Beware: The Fed Thinks It’s Different This Time

By Dhaval Joshi of BCA Research

The four deadliest words in life are ‘it’s different this time’. Anyone who utters these words usually ends up being carried away, feet first. So, it’s especially worrying that the ‘it’s different this time’ narrative is coming from none other than the world’s most important central bank, the US Federal Reserve.

Through the past 75 years, the US unemployment rate has either not gone up meaningfully, or it has gone up by a lot. The US unemployment rate has never gone up by ‘just’ 1 percent. Yet when asked at last week’s press conference if the cost of killing inflation could be kept to the unemployment rate going up by ‘just’ 1 percent, Jay Powell answered:

“Yeah, absolutely it’s possible… this is not a standard business cycle where you can look at the last ten times there was a global pandemic… it is unique”

The Sequence Of Events Leading To Recession Is Always The Same

It’s not every day that there’s a global pandemic. Then again, it’s not every day that the Bretton Woods monetary system collapses, as happened prior to the 1970s recessions. It’s not every day that the mother of all stock market bubbles bursts, as happened prior to the 2001 recession. And it’s not every day that there’s a nationwide housing bust in the US, as happened prior to the 2008 global financial crisis.

The backdrop to every business cycle is ‘different this time’. But the chain reaction that takes the economy into recession is always the same.

First, sales decline relative to wages.

Second, firms’ profits plunge.

Third, firms lay off workers.

Fourth, at a tipping-point of a 0.5-0.6 percent rise in the unemployment rate, consumers take fright and increase their precautionary saving, and banks slow their lending.

Fifth, this further slowdown in spending is the self-reinforcement which causes the unemployment rate to go up by at least 2 percent. Meaning, a recession.

This chain reaction explains why the US unemployment rate is non-linear: it either doesn’t go up meaningfully, or it goes up a lot. If the chain reaction breaks down before stage four, then unemployment doesn’t rise meaningfully, but if the chain reaction gets to stage four, then unemployment rises a lot.

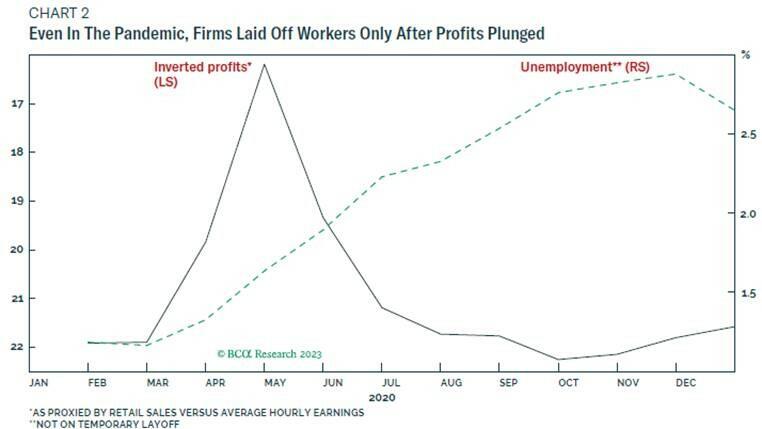

The latest employment data shows that the US jobs market remains red hot, but this should come as no surprise. To repeat, firms only lay off workers after their profits plunge. Not before. So far, the chain reaction is only at stage two. Sales are declining relative to wages, but economy-wide profits have not declined enough to trigger widespread layoffs.

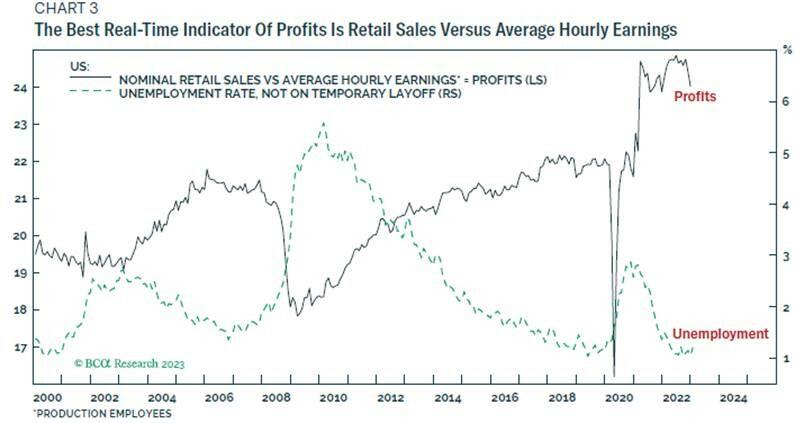

Only if we get to stage four in the chain reaction will we know whether it’s different this time. But as I explained in The US Approaches Its Event Horizon, to get to stage four, the best real-time indicator for profits – retail sales versus average hourly earnings – must decline by 3-4 percent. So far, this indicator has declined by 3 percent, so it is at the cusp of unleashing stage three and four of the chain reaction. Hence, we await next data release on Feb 15th as a crucial signpost.

So Far, It’s Not Different This Time

It rarely is different this time. Yet we should keep an open mind. There is a first time for everything. The Fed is betting that it’s different this time because the self-reinforcement in stage five of the chain reaction will be much weaker this time. So, rather than rising by well over 2 percent, the unemployment rate will rise by just 1 percent. To repeat, this outcome is unprecedented. But given this outlook, says Powell, “I don’t see us cutting rates this year.”

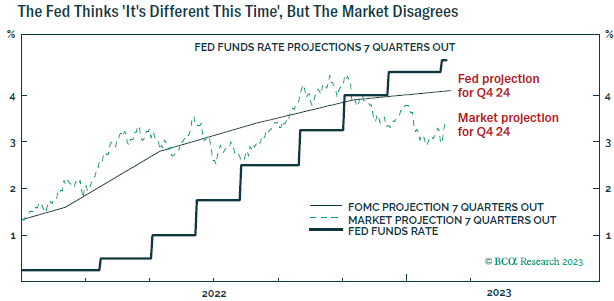

After the red hot jobs report for January, the market broadly agrees. Projections for the fourth quarter of 2023 show that both the Fed and the market expect one to two further quarter-point hikes, and then a pause, but no rate cuts.

Projections for the fourth quarter of 2024 are more interesting. Given the Fed’s outlook for the unemployment rate to rise by just an unprecedented 1 percent or so, it is projecting the policy rate to be only modestly lower than today. Meanwhile, the market is projecting 125 bps lower than today.

Therefore, if you believe the Fed is right, and it really is different this time, the investment recommendation would be to sell the less optimistically priced November 2024 Fed funds future (FFX24), or more liquid close equivalent FFZ24.

What if you believe that the Fed is wrong, and that it’s not different this time – does the less optimistic market pricing for 2024 already discount this? No, in every cycle, interest rates climb up the stairs, but fall down the elevator shaft. Meaning that once in a recession, the pace of cutting rates is always aggressive. In 2001, rates collapsed at a pace of 150 bps per quarter, in 2008 by 100 bps per quarter, and in 2020 – even starting from a very low peak of 2.5 percent – by 80 bps per quarter.

Therefore, if this time is not different, the unemployment rate will rise by well over 2 percent, killing wage inflation, and unleashing the typically aggressive rate cutting that follows a recession. In this case, the pricing of the late 2024 Fed funds futures is not pessimistic enough, and the investment recommendation would be to buy them.

So far, there is nothing to suggest that it’s different this time. To repeat, the US jobs market remains strong because economy-wide profits have not declined enough to trigger widespread layoffs. We will only discover if it’s different this time after profits plunge, and we won’t have to wait long to find out.

We must watch the data and keep an open mind. But until the data proves that this time is different, it most likely is not. Therefore, the recommendation is to buy the November 2024 Fed funds future (FFX24), or more liquid close equivalent FFZ24.

It also implies staying overweight bonds versus equities on a 6-12 month horizon.

Tyler Durden

Thu, 02/09/2023 – 15:35

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com