A Multipolar Shift With Energy And Dollar Disruptions

Authored by Victor Xing via The Mises Institute,

Executive Summary

-

In the near term, China’s reopening and buying of ESPO crude would likely erode the role of Brent & energy indices

-

Gulf nations envision the scope of petroyuan to be on par with demands for Chinese goods & technology transfer

-

Rising yuan payments for Russian energy and more China-Gulf bilateral trade imply future dollar demand decline

-

In the long term, more local currency trade settlements would erode dollar flows and Federal Reserve’s influence

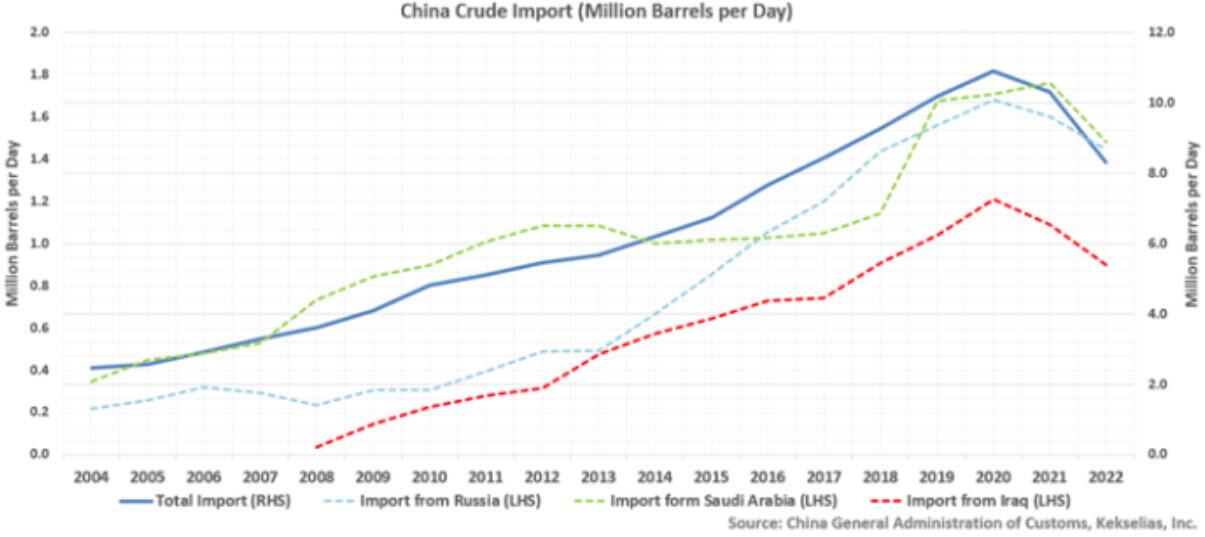

China’s yuan denominated Russia crude rivals Saudi imports

In 2021, China imported 79.6 million tons of crude from Russia (1.6 million barrels per day) vs. 87.6 million tons from Saudi Arabia (1.8 million barrels per day). These two producers respectively accounted for 15.5% and 17.1% of China’s total crude import at 513.2 million tons (10.3 million barrels per day), which was near Saudi Arabia’s total 2021 output of 515 million tons. At present demand, China is both Saudi Arabia and Russia’s top energy customer:

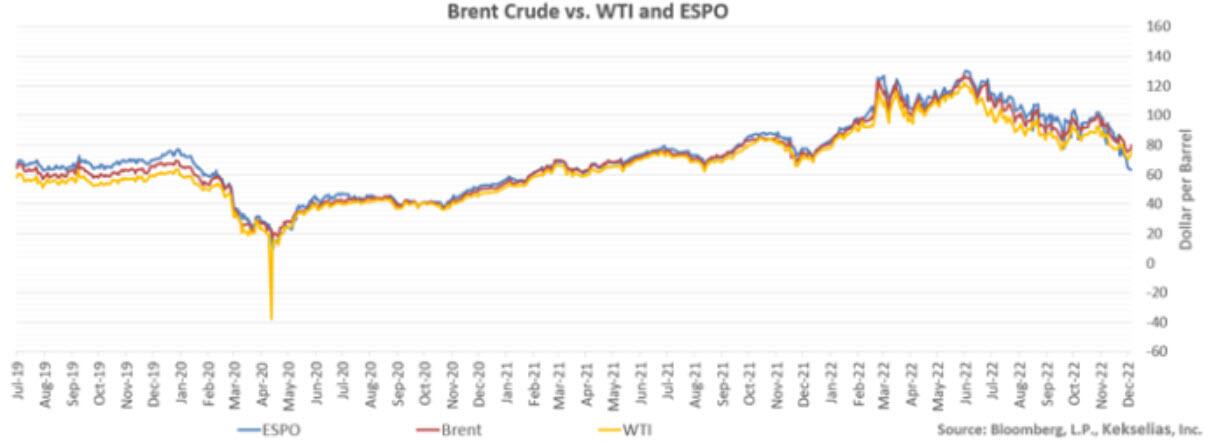

Following the onset of the war in Europe, rising yuan-denominated Russian crude export and omission of Russia’s Eastern Siberia Pacific Ocean (ESPO) grade crude from broader commodity indices would likely erode Brent crude’s role as a global oil benchmark. Investors focusing solely on Brent may overlook key market shifts.

China’s energy demand was subdued in 2021 and 2022 due to pandemic restrictions, and a broader economic reopening would likely accelerate demand for both Russian and Saudi energy products (by 2+ million barrels a day). However, Brent would only reflect part of the demand surge due to ESPO shipment and direct Russo-China pipeline flows. In 2022, sale of Russian pipeline crude to China totaled 33.3 million tons by October (nearly half of Russian flows to China over the period). Given crude pipelines would not use EU or G7 insurance services, the products would trade at uncapped prices into 2023.

Meanwhile, seaborne ESPO crude traded at $79 per barrel in Asian markets after the G7 + EU price cap came into effect at $60 per barrel, because the presence of a Russian tanker fleet that uses its own insurance.

The Bloomberg Commodity Index, as well as its futures instruments, uses WTI and Brent crude to construct its crude constituents, and it would underrepresent energy market developments in Asia if ESPO decouples from Brent:

Currently, yuan-denominated purchases of Russian crude uses a quasi-barter system: Chinese buyers would settle Russian crude purchases in yuan, and Russia would subsequently use the yuan to purchase Chinese technology products.

This is the same petroyuan model discussed at the China-Saudi Summit.

Saudi-China Summit and long-term impacts

A key market focus on the Saudi-China Summit attended by Crown Prince Bin Salman and President Xi was petroyuan. Xi proposed making “full use of the Shanghai Petroleum and National Gas Exchange as a platform to carry out yuan settlement of oil and gas trade.” A Saudi source previously said a decision to sell small amounts of oil in yuan to China could make sense in order to pay for Chinese imports directly, but “it is not yet the right time” to take the step.

This ambiguous stance preserved policy option for the Kingdom, for the Saudis do not see the yuan as an alternative reserve currency as Russia does. Riyadh, like Hong Kong, pegs its currency to the dollar, and it would require an ample dollar reserve to defend the riyal. As long as this system persists, Saudi Arabia would use petrodollar as a liquidity source, and it would reinvest reserves in interest-bearing dollar-denominated assets such as U.S. Treasury securities or corporate bonds. This supports the dollar and contributes to easier dollar-based financial conditions by boosting dollar asset prices. Ultimately, the petrodollar system plays a role to elevate the Federal Reserve as the dollar system’s central bank that affects global financing costs.

Yet, Saudi Arabia’s willingness to consider a system modeled after yuan-based Russian crude trade reflects its pragmatic considerations: it creates an incentive for Beijing to broaden economic ties with Riyadh. Greater the overall bilateral trade in yuan, greater the Kingdom’s demand for renminbi to pay for Chinese goods and technology, and petroyuan would fulfill a similar purpose as petrodollar to supply Riyadh with a non-dollar invoicing currency.

Overtime, greater the Saudi-China bilateral trade, greater the likelihood of more crude transactions settled in yuan, thus smaller the role of the dollar (and Fed policy) on global asset markets. While petroyuan would hardly replace petrodollar given its limited scope, less dollar in commodity settlement would result in less reinvestment of dollar reserves into dollar assets. This has ramifications from U.S. fiscal policy (less demand for dollar debt) to U.S. fixed income and equity markets.

Combined with India’s work on rupee transactions with Russia, a slow grind toward a multipolar (fragmented) world would likely weaken the dollar and erode existing asset correlation paradigms to create new market opportunities.

Tyler Durden

Sat, 12/31/2022 – 21:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com