US Tech’s Dominance At Risk From China’s Reopening

Authored by Simon White, Bloomberg macro strategist,

The US tech sector, as well as the dollar and Treasuries, will come under pressure as China’s reopening gathers pace.

In The Sun Also Rises, Ernest Hemingway memorably expressed the process of going bankrupt: “first gradually, then suddenly.” It is also an apt description for the way China reopened after Covid. After incrementally easing social restrictions through last year, the country abruptly dropped them all in December.

China had also been slowly easing financial conditions, but policies designed to allay pressure on the property market and new liquidity were unable to “bite” while the country was in lockdown.

Now, though, monetary conditions are showing a sudden easing shift, which will further pressure the dollar, while eventually driving a cyclical uplift in US price growth, ending the inflation-sensitive tech sector’s recent outperformance.

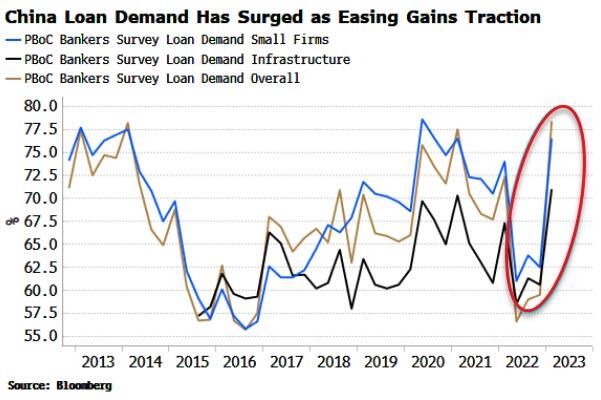

This marked change can be seen in loan demand in China, which had slumped during the pandemic, and has now surged back close to its pre-pandemic highs.

This is a clear sign that China’s easing policies are beginning to gain traction. The nation’s command-and-control economy means that new credit often does not get allocated to the parts of the economy that need it most. Required-reserve-ratio and lending-rate cuts can be blunt instruments that do not automatically help the typically more credit-starved private-business and household sectors.

These were effectively repressed through the pandemic as China’s Covid support focused not on consumers, as in the US, but on state-owned firms. Exports surged, but imports flat-lined as the biggest net importer – the household sector – saw its income fall.

Household loans and demand for loans from small businesses are now rising. This is beginning to be reflected in a burgeoning increase in M1 – the best leading indicator in China of an upturn in economic growth. Easing is finally reaching where it’s needed most.

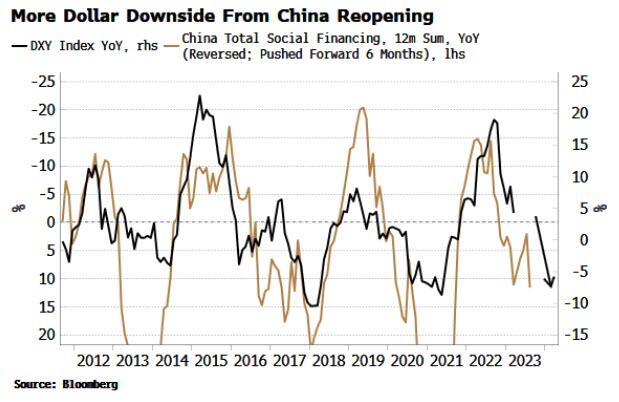

A cyclical credit-driven upturn in China also points to a weaker dollar. This is because non-US regions, principally Europe, as well as Australia, disproportionately benefit when credit in China is expanded. The recent rise of TSF (Total Social Financing) in China points to further weakness in the DXY, as shown in the chart below.

But the impact of China’s easing is not restricted just to the dollar. It is also likely to cause the fall in US inflation we have seen since last summer to level off, or even lead to a renewed rise.

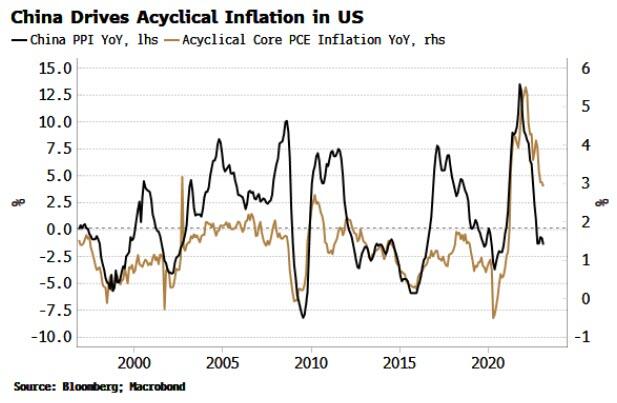

Inflation in the US can be broken into cyclical and acyclical components. The cyclical parts are those most sensitive to the Fed’s monetary policy, while the remaining acyclical ones are mainly driven by global inflationary forces. In fact, we find that acyclical inflation in the US is primarily influenced by PPI in China.

Moreover, as cyclical inflation remains near its highs, the fall in acyclical inflation – in other words, Chinese PPI – has been responsible for the fall in headline inflation in the US (see chart below).

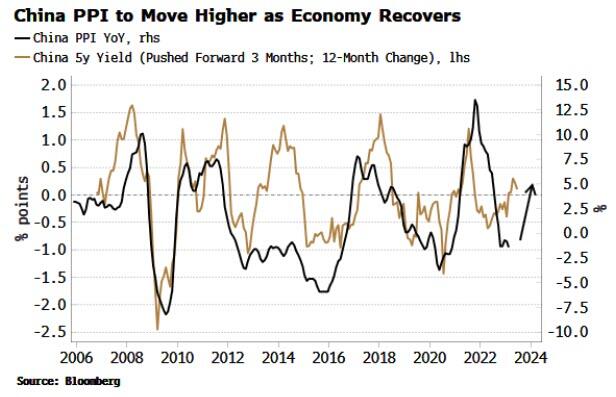

The upturn in China strongly hints that inflationary forces in China will re-appear as easing gathers pace, with the increase in its bond yields a good indication that PPI will soon start rising.

Thus the fall in headline inflation will probably peter out – or even partially reverse – as acyclical inflation likely starts rising again, even if cyclical inflation starts to fall as the Fed’s rate hikes take effect.

This would have implications for the impressive tech rally we have seen in the US this year. Stocks there are behaving as if inflation were yesterday’s problem. High-duration sectors, such as tech, have been leading the rally, while low-duration sectors such as energy and utilities have fallen by the wayside.

That would quickly come undone if the projected path of falling inflation were to be upset by China’s reopening.

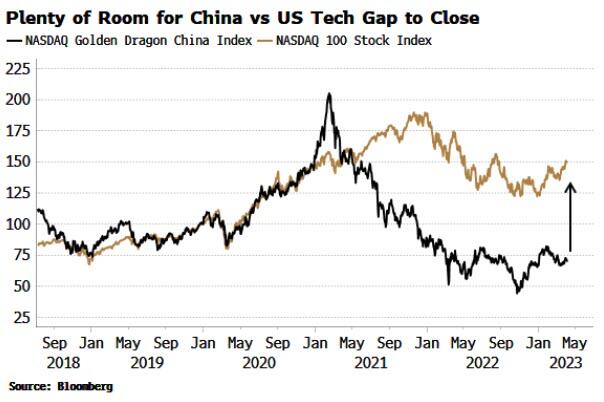

China’s tech sector faced a savage decline through 2021 and 2022. The pandemic and a crackdown on tech companies caused an almost 80% drawdown in the sector.

But as easing permeates through the economy, and China pulls back on its crackdown, the country’s tech sector is poised to continue its recovery.

Indeed, as inflation knocks tech back in the US, there is a big gap for China’s tech firms to fill versus the US’s. As the chart below shows, the two sectors moved almost in lockstep until early 2021.

The return of inflation is also a risk for longer-term Treasury yields. If it became clear that inflation was not going to return to target and instead remain sticky, bond holders would be more likely to demand greater compensation through an increase in term premium. This would mean a structural rise in long-term bond yields and a weaker transmission mechanism between Fed policy and the wider economy.

There are the usual geopolitical risks to consider, such as tensions over Taiwan and the US-China relationship. Nevertheless, a weaker dollar, China tech’s outperformance and the eventual underperformance of longer-term USTs are three likely consequences of China’s great, but long-delayed, reopening.

Tyler Durden

Thu, 04/06/2023 – 09:35

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com