“This Is A CDO”: Cerberus Selling $300MM In “Potentially Worthless” BBB- Rated CMBS IO-Strips As AAA Securities

Tyler Durden

Sun, 10/04/2020 – 18:40

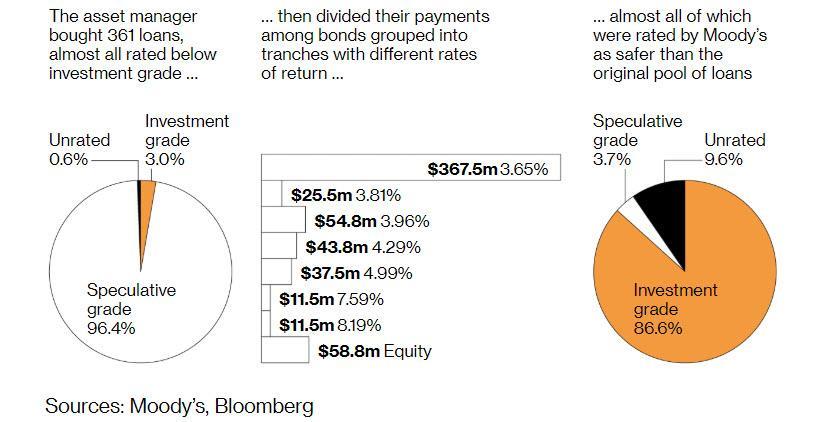

Back in May, when the Fed was struggling to rekindle animal spirits and force investors into every possible toxic debt instrument it could find, we explained how through the magic of modern monetary alchemy, a portfolio consisting of 96% Junk Loans had been converted into 87% investment grade bonds.

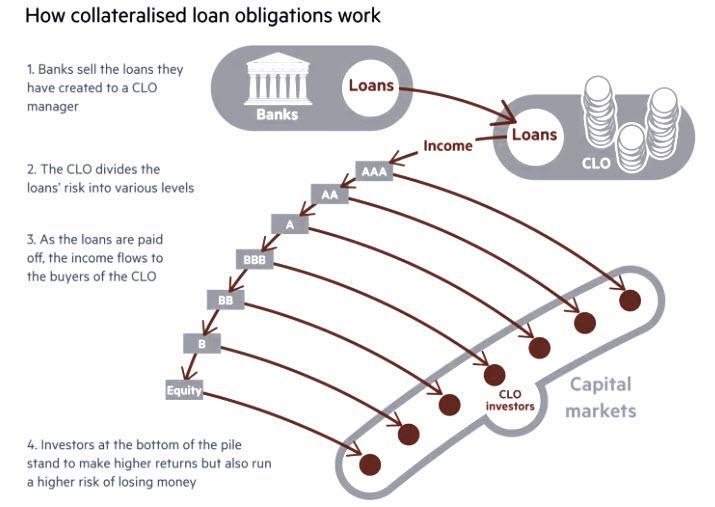

The magic catalyst in question: CLOs, which are structured credit products that take a portfolio of mostly junk loans – which are used to fund much of corporate America – and repackage them in such a way that the resulting product looks and feels much higher in credit quality, even though it consists of the exact same junky underlying securities, just presented in a different way.

Of course, this is hyperbole there is nothing “magical” about what CLOs do – in a nutshell, such structured products merely take advantage of the diversification nature of a broad pool of loans and make the assumption that absent a catastrophic economic crash, it is unlikely that more than a given percentage of loans will default at any one time. Now, we got perilously close to just such a mass default event after the covid shutdowns, which is also why the Fed had no choice but to step in and effectively bailout both corporate bonds and loans, or else it risked a complete collapse of the corporate bond and loan markets, and trillions of downstream losses in the CLO space.

In retrospect, and looking where risk assets trade now, the Fed has succeeded in kicking the can (whether it can continue doing that even as we head into the peak turbulence period of the US election and a potential second wave and new shutdowns, remains an open question).

One company which is not waiting to see what happens to the economy or to euphoria investor risk appetite, is the iconic distressed investor, Cerberus Capital, which has taken the CLO example above one step further, and instead of selling repackaging loans, has taken a bunch of freefalling, and potentially worthless, CMBS interest-only tranches and repackaged this steaming pile of dogshit into a $300 million product that the rocket scientists at DBRS rated, drumroll, AAA.

The product? A CDO, or Collateralized Debt Obligation, very much of the type that led to the collapse of the financial system in 2007/2008 when a handful of banks repackaged subprime mortgages into CDOs (and CDO squareds), giving the impression of riskless securities, which were virtually all wiped out once the housing market crashed, and one-hit wonder investors such as John Paulson made billions.

As Bloomberg details this latest “Wall Street alchemy” enabled by the Fed’s idiotic bubble-blowing policies, “in a maneuver that recalls the complex home mortgage investments in the mid-2000s, Cerberus Capital Management has used relatively low-quality commercial mortgage bonds to create triple-A debt.” In doing so, it is taking advantage of the greed and stupidity of the prevailing investor, because as we have repeatedly noted, the commercial real estate market has been clobbered especially hard by the pandemic, and a CMBX series focusing on hotels has emerged as the “Big Short 3.0” trade.

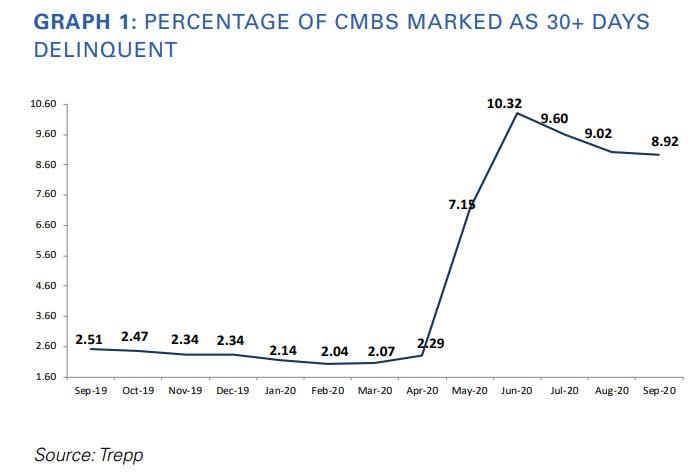

Just how bad is the CRE market? Consider that according to Trepp, around 9% of all commercial mortgages that have been bundled into bonds were delinquent in August, as Covid-19 keeps shoppers out of malls, travelers away from hotels and workers home from offices. The real number is far higher, and only the fact that $20 billion in CMBS forbearances have been granted is preventing this chart from exploding.

This is why hedge funds that find themselves holding to these securities are looking for creative ways to offload them to the army of idiot investors spawned by Jerome Powell’s monetary idiocy, while also making money from flipping them. Sure enough, Cerberus will likely strike gold in both regards: the securities sold by the hedge fund mature in 2.2 years, and the AAA portion is being marketed at a price of between 1.4 and 1.5 percentage points over benchmarks, according to Bloomberg sources. The high ratings combined with relatively high yields and short-term maturity could attract some investors.

Specifically, Cerberus – where Dan Quayle is Chairman of Global investments and may explain how Cerberus ended up with this pile of steaming horseshit in the first place – is taking derivatives of commercial mortgage bonds, known as interest-only strips, and packaging them into around $390 million of notes, about $300 million of which have top ratings from DBRS Morningstar.

As Bloomberg explains the structured product “alchemy” we first deconstructed back in May, “most of the commercial mortgage securities at the foundation of this transaction have the lowest investment-grade rating, BBB-, but through the magic of securitization they’re transmuted into AAA instruments, similar to subprime mortgage bond derivatives that were bundled into top-rated collateralized debt obligations during the U.S. housing bubble.”

Attempting to explain why investors have once again learned absolutely nothing from the financial crisis, Jason Callan, head of structured assets at Columbia Threadneedle Investments said “I’m sure the ratings are what’s driving the demand.” He is right, although it’s worth remembering that rating agencies rated hundreds of similar CDOs AAA in the summer of 2007, only to see them completely wiped out less than a year later.

“This is a CDO,” said Jen Ripper, an investment specialist at Penn Mutual Asset Management. “There could be a real risk of some principal loss at the BBB- level, which most of these interest-only tranches are ‘stripped’ off of.”

As Bloomberg adds, the transaction is being referred to as a “resecuritization”, according to deal docs, which say it’s structured so that cash flows have some protection from early repayment of principal through refinancing, and losses due to defaults. By some protection it likely means 1-2 months of capital buffer after which buyers are on their own. And in a world where a $700 million mall-backed CMBS portfolio is about to become the first mega casualty of the covid crisis, they will be on their own very soon.

Not convinced yet? Well, the deal is backed by about 9,300 mortgages, 27.6% of which are office, 25% retail and 15.5% hotel – the three hardest hit sectors in the post-covid age – while the rest is a mix of other commercial real estate sectors, initial marketing materials show.

Worse, CMBS “interest-only strips” are linked to the performance of corresponding bonds with the same ratings that pay both principal and interest. They represent securities backed by the excess interest generated from a pool of commercial mortgages. In other words, these securities default first, before any other impairments hit the capital structure. It also means that anyone who investors in such a “resecuritization” will lose money, guaranteed… unless of course the Fed buys it all.

Completing the farce, the Cerberus deal is being arranged by Deutsche Bank, JPMorgan Chase and Wells Fargo, the three banks that have the worst criminal record in the world and which collectively have paid tens of billions of legal fees, penalties and settlements. And soon, once this deal also blows up, we can add a few more billion in legal penalties.

But don’t worry, nobody will go to prison, because if anyone is guilty of anything, it is the Fed for allowing this kind of financial crisis stupidity to make a triumphal return.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com