The Tech Reckoning, Global Synchronized Debasement, & Late-Cycle Signs

Tyler Durden

Fri, 10/30/2020 – 10:15

Authored by Kevin Smith and Tavi Costa via Crescat Capital,

History does not exactly repeat, but it often rhymes. The art and science of macro investing is comparing past business cycles with the present across a mosaic of different indicators and time frames to determine the most probable path forward for markets. Throughout time, financial markets and the economy have been intimately linked to cycles of expansion and contraction of money and credit. The Federal Reserve was created by bankers and enacted by Congress in 1913 to provide a more flexible and stable monetary and financial system, but by no means did the Fed repeal the business cycle. In fact, the central bank has often played a role in amplifying booms and busts. For example, after introducing large-scale purchases of government securities to stem the recession of 1923, the Fed continued to expand the money supply and suppress interest rates through the remainder of the 1920s. Such monetary policy fanned the flames of historic stock market speculation which culminated in the stock market crash of 1929 to 1932 and the Great Depression. The macro set-up today is eerily similar as we will explain below.

The Fed operates under the premise that it is making the financial system safer by attempting to stabilize the credit cycle, but since the Global Financial Crisis, monetary policy has served less like a temporary, elastic tool to smooth the business cycle and more like an addictive drug that requires a bigger and bigger dose to have the same effect while at the same time making its subject more imbalanced and prone to crash.

At Crescat, our composite of eight fundamental stock market valuations measures shows that we have the most euphorically over-valued US stock market in history, higher than 1929 and higher than 2000. As prudent investors and fiduciaries, we are forced to devise strategies to protect against the combined risks of the most overvalued US stock market and the largest global debt-to-GDP imbalance ever. The historic blueprint for the unwinding of such twin manias is the reason why we are such big proponents of the “buy gold and sell stocks” theme at Crescat today.

There are three useful case studies to understand why investors need to seriously consider a hedged strategy of shorting the most over-valued US equities and buying undervalued gold and silver mining companies in an attempt to capitalize on (rather than be run over by) the likely unwinding of today’s stock market and credit imbalances. Only one side needs to play out for this spread trade to work, but what is so interesting now is that history shows that both sides can win substantially under the macro setup like we have today:

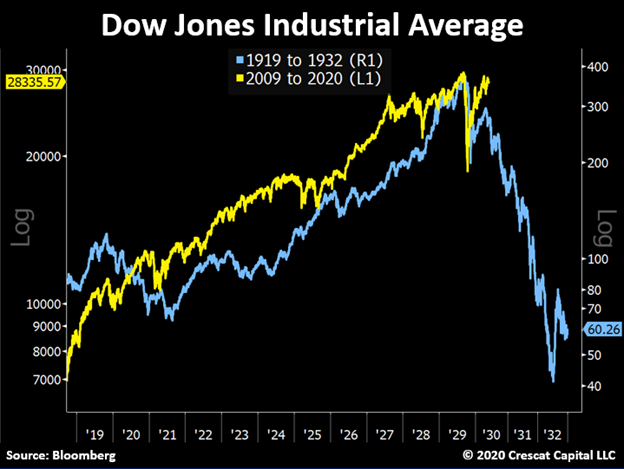

1. The Deflationary Great Depression

The chart below illustrates how stocks were decimated in the credit deflationary bust of the Great Depression, but at essentially the same time, gold mining companies acted in counter cyclical fashion to create wealth during the downturn. Homestake Mining, the biggest gold producer of the time, increased seven-fold from 1930 to 1936 a period during which the US dollar was devalued from .048 ounces of gold to .026.

Currency devaluation relative to gold was necessary then just as it is likely to be today to counter the deflationary impact of record debt-to-GDP imbalances combined with a stock market and economic collapse.

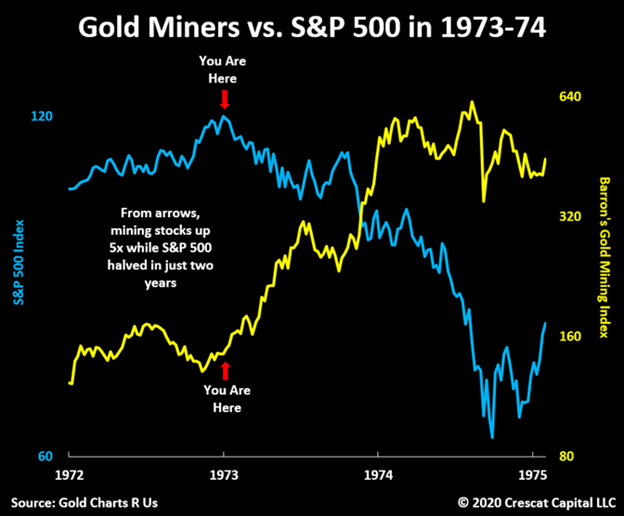

2. The 1973-74 Stagflationary Recession

Late 1972 was another macro set-up comparable to today in our analysis. Then, institutional investors were crowding into a narrow group of large cap growth stocks dubbed the Nifty Fifty driving them to extraordinarily high price-to-earnings valuations. By 1972, S&P 500 Index’s P/E was a then lofty 19, but the Nifty Fifty’s average P/E was more than twice that at 42. Among the richest valuations were Polaroid with a P/E of 91; McDonald’s, 86; Walt Disney, 82; and Avon Products, 65. The parallel to these stocks today are large cap growth oriented FAANG and software-as-a-service technology stocks. These stocks are owned by cabals of hedge fund whales and Robinhood traders alike. In the stock market collapse of 1973-74, the S&P 500 Index was cut in half in just two years.

From their respective highs, Xerox fell 71 percent, Avon 86 percent and Polaroid 91 percent. But over the same time, the Barron’s Gold Mining Index increased 5-fold! Meanwhile, just like in the Great Depression, the US dollar was being devalued relative to gold. This time, it was the end of the Bretton Woods monetary system and the US dollar gold standard. Surprise inflation was also arriving on the scene with the first of the 1970’s oil crises.

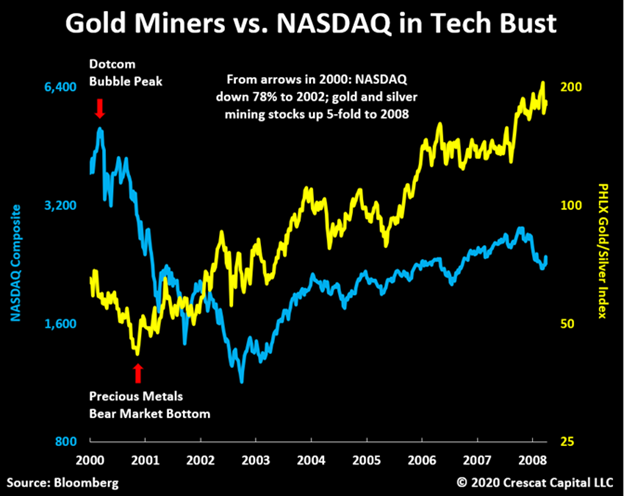

3. The Tech Bust

The tech bust is the third comparable set-up to today, precipitated by another time of record stock over-valuation and low precious metals prices relative to money supply. From 2000 to 2002, the tech heavy Nasdaq composite declined 78%. 2000 also marked the bottom of a gold stock bear market.

The Philadelphia Stock Exchange Gold and Silver Index would go on to increase five-fold from 2000 to 2008. Tech stock over-valuation is even more egregious today than it was in the dotcom bubble. Meanwhile, in our view, gold and silver stocks, particularly smaller cap exploration focused names that we favor at Crescat today, have only just started to rise off the depths of a ten-year bear market.

The Largest Supply/Demand Mismatch

We are now at the onset of a major global synchronized debasement. Today’s historically depressed macro environment has hamstrung central banks to pursue a suicide mission set to severely devalue fiat currencies in coordinated fashion. It’s inevitable and unavoidable. The combination of long-term debt imbalances and unprecedented levels of fiscal and monetary imprudence have likely reached an inflection point in the world economy to such a degree that we have the IMF conspicuously telegraphing the idea of a “New Bretton Woods Moment”.

As investors feel the urge to seek capital protection, this is soon to be one of the largest supply/demand mismatches we have ever seen in the gold market. For decades, the rise of popularity in risk parity strategies has abolished the use of monetary assets as part of conventional portfolio construction. The current macro set up, however, will likely reverse this trend. The fixed income and equity markets are both trading at record valuations and risk is now mispriced. With a long history of serving as a resilient hedge against monetary debasement, precious metals will likely become a key alternative for asset allocators.

The supply side of the market is arguably even more extreme. There were zero gold discoveries above 2 million ounces in the last 3 years. That’s right, zero. For the first time in history, precious metals companies are reluctant to spend capital even though gold prices have recently reached all-time highs. It’s the result of drastic capital conservatism imposed after a decade long bear market in the mining industry. This declining trend in exploration investments and the rising geological challenges to find and extract gold will likely ensure an incredibly constrained supply for the metal in the following years.

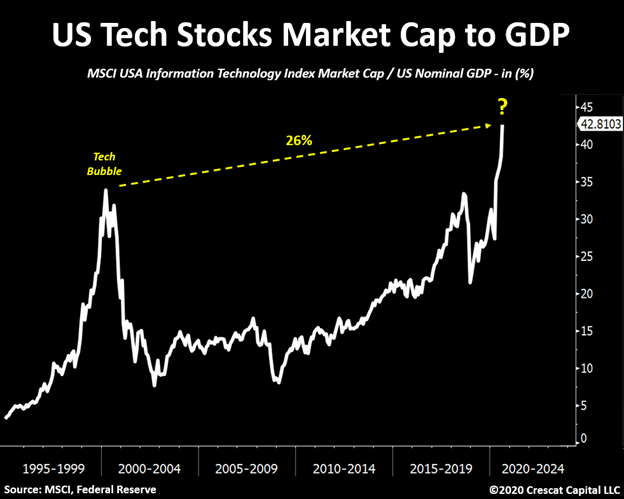

The Tech Reckoning

The debt overhang problem on such a severely impaired global economy inhibits the efficiency of stimulative polices to restore growth and to justify the historic valuations we currently see in equity markets. In our view, today’s mass of indolent market participants with unrealistic investment expectations is on the verge of facing the cold hard truth of a natural downturn in the business cycle.

Artificially low interest rates and the idea that the Fed has “got your back” has forced investors to move up the risk curve creating a crowded stock market environment. In particular, the tech sector is priced for perfection. The aggregate market cap of info tech companies now represents a record 43% of US GDP. This ratio is now over 26% higher than the internet bubble peak levels we reached in March 2000! We urge investors to be mindful of such important historical precedent. Equity markets are running on fumes. Sadly, most people refuse to learn from history.

The New Growth Stocks

Policy makers have no choice but to continue diluting the value of fiat currencies to enable a levered financial system to withstand such extreme macro imbalances. If past is prologue, large central bank interventionism leads to the appreciation of monetary assets and, in our view, precious metals will be the real beneficiaries of a global synchronized debasement trend that now seems irreversible. Therewith, gold and silver mining companies should be the largest beneficiaries of this environment. They look fundamentally stronger than any other industry in equity markets today.

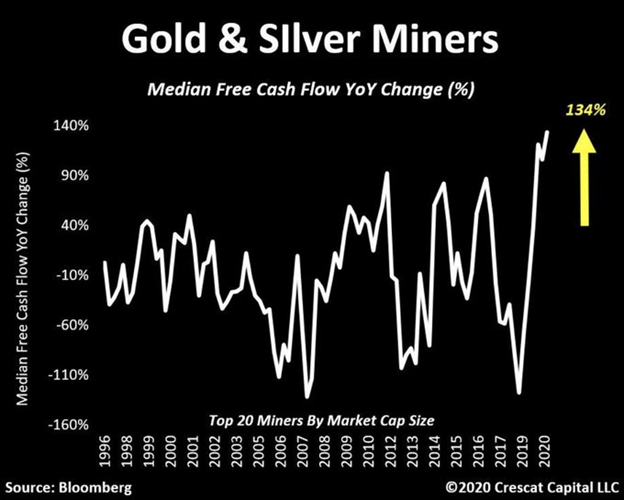

In fact, free cash flow among the top 20 miners have grown by 132% year over year in their latest report. Despite all its reputation of being capital destroyers, this industry is finally proving the contrary and becoming financially prudent. In aggregate, gold and silver miners did the second least amount of equity dilution in history while also paying down debt last quarter. As we pointed out in prior letters, if the precious metals industry were a sector, it would have the cleanest balance sheet of them all. Against all the odds of such a challenging business model, we believe gold and silver stocks are poised to become the new growth stocks of the next years.

Pedal to the Metal

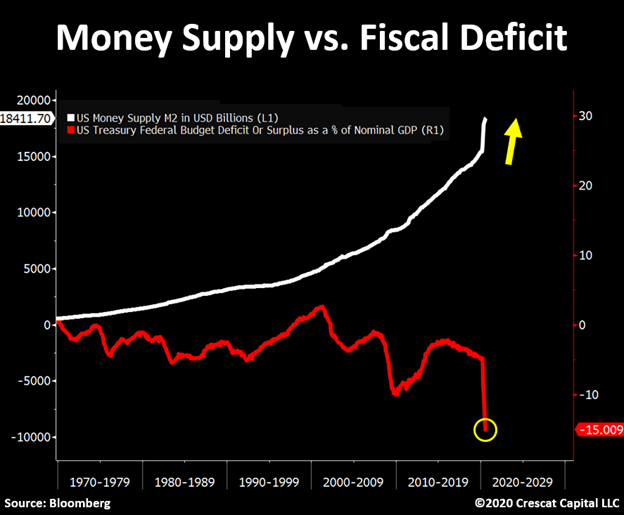

Even though almost every economic indicator has somewhat bounced since the pandemic lows, fiscal deficits remain with the pedal floored to World War II levels.

The speed of which the US government debt is now rising is unmatched to any other period since the break of the gold standard. Monetary and fiscal disorder have perhaps gone too far this time around and significant monetary debasement is, in our view, inevitable.

Global Synchronized Debasement

More is more. Jerome Powell, president and chairman of the Federal Reserve, recently made some truly remarkable statements when expressing his views about the potential size of further fiscal and monetary stimulus to fight the current recessionary forces:

“The expansion is still far from complete. At this early stage, I would argue that the risks of policy intervention are still asymmetric. Too little support would lead to a weak recovery, creating unnecessary hardship. Even if policy actions ultimately prove to be greater than needed, they will not go to waste”

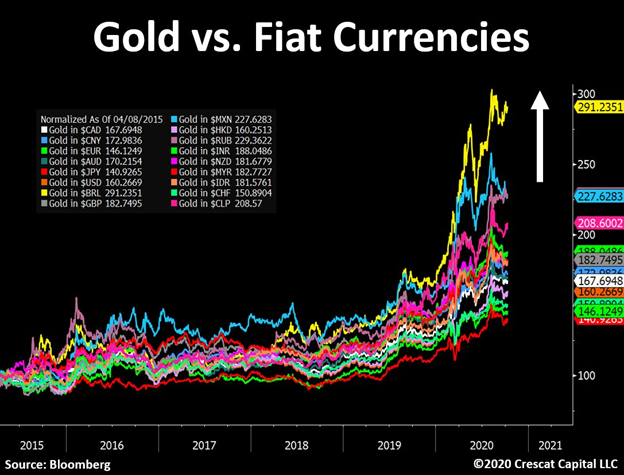

Central banks are indeed hamstrung. The severity of the underlying problems in the global economy while asset prices remain completely detached from depressed fundamentals ensures the need for further monetary and fiscal response to prevent the stop of this rolling snowball. We are likely to see a continuation of extreme accommodative policies globally. As a result, it is no surprise that gold is already rising versus all fiat currencies in the monetary system. We think this is a trend that is poised to continue if not accelerate. We call this global synchronized debasement.

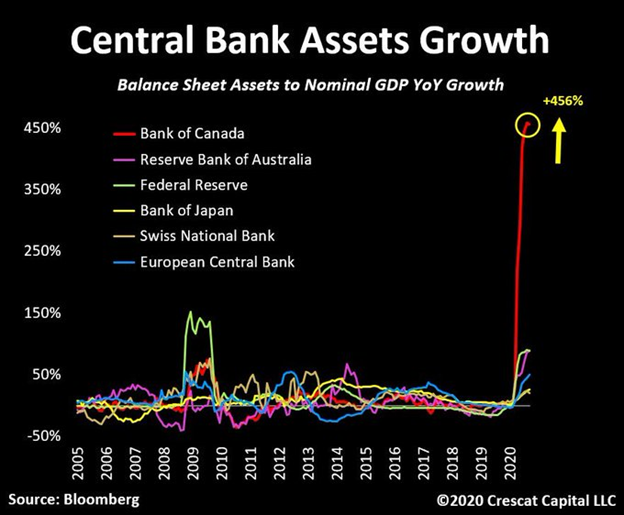

The Federal Reserve added about $3 trillion of assets to its balance sheet since late February when the pandemic began to noticeably hit the US while stocks started selling off. Other central banks didn’t perform quite the same amount but are now catching up fast. The Bank of Canada is a great example.

Even though it’s coming off a lower base, the BoC has just taken its balance sheet assets from 7% to close to 30% of nominal GDP in one year. Of note, the Canadian economy has suffered significantly from its oil exposure and its historically leveraged housing market that requires an incredible amount of monetary support.

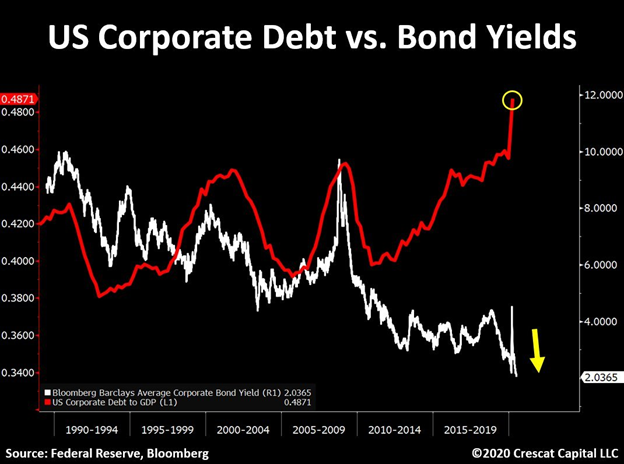

A Debt Trap

There have been critical unintended consequences of this prolonged period of cheap money. The US corporate bond market, for instance, has become one the most central bank dependent parts of financial markets today.

Even though the Federal Reserve has purchased a less significant amount of these assets, its extreme accommodative policies allowed corporations to access the debt market at record low interest rates despite having the most leveraged balance sheets in history. How do we ever get out of this debt trap? The Fed has created its own monster and has no option other than to keep printing money to counter a deflationary debt implosion.

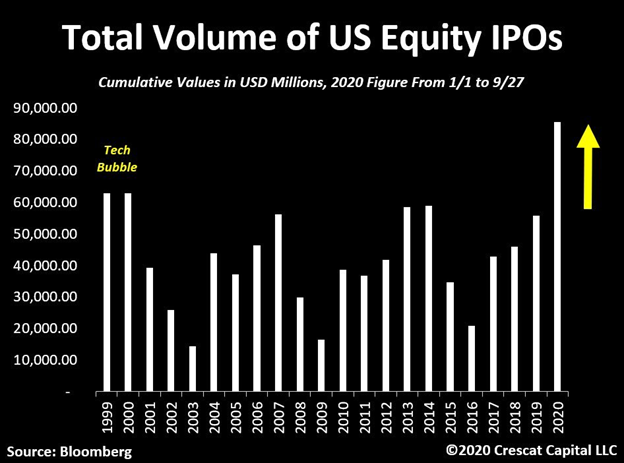

Late Cycle Signs

The lack of investor skepticism after long-years of great excesses in equity markets only validates how late we are in the investment cycle. Demand for stocks has been insatiable and undiscerning. 2020 has already set the record for the largest dollar volume of IPOs. With still two months to go, we are already 36% higher than the full year 2000, the year the tech bubble peaked. Bear in mind that only 9% of all 2020’s IPOs were actually profitable, not unlike the tech bubble.

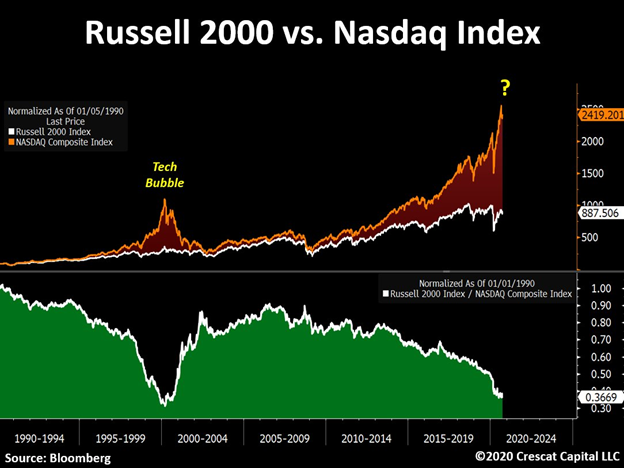

Small caps are a big testament for the real shape of the economy. While overall stocks remain near record levels, the Russell 2000 peaked over two years ago. They have been trending with lower highs since then.

Consequentially, the ratio of Russell 2000 to Nasdaq just reached near all-time lows and is about to retest tech bubble levels.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com