Lower Stock Prices Are The Fed’s Goal

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

You read that right, the Fed wants lower stock prices.

Fed members will not say it as bluntly as we do in our title. But they have a long-held belief that stock prices directly impact the economy and, therefore, inflation. Thus, in the Fed’s efforts to quell inflation, it makes sense that they are likely using their stock market lever, specifically lower stock prices, to help improve the efficacy of monetary policy.

Before we delve into recent Fed comments about asset prices and describe the groundwork that Ben Bernanke laid for the Fed’s stock market theory, we share a quote of Fed Chair Janet Yellen from September 2016:

“It could be useful to be able to intervene directly in assets where the prices have a more direct link to spending decisions.”

December 2022 FOMC Minutes

Within the minutes of the December 15, 2022 FOMC meeting comes the following statement :

Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.

More straightforwardly, financial markets are an important way monetary policy is transmitted to the broader economy. As such, higher stock prices (“an unwarranted easing of financial conditions”) driven by a belief the Fed will pivot to lower rates make it more challenging for the Fed to tackle inflation.

In lay terms, lower stock prices can help the Fed get inflation back to its 2% objective.

Jerome Powell and other Fed members have made similar statements. For example, on Friday, August 26, 2022, Powell made an exceptionally hawkish speech about raising interest rates. The S&P 500 fell over 3% that day as investors expected a more market-friendly tone. On the following trading day, Minnesota Fed President Neel Kashkari responded:

I was actually happy to see how Chair Powell’s Jackson Hole speech was received.

Kashkari is cheering on lower stock prices!

Ben Bernanke Coins the Wealth Effect

In 2003 Ben Bernanke laid the groundwork for the Wealth Effect. His theory associates stock prices with the transmission of monetary policy to the economy.

In a speech entitled Monetary Policy and the Stock Market: Some Empirical Results Bernanke states:

The logic goes as follows: Easier monetary policy, for example, raises stock prices. Higher stock prices increase the wealth of households, prompting consumers to spend more–a result known as the wealth effect. Moreover, high stock prices effectively reduce the cost of capital for firms, stimulating increased capital investment. Increases in both types of spending–consumer spending and business spending–tend to stimulate the economy.

Bernanke argues that additional wealth resulting from stock market gains results in more household spending. While he doesn’t say it in this speech, the Wealth Effect also works in reverse!

Policy and Stocks are a Two-Way Street

Easy Fed policy, including lower rates and QE, tends to correlate with higher stock prices. Equally important and apropos for today, higher rates and QT are associated with lower stock prices.

The graph below quantifies monetary policy to show the correlation between stock prices and the degree of policy. The degree of Fed policy (red/green) is derived from the level of real Fed Funds and recent changes in the Fed’s balance sheet.

It’s not a perfect indicator, but you can generally see tightening policy (red) led to the significant drawdown in 2008, the 2020 decline, and the recent selloff. Conversely, stocks often trend upward when an easy Fed policy (green) is in place.

Inflation is a function of the supply and demand for goods and services. The Fed holds minimal sway over the supply side of the equation. However, they can, directly and indirectly, influence consumer and corporate demand. Not only do stock market gains or losses influence spending and investment, but interest rates significantly impact demand for specific items such as real estate and autos.

The Fed, aware it has little influence on supply, must target demand to reduce inflation. On November 30, 2022, Powell made it clear that the Fed’s objective is to weaken demand to reduce inflation.

We are tightening the stance of policy in order to slow growth in aggregate demand. Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.

Controlled Burn of Stocks

Between higher interest rates and QT, the Fed is trying to cool demand and bring inflation to its target. Based on numerous comments like those shared, it also appears the Fed is targeting stock prices to help reduce inflation.

The Fed does not want to plunge stock prices as it could result in significant financial disruptions in which they could quickly lose control. We believe they want lower trending stock prices with controlled volatility until they meet their goals. Hawkish rhetoric, higher interest rates for longer, and QT can help them on their quest. The graph below shows volatility has been higher than average during the recent decline, but it did not spike as in the disorderly declines of 2008 and 2020.

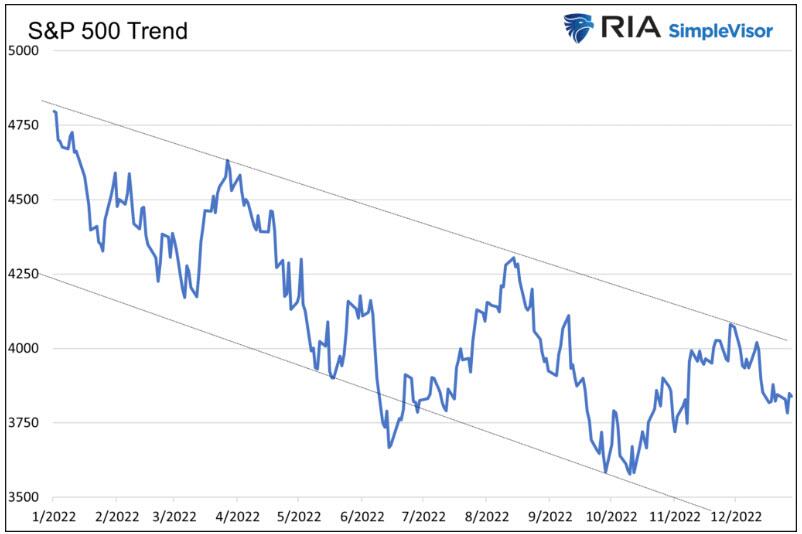

The Fed likely wants a controlled, low-volatility burn on stock prices. If prices gravitate too far upward or downward from the trend channel, the Fed can adjust liquidity via the combination of QT and its Reverse Repurchase Agreement (RRP) program. Such policy management might explain the clean channel the S&P 500 followed throughout 2022.

Our article S&P 3500 By Year End details RRP and Fed-generated liquidity.

Summary

Bernanke and Yellen acknowledge that influencing stock prices is crucial for the Fed to help them accomplish their goals. Powell is following in their footsteps and, in our opinion, trying to push stock prices lower to help ensure inflation is slayed.

Given inflation remains well above the Fed’s target, we suspect the Fed will try to guide stock prices lower in the foreseeable future. In doing so, the Fed may get inflation back to target and bring valuations back to historical norms as a side benefit.

The risk the Fed faces is that volatility spikes and stock declines get out of hand. Such would not only create financial instability but could significantly hamper economic activity. Likely, inflation would turn to deflation in the said scenario and allow the Fed to get back to its preferred playbook of pumping stocks higher to boost economic activity and get inflation up to its target.

The road ahead for stocks is likely lower until inflation is tamed. If the Fed is successful in a controlled burn of stock prices, we should see rallies from the lower range of the trend channel and declines from the upper end. Both extremes may very well present trading opportunities.

In market jargon, expect pumps and dumps as the stocks grind lower.

Tyler Durden

Wed, 01/11/2023 – 08:20

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com