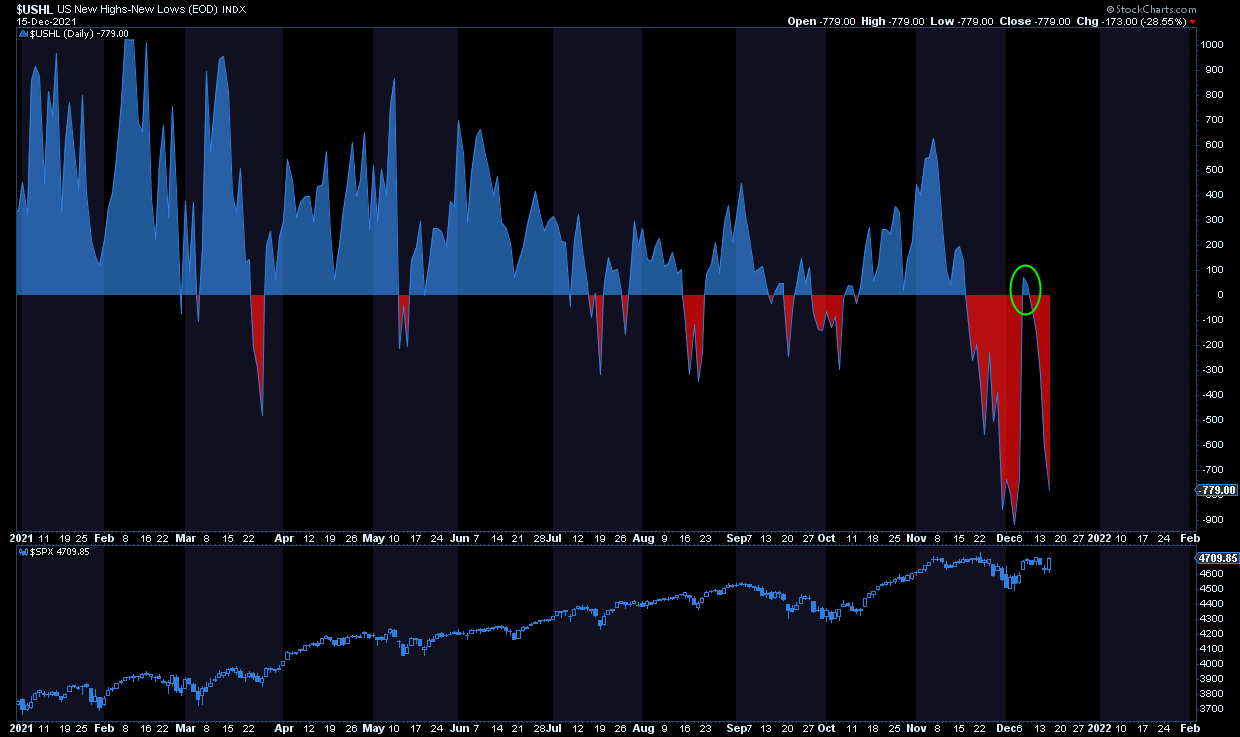

New highs/new lows perhaps best reflect the bleeding beneath:

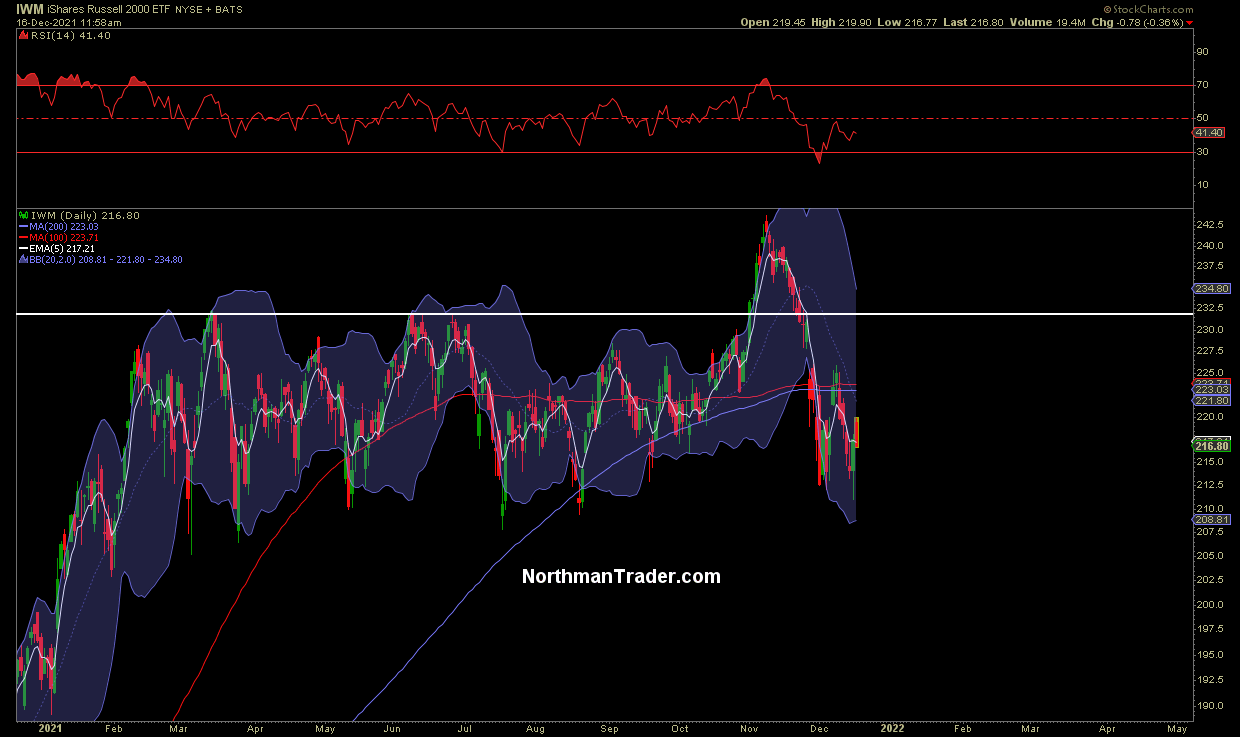

And small caps also reflect how poor 2021 has actually traded for most stocks:

A massive fake break out in November, now a bunch of trapped supply above.

It is no wonder then that Fund performance is exactly far from impressive:

GOLDMAN: “.. just 32% of large cap mutual funds have beat their respective style benchmarks YTD .. long/short hedge funds have fared no better, with the typical fund posting a flat YTD return according to Goldman Sachs Prime Brokerage compared with +23% for the S&P 500.” pic.twitter.com/AJzejCFfYr

— Carl Quintanilla (@carlquintanilla) December 6, 2021

So I submit the notion of a raging bull market is a myth. Indices propelled to constant new highs by still flowing central bank liquidity increasingly held together by a few stocks.

Yes, mark it up all you want, but accelerated taper is coming in January, profit motive will see people locking in gains on the winners and the end of QE will bring about a larger asset correction as it always does:

And that’s when Powell will cave as he always does and then markets can rally again.

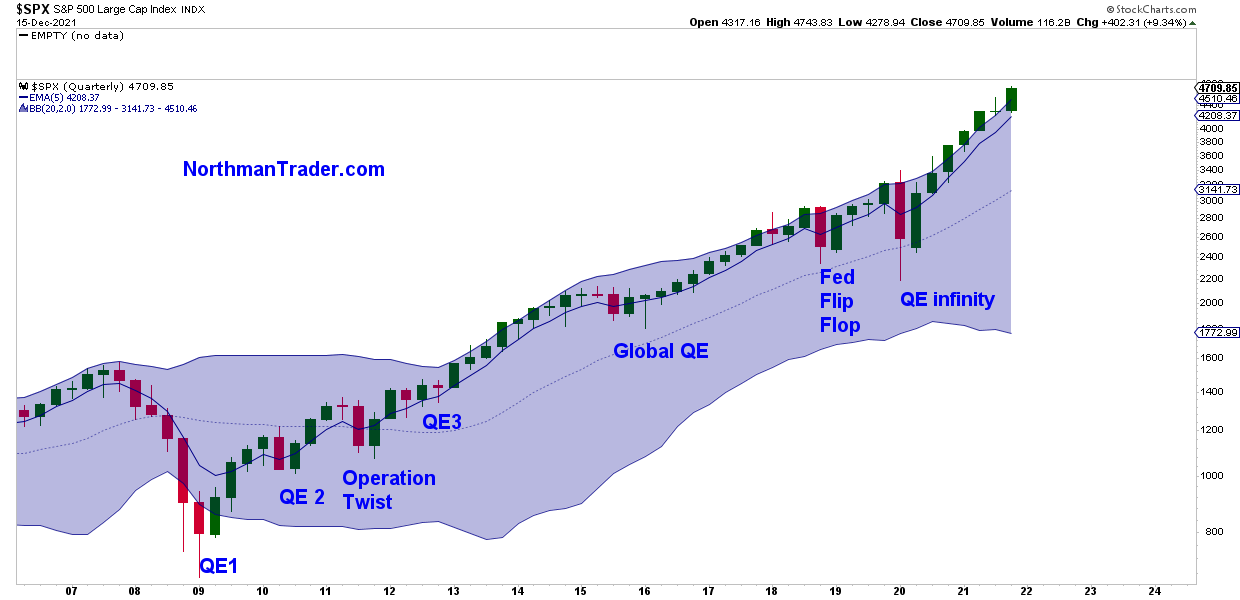

But keep a close eye on this chart. Not only do prices remain far outside the historical resistance of the upper quarterly Bollinger band, $SPX also remains far above its quarterly 5 EMA. A chart that demands its eventual technical reconnect, a process many of its components have already undertaken.

My view here: Powell made a mistake with transitory, he made a mistake with printing too much for too long, and now he’s making a mistake with being too beholden to markets vis a vis what the needed policy response is.

As he said himself: “If expectations were to begin to drift, the reality or expectation of a weak initial response could exacerbate the problem.”

And that’s it right there. The Fed is exacerbating the problem and that will force their hand in 2022 and Powell will come to regret continuing to suck up to the market. 2022 will again become a giant gaming exercise to anticipate what the Fed may or may not do and when the Fed will again cave to market pressure.

But be clear: A market that has been proven to be entirely dependent on Fed’s balance sheet expanding will have to contend with the Fed balance sheet suddenly no longer expanding. A market that now sees $11 trillion in market cap tied up in just 6 stocks is walking an extremely narrow path that can lead to a much larger unraveling then what the broader market has already begun to do. Lagging funds may want to performance chase into the end of year, but the game is changing, the valuations are still astronomical, and dare I say: Given the absolute disastrous performance in the majority of individual stocks bears were absolutely correct to warn of chasing into unrealistic valuations. Unfortunately many individual investors are now not only paying the price of inflation run hot by a stubborn Fed, they now also pay the price with major drawdowns in stocks.

Bull market in indices, bear market in stocks and liquidity injections coming to an end. 2022 will be interesting.

* * *

On a final note: If you want to stay updated with what’s happening in markets I’m discussing ongoing technical developments in markets and crypto on a regular basis in the NorthCast and you are welcome to follow there (it’s free). For the latest public analysis please visit NorthmanTrader and the NorthCast. To subscribe to our directional market analysis please visit Services.

Tyler Durden

Thu, 12/16/2021 – 15:21

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com