German ZEW: A First Glimpse Of The Consequences Of The Second Nationwide Lockdown

Tyler Durden

Tue, 11/10/2020 – 07:28

Submitted by Christopher Dembik, Head of Macro Analysis at SaxoBank

Summary: The German November ZEW Survey is at the top of the economic calendar today, but it did not really drive market sentiment as investors are still focusing on Pfizer vaccine news and hopes of swifter economic recovery in 2021.

Today’s German November ZEW report is one of the most important data set released this week. It gives us a first glimpse of the consequences of the second nationwide lockdown on economic expectations. Aligned with consensus, all the main components of the survey for November are declining, reflecting the impact of the new partial lockdown or light lockdown decided by the German government to contain the second wave of the virus. The current situation assessment is deteriorating again, sliding 4.8 points to land at minus 64.3 versus expected at minus 65.

Without much surprise, many panelist mentioned as a key concern the economic uncertainty related to the virus and the poor financial situation of the banking sector and insurers due to the low growth and low interest rates environment and risks of rising non-performing loans in coming months. This is not really new, but it will certainly continue to weight on the panelists’ mood in the coming months as long as there is no better economic visibility.

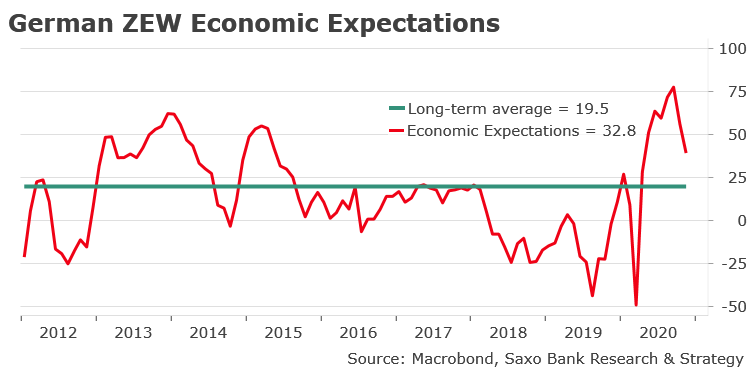

Looking into details, there are clear indications in the report that the German economy is once again edging closer to recession territory. Economic expectations, which are the most watched components of the report, are edging down again. In November, the subindex recorded a massive drop of 19.5 points to 32.8, but it is still standing way above its long-term average of 19.5.

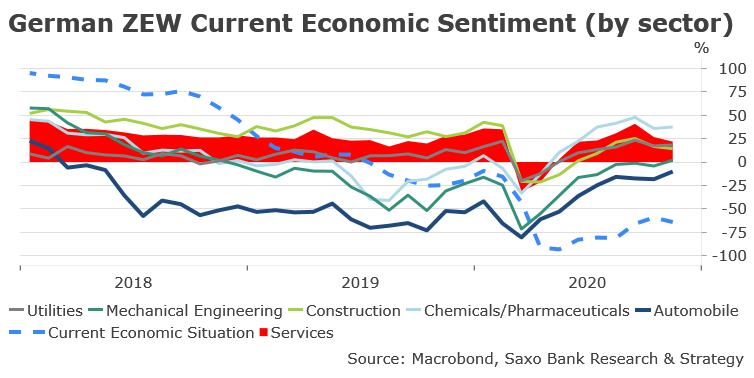

Unlike what has happened during the previous lockdown that occurred last Spring, we don’t see a general decline in economic sentiment across all the sectors. Firms most exposed to the new restrictions (mostly in the services sector and in the construction sector) are experiencing a new deterioration in economic sentiment. The subindex for the services sector is down at 21.8 vs prior at 26.7 and the subindex for the construction sector is also falling, at 14.3 vs prior at 16.6. In contrast, all the other sectors are going through stabilization (such as the utilities sector) or are heading north (automobile, mechanical engineering and chemicals/pharmaceuticals). This gap in economic sentiment is not only indicating that some firms are less hit by restrictions than in the first lockdown but also that higher foreign demand, especially from Asia/China, is fueling increased optimism in the German manufacturing sector. It thus confirms that economic contraction in Q4 will be less important than in Q2 as business continues more or less as normal in the manufacturing sector.

There is light at the end of the tunnel. The survey has been conducted before Pfizer and BioNTech announced vaccine candidate against COVID-19 achieved success in first interim analysis from Phase 3 study yesterday. It was undoubtedly positive and unexpected news, though it is still too early at that stage to know the exact implications of these announcements. There are still a lot of pending questions such as whether the vaccine will prevent transmission of COVID-19 or how many doses will be necessary etc. That being said, the increased likelihood of an imminent vaccine might have positive trigger effects on consumers and some firms. Most of the economic damage related to the pandemic mostly results from the fear of the virus, not the virus itself. Therefore, if there is credible hope of economic normalization in 2021, perhaps in the first semester, we can expect to see in coming months an improvement in sentiment survey, including in the ZEW survey. Most firms that are currently going through turmoil, typically hairdressers, will get a decisive boost from the vaccine and will be able to see demand going back to normal almost immediately afterwards. That’s why we should not overstate the impact of today’s ZEW report and, in that sense, the market was certainly right not to pay too much attention to it.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com