Buffett Praises Apple As One Of Berkshire’s “Four Giants” In Latest Annual Letter

The “Oracle of Omaha” Warren Buffett published his 57th annual letter to Berkshire Hathaway shareholders on Saturday, and in it he proclaimed that Apple – which Berkshire finally bought in 2016, overcoming its decades-long aversion to consumer tech – had become one of “our four giants” responsible for the firm’s continuing prosperity.

The firm recorded more than $90 billion in net earnings during 2021, with nearly $40 billion of those coming during Q4 alone.

Buffett used the “giants” theme to great effect in his latest letter. And while he praised Apple at No. 2, much of Berkshire’s success is due to the company’s No. 1 “giant”, its “cluster of insurance operations”, which includes GEICO, MedPro, National Indemnity, etc., and generates a massive cash “float” that is now worth more than $147 billion.

Nevertheless, operations of our “Big Four” companies account for a very large chunk of Berkshire’s value. Leading this list is our cluster of insurers. Berkshire effectively owns 100% of this group, whose massive float value we earlier described. The invested assets of these insurers are further enlarged by the extraordinary amount of capital we invest to back up their promises.

The insurance business is made to order for Berkshire. The product will never be obsolete, and sales volume will generally increase along with both economic growth and inflation. Also, integrity and capital will forever be important. Our company can and will behave well.

There are, of course, other insurers with excellent business models and prospects. Replication of Berkshire’s operation, however, would be almost impossible.

But at No. 2, Apple has performed tremendously, and Buffett credited CEO Tim Cook for protecting the company’s dominant position as one of the world’s most valuable enterprises. Apple also paid Berkshire $785 million in dividends last year alone:

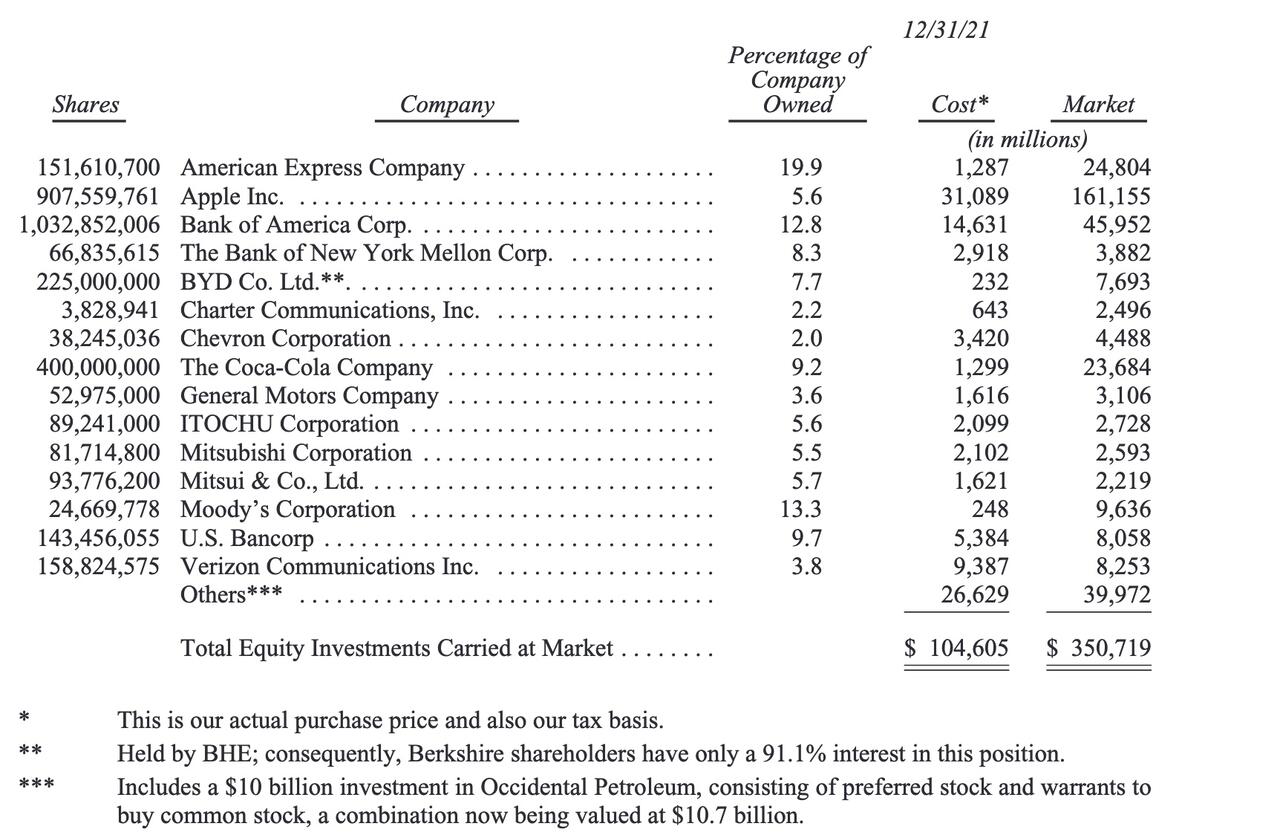

Apple – our runner-up Giant as measured by its yearend market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier. That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job.

It’s important to understand that only dividends from Apple are counted in the GAAP earnings Berkshire reports – and last year, Apple paid us $785 million of those. Yet our “share” of Apple’s earnings amounted to a staggering $5.6 billion. Much of what the company retained was used to repurchase Apple shares, an act we applaud. Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well.

Giants No. 3 and No. 4 were Berkshire’s freight rail business, BNSF…

BNSF, our third Giant, continues to be the number one artery of American commerce, which makes it an indispensable asset for America as well as for Berkshire. If the many essential products BNSF carries were instead hauled by truck, America’s carbon emissions would soar.

Your railroad had record earnings of $6 billion in 2021. Here, it should be noted, we are talking about the old-fashioned sort of earnings that we favor: a figure calculated after interest, taxes, depreciation, amortization and all forms of compensation. (Our definition suggests a warning: Deceptive “adjustments” to earnings – to use a polite description – have become both more frequent and more fanciful as stocks have risen. Speaking less politely, I would say that bull markets breed bloviated bull . . ..)

BNSF trains traveled 143 million miles last year and carried 535 million tons of cargo. Both accomplishments far exceed those of any other American carrier. You can be proud of your railroad.

…and BHE, Berkshire’s energy business.

BHE, our final Giant, earned a record $4 billion in 2021. That’s up more than 30-fold from the $122 million earned in 2000, the year that Berkshire first purchased a BHE stake. Now, Berkshire owns 91.1% of the company.

BHE’s record of societal accomplishment is as remarkable as its financial performance. The company had no wind or solar generation in 2000. It was then regarded simply as a relatively new and minor participant in the huge electric utility industry. Subsequently, under David Sokol’s and Greg Abel’s leadership, BHE has become a utility powerhouse (no groaning, please) and a leading force in wind, solar and transmission throughout much of the United States.

Here are some other key points outlined in the letter.

Berkshire’s cash position:

Berkshire’s balance sheet includes $144 billion of cash and cash equivalents (excluding the holdings of BNSF and BHE). Of this sum, $120 billion is held in U.S. Treasury bills, all maturing in less than a year. That stake leaves Berkshire financing about 1⁄2 of 1% of the publicly-held national debt.

Charlie and I have pledged that Berkshire (along with our subsidiaries other than BNSF and BHE) will always hold more than $30 billion of cash and equivalents. We want your company to be financially impregnable and never dependent on the kindness of strangers (or even that of friends). Both of us like to sleep soundly, and we want our creditors, insurance claimants and you to do so as well.

Taxes:

Every year, your company makes substantial federal income tax payments. In 2021, for example, we paid $3.3 billion while the U.S. Treasury reported total corporate income-tax receipts of $402 billion. Additionally, Berkshire pays substantial state and foreign taxes. “I gave at the office” is an unassailable assertion when made by Berkshire shareholders.

Berkshire’s history vividly illustrates the invisible and often unrecognized financial partnership between government and American businesses. Our tale begins early in 1955, when Berkshire Fine Spinning and Hathaway Manufacturing agreed to merge their businesses. In their requests for shareholder approval, these venerable New England textile companies expressed high hopes for the combination.

The Hathaway solicitation, for example, assured its shareholders that “The combination of the resources and managements will result in one of the strongest and most efficient organizations in the textile industry.” That upbeat view was endorsed by the company’s advisor, Lehman Brothers (yes, that Lehman Brothers). I’m sure it was a joyous day in both Fall River (Berkshire) and New Bedford (Hathaway) when the union was consummated. After the bands stopped playing and the bankers went home, however, the shareholders reaped a disaster.

In the nine years following the merger, Berkshire’s owners watched the company’s net worth crater from $51.4 million to $22.1 million. In part, this decline was caused by stock repurchases, ill-advised dividends and plant shutdowns. But nine years of effort by many thousands of employees delivered an operating loss as well. Berkshire’s struggles were not unusual: The New England textile industry had silently entered an extended and non-reversible death march.

During the nine post-merger years, the U.S. Treasury suffered as well from Berkshire’s troubles. All told, the company paid the government only $337,359 in income tax during that period – a pathetic $100 per day.

As far as profits were concerned, 2021 was a blockbuster year for Buffett and Berkshire. The firm’s shares managed to outperform the S&P 500, booking a 29.6% gain, compared with 28.7% for the S&P 500 (with dividends included). That’s a much better showing than the prior year (2020), where Berkshire shares notched a gain of just 2.4%, compared with more than 18% for the S&P 500 (again, with dividends).

Berkshire’s Q4 net earnings increased to $39.65 billion, or $26,690 per Class A share equivalent, up from $35.84 billion, or $23,015 per share, during Q4 2020. Operating earnings, which exclude some investment results, rose to $7.29 billion from $5 billion a year before. Net earnings increased 11% due to gains from Berkshire’s investment portfolio.

2021 was a quiet year for Berkshire in terms of deal flow: no major acquisitions were announced, although the firm remained an active buyer of its own shares, spending $51.7 billion on repurchases over the past two years. As of Feb. 23, Berkshire had spent another $1.2 billion on buybacks this year, as Buffett again insisted that the firm’s appetite for its own shares will remain “price dependent”.

As for the firm’s annual meeting, that will begin Friday April 29 and continue through May 1.

Readers can find the full letter below:

2021ltr on Scribd

Tyler Durden

Sat, 02/26/2022 – 10:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com