Goldman: The Case For A Hard (Or Soft) Landing

Optimism is increasing on Wall Street, with investors hoping for a “soft landing” in the economy.

“David Kelly, the chief global strategist at JPMorgan Asset Management, is betting that inflation will continue to ease in 2023, helping the U.S. economy to narrowly escape a recession. Ed Yardeni, the longtime stock strategist and founder of his namesake research firm, is putting the odds of a soft landing at 60 percent based on strong economic data, resilient consumers, and signs of tumbling price pressures,” reported Bloomberg.

As Lance Roberts recently explained, the hope is that despite the Federal Reserve hiking rates at the most aggressive pace since 1980, reducing its balance sheet via quantitative tightening, and inflation running at the highest levels since the 1970s, the economy will continue to power forward.

Is this a possibility, or is the “soft landing” scenario another Fed myth?

To answer that question, we need a definition of a “soft landing” scenario, economically speaking.

According to a definition by Investopedia, “A soft landing, in economics, is a cyclical slowdown in economic growth that avoids a recession. A soft landing is the goal of a central bank when it seeks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation without causing a severe downturn.”

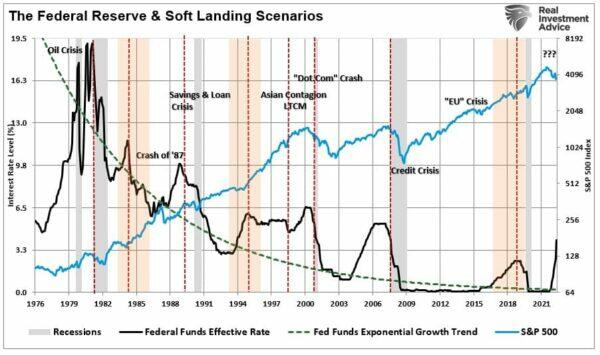

The term “soft landing” came to the forefront of Wall Street jargon during the tenure (1987–2006) of former Fed chair Alan Greenspan. He was widely credited with engineering a soft landing in 1994–95. The media has also pointed to the Federal Reserve engineering soft landings economically in both 1984 and 2018.

The chart below shows the Fed rate-hiking cycle with soft landings notated by orange shading. I have also noted the events that preceded the “hard landings.”

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

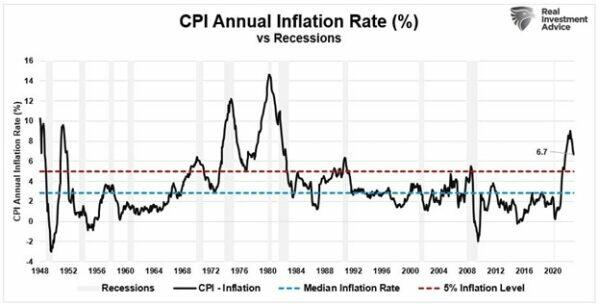

There is another crucial point regarding the possibility of a soft landing. A recession, or “hard landing,” followed the last instances when inflation peaked above 5 percent. Those periods were 1948, 1951, 1970, 1974, 1980, 1990, and 2008. Currently, inflation is well above 5 percent throughout 2022.

(Source: Federal Reserve Bank of St. Louis / Refinitiv chart by RealInvestmentAdvice.com)

Could this time be different? Absolutely, but there is a lot of history that suggests otherwise.

Furthermore, while the technical definition of a soft landing is “no recession,” if we include crisis events caused by the Federal Reserve’s actions, the track record becomes worse.

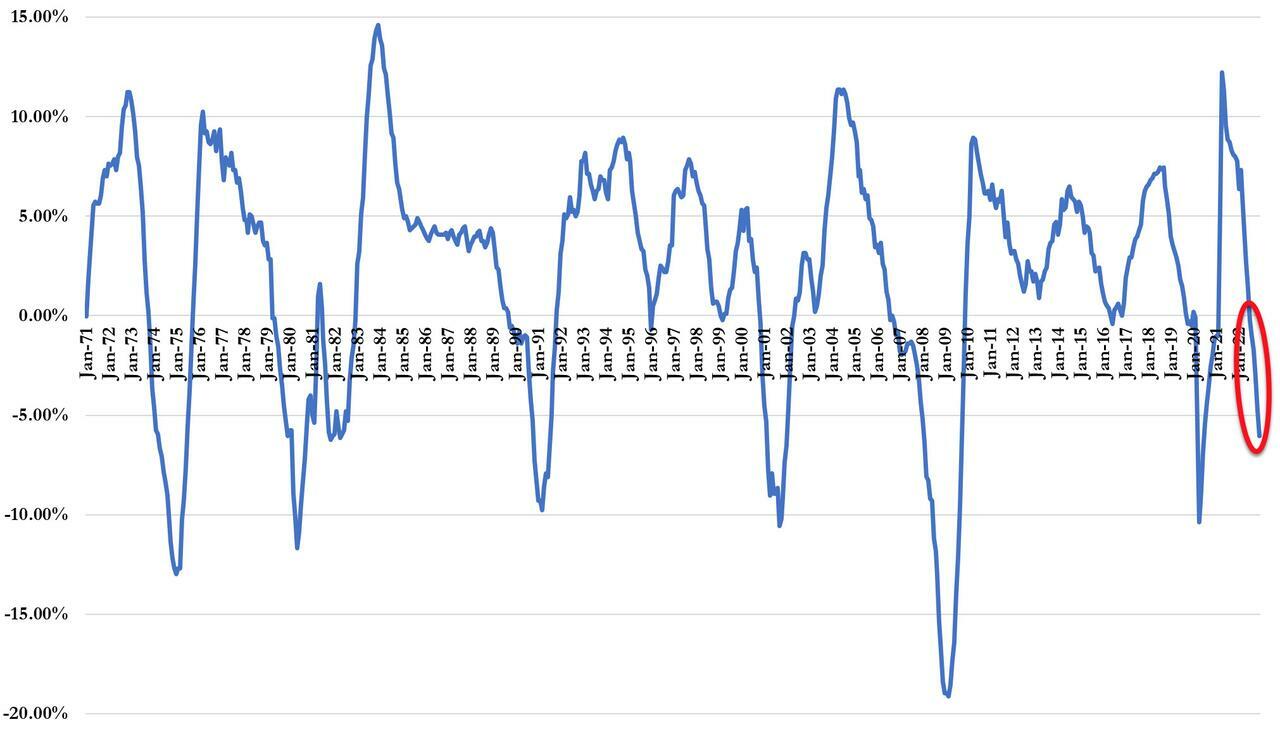

Bear in mind also that it is the labor market alone that is holding up the economic ‘signals’ as ‘soft’ survey and ‘hard’ industrial data is sliding significantly…

…and Leading Economic Indicators are screaming ‘hard landing’…

As noted above, there were three periods where the Federal Reserve hiked rates and achieved a soft landing, economically speaking. However, the reality was that those periods were not pain-free events for the financial markets.

Goldman Sachs notes in its latest ‘Top of Mind’ report, there are plenty of ‘experts’ on either side of the ‘soft’ vs ‘hard’ landing question:

Soft Landing

“I do continue to believe that there’s a path to a soft, or soft-ish, landing... And I think the path is pretty clear… We see inflation and, you know, the goods inflation get better, housing services inflation gets better, and the labor market softens but doesn’t go into recession.”

– Jay Powell, Federal Reserve Chair (Brookings Institution interview, December 2022)“The probability of a soft landing has increased compared to where it was in the fall of 2022, where it was looking more questionable… And the reason I think that the prospects for a soft landing have increased is that the labor market has not weakened the way many had predicted… and growth levels rebounded from weakness.”

– James Bullard, President, Federal Reserve Bank of St. Louis (CFA Society speech, January 2023)“My own prediction is indeed for a softish landing: inflation does seem to be coming down, and while we might not completely avoid a recession, if we have one it will probably be mild.”

– Paul Krugman, Nobel Prize winning economist (New York Times column, January 2023)“We might see, actually, the job market loosen up dramatically… but that GDP grows much faster than most people think and we have a chance, if the Fed pivots, to really avoid a recession and have a good year for profits.”

– Jeremy Siegel, Professor, Wharton (CNBC interview, December 2022)“All the signs are pointing to a higher, not a lower, probability of a soft landing… It may still not be more than 50-50. But 50-50 is looking better than it was a few months ago.”

– Alan Blinder, former Federal Reserve Vice Chair (Fortune interview, January 2023)“The deeper I look into the bowels of last week’s job market data, the more I think we can skirt a recession…”

– Mark Zandi, Chief Economist, Moody’s (Twitter, January 2023)

Hard Landing

“One has to be careful of false dawns… I would stick with my view that a recession this year is more likely than not.”

– Larry Summers, former Secretary, US Treasury (Bloomberg interview, January 2023)“A recession is pretty likely just because of what the Fed has to do.”

– Bill Dudley, former President, NY Fed (Bloomberg interview, January 2023)“A recession does appear to be the most likely outcome at this time. While the last two monthly inflation reports did show a deceleration in the rate of price increases, it does not change the fact that prices are still increasing… Wage increases, and by extension employment, still need to soften further for a pullback in inflation to be anything more than transitory.”

– Alan Greenspan, former Federal Reserve Chair (Advisors Capital note, December 2022)“I don’t want a recession. I hope we luck out with a soft landing but I just think a soft landing is a hard thing to achieve… It’s easy to avoid a recession, its hard to avoid a recession while bringing inflation down.“

– Jason Furman, former Director, National Economic Council of the US (CNBC interview, January 2023)“I think either it’s going to be a borderline or very mild recession, or it could be a deeper one… There has been a little bit of good news recently, but the markets maybe are overplaying it, wages have a long ways to go. Wages have not kept up with inflation.”

– Kenneth Rogoff, Professor, Harvard University (CNBC interview, January 2023)“[We] are predicting the recession to start mid-year and it’s because we think the Fed is continuing to push on the QT accelerator and continuing to drive down inflation as well as labor costs… The more quantitative tightening that we see, the more we see the risk of a more prolonged and deeper recession.“

– Anne Walsh, CIO, Guggenheim Partners (CNBC interview, January 2023)

The Case for a Hard Landing…

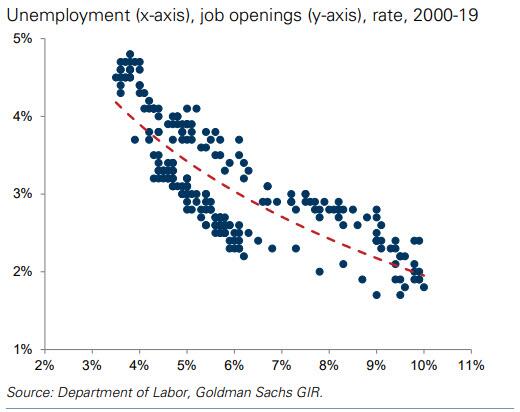

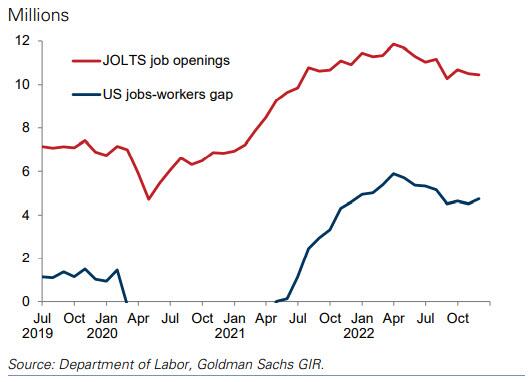

Historically, a substantial decline in job openings – a key requirement to tame the current bout of inflation – has never occurred without a sharp rise in unemployment…

…and since 1949, every time the three-month moving average of the unemployment rate has risen by 0.5pp+ relative to its low during the previous 12m, a recession has ensued (Sahm Rule)

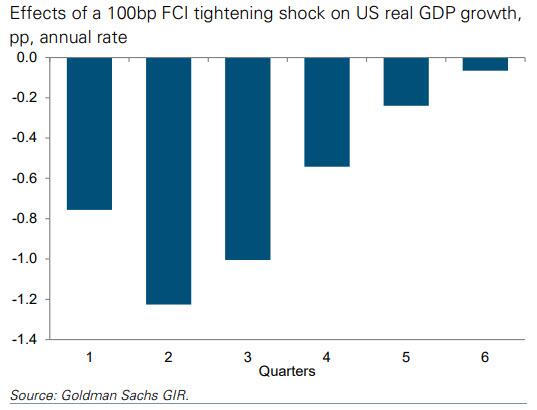

Financial conditions tightened substantially over the course of 2022…

…and macro models suggest that monetary policy, which affects the economy through financial conditions, affects the level of GDP with a relatively long lag.

Inflation has declined, but remains well above target…

…and while wage growth has moderated, it remains high

The Case for a Soft Landing…

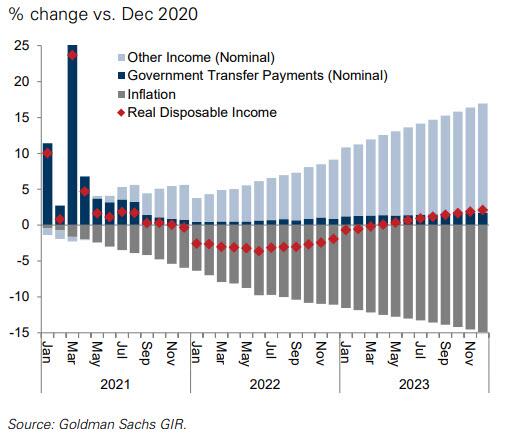

We expect solid growth in real disposable income this year…

We find that the lags from financial conditions on GDP growth are relatively short, suggesting that the US economy has already bore the brunt of the 2022 tightening in financial conditions…

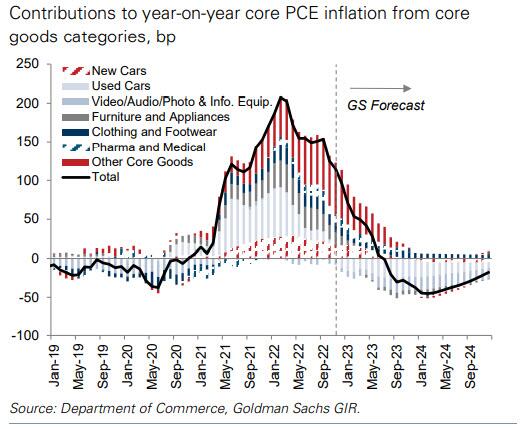

We expect core goods inflation to turn negative this year…

The jobs-workers gap has so far shrunk mainly through a decline in job openings without a sharp rise in the unemployment rate, and we expect this pattern to continue…

The best alternative measures of new lease rent growth have slowed, and show signs of further slowing ahead…

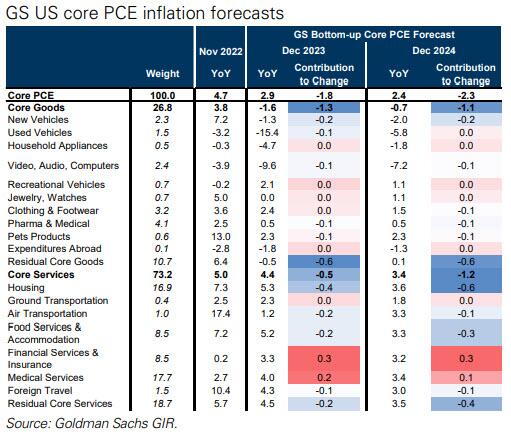

Accordingly, we expect core PCE inflation to decline to 2.9% by YE23…

With those thoughts in mind, Goldman opines on how will the market react to a ‘soft’ (no recession) landing or a hard (recession) landing…

-

The avoidance of a US recession and an improving global growth picture would push global equities higher. US 10y Treasury yields would be expected to rise by around 40bp, and bund yields potentially by more. Shorter-dated rates would also potentially climb higher as the market backs away from the deep rate cuts it has begun to price. Non-US equities would be expected to outperform, both in local and USD terms. Commodities would be expected to rise significantly, particularly under the more generous assumptions about China pricing. The USD would broadly weaken but would strengthen against JPY and weaken less versus EUR, with cyclical currencies performing strongly. A “Goldilocks” version of this outcome in which rapid inflation declines lead to more Fed relief despite improving growth would mitigate upward yield moves, provide a further tailwind to global equities, and reinforce USD weakness.

-

In the case of a recession, US equities would be expected to fall significantly, with cyclical equities underperforming, and credit spreads widening sharply. Non-US equity markets would decline too, but to a lesser degree. US yields would decline along the curve, with the 10-year Treasury yield falling by nearly 60bp and smaller predicted declines in bund yields. Front-end rates would likely fall by more, implying yield curve steepening. In FX, cyclical and EM currencies would mostly weaken against the USD, but EUR, CHF, and, most significantly, JPY would be expected to strengthen against the USD. Commodities would generally weaken. A “hawkish recession” – in which inflation proved stickier – would be expected to lead to larger declines in risky assets, more limited declines in yields, and broader USD strength.

So, with all that said, RealInvestmentAdvice.com’s Lance Roberts notes that Powell’s recent statement during a speech at the Brookings Institution was full of warnings about the lag effect of monetary policy changes. It was also clear that there is no pivot in policy coming anytime soon.

When that lag effect catches up with the Fed, a pivot in policy may not be as bullish as many investors currently hope.

We doubt a soft landing is coming.

Tyler Durden

Mon, 01/30/2023 – 06:55

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com