Land Of The Rising Prices

By Maartje Wijffelaars, Senior economist at Rabobank

Over the past few days, Russia has made it all the more clear that its only concern is winning the war, whatever the collateral damage. Not only has the country withdrawn itself from the Black Sea Grain Initiative deal, but has also bombed port infrastructure, grain silos and processing equipment. Subsequently it warned that any ships sailing to Ukraine’s Black Sea ports would be seen as “potentially carrying military cargoes”, further escalating the situation. In response, Ukraine on Thursday said it will do the same with ships sailing to Russian ports or ports in territories occupied by Russia.

If anything, de-escalation of tensions seems very difficult at this point, let alone the renewal of the Grain deal – even though Russia risks alienating ‘friendly’ countries in the middle east, Africa and Asia who suffer from a smaller supply of wheat and higher prices. Uncertainty, higher transportation costs to get grains out of the country, and the burning of crops, have send for example wheat futures for September some 10% higher over the past few days – though they have started to come down from their peak somewhat. The higher prices have already led Egypt, which is usually wary of expressing hard words against Russia due to its economic dependence, to condemn Russia’s withdrawal from the deal and the bombing. It has already been forced to ask for financial support from the United Arab Emirates to help buy grains at the higher costs.

Importantly, even if tensions de-escalate and the Grain deal were to be renewed at some point, the destruction of infrastructure would mean the deal would be less effective as before, according to our agri commodity analysts.

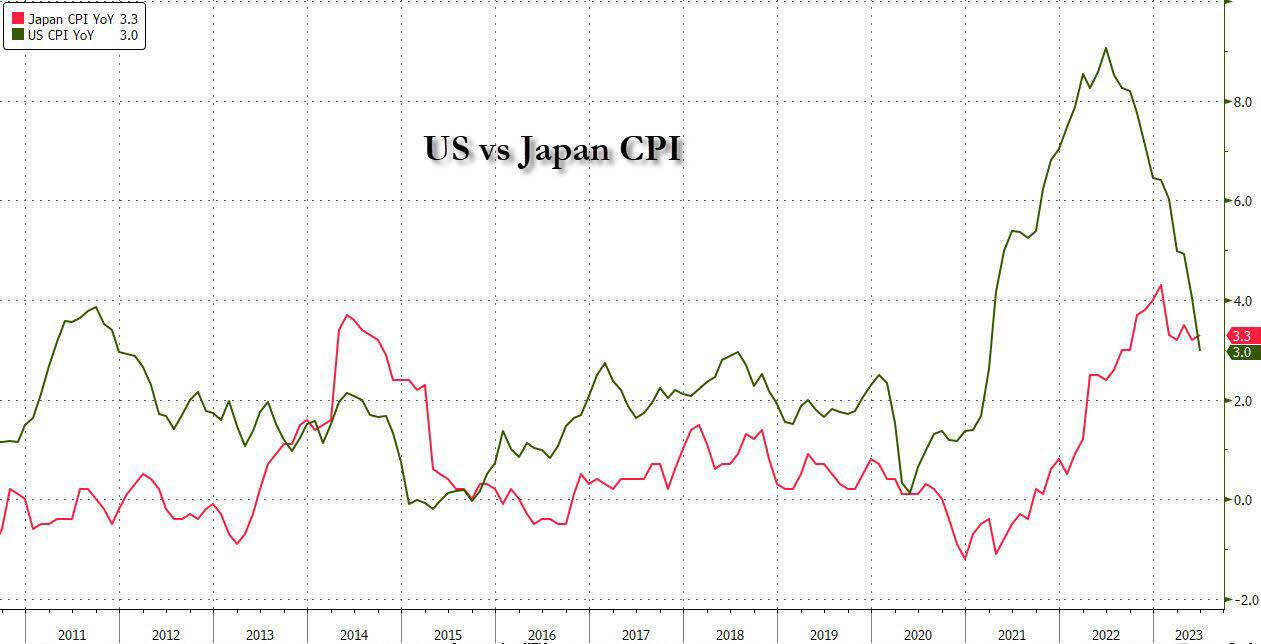

An ongoing increase in food prices next to a hike in utility bills were also among the main drivers of Japan’s headline inflation, which came in at 3.3% in June. The figure matches expectations and follows a 3.2% rate in May. Fun fact is that Japanese inflation is now higher than that in the US for the first time since October 2015.

More important, however, is that the indicator more closely watched by the Bank of Japan, i.e. CPI excluding fresh food and energy, dropped slightly from 4.3% to 4.2%. The decline was small and the first in over a year, but it could well fit the narrative the BoJ has been trying to bring across. The BoJ argues that recent inflation has been cost push and that it will come down again in line with fallen commodity prices, absent any significant and sustainable increase in wages that is.

Even though wages have increased this year and some more wage pressure is in the cards, it remains to be seen if this trend can be sustained into next year. In any case, given its long history of very low inflation, policy makers will likely be wary of tightening monetary policy too soon, which is underscored by recent comments by the governor. Earlier this week Kazuo Ueda, said “There is still a distance to sustainably and stably achieving our 2 per cent inflation target”. While the BoJ could present an upwardly revised inflation outlook after its policy meeting next week, such statements signal that a policy tweak is likely to be delayed. Based on this expectation, our FX strategist Jane Foley last week softened some of our JPY forecasts.

The ultra-loose policy in Japan marks a stark contrast with the policy tightening in the rest of the world. While Turkish policy rates of 17.5%, where the central bank yesterday hiked the rate with 250bps, are unthinkable in western economies, policy rates are nevertheless highest in over a decade and hiking cycles have not fully run their course yet. Our US analyst Philip Marey, for example, expects the Fed to hike its policy rate once more at its meeting next week, raising its target range by 25bps to 5.25%-5.5%.

Meanwhile, the ECB has pretty much confirmed another 25 basis point hike next week. We still subscribe to the view that this takes the ECB’s rates to the peak of this cycle, but September remains a very close call. Any setback in terms of inflation data or doubts about policy transmission could force the ECB to continue hiking after summer. On that note, yesterday’s second revision of the eurozone’s Q1 GDP figure showing that the Eurozone managed to escape a recession after all is a case in point. It shows weakness, as growth stalled, but also relative strength, as it did not contract. The ECB’s internal indecisiveness, while fully justifiable given the current backdrop, creates additional challenges when it comes to the communication strategy. All the more so because there is some time inconsistency in the ECB’s communication needs. Whereas the Council wants to keep their options open in the near-term, they will probably also want to send a much stronger message for the medium-term in order to lower expectations of rate cuts in early 2024. It may be difficult to reconcile these two objectives.

Finally, our UK analyst Stefan Koopman still projects two more 25bps hikes by the BoE, one in early August and another mid-September. This would raise the policy rate to 5.5%. This morning’s retail and confidence data have not altered that view. Retail sales in the UK rose by 0.7% m/m in June, well above the expectation of 0.2% growth. The country’s warmest June ever recorded spurred retail sales growth, as consumers flocked to department stores and supermarkets to purchase items ranging from home furnishings to groceries. There remains, however, a continued divergence between volumes and values due to inflation. Compared to February 2020 levels, total retail sales were 17.9% higher in value terms, but volumes were still 0.2% lower. Meanwhile, consumer confidence declined significantly in July, falling by 6 points to -30 according to GfK. It was the sharpest monthly drop in confidence in over a year and brought the index down to its lowest level since April. The decline interrupts a rebound in sentiment over the previous six months, reflecting concerns about rising prices and mortgage rates impacting household finances

Tyler Durden

Fri, 07/21/2023 – 14:05

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com