“81% Of All Tradeable Assets” To Produce Negative Returns Over Decade, Warns Macro Fund

Tyler Durden

Wed, 08/05/2020 – 15:15

Authored by Teddy Vallee, Founder & CIO of Pervalle Global,

It has been a tough decade for macro, with annualized returns of 1% failing to outpace the S&P 500 in nine of the last ten years. While there have been clear opportunities, increasing levels of Central Bank intervention and lower growth profiles have taken the life, yield, and volatility out of many macro assets.

The global bond market is a prime example, as roughly 50% of sovereigns now have policy rates at or below zero versus none 10 years ago. As these rates have trended lower, so to has the volatility of both economic data and financial assets, thereby creating a positive feedback loop between lower growth, lower rates, lower vol, and higher risk. Adding to the feedback loop has been the lack of global yield, which has forced investors further out on the risk curve in search of returns.

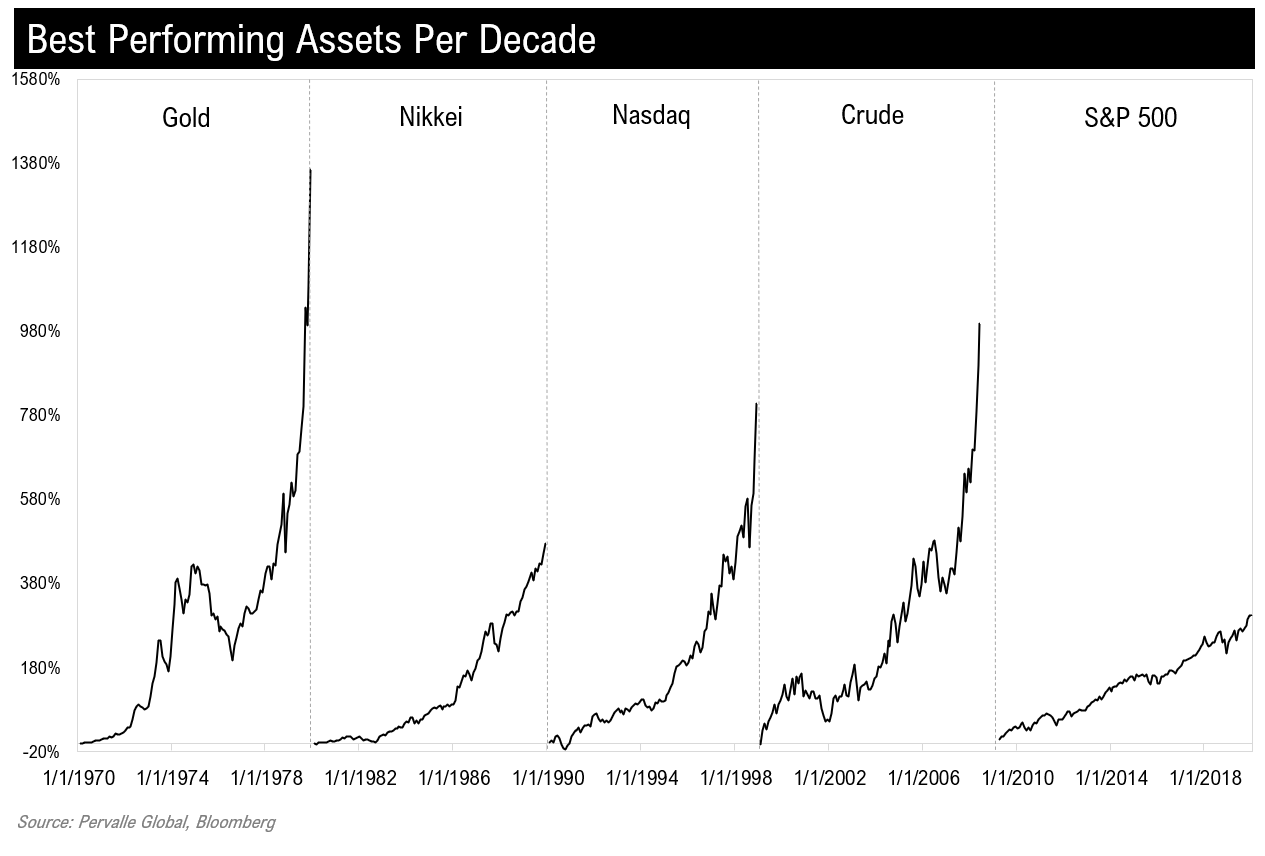

The biggest beneficiary of this interplay has been the US equity market, which is evident in return profiles, as over the past 10 years US equities have compounded at 14.2% per year (as of the recent high). However, after analyzing the best-performing assets of the decade’s past, we find forward returns over the next decade are quite poor, compounding at negative 4.8% per year, with 95% of the annual returns following the decade high also negative.

We see this scenario playing out in the US over the next 10 years, as lower growth and lower rates fail to lead to lower volatility and thus higher risk assets. This is primarily due to the recent multiple sigma move in growth, which destroys the foundation for the feedback loop of the past 10 years, as it forces the excess out of the system. Additionally, we can envision an environment where the confines of the lower bound force Central Banks to get creative, which as a result would lead to higher rates and higher vol, creating a difficult environment for equities.

While it’s been a good decade for US stocks, we can not say the same for the next.

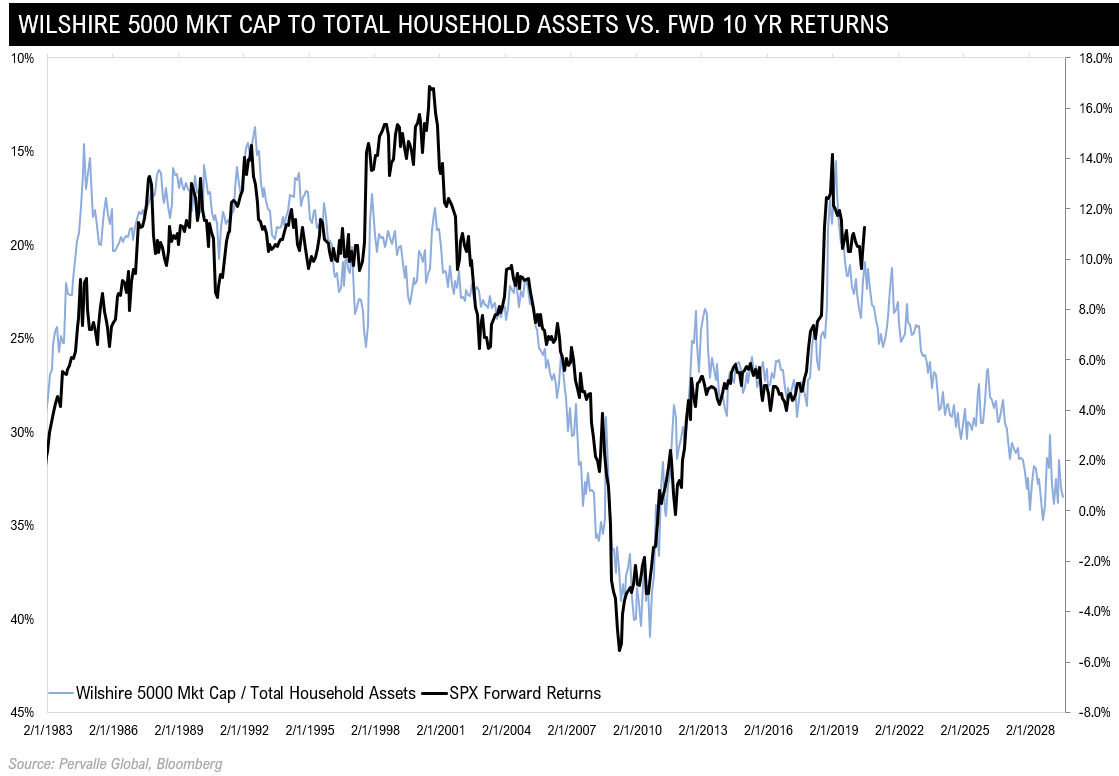

We find additional evidence of this view based on a combination of our forward return models. For example, over the past 10 years the market cap of the Wilshire 5000 has grown from $7T to $31T, which equates to roughly 40% of total US household assets. With such a large portion of household wealth tied up in the equity market, the incremental dollars to power the market higher dry up, resulting in a period of very poor returns, as shown below.

We come to the same conclusion on a valuation basis, as the price of the S&P 500 relative to the S&P’s 10-year earnings stream indicates forward returns will also be negative.

And in terms of the size of the stock market relative to the economy, that too indicates forward returns will be quite unappealing.

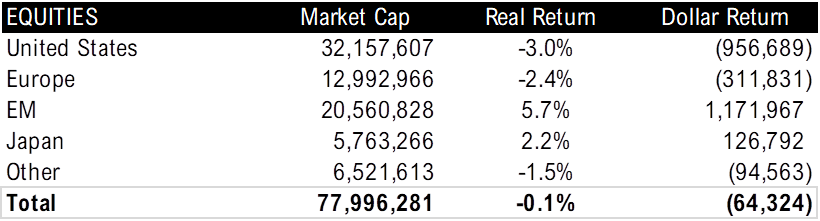

However, it is not solely the US which will have poor returns over the next 10 years, as the aggregate global equity market is likely to produce a negative real rate of return based on our forward return models.

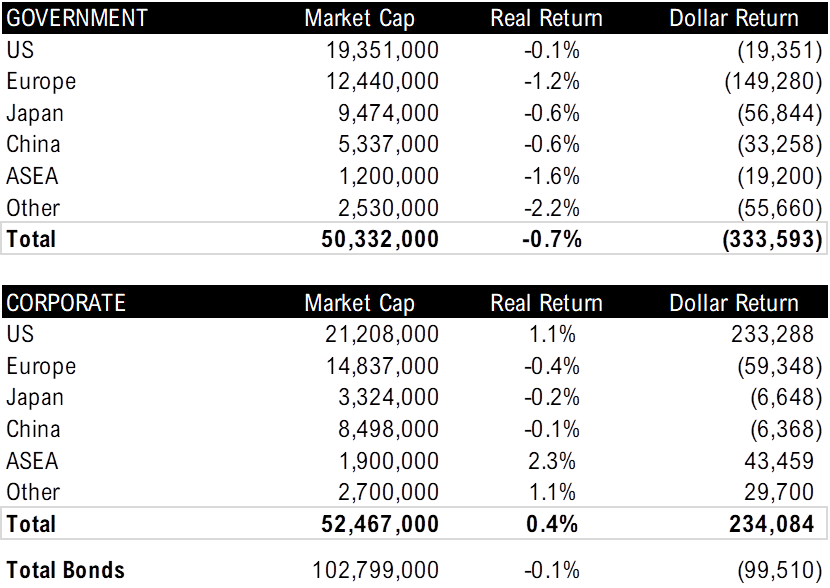

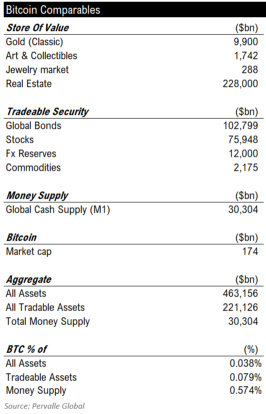

Given this backdrop, investors will be forced to turn to the bond market to provide a positive return on capital. Unfortunately, that too will produce a negative rate of return, as shown by our breakdown of the global corporate and sovereign bond market below. This would imply that over the next 10 years, 81% of all tradeable assets ($180T) produce a negative return for investors, leaving only the commodity and currency markets for some form of capital appreciation.

While we do see pockets of positive returns for industrial commodities, the cyclical nature of these assets reduces their upward drift, which over a longer period would not provide any positive real return to an investor’s portfolio. On the other hand, precious metals should have positive returns given their use as a store of value and hedge against currency debasement; however, there is a growing probability that we may experience a deflationary environment, which under the assumption it hit, would materially weigh on the whole commodities complex.

This leaves cash and currencies as the main source of return for investors over the following 10 years, which is a difficult proposition given US money supply is growing at a 42% annualized pace, and is likely heading much higher over the following years as Central Banks lose their ability to stimulate growth through lower interest rates.

By process of elimination, investors are only left with one asset that both provides a store of value and is a hedge against currency debasement.

Bitcoin.

As it stands today, bitcoin represents roughly 4 basis points of all assets, and roughly 7 basis points of total tradeable assets. While we are only looking at BTCUSD as a store of value versus its application, it is feasible to view this emerging asset as a large percentage of both the gold market and the total tradeable security market.

If we assume that over the next decade, bitcoin replaces 15% of the gold market, this would equate to a 24% return per year for the next 10 years. That said, based on the scenario we outlined above; it is quite probable that the $221T in tradeable assets will need to find a home. Assuming 3% of these assets flow to bitcoin, investors would expect a 44% rate of return per year over the next decade.

The cryptocurrency space will be imperative for investors to understand over the following years; however, the size of the market and the potential upside returns, unfortunately, do not outweigh the negative drag from the remaining tradable assets (assuming average stock/bond allocations), leaving passive participants in a difficult position.

Therefore, in order to produce positive returns over the next 10 years, investors will need to actively manage growth cycles. By understanding how assets trade during different cycles, and actively forecasting those cycles, investors can get in front of growth upcycles and take advantage of growth down cycles across nearly every asset class.

This the edge of a macro investor, particularly an active one, and the ability to jump across every asset class further increases that edge.

We see the next decade as the decade of Macro.

Macro is back.

* * *

Pervalle Global Research is the research arm of Pervalle Global, an NYC based global macro fund. This note appeared in Pervalle Global’s June institutional research piece. Email info@pervalleglobal for more info|

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com