Fed Funds Futures Are Unreliable – Expect The Unexpected Again

Authored by Michael Lebowtiz via RealInvestmentAdvice.com,

The 2024 Fed Funds futures contracts imply that the Fed will only cut interest rates slightly between now and the summer of 2024. If the Fed Funds forecast proves correct, then it’s highly likely the yield curve will remain inverted and or longer-term yields will rise sharply. Pick your poison. Both will cause economic weakness. Why? As we wrote in Is this Inversion Different, the shape of the yield curve has a significant influence on bank lending and, therefore, economic growth. And no, this inversion is not different despite what the media may say.

This article updates Investors Are Grossly Underestimating the Fed, an article from 2019 that quantifies how Fed funds futures traders fare at forecasting short-term interest rates.

With the recent Fed pause in rate hikes comes a growing likelihood that Fed Funds are at or near their highs for this cycle. The market and Fed now believe current levels of rates will stay with us for an extended period. It could be, but history tells us to ignore Fed and market forecasts and start anticipating a rate-cutting cycle.

Key Takeaways

-

The market has underestimated the Fed every time it cuts or hikes rates meaningfully.

-

The Fed Funds futures market and the Federal Reserve believe rates will stay around current levels for almost a year.

-

Don’t be surprised if the Fed lowers the Fed Funds rate by 2-3% lower within a year.

Fed Funds Futures Predictability

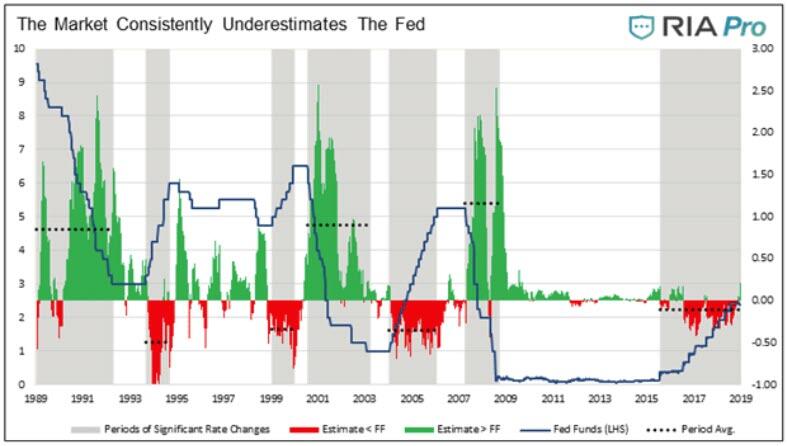

The graph below, from our article mentioned above, Investors Are Grossly Underestimating the Fed, compares the difference between what the six-month continuous Fed Funds futures contract expected in six months and the Fed Funds rate that came to fruition six months later. As shown in green, Fed Funds traders consistently underestimated how much the Fed would cut rates during the 1990, 2001, and 2008 recessions by 2.0% to 2.5%.

Professionals were slightly better when the Fed was hiking the Fed Funds rate. During these periods shaded in red, they were short by about .50% to 1.00%.

In 2019 we opined:

If the Fed initiates rate cuts and if the data in the graphs prove prescient, then-current estimates for a Fed Funds rate of 1.50% to 1.75% in the spring of 2020 may be well above what we ultimately see. Taking it a step further, it is not farfetched to think that the Fed Funds rate could be back at the zero-bound, or even negative, at some point sooner than anyone can fathom today.

In 2019, we had no idea a pandemic would devastate the economy. But we did warn that Fed Funds could be at zero percent sooner than anyone expected. Such proved to be true.

Fed “Dot Plot” Forecasts Are Unreliable

As we will discuss, we updated the initial analysis by shifting from the six-month Fed Funds contract to the one-year contract. We did this because the Fed, via their “dot plot” expectations and various speeches, imply that Fed Funds will likely stay near current levels for over a year.

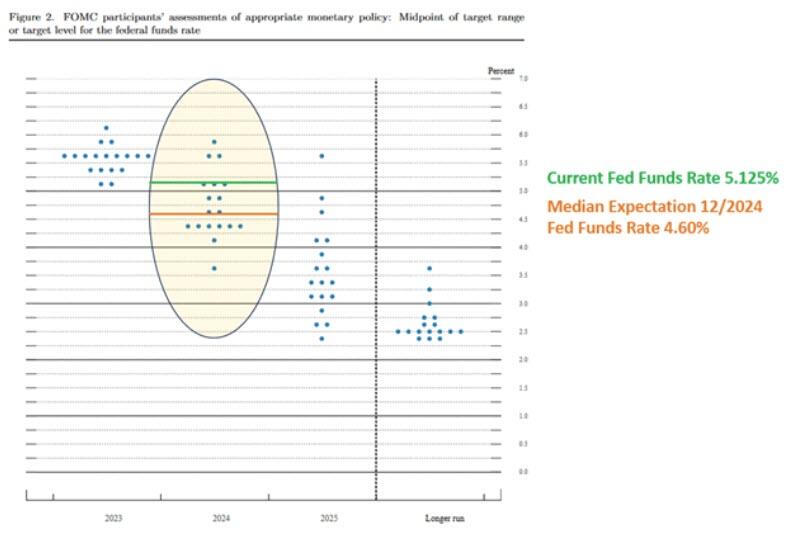

The “dot plot” graph below shows where the 18 FOMC members think Fed Funds will be by December 2024. One-third of the members think it will be at the current 5.125% or higher. The median estimate is 4.60%. Only one member thinks Fed Funds will be below 4% by the year-end 2024.

Mind you, the Fed does not have a good forecasting track record. They started 2022 expecting Fed Funds to end that year slightly below 1%. Furthermore, they anticipated the rate to continue higher through 2024 to a terminal rate of about 2.50%. As we know, Fed Funds ended 2022 over 3% higher than they originally forecasted. The 2024 rate forecast may be correct, but whereas the Fed expected rates to rise to that level, it only proves accurate if they fall appreciably to 2.50%.

Fed Funds Futures Outlook

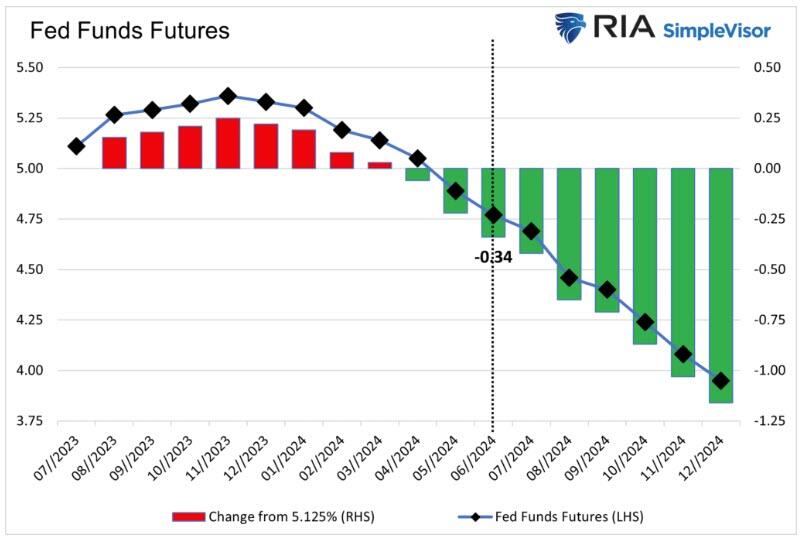

Many traders take their lead from the Fed. Consequently, if the Fed is grossly offside in their expectations, the market usually is as well. Currently, the market believes the Fed forecasts that rates will stay “higher for longer.”

Fed Funds futures imply Fed Funds will stay at current levels or creep a little higher through March 2024. At that point, the market starts to price in rate reductions. By June 2024, they imply that Fed Funds will be around 4.75%, or about .34bps lower than it is today.

Fed Funds Traders and the Fed are Poor Forecasters at Turning Points

Fed and market Fed Fund forecasts are often wrong at critical turning points. If higher rates and the inverted yield curve do not cause a recession in the next six months, the Fed and professional Fed Funds futures traders’ expectations may prove correct. That presumes that interest rates have little effect on a heavily indebted economy. We find that extremely hard to believe.

Suppose, instead, the relatively predictable lag effect of prior rate hikes catches up with the economy, as we suspect. In that case, the Fed and the market will again prove they were wrong at a critical turning point in monetary policy.

So, what if they are both wrong, and the economy starts slipping as the year progresses? The Fed will likely cut rates aggressively if inflation continues lower and gathers downward speed with weakening economic activity.

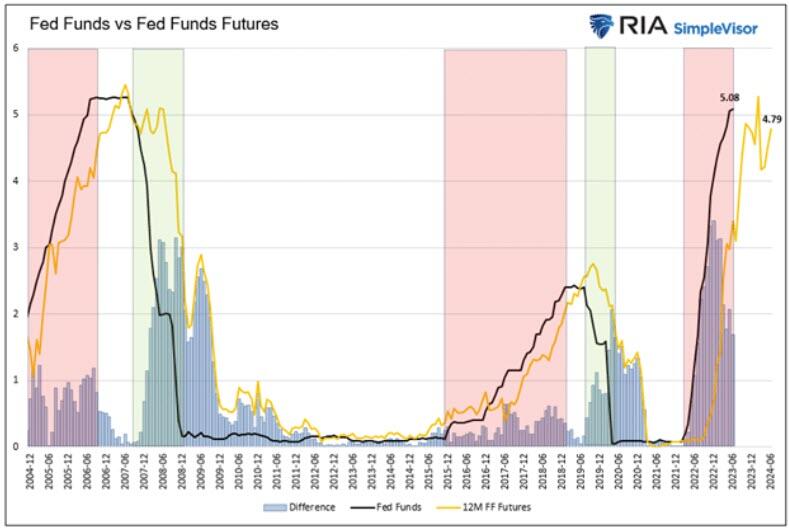

The graph below shows one-year Fed Fund expectations versus what Fed Funds did over the last twenty years.

During the last two rate cut cycles of 2008 and 2019-2020, Fed Funds futures traders again underestimated the Fed. In 2008, they missed by over 3% and by about 2% in 2020. Based on where Fed Funds are today and the significant impact interest rates have on economic activity, do not be surprised if Fed Funds are in the 2-3% range or even lower come next summer.

Summary

A forecast of 2% or 3% Fed Funds by next June may sound outlandish. But history has proven the Fed Funds forecasts of professional traders and the leading experts at the Fed are most often faulty. Expect the unexpected!

Fed Funds have a history of slowly climbing and then dropping precipitously. Some say they take the stairs up and the elevator down. Given the economic dependency on interest rates, we have no reason to suspect that the next time the Fed cuts rates will be any less aggressive than prior instances.

Tyler Durden

Wed, 07/05/2023 – 11:15

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com