A Roman Lesson On Inflation

Authored by Alasdair Macleod via GoldMoney.com,

“While it is the duty of the citizen to support the state, it is not the duty of the state to support the citizen”

– President Grover Cleveland

After two centuries of debasement the Roman denarius ended up with no silver content.

The decline of the empire was accompanied by increasingly costly bureaucracy, stifling the economy.

It was a template for today.

There are differences.

But we share suffocating bureaucracy and the lack of specie in our currency systems.

As Rome did from Nero onwards, we have lost the plot. A general deterioration in our sense of purpose is an additional factor.

Perhaps Diocletian was the Joe Biden of his day. He was infamous for his edict on maximum prices, which basically shut down the production of goods. Will Joe Biden introduce a similar edict? Don’t rule it out…

Intervention’s slippery slope

The point President Cleveland made back in the 1880s was that individuals and vested interests had no rights to preferential treatment by a government elected to represent everyone. For if preference is given, it is always at the expense of others.

Those days are long gone, and the last president to take this stance was Calvin Coolidge in the 1920s. He was followed by Herbert Hoover, who was very much an interventionist. As Coolidge reportedly said of his Vice-President, “That man has given me nothing but advice, and all of it bad”. Hoover was criticised for his disastrous intervention policies by Franklin Roosevelt, who succeeded in ousting him in the 1932 election, and then outdid him with even more intervention. The outflows of gold generated by accelerating government spending and the Fed’s monetary policies led in 1933 to the suspension of gold convertibility for American citizens and the devaluation of the dollar in 1934 from $20.67 to $35 per ounce of gold.

Interventionsism has increased ever since, not just in America but in all other advanced nations. The socialisation of earnings and profits and the regulation of our behaviour by governments dominates economic activity today. Despite the warnings of sound-money theorists, a process that commenced over a century ago has not yet led to economic collapse, though the dangers of escalating state liabilities are a growing threat to economic stability.

A point that is ignored by nearly everyone is that government spending is an expensive luxury for any economy, tying up capital resources in the most inefficient way. Furthermore, governments, through tax and the diversion of savings and monetary inflation, destroy personal wealth. Yet, it is clear both through observation and logic that a successful economy is one that instead maximises personal prosperity.

This is clearly illustrated by observing the difference between Venezuela and America. Venezuela overtly and covertly has transferred nearly all personal wealth to its socialist government in the name of equality for all. The costs of government increased exponentially relative to its sources of available finance, bringing forward the day when economic and civil order cease entirely. America, despite decades of growth in government spending, has not yet sequestered most of its citizens’ wealth, though the process has been accelerating in recent years.

However, the problem is likely to become more of a public issue in the coming months, triggered perhaps by an increase of US Government bond issues at a time of an economic downturn and a downturn in bond demand due to a reluctance by the Fed to raise government borrowing costs.

At the same time as President Biden’s administration faces increasing spending demands, the Fed is trying to normalise its balance sheet by ceasing QE, and then presumably running off its bond exposure. Add to the mix marginal reductions of financial securities exposure in foreign-owned portfolios, and we have the potential for a perfect storm in the reserve currency’s bond market.

We have already seen a sharp increase in bond yields since March 2020, with the benchmark 10-year US Treasury yield increasing from 0.5% to 3%. On an historic basis and given that the Fed’s inflation target of 2% is left in the dust, the time-value on this bond is still far too low, despite the increase in yields so far.

Official consumer price inflation already exceeds 8%, and there is unlikely to be any significant let-up in this rate. And readers should give more credence to independent estimates than clearly biased government ones. ShadowStats.com currently has consumer prices rising at well over 15%.

We should not be surprised if these dynamics soon result in a derating of US Government bonds, and of the US Government’s finances. The derating won’t come from rating agencies which rightly fear official sanctions, but from markets themselves. But then markets are always the final arbiters of value.

Instead of passively accepting the Fed’s monetary cool-aid, proper assessments of bond risk can be expected to increasingly dominate valuations. Assuming the Fed continues to suppress interest rates, market pressures will lead to bond yield curves steepening and overcoming attempts at yield curve control. The interest cost to the Treasury will increase for all its new debt, except for very short-term borrowing. After snoozing through the period of zero interest rates, we are bound to awaken with some suddenness to the consequences of monetary debasement, which we have been collectively ignoring for too long.

Therefore, when thinking about risk, the economics of inflation are likely to become central to our thoughts. And as bond yields adjust by rising, we will be increasingly aware of the debt trap faced by the US Government. A one per cent increase in interest costs it an extra $230bn. Will President Biden pay for this by cutting the overall budget at a time of economic downturn? Unlikely, on the evidence so far. And when we begin to think in terms of what the time-value on US Government debt should be, possibly two per cent above a rising, but heavily doctored, CPI, how will an increase of borrowing costs of perhaps three or four per cent or even more look on the government’s books?

The UK faced a similar situation in the 1970s, when the IMF had to rescue government finances. Putting to one side the IMF’s mandated function which is to rescue emerging market economies from policy errors, there is no way the IMF or any other supranational organisation can intervene in US economic policy. In the absence of a supranational agency, the checks and balances which force the politicians to accept economic and monetary reality are entirely in the hands of the market —a situation which the establishment simply does not understand or recognise.

An inflationary collapse is the oldest of stories

The pressure to increase the rate of wealth-transfer from the productive private sector by dollar debasement will simply increase as bond yields rise. And the more wealth is transferred, the less there is left to transfer. This was the underlying reality faced in the Roman Empire, when the spendthrift Nero began the process by reducing the silver content of the denarius to pay his soldiers, having run out of funds. Among other costly acts, he set much of Rome on fire to rebuild it, through which legend has it he fiddled. This was perhaps a metaphor, because according to Suetonius, Nero was dedicated to the arts, sex, and debauchery, and may have been a pyromaniac as well. If Nero fiddled with anything, it was the currency. Some forty-three emperors following Nero continued the debasement process until the final monetary destruction under Diocletian over two centuries later.

The current century’s-worth of spending-led monetary debasement includes the additional burden (that is additional to Roman profligacy) of promises to the public in defiance of President Cleveland’s maxim quoted under the heading of this article. Depending on the rate at which future financial liabilities are discounted, in addition to current liabilities these are anything between five- and ten-times current GDP for America, and probably considerably more proportionately for Japan and many EU member states. Not even heavily-doctored price inflation figures can suppress the debt trap in which governments are now visibly ensnared, which all precedence tells us will be met with accelerating monetary debasement.

Since Herbert Hoover’s presidency, the US Government has been unconsciously rhyming the American economy with the Roman. Just as Rome’s emperors debased the coinage to pay for their profligacy and armies, so have America and her western allies debased their currencies to pay for welfare and military spending.

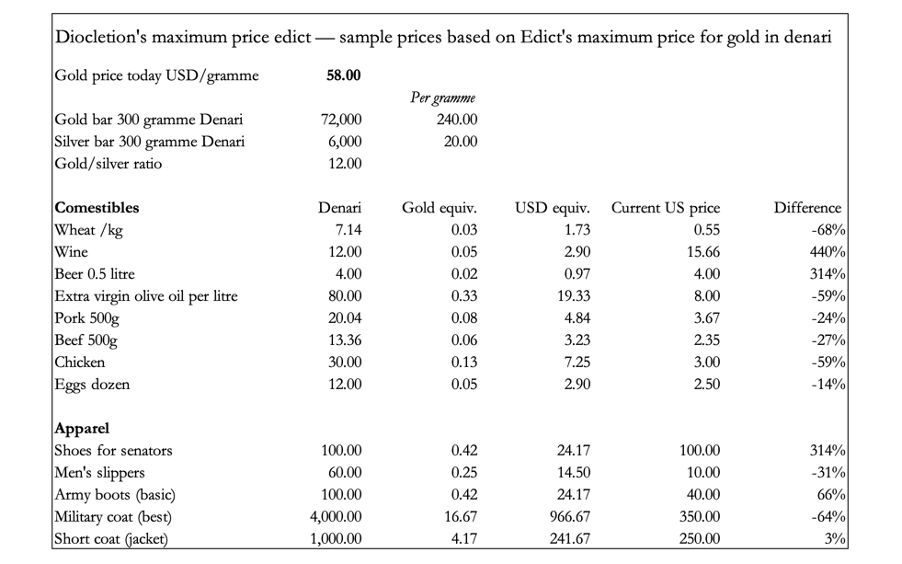

Excessive military spending was a Roman theme: pay the soldiers or courtesy of the Praetorian Guard the emperor dies. A declining empire and increasing bureaucracy further strangled its finances. 225 years after Nero, Diocletian went on to issue an edict in stone, banning traders from raising prices any higher than in the edict. Trade ceased, and Rome and other cities emptied for lack of food and growing disorder. The table below translates a few items from Diocletian’s price edict into current values, using the gold price as the exchange medium between then and now.

Other than beer and wine, price caps then were not too dissimilar from those of today and the cost of a jacket is almost the same as a modern blazer. While Biden is not Diocletian, perhaps these disparities indicate the levels towards which the US administration will be tempted to introduce price controls. And with respect to food, meat and dairy staples prices could reach Diocletian’s maximum prices this summer.

But Joe Biden and his predecessors have overseen other methods of achieving the same result. For the last forty years, prices for goods and services have been officially controlled by doctoring the inflation figures, though the reality is prices have continued to rise. The government’s inflation-linked spending commitments have been curbed and the state’s beneficiaries cheated. That cannot go on for ever.

Wage increases, which normally keep pace with rising prices, have been replaced by the simple expedient of encouraging the expansion of bank credit to fund personal consumption, along with discouragements to saving. Consequently, US Household debt now stands at $15.6 trillion funding personal consumption expenditures of $16.6 trillion. It amounts to modern smoke-and-mirrors deflecting attention from an underlying problem. But that is coming to an end, with labour shortages and a renaissance in union power.

The comparison with Rome has a further, worrying similarity. Roman silver and gold coins were the principal money for the known world. The US dollar is the world’s reserve currency today, and nearly all the other 170-odd government fiat currencies are aligned with or refer to it. An accelerating dollar collapse will take most of them down, just as surely as the Roman currency collapse propelled the world into the Dark Ages.

So far in this article, we have seen that the US economy has provided us with an example of a modern debt trap, that if not faced up to, will inevitably lead to an acceleration of monetary inflation and ultimately a collapse of purchasing power for the dollar. Most other nations are in the same position, though the high levels of personal borrowing are more endemic to America and the UK than anywhere else. Consequently, when the final currency collapse happens, profligate Anglo-Saxons will suffer a slightly different fate from the citizens of nations who habitually save.

The next phase of today’s monetary debasement

The next major expense facing governments and their central banks is a future credit crisis, likely to tip the inflation story into hyper-drive. Possibly, it will be a modern Diocletian moment, the final act of debasement before the lights go out, and we (only metaphorically, one hopes) leave the cities to forage in the country. A credit crisis is always the culmination of a cycle of credit, endemic to economies destabilised by banking systems trying to stimulate consumption by the inflation of currency and credit.

The time for the next credit crisis is rapidly approaching. We should be prepared for it to happen by the year-end. Crucially, inflation prospects will be set by the response of central banks. If they do not stand ready to bail out the commercial banks with monetary inflation, the global banking system will almost certainly collapse. Assuming central banks will attempt to prevent it, it will require the injection of enormous quantities of extra currency and central bank credit, potentially far larger than was required to bail out the global banking system in 2008/09. Not only that, but with their enormous holdings of interest-rate sensitive financial assets, central banks will themselves need to be recapitalised.

The Lehman rescue was itself of historic proportions, but the looming crisis is far larger. The risk is that governments and their central banks won’t succeed next time without collapsing their unbacked currencies. Additionally, since the last credit crisis all G20 nations agreed to introduce bail-in procedures to replace bail-outs, creating rescue uncertainty. The false reasoning was that governments shouldered the cost of the Lehman crisis, when bondholders and large depositors should have borne it instead. Governments never shoulder the costs of a crisis because it is paid for by debauching the currency. But bail-ins may be logical for rescuing single banks, or the banking system of a small country, but is likely to complicate the difficulties in a broader systemic crisis, because bondholders and large deposit holders will cause anticipatory runs on the system to protect themselves.

Large depositors have only two escapes, now the alternative of withdrawing cash notes in quantity is effectively closed. They can buy physical assets, at any price, to get rid of bank balances, or alternatively buy physical commodities. And top of the list of commodities must be gold, followed by silver, because they are widely accepted as the mediums of exchange everywhere.

But when you sell a currency to buy an asset, you are simply passing the currency to a willing buyer. The prescient observer might expect that there will be no bid for the riskiest currencies on the foreign exchanges, and then possibly no bid for the dollar itself. In other words, what in the past has been a systemic crisis for the global banking system could rapidly become a systemic crisis for the currencies themselves.

A currency crash is a growing risk

The future might be forecastable, but its timing is not. We can only speculate how rapidly events might evolve. However, unlike the Roman experience, which took 225 years to destroy the denarius, its successors, and the empire itself, today’s wave of monetary destruction looks like terminating soon after only a century or so.

Central banks are keenly aware of some systemic dangers, which is why they want to move us to a cashless society. With no cash, there cannot be an old-fashioned bank run. Their response to every successive credit crisis has been to restrict how businesses and people can protect themselves in the event of a systemic meltdown.

But now, long after President Cleveland made the remark that heads this article, his successors’ attempts to curry electoral favour have led to escalating costs, now demonstrably out of control. The combination of a debt trap sprung on governments by higher interest rates, and the unsustainability of private sector debt threatens a financial and monetary crisis world-wide, from which any attempted rescue through money-printing is bound to fail.

The rate at which inflation and the destruction of paper currencies accelerates from now will be determined by how swiftly the financially aware and the ordinary public wake up to the true scale of the monetary fraud governments have perpetrated. The consequences of currency and bank credit expansion have not yet been reflected in official price statistics, which have been hedonically manipulated to hide the evidence. An awakening to the reality, that fiat currencies have been badly abused by all governments, can be expected to have a suddenness about it.

Reflecting a loss of purchasing power, prices could begin to move rapidly higher. If the effects of Roman inflation over more than two centuries progressed with the lumbering speed of a laden oxcart, today it could suddenly accelerate like a post-Roman Ferrari.

Tyler Durden

Sun, 05/29/2022 – 15:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com