Fed-Driven Housing Mania Sends Average Homebuyer Loan Size To Record High

A new report by the Mortgage Bankers Association (MBA) caught our eye by highlighting an unfortunate reality of low-interest rates: while they initially make homebuying affordable for middle- and working-class Americans, cheap money flooding into the market for an extended period will cause housing affordability issues as home prices soar.

Data from MBA shows that’s happening as home price appreciation since the beginning of the virus pandemic has been due to low-interest rates and tight housing inventory, creating some of the fastest home price growth spurts in decades. Many homebuyers chased prices in fierce bidding wars, as they took on the largest average purchase loan sizes on record.

“Prospective buyers still face elevated sales prices in addition to higher mortgage rates. The heavier mix of conventional applications again contributed to another record average loan size at $453,000,” said Joel Kan, an MBA economist.

In a separate report, CoreLogic shows home prices climbed across the country as demand outstripped supply. In December, prices nationally jumped 18.5% year over year, one of the fastest increases in years. The housing boom is at an infection as buyers take on too much debt, many are priced out of markets, and others are forced to rent because of affordability issues.

When it comes to first-time homebuyers, the National Association of Realtors said their mortgage payments in the fourth quarter jumped to 25.6% of their household incomes, the highest in three years and up 3.2 percentage points from the same quarter last year. Homebuyers generally follow the 28/36 rule, a personal finance guide that limits how much money should go to housing costs and monthly debt payments, shouldn’t exceed 28% of a household’s monthly pre-tax income and 36% of total debt; this is also known as the debt-to-income ratio. The increase in debt service payments was mainly due to homebuyers purchasing homes at record high prices and locking in mortgage rates at higher levels.

As average mortgage debt size swells to most on record and housing affordability becomes a significant issue, the Federal Reserve is well aware the housing market is in a bubble. St.Louis Fed president Jim Bullard went full hawktard last week after the Biden White House appears to have greenlit The Fed to crash the economy:

FED’S BULLARD FAVORS 100 BPS INTEREST-RATE INCREASES BY JULY 1

BULLARD FAVORS FIRST HALF-POINT U.S. RATE INCREASE SINCE 2000

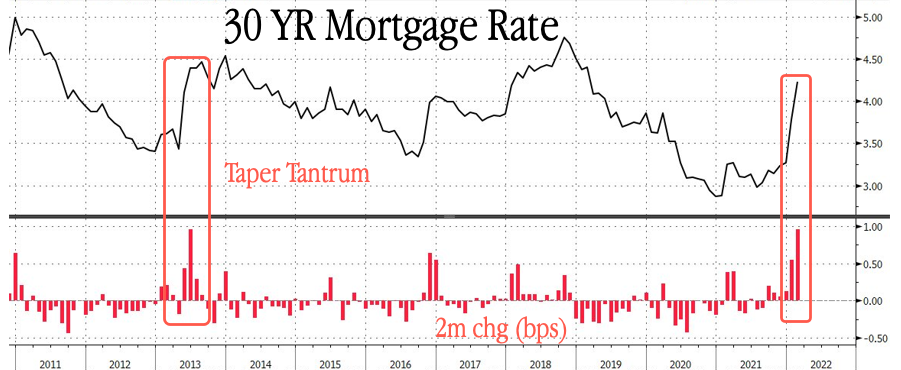

Bullard’s hawkish statements come as mortgage rates topped 4.23% on Wednesday and have experienced the most significant multi-month increase since the taper tantrum days of 2013.

Today’s inflationary environment is very different than 2013. Inflation is a four-decade high as the Fed has little wiggle room to fold, which could mean, unlike 2013, housing prices may experience a correction. However, a silver lining for prospective homebuyers as the Fed embarks on an aggressive rate hike cycle is that institutional investors (who’ve dominated real estate markets for years) will have funding challenges as the short end of the yield curve rapidly rises in sync with interest rates. A correction in home prices and the possibility of diminished demand from institutional investors could finally give first-time homebuyers a fighting chance at a good deal.

Now rounding back to all those folks who took out record mortgage debt and chased home prices to record highs, well, if history serves, it took people from the Dot Com boom at least a decade to break even.

Tyler Durden

Thu, 02/17/2022 – 05:45

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com