Trucking Industry Will Be In Dire Straits If Demand Drops To Pre-COVID Levels

By Craig Fuller, CEO of FreightWaves

Trucking spot rates are way up, but so are operating expenses. What does this mean for carriers?

“Demand is just falling back to pre-pandemic levels.” I’ve heard this rebuttal to my earlier articles about a 2022 trucking “bloodbath” (here and here) for the past week. If “demand falls back to pre-pandemic levels” turns out to be true, the situation for truckers will actually be much worse than even I have predicted.

Since the pandemic began, the number of dispatchable trucks in the for-hire trucking market (trucks with a driver and available to haul a load) is up approximately 10%. Since trucking rates are contingent upon the balance of supply and demand, if volumes were to drop back to pre-pandemic levels (with far more capacity in the market), rates would collapse.

{kind=link}

But even more worrisome is that the operating expenses of carriers are at much higher levels than before COVID. FreightWaves estimates that operating expenses for nearly all carriers have surged by as much as $0.38 per mile over pre-COVID levels. This calculation only includes maintenance, insurance and fuel costs.

{kind=link}

The calculation does not include driver wages or equipment purchase/finance, which could nearly double the increased amount of operating expenses.

If a trucking fleet were to start up today with an employee driver, its operating cash expenses would be as much as $0.72 per mile higher than a trucking fleet that was started in 2019.

Fuel

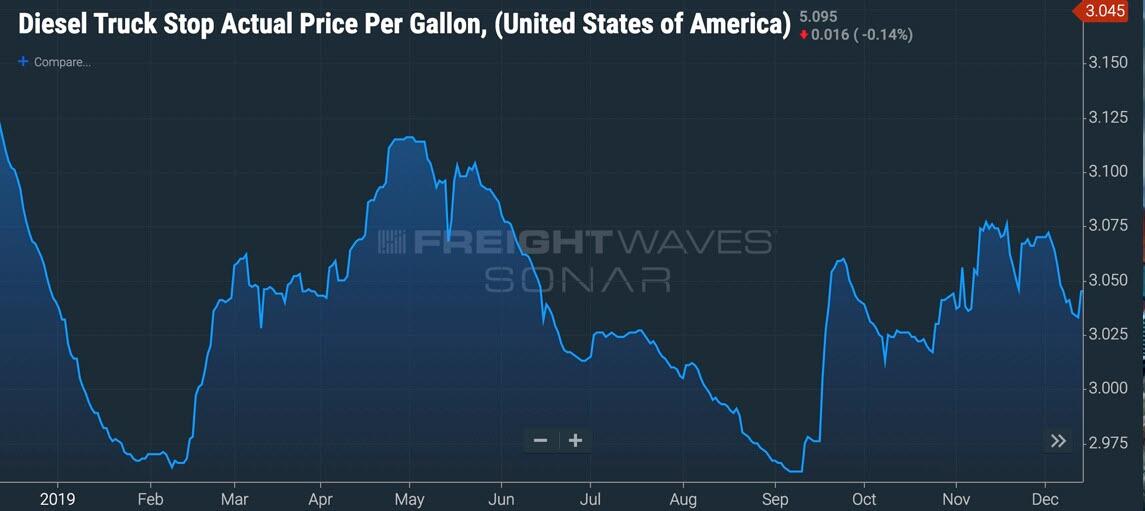

The cost of fuel is one of the largest variable operating expenses in the trucking industry. During 2019, retail diesel prices ranged between $2.97 and $3.11 per gallon. For the most part, retail diesel prices hardly moved in 2019.

Using an average of 7 miles per gallon, the cost of fuel during 2019 ranged from $0.42 to $0.44 per mile for a Class 8 truck. For most carriers operating in 2019, fuel was incredibly stable and was largely an afterthought.

{kind=link}

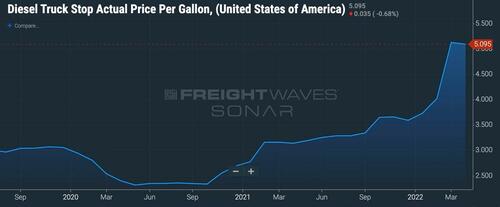

Fast forward to April 5, 2022. The retail diesel price is $5.10/gallon. At 7 miles per gallon, that equates to $0.73/mile. This $0.30 increase per mile will significantly impact the cash flows of carriers.

{kind=link}

Fuel is often paid for at the point of sale, when a truck is fueled. But shippers and brokers often pay a carrier a month or two after the load has been delivered.

According to data from the Truckload Carriers Association (TCA), an average carrier runs about 6,500 miles in a given month. At $0.30 per mile, the additional cash outlay for an operator compared to 2019 is approximately $1,950 per month. This is cash that a fleet must advance before collecting it from a broker or shipper. While carriers that have fuel surcharges will be able to pass on some of their fuel expenses to their shipper customers, carriers that operate in the spot market will not. Spot freight typically doesn’t include a surcharge for fuel.

Insurance and maintenance

Referencing TCA data, insurance costs per mile were $0.07 in 2019. In 2022, these costs have increased to $0.09 per mile. Using the same dataset, maintenance costs have increased from $0.20 to $0.26 per mile. In total, insurance and maintenance are up $0.08 per mile.

When added together (fuel, insurance, and maintenance) nearly every trucking company has experienced increases of at least $0.38 per mile versus 2019, regardless of when they consummated operations.

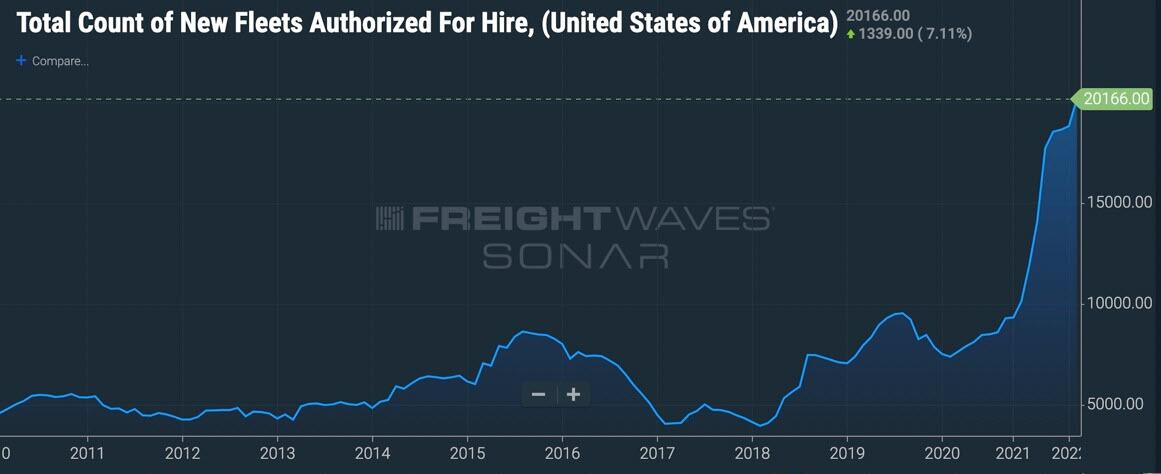

Lots of new entrants bought at the top of the market

The trucking market has experienced the highest number of new fleet startups in its history. The chart of new startup fleets could easily be confused with a meme stock.

Entrepreneurs and aspiring fleet executives registered a new carrier with the FMCSA and then went out and purchased a truck. Since it was nearly impossible for these carriers to order a new truck from a truck manufacturer, we can assume that they bought a truck that was at least three years old from another carrier.

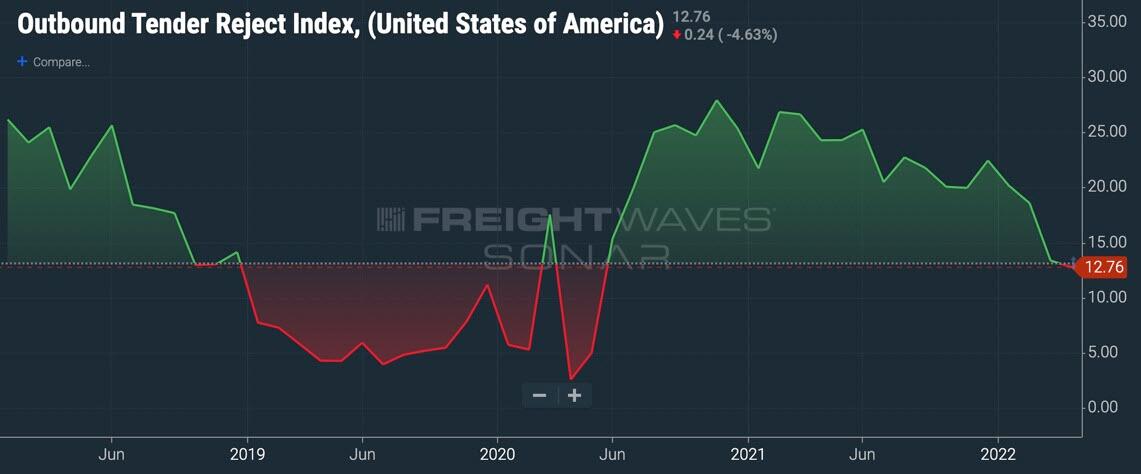

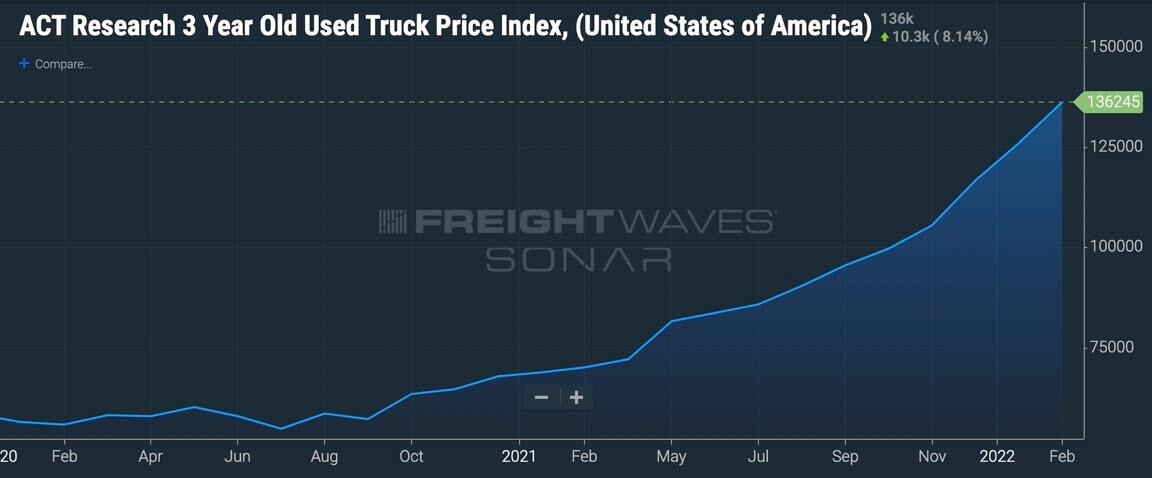

The worst thing anyone can do in any situation is to buy at the top of the market. With tender reject data warning that trucking companies are quickly losing pricing power for hauling loads, equipment values will soon follow.

{kind=link}

Equipment purchase and finance

One of the largest expense increases is the truck itself. The cost of purchasing a new or used truck is mostly dependent upon when the truck was purchased. Therefore, there is a wide range in costs.

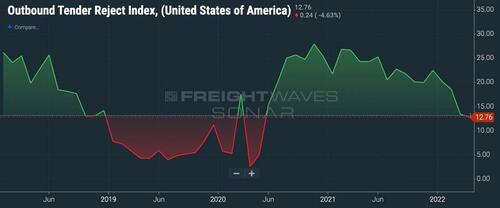

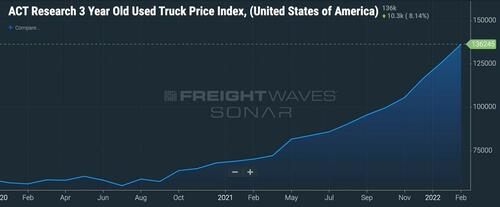

According to ACT data, a 3-year-old used truck could have been purchased for $69,000 in 2019. In early March 2022, the price of a 3-year-old truck had nearly doubled – to $136,000. This $67,000 increase in the cost of a used truck is unprecedented.

{kind=link}

For this example, I will use a finance rate of 5% and a 60-month finance schedule. I will also assume that the buyer put no money down on the purchase and that there was 7% sales tax on the truck. I will also assume that a truck is being driven 6,500 miles per month.

At a 2019 sales price of $69,000, the monthly payment would be $1,393. At 6,500 miles per month, the fleet would need to generate $0.21 per mile in cash flow just to cover the equipment purchase.

The truck will have a residual value when it is sold five years later, but it is hard to predict what the market will be at that point. For our calculations, we are going to use cash flow and not GAAP.

If a similar truck was purchased in 2022, it would cost $136,000. The monthly payment would be $2,746, or $0.42 per mile.

While it is hard to predict how many used trucks traded at these extremely high levels, we know that many fleets have been growing quickly throughout the past few quarters and some fleets will be saddled with these headwinds.

Taken all together, a fleet that is relatively new to trucking, operating a used truck purchased in 2022, would need to generate $0.59/mile more than they would have if it had started operations in 2019. If there is an employee driver to consider, an over-the-road driver in 2022 can expect to make around $0.60/mile. In 2019, the same driver would have made around $0.47/mile.

With an employee driver, plus a truck purchased in 2022, a new fleet entering the market would have operating cash requirements that are $0.72 per mile more than the same fleet in 2019. Therefore, if a fleet is paying out an additional $0.72 per mile in operating cash compared to pre-pandemic, it will have an incredibly difficult time surviving in a dropping spot rate environment.

The spot rate environment is changing – and quickly

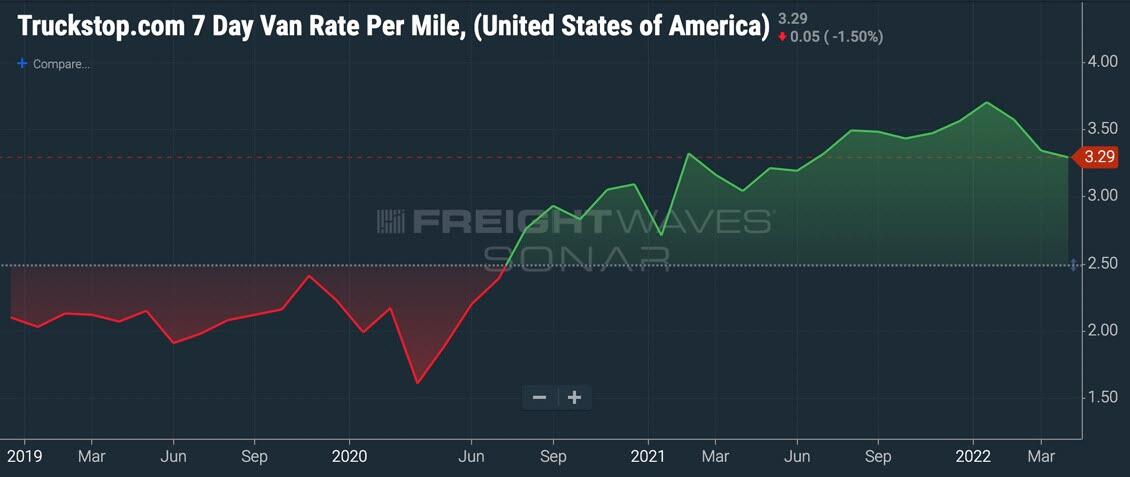

According to Truckstop.com, the current van truckload spot rate is $3.29 per mile (as of April 5, 2022). The Truckstop.com spot rate in SONAR includes fuel in the entire rate. All references to spot rates will include fuel.

Trucking spot rates peaked on Jan. 9, 2022 at $3.83 per mile. The $0.54 drop per mile is significant, but in historical context trucking spot rates are still way up – by over $1.00 per mile.

Looking back at 2019, which was when we experienced the last freight recession, trucking spot rates ranged from $1.91 to $2.54 per mile. While these ranges are the low and highs, the typical range during 2019 was closer to $2.00-2.20 per mile.

But here is where it gets tricky. The trucking spot rate is only one part of the story. It doesn’t tell us how profitable trucking carriers are.

Trucking is a very difficult business to make money in

A lot of this depends on whether or not spot rates drop to levels that drain the cash flow of carriers to the point that they run out of money.

Trucking is a notoriously difficult business, with violent swings between bull and bear markets. Even in the best of times, trucking companies struggle for every penny of profit.

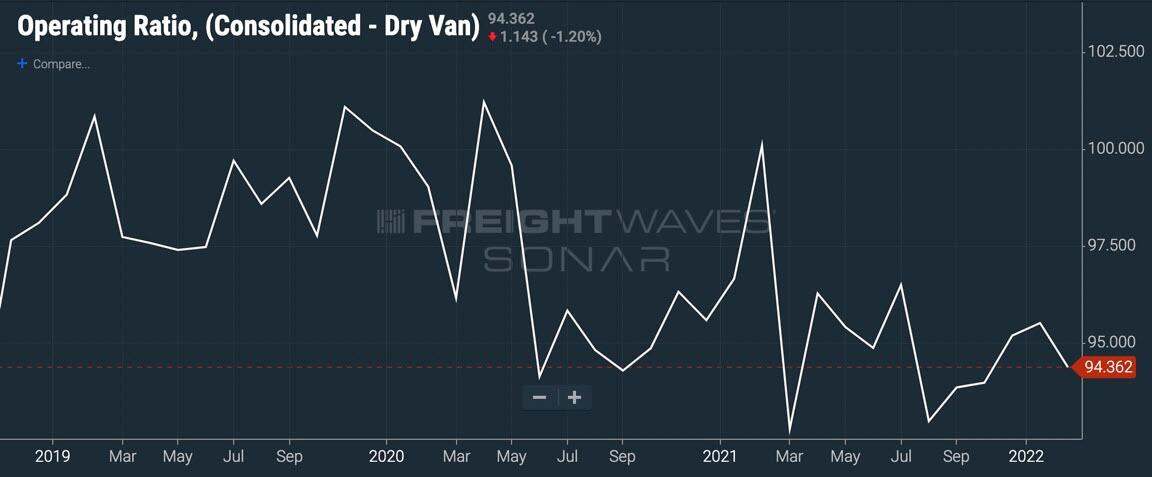

The best trucking market in history took place in 2021, marked by record volume and unprecedented trucking spot rates. Nonetheless, average trucking companies struggled to make money.

The operating ratio for dry van truckload carriers in 2021 across TCA’s benchmarking program ranged from 92 to 97. That means for every $100 of revenue the fleet generated, it generated an operating profit of just $3 to $8. This was before the fleet paid for any working capital lines of credit (debt) or taxes.

Is a bloodbath on the way?

The bloodbath of 2019 was marked by the highest number of trucking fleet bankruptcies in history. If we see trucking spot rates continue to drop, we may see similar or worse conditions in the market.

The operating ratio for truckload carriers in 2019 ranged from 97 to 101. A significant deterioration in spot rates, combined with the surge in operating expenses that fleets are contending with, could spell disaster for many.

The low for trucking spot rates in 2019 was $1.91/mile. I am assuming that this is the baseline for which many small carriers will struggle to survive. Fuel is a part of the spot rate, so the calculation should be adjusted.

The $0.30/mile increase in fuel means the adjusted 2019 spot rate “bloodbath baseline” would be around $2.21 per mile. Since fuel bills are paid immediately, I assume that anything below this spot rate level will be dire for many small trucking companies and could result in a rapid acceleration in fleet bankruptcies.

Insurance and maintenance are not “instant” killers of fleets, but kill over time. As long as spot rates are above $2.34 per mile for most of 2022 the majority of small fleets that entered the market prior to 2020 will survive – at least until their insurance bills hit or they have a breakdown.

{kind=link}

But new fleets will be at a major disadvantage to existing fleets

If a fleet is new to trucking and purchased a truck in 2022, it has the worst operating environment of any carrier. Assuming that the truck is being driven by an employee driver, spot rates below $2.63 per mile could spell disaster for trucking fleets if that rate persists for long.

All of this could change – and quickly.

If retail diesel prices move up, the break-even point for carriers would move up as well. If fuel drops, the break-even point would be lower. Watch the direction of retail diesel; it has a lot to do with the profitability of trucking fleets, especially small carriers.

If fuel continues to surge, the “bloodbath baseline” will also move up as well. On the other hand, if fuel drops, there could be significant relief for the small spot market carriers.

There is a great deal of disagreement on the direction of fuel and trucking spot rates, but one thing is certain – there will be volatility. Hopefully, we all avoid vertigo along the way.

Tyler Durden

Thu, 04/07/2022 – 18:05

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com