Macleod: The End Of Fiat Is Hoving Into View…

Authored by Alasdair Macleod via GoldMoney.com,

Tragic though the situation in Ukraine has become, the real war which started out as financial in character some time ago has now become both financial and about commodities. Putin made a huge mistake invading Ukraine but the West’s reaction by seeking to isolate Russia and its commodity exports from the global marketplace is an even greater one.

Furthermore, with Ukraine being Europe’s breadbasket and a major exporter of fertiliser, this summer will bring acute food shortages, worsened by China having already accumulated the bulk of the world’s grains for its own population. Inflation measured by consumer prices has only just commenced an accelerated rise.

Because they discount falling purchasing power for currencies, rising interest rates, and collapsing bond prices are now inevitable. Being loaded up with bonds and financial assets as collateral, the consequences for the global banking system are so significant that it is virtually impossible to see how it can survive. And if the banking system faces collapse, being unbacked by anything other than rapidly disappearing faith in them fiat currencies will fail as well.

Unforeseen financial and economic consequences

Back in the 1960s, Harold Wilson as an embattled British Prime Minister declared that a week is a long time in politics. Today, we can also comment it is a long time in commodity markets, stock markets, geopolitics, and almost anything else we care to think of. The rapidity of change may not be captured in just seven calendar days, but in recent weeks we have seen the initial pricking of the fiat currency bubble and all that floats with it.

This is turning out to be an extreme financial event. The background to it is unwinding of economic distortions. Through a combination of currency and credit expansion and market suppression, the difference between state-controlled pricing and market reality has never been greater. Zero and negative interest rates, deeply negative real bond yields, and a deliberate policy of artificial wealth creation by fostering a financial asset bubble to divert attention from a deepening economic crisis in recent years have all contributed to the gap between bullish expectations and market reality.

Today, almost no one thinks that our blessèd central banks and their governments can fail, let alone lose control over markets. And if you walk like a Keynesian, talk like a Keynesian you are a Keynesian. Everyone does — even the gait of mathematical monetarists is indistinguishable from them in their support of inflationism. And Keynesians believe in the state theory of everything, despising markets and now fearing their reality.

This week sees growing concerns that American-led attempts to kick Putin’s ass comes with consequences. Put to one side the destruction wreaked on the Ukrainian people as the two major military nations wage yet another proxy war. This one is in Europe’s breadbasket, driving wheat prices over 50% higher so far this year. Having laid waste over successive Arab nations since Saddam Hussein invaded Kuwait in 1990, the people who have survived American-led wars in the Middle East and North Africa and not emigrated as refugees are now going to face starvation.

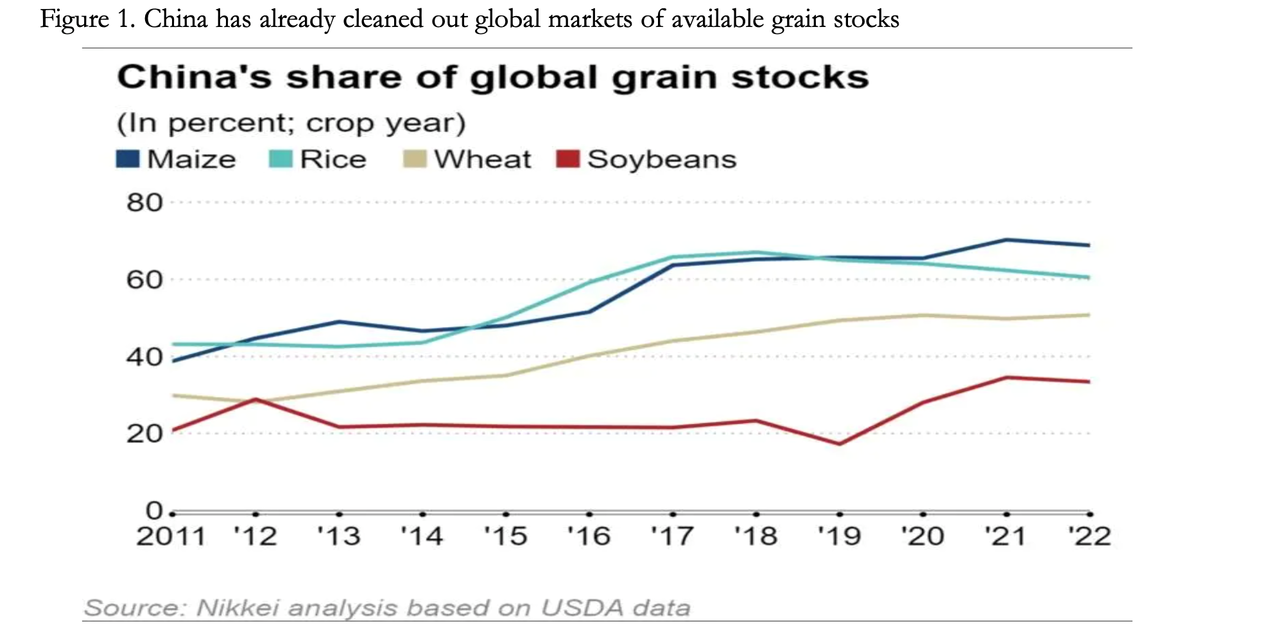

Fuelled by the expansion of currency and credit, it is not just wheat prices which are soaring. Other foodstuffs are as well. And we learn through various sources that the Chinese have been prescient enough to stockpile enormous quantities of grains and other comestible materials to protect their citizens from a summer food crisis. Twenty per cent of the world’s population has secured more than half the globe’s maize and other grains (Nikkei Asia, 23 December – see Figure 1). And that was two months before Putin ordered the invasion of Ukraine, which has made the position over global food supplies even worse. And China’s dominant position in maize will hit sub-Saharan Africa especially hard, while global shortages of rice will hit Southern and East Asian nations.

All we need now is crop failures. Speaking of which, fertiliser shortages, exacerbated by the Ukraine war and high gas prices, are bound to affect global food production adversely for this year’s harvest. And well done to our elected Leaders for imposing sanctions on Russian exports of fertiliser, which added to China’s conservation of its supplies will ensure our poor, and everyone else’s poor, face soaring food prices and even starvation in 2022.

Yet, few seem aware of this developing crisis. While Ukraine is an obvious factor driving up food and energy prices, the root cause has been and will continue to be monetary policies driving the leading currencies. History is littered with examples of currency debasement leading to a food crisis and civil unrest: the Emperor Diocletian’s edict controlling prices in 301AD; coin debasement leading to soaring food prices in 1124AD at the time of England’s Henry I; the collapse of John Law’s livre in 1720 France, to name but a few.

From the dollar as the reserve currency, to euros, yen, pounds, and the rest, all of them have been debased in what used to be called the civilised world. And an understanding of money and the empirical evidence both point to a consequential food crisis this summer.

How will we pay for the higher prices? Well, no one need go without, because it will be a Keynesian designated slump. And the authorities will be onto it. Your central bank will simply issue more currency and you might even get some helicoptered to you. Price controls will prove irresistible to our leaders, and just as Diocletian penalised butchers and bakers who raised their prices under pain of death, today’s providers of life’s essentials will be accused of profiteering and taxed accordingly.

And how do we ensure our lifestyles will be not undermined? We can borrow more to pay for cars and holidays. And how do we ensure we preserve our wealth? Your central bank will suppress interest rates to keep stock markets bubbling.

It is, in essence, a trick played on us all by using fiat currency masquerading as traditional money. The risk is that the investing public, and then the public on Main Street, will twig it. First the financial asset bubble pops and then we will be unable to feed ourselves. Those who vaguely see the danger by projecting known factors think that decline is a gradual process. The mistake they make is a human element, which results in unforeseen consequences in the form of a sudden financial and economic crisis.

This article is about the approaching financial and banking crises, which we can now say will likely overwhelm us sooner rather than later. We start with a reality check on the current state of the commodity, financial and economic war. That is raging now, and it will almost certainly destabilise the current world order. And the consequences for interest rates will require the entire global financial system to be recapitalised, starting with the central banks.

The developing commodity and financial crisis

If Putin had stuck to his original objective of driving a wedge between Europe and America, he would have been able to push up natural gas prices in Western Europe without resorting to any other economic weapons. Events have dictated otherwise. And now America in kick-ass mode has united its NATO European members to drive up energy prices beyond Europe and food prices globally by proscribing all financial payments with Russia. The wider economic concern is that soaring commodity, energy, and food prices will lead to a worldwide slump.

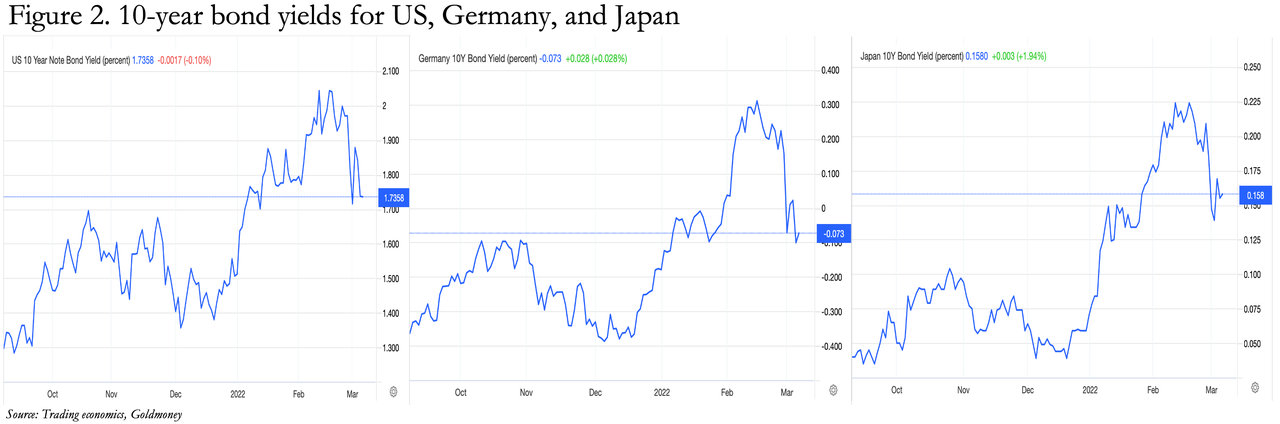

Driven by an initial flight by investment funds away from risk towards safety, bond yields were initially driven lower from recent highs. Figure 2 shows how bond yields for the 10-year bonds in America, Germany, and Japan had declined from recent peaks earlier this week.

Though yields have risen slightly since, these declines were something of a lifeline for the Fed, ECB, and BOJ, and it would be convenient for them if they were to stabilise at current levels. It fits their preferred narrative, which is that inflation, by which they mean rising consumer prices, is fuelled by temporary factors which will diminish in time. And when Putin is forced to give up his aggression against Ukraine, prices will normalise.

Western policy planners see signs that their economies are being undermined by these developments and expect the outlook will change from inflation to recession. Therefore, central bankers and economists are beginning to think that to raise interest rates would prove to be an error of policy which could drive a mild recession into a possible slump.

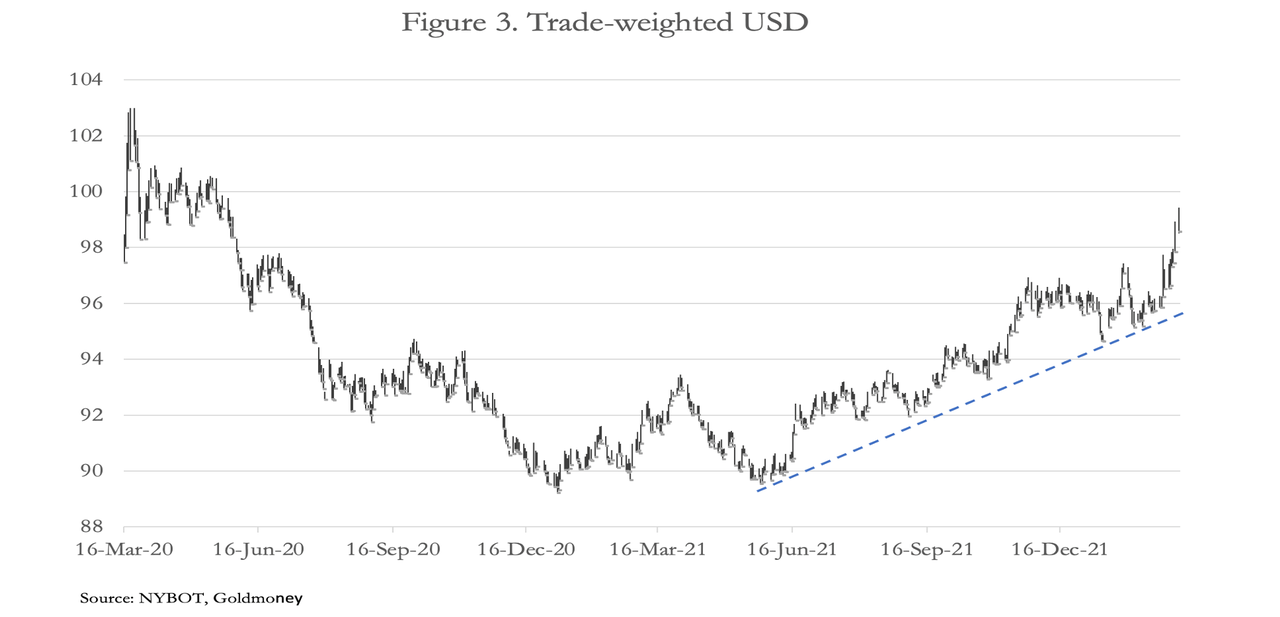

Currencies are also affected by the flight to safety. The conventional view is that the safest currency is the dollar, and that has rallied sharply, as shown in Figure 3.

But it should be noted that foreign ownership is already heavily skewed into US dollars and US dollar assets. According to the latest US Treasury TIC figures, Long-term and short-term securities and bank deposits owned by foreigners totalled $34 trillion last December. This represents about 150% of US GDP and has almost certainly risen further since.

By any measure, the US dollar is over-owned by foreigners.

The current wave of foreign currency deposits fleeing into dollars is storing up trouble for the dollar in future, because they either represent inefficiently deployed liquidity for foreigners accounting in other currencies or they are invested in over-valued financial assets. But for now, not only is the dollar the king of currencies, but the proximity of the Eurozone to Ukraine and the commercial links to Eastern Europe in the wider sense undermines confidence in the euro. The euro is the largest component of the dollar’s trade-weighted index in Figure 3 above.

But the flight to safety in currencies and bonds is a temporary step driven by investors in thrall to Keynesian macroeconomics. Having been educated exclusively in Keynesianism they lack an understanding of gold and its monetary role. When freely exchangeable for gold coin, only then does a currency take on gold’s monetary qualities. It has been eighty-nine years since the dollar enjoyed this status, and for the last fifty-one years it has been totally fiat, taking all other currencies off gold with it. In fact, the temporary suspension of the Bretton Woods agreement has been replaced with American anti-gold propaganda in to secure dollar hegemony.

The few people who both understood money as opposed to fiat currencies and manage financial assets have long since retired. All currencies are now state-issued fiat, vulnerable to a schism between their purchasing power and that of gold. The escape from these unsound characteristics will undoubtedly be into metallic money, that is gold and silver, when public confidence in fiat finally disappears. That is not yet the current situation.

Russia’s central bank will be considering its position

The position in Russia is contrastingly different. Over the last two years its M2 money supply has increased by 27% compared with 41% for the dollar. The rouble has not been driven down so much by inflationary policies but by an external threat to it. This has led to cash withdrawals from their bank accounts by middle-class Russians, reflecting an erosion of domestic confidence in the commercial banks. On the foreign exchanges, the rouble has almost halved against the dollar. The Russian Central Bank will be considering its reserves policy, beyond its initial response of raising interest rates to 20% and imposing restrictive foreign exchange controls.

Of the RCB’s total foreign reserves, about $500bn equivalent is in foreign currencies and $130bn is in gold. Sanctions against it have rendered the foreign currency element valueless, at least so long as sanctions are enforced. The difference between fiat currency and gold has been clearly demonstrated. Only physical gold reserves, which have no counterparty risk, has any value to the Russian state. The question now faced by the RCB is how to stabilise the currency and return public confidence in it.

It has some high-value cards in its hand. The run on the banks is likely to diminish in time and the rouble should stabilise after the initial fall on the foreign exchanges. A period of currency stability will take the pressure off the banking system as the panic recedes. The increase in global commodity prices will go a long way towards stabilising Russia’s finances, despite Western sanctions. Russia will adapt to sanctions and find ways to export energy and raw materials. Whenever sanctions have been imposed, such as against South Africa in the apartheid years, after an initial shock the nation emerges stronger. And in the near term, labour costs have been halved relative to commodity outputs.

Meanwhile, a consequence of the failure to take Ukraine will increase the likelihood that Putin will escalate the energy and commodity crisis as a means of destabilising Russia’s Western enemies. He has been forced into a corner in this respect, and we have not yet seen his response. The intriguing question is what Russia will do about gold.

Clearly, with the bulk of its currency reserves sanctioned by the West, gold has become the stand-out asset. And if the RCB feels the need to stabilise the rouble in the longer term, then its gold reserves could be deployed to stabilise the currency and insure it against future hostilities. To advance a gold policy, the RCB might want to drive the dollar gold price higher before fixing a rate for the rouble, which would also have the effect of increasing the value of its gold reserves relative to roubles in circulation. It could do this through Asian markets, particularly the Shanghai Gold Exchange, deploying its yuan reserves.

For the moment, any such action is merely conjecture. But the consequences for the West and its dollar-based currency system would likely be to see confidence in its fiat money system undermined, making it an interesting option for Putin. Together with rising commodity and energy prices rising gold prices would draw attention to the counterparty risks faced by holders of currencies in the foreign exchanges. The West’s response is likely to be hampered by the mindset of fifty-one years of American anti-gold propaganda. And the lack of physical bullion in the US Treasury’s possession to sell into the markets could become widely suspected — this was exposed by the difficulties Germany had in getting the Federal Bank of New York to return a minor portion of its earmarked gold back in 2013.

If gold became an issue, doubtless America would apply pressure on the Europeans to supply some of their gold into bullion markets to drive the price down. But this would probably play into Putin’s hands because the European central banks, facing their own difficulties (more on this below) are unlikely to cooperate. That would drive the wedge between America and Europe, which before his mistaken invasion of Ukraine was Putin’s real objective.

Despite what might happen on gold, if interest rates in Western currencies are not permitted to rise, their purchasing power will be undermined at an increasing pace. Let it be explained for our Keynesian friends: interest rates are not the price of money, but compensation demanded by markets for expectations of a currency’s loss of purchasing power. Withhold that compensation and your currency is toast.

Recapitalising the West’s global banking system

The flight into government bonds and the dollar shown above in Figures 2 and 3 respectively is merely an initial market response seeking safety and to preserve fiat liquidity. And bond yields remaining low are consistent with unrealistic expectations that the outlook will become less inflationary and more recessionary over time. This appears to reflect hope that Putin will fail in his attack on Ukraine, and the crisis will soon be over.

A proper understanding of the crisis in prices is that they are fuelled not by war itself, but by currency debasement. Following both the Lehman failure and covid lockdowns global currency debasement in the Western partnership has been both substantial and universal, and the fallout from Putin’s war can only increase it further. Therefore, measures of inflation will not decline back towards the 2% target but increase substantially. Following the initial commodity and financial crisis, driven by market expectations interest rates are bound to rise significantly despite central bank suppression.

The effect of higher interest rates on the banking system will be materially different from past cycles. US commercial banks have not increased their lending to Main Street materially in recent years, focusing on credit creation for the financial sector and the Federal Government. According to the Fed’s H.8 Table, since 11 March 2020 (before the Fed reduced its funds rate to zero and instituted QE of $120bn per month) the expansion of bank credit in favour of securities in bank credit has increased by 32%. The increase in favour of loans and leases has been only 6%. We can assume that the cycle of bank credit in its contraction phase will be driven more by rising bond yields and collapsing stock markets than by conventional business credit contraction.

Central banks have become similarly vulnerable themselves. They have taken on the role of investors in government and agency debt, and the Bank of Japan has also accumulated equities through exchange traded funds. So not only will commercial banks suffer losses that threaten to wipe out their equity, but the major central banks face the same problem when rising interest rates getting beyond their control undermine the value of their investments. Rising interest rates mean that the entire Western banking system will need to be bailed out by a recapitalisation.

It may surprise those unfamiliar with the differences between money, currency, and credit, that new capital for a bank is always financed from its own balance sheet. In effect, temporary credit is turned into permanent capital. This is because either a deposit from an existing customer is re-allocated, or one is paid in from another bank creating a new deposit. Alternatively, and this is usually the case today, an agent is appointed to arrange subscriptions for the new capital, be it in the form of a rights issue or placing. On completion, the agent transfers subscribers’ deposits to a deposit account created for the purpose at the recapitalising bank. The deposit is then exchanged for the extra capital promised to the depositors under the terms of subscription.

Understanding the process is important. Most people would think that money or currency is involved when it never is. Bank capital is always provided out of bank credit.

A central bank raises capital by the same means but has the additional facility of creating and then redeeming its own bank notes, swapping them across its books for permanent capital. For this reason, a note issuing bank or central bank is never stuck for permanent capital. Furthermore, when you read that a bank has permanent capital of a billion dollars, most people think it is paid up in hard money. But it is an illusion funded entirely by bank credit — credit created by the bank itself.

To explain the mechanics, we can refer to how the Bank of England’s capital was increased in 1697. The Bank was founded in 1694 to act as banker to the government with an original capital of £1,200,000.

In the second half of 1696 the Bank had stopped payment due to a depositor’s run on its stocks of silver, brought about by a shortage of new coin following the Recoinage Act of January that year, and its circulating notes fell to a discount of 20% to their face value. To restore public credit in the Bank, Parliament in 1697 determined to increase the capital of the bank by £1 million (the actual figure in the Bank’s records was £1,001,171 10s[i]) but no part of the increased capital was actually paid up in money, which was silver (England was on a silver standard at that time). In pursuance of the Act £800,000 were paid in Exchequer tallies (effectively a loan issued to the Treasury by the Bank to allow the Treasury to subscribe for stock) and £200,000 in the bank’s own depreciated notes which were taken at the full value in cash. Thus, at the first increase of capital from the original £1,200,000, £200,000 of the capital consisted of its own depreciated bank notes. And the Bank was then authorised to issue its own banknotes to the amount of this portion of the increase in capital, so that the quantity of circulating banknotes remained the same.

Such are the methods by which the capital of a bank which issues notes may be increased. But the capital of a bank which does not issue notes may be increased by similar means. The essence of banking is to make advances by creating credits or deposits, and they can be used to increase its capital. The method was proved in the case of the Bank of Scotland when it increased its capital in 1727.

Suppose that a bank wishes to increase its capital and its customers wish to subscribe. In theory, they may pay in currency (that is bank notes) but today that never happens. But they can give the bank a check drawn on their account. This is the same thing as paying the bank in its own debt to subscribe for capital. It is the release of a debt owed by the bank to its customer, and that debt released then becomes a matching increase of capital. The recently agreed procedures for bank bail-ins, whereby a failing bank is recapitalised by exchanging bond obligations and large deposits for equity stock, accords entirely with these principals and is the way in which the capital of all commercial banks is increased.

Having clarified the procedures, we can now understand how the global banking system can be recapitalised and the potential difficulties.

The consequences of a mass bank recapitalisation

The recapitalisation of commercial banks which are not irretrievably bankrupt has been not uncommon in the past. For the first time, we are likely to see additional losses on central bank bond investments at all the major central banks (excepting China and Russia) which on a mark-to-market basis will wipe out their notional equity, leaving balance sheet liabilities exceeding their assets. And because this will occur as interest rates rise and bond prices fall, it is likely to occur when commercial banks need rescuing from the same effects of rising interest rates on loan collateral and their bond investments, along with the complications of the usual cyclical contraction of commercial bank credit.

In 1697 the recapitalisation of the Bank of England was to stop the run on silver coin. No specie was involved in the recapitalisation. The outward appearance of the bank’s stability was enhanced which removed the embarrassing discount on its bank notes, making them acceptable as a substitute for silver coin. Today, the objective of a mass central bank recapitalisation will be so that their credit as issuers of fiat currencies can be maintained.

The obvious concern becomes how such an exercise will affect confidence in their currencies. With the Fed, the ECB, the BOJ, and the BOE all technically bust and with no money backing them (that is physical gold), the fiat currencies they issue rely on confidence in the issuer and its currency. The losses on their bond investments from rising interest rates and the need for their recapitalisation will be synchronised by circumstances. How this plays out in terms of public confidence in financial markets and currencies for now is a matter of speculation. But we should bear in mind that while the other central banks can perform a modern version of the Bank of England’s 1697 recapitalisation, the ECB has no government treasury ministry to act as the principal counterparty.

Its shareholders are the nineteen national central banks in the euro system. Nearly all the national central banks have liabilities in excess of their assets as well or will have on just a small increase in euro-denominated bond yields. There is the further complication that through the TARGET2 settlement system some NCBs are creditors of the ECB already, and most of them owe euro credits to Germany’s Bundesbank, that of Luxembourg, Finland, and a few others.

A further concern will be about the survival of commercial banks in a higher interest rate environment. Of the expansion of commercial bank credit in the US since March 2020, the overwhelming majority has been into government and agency debt. The average balance sheet leverage of the US’s global systemically important banks (the G-SIBs) is about eleven times, so a rise in interest rates sufficient to discount the falling purchasing power of the dollar will wipe out the capital in all of these banks, even before other negative effects of a collapse of financial collateral values are accounted for.

The commercial banking networks with the highest leverage are in the Eurozone with its G-SIBs asset to equity ratios averaging over 21 times, with some considerably higher. The Japanese banks are also at about 21 times. Both the ECB and the BOJ have imposed negative interest rates, so the rise in global interest rates are bound to wipe out commercial bank capital in these jurisdictions first.

These problems are only defrayed for as long as the Keynesian establishment, including the investment community, is unaware of the consequences of currency inflation past, present, and future. When it has become clear that whatever happens in Ukraine only aggravates a situation over food, energy, and other prices with their knock-on effects we will have seen bond prices already collapsing, taking down the whole banking system from top to bottom.

Full faith and credit in fiat currencies is bound to evaporate, repeating on a global scale what happened in John Law’s France in 1720.

Tyler Durden

Sat, 03/12/2022 – 12:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com