Volcker And Inflation…

Via AdventuresInCapitalism.com,

For my entire career, Paul Volcker has been deified. In fact, I cannot think of an unelected government official, since the Generals of WW2, who is held in such esteem—which may also be a function of how terrible most government functionaries are.

As JPOW suddenly pretends that Volcker was his boyhood hero, I think it’s worth re-examining Volcker’s inflation fight.

Of course, everyone knows the high-level story; Volcker broke the back of inflation by taking rates into the stratosphere, inducing a recession, taking the heat from politicians and the populace, and sticking to his principles. He had only one mission; defeating inflation. Nothing stood in his way, and he kept at it until the mission was accomplished.

As a result of Volcker’s sacrifices, we’ve since experienced four consecutive decades of economic boom. Or that’s how everyone seems to remember the situation today.

What if there were other contributing factors?

Let’s explore some of the other components that may have contributed to inflation peaking during Volcker’s tenure;

-

Oil was one of the primary causes of the 1970s inflation and everyone remembers the oil crisis. During the decade, oil ran all the way from $2 to $39. However, the flipside to this story is that with a lag, high oil prices will eventually incentivize production. The issue was that the US specifically disincentivized US producers and importers. Ronald Reagan signed an Executive Order in January of 1981 to eliminate oil price controls and then removed Jimmy Carter’s idiotic Windfall Profits Tax a few years later. As expected, global production expanded rapidly and with the removal of price controls, that production flooded into the US. By the middle of the decade, despite repeated production cuts by OPEC, there was a global glut of oil and by 1985, oil had collapsed all the way to $7. It wasn’t interest rates that made oil decline, it was government policy on the deregulation side, along with rapid production increases from non-OPEC countries.

-

President Reagan’s Economic Recovery Tax Act was signed into law in August of 1981, designed to reduce tax rates and incentivize investment by rewarding risk-taking by businesses. In particular, the Accelerated Cost Recovery System served to accelerate depreciation, reducing taxes for those that invested in productive capacity. Once again, government policy, not interest rates led to an increase in investment and ultimately supply, helping to tame inflation.

-

It wasn’t just Reagan working on de-regulation; The Staggers Act of October 1980, deregulated the railroads, The Motor Carrier Act of July 1980, deregulated the trucking industry, and the Airline Deregulation Act of October 1978 effectively deregulated transport industries. The net effect was dramatic price competition, better ability to invest and innovate, and the ability to eliminate unprofitable business that was funded by profitable business. Almost immediately after passage, pricing for transport services collapsed and the ease of transporting goods expanded.

-

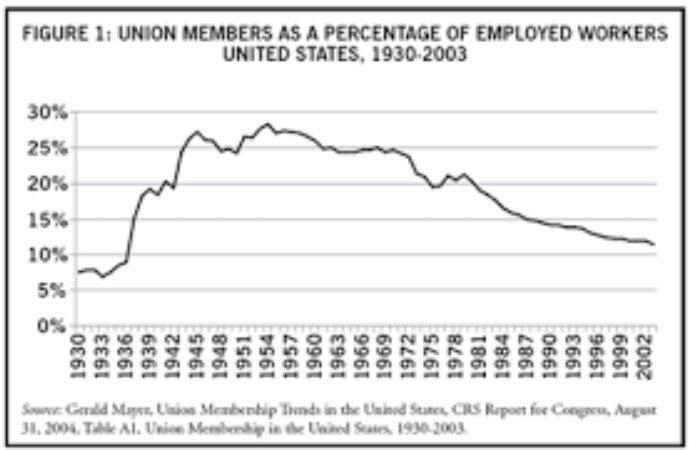

Organized labor was also dealt a near-fatal blow when Reagan fired the air traffic controllers in August of 1981. This may have reduced the wages for a generation of middle-class workers, but it sure wasn’t inflationary. It also accelerated the decline of unions which had already peaked out as a percentage of workers. More importantly, it reduced the militancy of unions and took the teeth out of their ability to disrupt businesses, leading to better efficiency and lower costs for consumers.

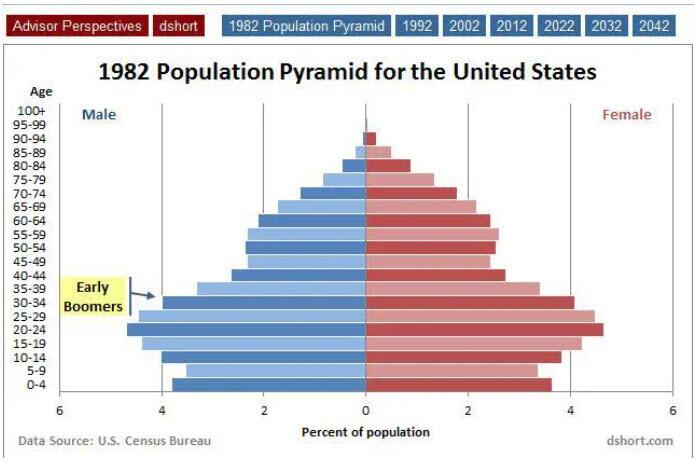

- At the same time, when it comes to macroeconomics, demographics equals destiny. In this case, Volcker simply got lucky. Think of the Baby Boom generation, the last of whom was born in 1964. By 1982, these last Boomers hit 18 and started joining the workforce. The eldest Baby Boomers, born in 1946, were already 36 by then. Look at the massive increase in workers starting in the late 1970s and into the 1980s, which tamped down wages and tamed inflation—especially as female participation in the workforce expanded dramatically. This added labor slowed a key component of the inflation.

I could continue into the weeds of the various policy changes along with a bit of luck on the demographics side, but I’ve hit enough of the high points to give you a flavor of what was afoot while Volcker was supposedly single-handedly taming inflation. What’s interesting is that despite rapidly accelerating fiscal deficits during the 1980s, inflation continued to subside. Was the decline in inflation due to a short-term spike in interest rates, mostly reversed a few years later? Or, due to longer-term policy changes that unleashed supply, while improving competition and efficiency? It clearly was a combination of the two, but I believe that far more of the credit should go to the policy side, not the monetary side.

This all has interesting implications as the policy apparatus is going haywire under the current administration.

From repeated attacks on energy, to crazy regulations designed to force people out of the labor force, to all the carbon nonsense, to the extreme fiscal deficits, to all the other asinine regulation; the policy side currently appears to be overwhelming the monetary side when it comes to inflation.

Here’s my alternative view; what if monetary actions mostly serve to impact the price of risk assets, while fiscal mostly impacts the economy’s growth rate, and government policy mostly controls for inflation? As I’ve experienced the interplay of these three factors over more than two decades as an investor, I increasingly think that this is the case. Sure, there is plenty of cross-over. For instance, the S&P wealth effect is increasingly as important for consumer spending as are interest rates, allowing home equity to get tapped. Hence the price of risk assets bleeds into the overall economy. However, I am mostly of the view that these three buckets (monetary, fiscal and policy) control for a substantial percentage of the changes in their respective key categories (risk assets, GDP and inflation), hence why inflation is now accelerating at roughly the rate of government policy mistakes. Meanwhile, the Fed will take interest rates to a level where it nearly detonates the financial system, yet it cannot impact the price of oil.

Coming full circle here, Volcker is still a hero of mine. At the time, he was one of the most hated people in our government, yet he continued forward with his rate plan because he knew it was the right thing to do. He had conviction and didn’t bend to the mob. Ultimately, he was part of the solution. I just think that our collective knowledge has evolved in a way that most people are ignoring many of the other factors that may have had a much greater role in reducing the runaway inflation of the 1970s. If we forget that tax and regulatory policy were the primary factor in reducing inflation, we are bound to repeat Carter’s inflation disaster.

* * *

If you enjoyed this post, subscribe for more at http://www.adventuresincapitalism.com

Tyler Durden

Mon, 06/13/2022 – 20:20

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com