Futures Rise As Dip Buyers Emerge To Cap Best Week Since Mid-March

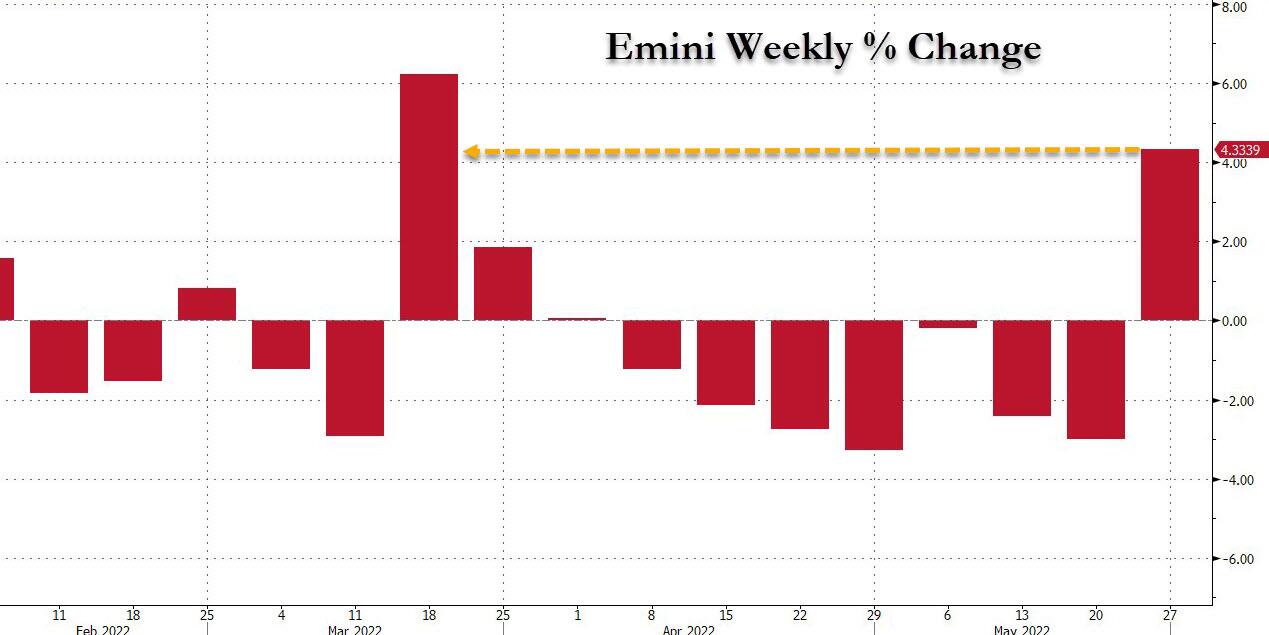

Unless stocks crater today, and the S&P tumbles by 4.3%, the streak of seven consecutive weekly declines in the S&P is about to end…

… as US stock futures rose again on Friday, their third consecutive gain, setting up the underlying indexes for the first strong weekly finish since late March on signs consumers remain resilient despite inflationary pressures, as upbeat earnings from Alibaba and Baidu eased some fears on the economic impact of China’s Covid lockdowns, and as investors (mostly retail) have staged a cautious return to the market hoping that the selloff earlier this month left valuations at bargain levels. Nasdaq 100 contracts rose 0.5% by 7:15 a.m. in New York, while S&P 500 futures were up 0.4%. Still, even after the recent rout, upside may be limited as the S&P 500’s 12-month fwd P/E ratio is now near its 10-year average.

Among notable moves in premarket trading, Gap Inc. shares sank as much as 17% as analysts after analysts said that the retailer’s guidance cut was worse than expected, prompting brokers to lower their targets and downgrade the stock given a worsening macroeconomic environment could trigger further bad news. China’s Uber, Didi Chuxing, jumped after a Bloomberg News report that state-owned automaker China FAW Group is considering acquiring a significant stake in the ride-hailing company. Zscaler Inc. rose after the security software company reported results above expectations. Here are some other notable premarket movers:

- Gap (GPS US) shares dropped as much as 17% in US premarket trading with analysts saying that the retailer’s guidance cut was more than expected, prompting brokers to lower their targets and downgrade the stock given a worsening macroeconomic environment could trigger further bad news.

- Costco (COST US) shares dropped 2.1% in US after-hours trading on Thursday. While Costco’s margins disappointed analysts, brokers were generally positive on how the wholesale retailer is navigating an environment with rising inflation by controlling expenses.

- Zscaler (ZS US) shares rose 2% in extended trading on Thursday, after the security software company reported third- quarter results that beat expectations and raised its full-year forecast. Analysts lauded strength in multi-product deals.

- Marvell Technology (MRVL US) shares climbed 3.4% in US postmarket trading after results. Analysts highlighted that the semiconductor maker is seeing strength across key markets, in particular across data center and carrier infrastructure.

- 23andMe Holding Co. (ME US) dropped 8.3% in postmarket trading Thursday. It is in a “tough spot,” Citi says in note after the consumer genetics firm gave a fiscal 2023 revenue forecast that missed expectations.

- Workday (WDAY US) shares fell 9% in extended trading on Thursday, after the software company reported adjusted first-quarter earnings that missed expectations. Analysts noted that software deals were pushed out of the quarter and cut their price targets as they factored in the increased global uncertainty.

The latest round of retail earnings have restored some confidence in consumer demand, lifting appetite for risk assets, while speculation is growing that the Federal Reserve will pause its rate hikes later this year as inflation shows signs of peaking. Still, Citigroup strategists on Friday cut their recommendation on US stocks to neutral on the risk of a recession, joining an increasing number of banks in warning of a growth slowdown.

The path for the Federal Reserve to successfully bring inflation down while keeping the rate of economic growth above zero is narrow, according to Mark Haefele, chief investment officer at UBS Global Wealth Management. “If Fed policymakers underestimate the strength of the US economy, we face an extended period of above-target inflation. If they overestimate it, we face a recession. And we can’t know with great conviction which path we’re on,” he wrote in a note.

Global stock funds saw their biggest inflows in 10 weeks, led by US stocks, according to EPFR data, as cheaper valuations lured buyers after a steep selloff on recession fears. The selloff made valuations attractive and enticed investors back into a market still shadowed by worries about inflation and higher interest rates, China’s downbeat economic outlook and the war in Ukraine.

“We may see a little bit more stability here because we have repriced the stocks so much already,” Anastasia Amoroso, iCapital chief investment strategist, said on Bloomberg Television. “In the next three to six months it’s still going to be a constrained market environment.”

Meanwhile, China-US tensions are once again being played out after direct comments from Secretary of State Antony Blinken aimed at Chinese President Xi Jinping. And in a fresh challenge to Beijing, the US and Taiwan are planning to announce negotiations to deepen economic ties.

And elseshwere, as the Russins war in Ukraine approaches 100 days, the US may announce a new package of aid for Kyiv as soon as next week that would include long-range rocket systems and other advanced weapons. Boris Johnson urged further military support for Ukraine, including sending it more offensive weapons such as Multiple Launch Rocket Systems that can strike targets from much further away. Russia’s efforts to avoid its first foreign default in a century are back in focus on Friday, when investors are supposed to receive about $100 million in interest on Russian debt.

Turning back to markets, consumer and technology sectors led gains in Europe’s Stoxx 600 which rose 0.9%, and was headed for its best weekly advance since mid-March, while utilities and energy shared lagged after the UK government announced windfall tax plans on oil and gas companies on Thursday. BP Plc said it will look again at its plans in the country. Here are some of the more notable movers in Europe:

- Cantargia gains as much as 23%, the largest intraday rise since December, after releasing three research updates late Thursday. The interim readout for the company’s nadunolimab (CAN04), used in combination with gemcitabine and nab-paclitaxel as a first line treatment of PDAC, a type of pancreatic cancer, was the most interesting of the data releases, according Kempen.

- FirstGroup shares jump as much as 9.8%, extending the gains from yesterday’s confirmation that the public transport operator received an unsolicited takeover approach from I Squared.

- Richemont shares rise as much as 8.3%, heading for their best weekly advance since November, pushing the Swiss Market Index higher as dip buyers returned more broadly this week.

- European miners advance for a third day, outperforming all other sectors on the Stoxx 600 on Friday as iron ore futures climb and metals posted broad gains.

- Hapag-Lloyd falls as much as 7.1% after Citi cut the recommendation to neutral from buy due to valuation versus peers. In note on European shipping, broker says it expects the supply and demand dynamics to remain favorable in the near term.

- Rieter Holding falls as much as 5.4% as Baader Helvea downgrades its recommendation to reduce from add after the manufacturer of chemical fiber systems said that it’s seeing a challenging first half.

Earlier in the session, Asian stocks also advanced as upbeat earnings from Alibaba and Baidu eased some fears on the economic impact of China’s Covid lockdowns and fueled risk-on sentiment. The MSCI Asia Pacific Index rose 1.6%, poised for its first gain in four sessions, led by consumer discretionary and technology shares. Most markets in the region were up, led by Hong Kong. Alibaba and Baidu both delivered better-than-expected quarterly sales growth, providing investors with some relief after Tencent’s recent lackluster report and amid concerns over China’s virus measure and regulatory crackdowns. The Hang Seng Tech Index, which tracks the nation’s tech giants listed in Hong Kong, surged 3.8%. Asian equities have gained about 0.7% this week, set for a back-to-back weekly advance as dip buyers emerged. The regional MSCI benchmark is still down about 14% this year amid ongoing market concerns over global inflation and higher US interest rates, China’s economic outlook and the war in Ukraine.

“The risk of a bull trap cannot be dismissed,” Vishnu Varathan, the head of economics and strategy at Mizuho Bank, wrote in a note. “Bear markets are famous for the pockets of relief rallies,” and increasing strains on liquidity in the coming quarters “may not pass without pain.”

Japan’s stocks likewise advanced as the nation prepared to reopen to foreign tourists and China’s tech shares jumped. The Topix rose 0.5% to 1,887.30 as of the 3pm close in Tokyo, while the Nikkei 225 advanced 0.7% to 26,781.68. Tokyo Electron Ltd. contributed the most to the Topix’s gain, increasing 3.2%. Out of 2,171 shares in the index, 1,480 rose and 615 fell, while 76 were unchanged

In Australia, the S&P/ASX 200 index rose 1.1% to close at 7,182.70, the highest level since May 6, led by energy and consumer discretionary shares. Woodside Energy Group was among the biggest gainers as US crude and gasoline stockpiles showed signs of continuing decline ahead of the summer driving season. Appen was the top decliner after saying that Telus revoked its indicative proposal for a takeover. In New Zealand, the S&P/NZX 50 index fell 0.3% to 11,065.15

In FX, the Bloomberg Dollar Spot Index slumped as the dollar was steady to weaker against all of its Group-of-10 peers. Treasuries were steady across the curve. The euro inched up to touch a fresh one- month high of 1.0765 before paring. The bund yield curve bull- flattened slightly, drawing the 10-year yield away from 1%. Risk- sensitive Antipodean and Scandinavian currencies led gains. The Australian dollar climbed as a decent retail sales print brightened the outlook and a drop in the greenback triggered buy-stops. Benchmark bonds slipped. Australian retail sales rose 0.9% m/m in April vs estimate +1% and prior +1.6%. The pound ticked higher, touching its highest level in a month against the dollar, while gilts advanced. Chancellor of the Exchequer Rishi Sunak said that his package of support for the UK economy will have a “minimal” impact on inflation. The yen advanced for a second day as lower Treasury yields weighed on the dollar. Japanese bonds rise after being sold off on Thursday

In rates, Treasuries were steady, following gains in European markets where bull-flattening was observed across bunds and gilts. Yields were richer by 1bp-3bp across the curve, the 10-year yield dropped by ~2bp to 2.72%, underperforming bunds by 1.5bp, gilts by ~3bp. IG dollar issuance slate still blank in what has so far been the slowest week of the year for new deals; next week’s calendar is expected to total $25b- $30b. Focal points for US session include several economic data releases including April personal income/spending with PCE deflator. Sifma recommended 2pm close of trading for dollar-denominated fixed income ahead of US holiday weekend.

In commodities, WTI drifts 0.7% higher to trade below $115. Spot gold rises roughly $7 to trade at $1,858/oz. Most base metals are in the green; LME nickel rises 6.6%, outperforming peers.

Looking to the day ahead, and data releases include US personal income and personal spending for April, as well as the preliminary wholesale inventories for that month, and the final University of Michigan consumer sentiment index for May. In the Euro Area, there’s also the M3 money supply for April. Otherwise, central bank speakers include ECB Chief Economist Lane.

Market Snapshot

- S&P 500 futures up 0.3% to 4,068.25

- STOXX Europe 600 up 0.7% to 440.64

- MXAP up 1.6% to 165.89

- MXAPJ up 2.1% to 542.44

- Nikkei up 0.7% to 26,781.68

- Topix up 0.5% to 1,887.30

- Hang Seng Index up 2.9% to 20,697.36

- Shanghai Composite up 0.2% to 3,130.24

- Sensex up 1.2% to 54,919.92

- Australia S&P/ASX 200 up 1.1% to 7,182.71

- Kospi up 1.0% to 2,638.05

- German 10Y yield little changed at 0.99%

- Euro up 0.1% to $1.0737

- Brent Futures up 0.4% to $117.91/bbl

- Gold spot up 0.5% to $1,859.48

- U.S. Dollar Index down 0.16% to 101.67

Top Overnight News from Bloomberg

- The path for Russia to keep sidestepping its first foreign default in a century is turning more onerous as another coupon comes due on the warring nation’s debt. Investors are supposed to receive about $100 million of interest on Russian foreign debt in their accounts by Friday, payments President Vladimir Putin’s government says it has already made

- China’s oil trading giant Unipec has significantly increased the number of hired tankers to ship a key crude from eastern Russia

- A central bank legal proposal envisages Russian eurobond issuers placing “substitute” bonds in order to ensure debt payments come through to local investors, Interfax reported

- The US and Taiwan are planning to announce negotiations to deepen economic ties, people familiar with the matter said, in a fresh challenge to Beijing, which has cautioned Washington on its relationship with the island.

- Profits at Chinese industrial firms shrank last month for the first time in two years as Covid outbreaks and lockdowns disrupted factory production, transport logistics and sales

- “The process of increasing interest rates should be gradual,” ECB Governing Council member Pablo Hernandez de Cos comments in op- ed in Expansion. “The aim is to avoid abrupt movements, which could be particularly damaging in a context of high uncertainty such as the current one”

- The RBA is poised for its first review in a generation as new Treasurer Jim Chalmers makes good on a pledge to ensure the nation’s monetary and fiscal regimes are fit for purpose

- The UK signed its first trade agreement with a US state, amid warnings that Prime Minister Boris Johnson’s stance on Brexit is hindering progress on a broader deal with Joe Biden’s administration

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took impetus from the risk-on mood on Wall St where all major indices were lifted amid month-end flows and encouraging retailer earnings. ASX 200 was led higher by outperformance in the commodity and resources industries, while consumer stocks were mixed after Retail Sales printed in line with expectations, albeit at a slowdown from the prior month. Nikkei 225 traded positively but with upside capped by a mixed currency and weakness in energy and power names after increases in international prices and with the government looking to address the tight energy market. Hang Seng and Shanghai Comp were firmer with notable outperformance in Hong Kong amid a euphoric tech sector after earnings from Alibaba and Baidu topped estimates which also inspired the NASDAQ Golden Dragon China Index during the prior US session, while advances in the mainland were moderated by the contraction in April Industrial Profits and after Premier Li’s unpublished comments from Wednesday’s emergency meeting came to light in which he warned of dire consequences for the economy.

Top Asian News

- China’s State Council will seek specific implementation rules by May 31st regarding necessary measures at all levels of government and will dispatch inspection teams to all 31 provinces, municipalities and autonomous regions to oversee the rollout amid an urgent need for national economic mobilisation, according to SGH Macro Advisors.

- US is seeking to hold economic discussions with Taiwan in the latest test with China, while supply chains and agriculture are said to be among the topics, according to Bloomberg. Furthermore, reports noted that bilateral economic talks will be announced in the upcoming weeks.

- Evergrande (3333 HK) is reportedly considering repaying offshore bondholders in instalments, according to Reuters sources; discussing giving the option of converting part of debt into equity of property management and EV units.

- China’s Health Official says some areas along the Jilin border report local infections without a clear source, close attention should be paid to the risk of importing the virus; COVID infections show a trend of gradual spread from border to inland areas, via Reuters

European bourses are firmer, Euro Stoxx 50 +0.9%, drawing impetus from APAC strength into month-end with catalysts thin thus far. Stateside, futures are supported across the board with familiar themes in play pre-PCE Price Index for insight into the ‘peak’ inflation narrative; ES +0.3%. Note, the FTSE 100 Unch. is the mornings underperformer amid pressure in energy names after Chancellor Sunak’s windfall tax announcement on Thursday. DiDi (DIDI) has reportedly drawn interest from FAW Group, regarding a stake purchase, according to Bloomberg. +7.5% in the pre-market

Top European News

- UK Oil Windfall Tax Prompts BP to Review Investment Plans; UK Energy Stocks Extend Windfall Declines as Retailers Gain

- Richemont Leads Swiss Stocks Higher as Dip Buyers Return

- Hapag-Lloyd Drops; Cut to Neutral at Citi on Valuation

- Big Dividend Payers May Be Next After UK Windfall Tax on Energy

FX

- Greenback grinds higher ahead of PCE inflation metrics with month end rebalancing flows providing impetus, DXY bounces from fresh WTD base just under 101.500 to 101.800.

- Kiwi and Aussie propped by bounce in commodities and Loonie protected by further gains in crude; NZD/USD tests Fib retracement at 0.7129, AUD/USD eyes 0.7150 and USD/CAD probes 1.2750.

- Big option expiries in the mix and potentially supportive for the Dollar into long US holiday weekend, +1bln rolling off at NY cut not far from spot in EUR/USD, USD/JPY, AUD/USD and USD/CAD.

- Rand firmer as Gold touches Usd 1860/oz after 200 DMA breach, USD/ZAR below 15.7000.

Fixed Income

- Debt futures on a firmer footing ahead of US PCE price metrics, but some way below weekly peaks.

- Bunds sub-154.00, Gilts under 119.00 and 10 year T-note below 121-00.

- Curves a tad flatter following hot reception for 7 year US issuance.

Commodities

- Crude benchmarks are underpinned, but off best levels, by broader sentiment and initial USD weakness going into a long US weekend with Memorial Day touted as the driving seasons commencement.

- WTI July and Brent August, at best, were in proximity to USD 115/bbl vs troughs of USD 113.61/bbl and USD 113.77/bbl respectively.

- US Treasury is reportedly expected to renew Chevron’s (CVX) license to operate in Venezuela as soon as Friday, according to Reuters citing sources.

- China’s State Planner has approved a coal mine in the Shanxi area to bolster annual output to 12mln tonnes per annum from 8mln; investment of CNY 5.35bln, via Reuters.

- Spot gold is steady and holding onto the bulk of overnight upside after breaching the 21-DMA at USD 1850.80/oz; USD 1860.19/oz peak, thus far.

US Event Calendar

- 08:30: April Advance Goods Trade Balance, est. -$114.8b, prior -$125.3b, revised -$127.1b

- 08:30: April Retail Inventories MoM, est. 2.0%, prior 2.0%

- April Wholesale Inventories MoM, est. 2.0%, prior 2.3%

- 08:30: April Personal Income, est. 0.5%, prior 0.5%; April Personal Spending, est. 0.8%, prior 1.1%

- 08:30: April PCE Deflator MoM, est. 0.2%, prior 0.9%; PCE Deflator YoY, est. 6.2%, prior 6.6%

- April PCE Core Deflator MoM, est. 0.3%, prior 0.3%; PCE Core Deflator YoY, est. 4.9%, prior 5.2%

- April Real Personal Spending, est. 0.7%, prior 0.2%

- 10:00: May U. of Mich. Current Conditions, est. 63.6, prior 63.6; Expectations, est. 56.3, prior 56.3; Sentiment, est. 59.1, prior 59.1

- 10:00: May U. of Mich. 1 Yr Inflation, est. 5.4%, prior 5.4%; 5-10 Yr Inflation, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

A reminder that it’s your last chance to answer our latest monthly survey, where we try to ask questions that aren’t easy to derive from market pricing. This time we ask if you think the Fed would be willing to push the economy into recession in order to get inflation back to target. We also ask whether you think there are still bubbles in markets and whether equities have bottomed out yet. And there’s another on which is the best asset class to hedge against inflation. The more people that fill it in the more useful so all help from readers is very welcome. The link is here.

I did have tickets available for tomorrow night’s Champions League final but there is a big 36 hole golf tournament at my club so I decided that at my age you never know when your body will fail next so playing sport now pips watching it live. So I’ll be playing golf all day, trying to rescue my marriage for an hour when I get home, and then blaring out the final on the TV at home with a couple of glasses of wine for good measure. I can’t honestly think of a better day. However I may come last and Liverpool may lose so let’s see what happens!

The market comeback this week is on a par with some of Madrid’s remarkable ones this year and indeed it’s been another strong performance over the last 24 hours, with better-than-expected outlooks from US retailers helping to bolster sentiment, coupled with growing hopes that the Fed won’t take policy much into restrictive territory, if at all. Those developments helped the S&P 500 to post a +1.99% advance yesterday, bringing its gains for the week to +4.01%, and means we should finally be on the verge of ending a run of 7 consecutive weekly losses. Obviously it’s not impossible things could end up in negative territory given recent volatility, and it was only last week the index posted a one-day decline of more than -4%, but it would still take a massive slump today to get an 8th consecutive week in the red for only the third time since the Great Depression.

That advance grew stronger as the day went on, with S&P futures having actually been negative when we went to press yesterday. But sentiment was aided by a number of positive earnings developments, with Macy’s (+19.31%) boosting its adjusted EPS guidance before the US open, whilst the discount retailers Dollar Tree (+21.87%) and Dollar General (+13.72%) both surged as well thanks to decent reports of their own. That helped consumer discretionary (+4.78%) to be the top performing sector in the S&P, and in fact Dollar Tree was the top performing company in the entire index. Cyclicals were the outperformers, but defensives also shared in the advance that saw around 90% of the index’s members move higher on the day.

As well as that news on the retail side, risk appetite has been further supported by growing speculation that the Fed won’t be as aggressive in hiking rates as had been speculated just a few weeks ago. I’m not sure I agree with that conclusion but if you look at the futures-implied rate by the December 2022 meeting of 2.64%, that is some way down from its peak of 2.88% back on May 3rd, and in fact means that markets have now taken out just shy of one 25bp hike from the rate implied by year end, which makes a change from that pretty consistent move higher we’ve seen over recent months.

Yesterday also brought fresh signs that this re-pricing is beginning to filter its way through to the real economy, with data from Freddie Mac showing that the average rate for a 30-year mortgage fell to 5.10% last week, down from 5.25% the week before. For reference that’s the biggest weekly decline since April 2020, and comes on the back of recent housing data that’s underwhelmed against the backdrop of higher rates. There was another report fitting that pattern yesterday too, with pending home sales for April dropping by a larger than expected -3.9% (vs. -2.1% expected). But as with the retail outlooks, the more timely data was much more positive, with the weekly initial jobless claims falling to 210k (vs. 215k expected) in the week ending May 21, whilst the Kansas City Fed’s manufacturing index for May came in at 23 (vs. 15 expected).

Treasuries swung back and forth against this backdrop, but ultimately the more bullish outlook led to a small steepening in the curve, with the 2yr yield down -1.6bps as 10yr yields were essentially flat at 2.75%. In a change from recent weeks, breakevens marched higher despite the little changed headline, with the 10yr breakeven up +7.0bps to come off its two-month low the previous day. But to be fair, that came amidst a big surge in oil prices after US data showed gasoline stockpiles fell to their lowest seasonal level since 2014, with Brent Crude (+2.96%) up to a 2-month high of $117.40/bbl, whilst WTI (+3.41%) rose to $114.09/bbl.

European markets followed a pretty similar pattern to the US, with the STOXX 600 advancing +0.78% on the day. However, utilities (-1.12%) were the worst-performing after the UK government moved to impose a temporary windfall tax on oil and gas firms’ profits at a rate of 25%. That came as part of a wider package of measures to help with the cost of living, adding up to £15bn in total. They included a one-off payment of £650 to 8mn households in receipt of state benefits, with separate payments of £300 to pensioner households and £150 to those receiving disability benefits. There was also a doubling in the energy bills discount from £200 to £400, whilst the requirement to pay it back over five years has been removed as well. See Sanjay Raja’s blog on it here and where he also compares the measures to similar ones seen in the big 4 EuroArea economies.

With more fiscal spending in the pipeline, UK gilts underperformed their counterparts elsewhere in Europe, with 10yr yields ending the day up +5.9bps. Those on bunds (+4.6bps) and OATs (+3.2bps) also rose too, but the broader risk-on tone led to a tightening in peripheral spreads, with the gap between 10yr BTPs over bunds falling -10.4bps yesterday to 189bps. There was a similar pattern on the credit side, with iTraxx crossover coming down -23.9bps to 439bps, which was its biggest daily decline in nearly 2 months.

Asian equity markets are joining in the rally this morning with the Hang Seng rising +2.93% as Chinese listed tech stocks are witnessing big gains after Alibaba (+12.21%) posted better than expected Q4 earnings yesterday. Mainland Chinese stocks are also trading higher with the Shanghai Composite (+0.52%) and CSI (+0.63%) up. Elsewhere, the Nikkei (+0.63%) and Kospi (+0.89%) are also in the green. Outside of Asia, futures contracts on the S&P 500 (-0.11%) and NASDAQ 100 (-0.14%) are seeing mild losses.

Data released earlier showed that Tokyo’s core CPI rose +1.9% y/y in May versus +2.0% expected. Core core was +0.9% y/y as expected with nothing here at the moment to change the BoJ’s stance. Elsewhere, China’s industrial profits (-8.5% y/y) shrank at the fastest pace in two years in April, swinging from a +12.2% gain in March.

On the geopolitical front, we heard from US Secretary of State Blinken yesterday, who gave a significant speech on the Biden Administration’s China policy. Blinken zoomed out to give a view of the forest from the trees, noting that the Russia-Ukraine conflict was not as strategically important as America’s relationship with China over the long-run. He offered a three pillar strategy for managing the relationship with China that involved investing in US competitiveness, aligning strategy with allies to enhance effectiveness, and to compete with China across economic, military, and technological frontiers. He noted the countries’ two different political systems need not impair connection between its peoples, or inhibit dialogue.

Staying on the US-China front but switching gears, a bi-partisan group of US senators sent a letter to President Biden urging him to keep tariffs on China, to improve the US’s negotiating position in future deals, pouring cold water on the prospects for tariff relief to provide a temporary salve to raging price pressures.

To the day ahead, and data releases include US personal income and personal spending for April, as well as the preliminary wholesale inventories for that month, and the final University of Michigan consumer sentiment index for May. In the Euro Area, there’s also the M3 money supply for April. Otherwise, central bank speakers include ECB Chief Economist Lane.

Tyler Durden

Fri, 05/27/2022 – 07:54

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com