FOMC Decision Preview: Biggest Rate Hike Since 1994 On Deck

Submitted By Newsquawk

Up Until Monday afternoon, the FOMC was been expected to hike rates by 50bps to 1.25-1.50% until the hot May CPI figures, rising consumer inflation expectations and a WSJ article, ignited a wave of 75bps calls to 1.50-1.75%. The Fed guidance initially called for 50bps (both in June and July) had the data evolved as they expected, but after the hot May data, some calls for larger hikes, a ‘Volcker moment’, fuelled speculative market activity leading into the meeting, and given a slew of publications with high-placed sources (WSJ, CNBC, Bloomberg) have come out suggesting a 75bps hike – the biggest hike since 1994 – is indeed possible on the eve of the confab, it is now seen as a base case for many…

- Barclays +75bps

- Deutsche Bank +75bps

- CapEcon +75bps

- Goldman +75bps

- JPMorgan +75bps

- Jefferies +75bps

- Nomura +75bps

- SocGen +75bps

- TD +75bps

- Wells +75bps

- BNP +50bps

- BofA +50bps

- Citi +50bps

- Credit Suisse +50bps

- HSBC +50bps

- Morgan Stanley +50bps

- StanChart +50bps

… and a certainty as per market pricing (the Fed has never hiked 100bps in the “modern” or post-Greenspan era, although it did hike 500bps in 1980 under Volcker).

Given the evolution of the data, the Fed will be expected to make hawkish adjustments to its guidance via the statement, and in Powell’s presser, some suggest another 75bps hike in July even. Furthermore, the accompanying ‘Dot Plot’ is expected to see ramped implied Fed hikes through 2023 – whispers suggest the median ’23 dot could be towards the 4% region vs March’s 2.8% forecast.

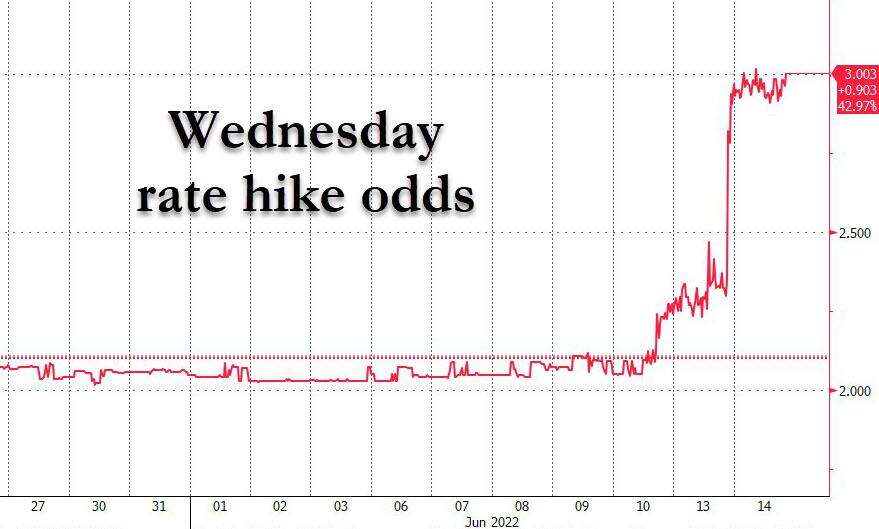

FROM 50 TO 75: Consensus had overwhelmingly called for a 50bps hike until May CPI on June 10th hit new multi-decade highs and the rise in the Uni of Michigan’s longer-term consumer inflation expectations. The tide began to turn as Barclays and Jefferies ramped their base case to a 75bps hike into the weekend, while Standard Chartered Monday said it does not “preclude a hike of 75bps or even 100bps” if the Fed sees the need for a ‘Volcker moment’. More of the Street followed suit on Monday evening after WSJ’s Nick Timiraos wrote, “A string of troubling inflation reports in recent days is likely to lead Federal Reserve officials to consider surprising markets with a larger-than-expected [75bps hike] this week”. That appeared all the more conspicuous after the journalist wrote just one day prior, “a 75bps rate hike remains unlikely because it would be a notable departure from how the central bank has conducted policy.” Money markets themselves went on to price 75bps with near certainty (see chart above).

BREAKING FROM GUIDANCE: The Fed’s guidance was indeed for 50bps in both June and July, but it did keep the door open (slightly) for larger increments if data did not evolve as they expected, which now appears to be the case. WSJ’s Timiraos said the May CPI “showed a bigger jump in prices in May than officials had anticipated.” In reference to the further rise in long-term consumer inflation expectations in the Uni of Michigan survey (3.3% from 3.0%) and short-term rise in the NY Fed survey (6.6% from 6.3%), the WSJ said that “could alarm Fed officials because they believe such expectations can be self-fulfilling.” SGH Macro’s Tim Duy writes (after previously saying such a move would stink of “panic”), “The Fed has said it will act forcefully if it thinks inflation expectations are unanchored, or about to become unanchored. Forcefully means stepping away from the reliance on forward guidance.” The strategist, who now expects 75bps, asserts, “Pushing rate hikes out into the future is not enough anymore to keep expectations in check.”

NEW GUIDANCE: Given the magnitude of moves in the front-end of the rates curve, SGH’s Duy believes “Powell will attempt to use this meeting and the press conference to regain control of the narrative.” Participants can expect hawkish language adjustments in the statement and presser. Regardless of the June hike increment, the statement will likely introduce commentary on the willingness to move faster/further if required, while Powell’s presser is expected to echo that. Meanwhile, markets are keeping a close eye out for commentary around the September meetings and beyond; indeed, part of this will be reflected in the Dot Plot. Pre-May data, several officials had publicly expressed a likely move down to 25bps hikes from September, but that seems highly unlikely now and Powell can be expected to guide closer to the market pricing of a year-end Fed Funds at 3.50-3.75%, which if the Fed hikes 75bps Wednesday, would include 50bps hikes through the remaining four meetings this year. Although that could be front-loaded, as Tim Duy notes, “assuming the Fed wants to ensure that expectations are in control, we may be looking at 75bp again in July.” Furthermore, it wouldn’t be surprising to see Powell lean into Governor Waller’s line of thinking, “not taking 50bp hikes off the table until I see inflation coming down closer to our 2% target”.

DOT PLOT: Bloomberg complied the following economist survey before the May CPI and inflation expectations surveys, thus, these can be considered somewhat stale, with informal expectations for the Fed Funds and inflation 2022/23 dots having nudged higher since the data and potentially higher unemployment and lower GDP dots as chances of a hard landing rise. Median dot expectations via Bloomberg’s June 3rd-9th survey:

- FEDERAL FUNDS RATE: exp. at 2.6% in 2022 (prev. 1.9% in Mar), 3.1% in 2023 (prev. 2.8%), 3.1% in 2024 (prev. 2.8%), 2.5% in longer run (prev. 2.4%)

- CHANGE IN REAL GDP: exp. at 2.5% in 2022 (prev. 2.8% in Mar), 2.1% in 2023 (prev. 2.2%), 2.0% in 2024 (prev. 2.0%), 1.8% in longer run (prev. 1.8%)

- UNEMPLOYMENT RATE: exp. at 3.5% in 2022 (prev. 3.5% in Mar), 3.6% in 2023 (prev. 3.5%), 3.7% in 2024 (prev. 3.6%), 4.0% in longer run (prev. 4.0%)

- PCE INFLATION: exp. at 4.8% in 2022 (prev. 4.3% in Mar), 2.7% in 2023 (prev. 2.7%), 2.3% in 2024 (prev. 2.3%), 2.0% in longer run (prev. 2.0%)

- CORE PCE INFLATION: exp. at 4.2% in 2022 (prev. 4.1% in Mar), 2.6% in 2023 (prev. 2.6%), 2.3% in 2024 (prev. 2.3%)

BALANCE SHEET: Little new is expected on the balance sheet runoff with reduced Fed reinvestments now having commenced in line with prior guidance. The only talking point to be expected is a potential nod to when/if they will commence outright sales of mortage-backed securities.

* * *

As a bonus, here is an excerpt from the latest Michael Hartnett Fund Manager Survey: how to trade the FOMC decision:

if Fed goes 50bps in June (= behind-the-curve) FMS says position deeper “risk-off” via short oil & resources (also big tech); if Fed goes 100bps (= ahead-of-curve) position “risk-on” via short US$, long EM & low quality growth stocks.

Bill Ackman agrees:

And yes, 100 bps tomorrow, in July and thereafter would be better. The sooner the @federalreserve can get to a terminal FF rate and thereafter can begin to ease, the sooner the markets can recover. https://t.co/lFDNvLl3oU

— Bill Ackman (@BillAckman) June 14, 2022

Tyler Durden

Tue, 06/14/2022 – 21:45

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com