Futures Resume Levitation, Push On To New All Time Highs

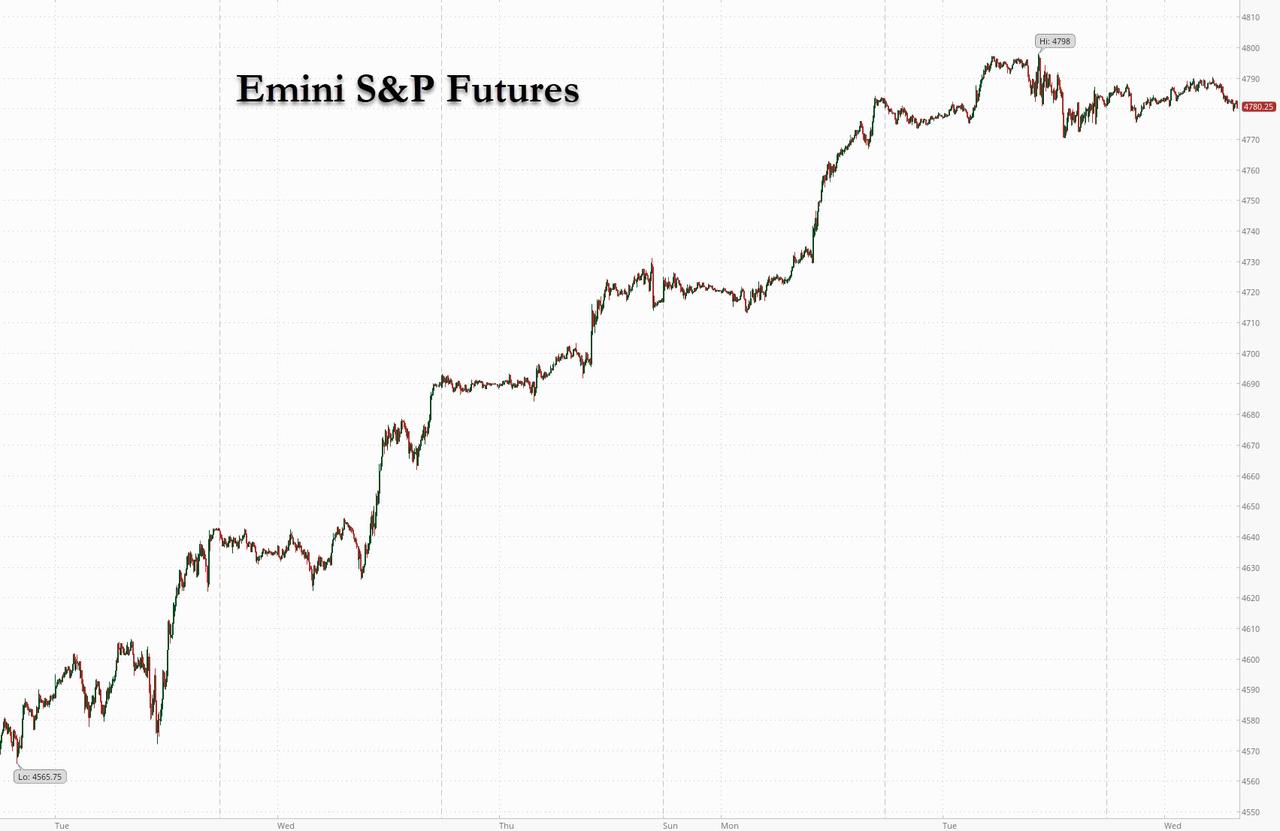

One day after a brief interruption in the Santa rally, as US stocks fell for the first time in five days amid a rotation out of megacap tech shares, futures have resumed their upward climb as investors brushed aside rapidly shifting fears about the economic implications of the omicron coronavirus outbreak. Treasury yields ticked higher along with the dollar. Bitcoin continued its recent tax-loss related selling which pushed it back under $47,000. As of 730am ET, emini S&P futures were up 2 points or 0.04%, fading an earlier gain which pushed ES up to 4,790, while Dow Jones futures were flat and Nasdaq futures were up 0.16%.

Tesla gained more than 2% in pre-market trading after Elon Musk sold a further $1.02 billion off shares, taking him that much closer to his target of reducing his stake in the electric-car maker by 10%. Other notable premarket movers include:

- Shares in Apple (AAPL US) rise 0.2% in premarket trading after it closed lower on Tuesday after a four-day rally that put it within striking distance of a historic $3 trillion market value

- Calix (CALX US) climbed 8.9% in extended trading on news the software company will join the S&P Midcap 400 Index before trading opens on Jan. 4

- Chembio Diagnostics (CEMI US) sank 22% postmarket after saying the FDA declined to review the company’s application for an emergency use authorization (EUA) for its DPP Respiratory Antigen Panel — a test for coronavirus and influenza

- Cal-Maine Foods Inc. (CALM US) fell 7.1% in after- hours trading as the egg producer posted 2Q profit that missed the average analyst estimate

Shares slipped in Japan, technology stocks drove a retreat in Hong Kong and China slid (more below). Sentiment in China is being sapped by Beijing’s tightening oversight of overseas share sales and economic risks from a property slowdown. Authorities are expected to add stimulus next year to steady expansion.

In the latest Omicron news, two years after reports of the mysterious disease first emerged in Wuhan, the pandemic shows no signs of abating, with the omicron variant pushing worldwide Covid-19 cases above 1 million for a second straight day. The Netherlands will require travelers arriving from the U.S. to self-quarantine for up to ten days. Rapid tests that are widely used to detect infections may miss some omicron cases, according to the U.S. Food and Drug Administration. Covid hospitalizations are spiking from New South Wales to New York state, pressuring health systems. Overall, however, omicron appears to be triggering a lower rate of hospitalizations. In China’s Xi’an, an outbreak eased after residents were asked to stay indoors and driving was banned.

“Although omicron cases in the U.S. and Europe amongst others, continue to surge, it has yet to make its presence felt negatively in economic data,” Jeffrey Halley, a senior market analyst at Oanda, said in a note. “With market activity much reduced for the holiday season, investors continue to tentatively price in a global recovery hitting a minor bump, and not a pothole.”

As Bloomberg notes, investors are rounding out the year by booking profits after a 17% jump in global equities. The coronavirus, Federal Reserve policy tightening and China’s outlook are cited among the key risks for 2022. Omicron fears are easing on growing evidence that the fast-spreading strain leads to milder symptoms. Still volatility remains with the Nasdaq now swinging more than 2.5% per week for 5 consecutive weeks, the longest stretch in a decade.

“We’re sober about potential headwinds that still could be coming, even the rest of this year, but early in 2022 — the Fed is going to be raising rates, that will change things for the markets,” Ann Miletti, head of active equity at Allspring Global Investments, said on Bloomberg Television. “We are also hopeful because as you look at a lot of the economic data, it remains strong.”

In Europe, the Stoxx Europe 600 index hit a new all-time high record before retreating, with retailers outperforming. The FTSE 100 Index climbed to its highest level since February 2020 as U.K. markets reopened after Christmas, catching up to European market gains, with the FTSE 100 Index rising to the highest level since February 2020. The FTSE 100 Index was up as much as 1% with Rolls-Royce the best performer with a 3% gain; the FTSE 250 Index gained as much as 1.3%; Darktrace jumps 5.1%. Technology shares declined, following the sector’s retreat in the U.S. and Asia. Volumes remained thin into the end of the year in some markets.

Earlier in the session, Asian stocks fell, led by losses in Chinese shares, amid an extended global selloff in technology giants. The MSCI Asia Pacific Index slid as much as 0.5%, with Samsung Electronics, Alibaba and Tencent among the biggest drags. China’s CSI 300 was the worst-performing major gauge in the region, losing 1.5%.

“There’s not much news, but the drop in Chinese shares has worsened the mood a bit,” said Tetsuo Seshimo, a fund manager at Saison Asset Management. “It’s almost strange how equity markets have been rising despite this sense of anticipated cutbacks in monetary easing by Europe and the U.S., so you’re seeing stocks correct recent gains.” U.S. stocks fell for the first time in five days amid a rotation out of megacap tech shares. While some traders saw a chance to take profits after the S&P 500 posted its 69th record-high close for 2021 on Monday, the market also remains wary over record numbers of daily Covid-19 cases. “I think the most pressing issue is omicron and whether or not surging case numbers lead to a pick-up in hospitalizations and fatalities in coming weeks,” said Kyle Rodda, a market analyst at IG Markets. “That could pull the rug from under the market, especially as trading conditions return to normal from next week onwards.”

Japanese equities also slid as investors sold technology shares, mirroring moves in the U.S. market overnight. Electronics makers were the biggest drag on the Topix, which fell 0.3%. Tokyo Electron and Fast Retailing were the largest contributors to a 0.6% loss in the Nikkei 225.

India’s key stock gauges likewise fell after a two-day advance, led by declines in lenders. Dr. Reddy’s Laboratories and Sun Pharmaceutical rose after the government approved more vaccines and treatments to curb the spread of coronavirus. The S&P BSE Sensex fell 0.2% to 57,806.49 in Mumbai, after swinging between gains and losses ahead of the expiry of monthly derivative contracts on Thursday. The NSE Nifty 50 Index slipped 0.1%. Twelve of the 19 sector sub-gauges compiled by BSE Ltd. fell, led by a measure of metals companies. The government on Tuesday granted approval for restricted emergency use of two new vaccines and the anti-viral drug Molnupiravir, to be manufactured by local firms including Dr. Reddy’s. India recorded 9,195 new Covid-19 cases, according to the latest data release on Wednesday. The daily count surged from 6,358 on Tuesday. Rising infections have prompted some Indian states to impose curbs on public gatherings, with New Delhi ordering closures of cinemas, schools and gyms. HDFC Bank contributed the most to the Sensex’s decline, falling 0.5%. Out of 30 shares in the benchmark, 18 fell and 12 rose.

In rates, Treasuries slipped in light trading as equity futures hold near Tuesday’s record high, with the year’s last auction – a sale of $56 billion in 7-year paper due at 1pm ET, in low-volume trading typical of the last week of the year. Yields are higher cheaper by 1bp-2bp in 10- to 30-year sectors with front-end and belly yields little changed; 30-year at 1.917% is above its above its 50-DMA, breached Tuesday for first time since late November. Monday’s 2-year and Tuesday’s 5-year auctions tailed slightly, though both have since improved and sported solid internals. The WI 7Y yield ~1.42% is between last two auction stops and ~16bp richer than last month’s. Euro-area sovereign bonds were mixed, with German bunds fluctuating. Japanese government bonds gained as concern over the coronavirus omicron strain supports demand for haven assets.

In FX, a gauge of the U.S. dollar rose for a third day, sending the Japanese yen sliding past 115/USD for the first time in a month. The Turkish lira resumed its collapse, dropping as much as 5% against the dollar, extending this week’s loss to 15% with the nation’s 10-year government bond yield standing at an all-time high. Turkey’s central bank will prioritize the promotion of lira deposits next year after President Recep Tayyip Erdogan announced controversial new steps to curb the currency’s depreciation. Meanwhile, China’s overnight interbank borrowing rates plummet to the lowest level in 11 months after the central bank injected more liquidity into the financial system.

In commodities, crude oil hovered near a one-month high, partly on bets that the global recovery can ride out omicron. Iron ore futures in Singapore and China declined for a third day. Bitcoin stayed below $48,000 after a tumble that hinted at diminished ardor for the most speculative assets; the cryptocurrency remains on course for its biggest monthly drop since the cryptocurrency rout in May.

Market Snapshot

- S&P 500 futures up 0.2% to 4,788.25

- STOXX Europe 600 up 0.2% to 489.63

- MXAP down 0.4% to 192.40

- MXAPJ down 0.3% to 625.02

- Nikkei down 0.6% to 28,906.88

- Topix down 0.3% to 1,998.99

- Hang Seng Index down 0.8% to 23,086.54

- Shanghai Composite down 0.9% to 3,597.00

- Sensex little changed at 57,920.29

- Australia S&P/ASX 200 up 1.2% to 7,509.81

- Kospi down 0.9% to 2,993.29

- Brent Futures little changed at $78.95/bbl

- Gold spot down 0.1% to $1,803.78

- U.S. Dollar Index up 0.17% to 96.37

- German 10Y yield little changed at -0.23%

- Euro down 0.3% to $1.1279

Top Overnight News from Bloomberg

- Investors are primed for the dollar to climb next year. But the juiciest trades may be over even before 2021 ends

- The Bloomberg Dollar Index is racing toward its best annual gain in six years and hedge funds’ net long bets on the currency have climbed to the highest since June 2019 as traders have been front-running a hawkish Federal Reserve

- European equities climbed toward a record in thin holiday trading as investors bet that the economic recovery can withstand the impact of the omicron variant

- Bitcoin edged higher after a steep decline in choppy year-end trading, but it’s still on course for its biggest monthly drop since the cryptocurrency rout in May

- U.K. households are heading into the “year of the squeeze” as surging energy bills and faster inflation eat into incomes, according to the Resolution Foundation think tank

US Event Calendar

- 8:30am: Nov. Advance Goods Trade Balance, est. -$88.1b, prior – $82.9b

- 8:30am: Nov. Retail Inventories MoM, est. 0.5%, prior 0.1%; Wholesale Inventories MoM, est. 1.5%, prior 2.3%

- 10am: Nov. Pending Home Sales YoY, prior -4.7%; Pending Home Sales (MoM), est. 0.8%, prior 7.5%

Tyler Durden

Wed, 12/29/2021 – 08:11

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com