Dave Collum’s 2020 Year In Review, Part 1: “Willfully Ignorant”

Authored by David B. Collum, Betty R. Miller Professor of Chemistry and Chemical Biology – Cornell University (Email: [email protected], Twitter: @DavidBCollum),

“David Collum is willfully ignorant.”

~ Mountain Man (@Pjas77)

Every year, David Collum writes a detailed “Year in Review” synopsis full of keen perspective and plenty of wit. This year’s is no exception.

Introduction

Imagine, if you will, a man wakes up from a year-long induced coma—a long hauler of a higher order—to a world gone mad. During his slumber, the President of the United States was impeached for colluding with the Russians using a dossier prepared by his political opponents, themselves colluding with the FBI, intelligence agencies, and the Russians. A pandemic that may have emanated from a Chinese virology laboratory swept the globe killing millions and is still on the loose. A controlled demolition of the global economy forced hundreds of millions into unemployment in a matter of weeks. Metropolitan hotels plummeted to 10% occupancy. The 10% of the global economy corresponding to hospitality and tourism had been smashed on the shoals and was foundering. The Federal Reserve has been buying junk corporate bonds in total desperation. A social movement of monumental proportions swept the US and the world, triggering months of rioting and looting while mayors, frozen in the headlights, were unable to fathom an appropriate response. The rise of neo-Marxism on college campuses and beyond had become palpable. The most contentious election in US history pitted the undeniably polarizing and irascible Donald Trump against the DNC A-Team including a 76-year-old showing early signs of dementia paired with a sassy neo-Marxist grifter with an undetectable moral compass. Many have lost faith in the fairness of the election as challenges hit the courts. Peering through the virus-induced brain fog the man sees CNBC playing on the TV with the scrolling Chiron stating, “S&P up 12% year to date. Nasdaq soars 36%.” The man has entered The Twilight Zone.

A nutty Chem prof from Cornell

Has interesting stories to tell

The year 2020

Had crazy-a-plenty

T’was a year that was crafted in hell~ @TheLimerickKing

Figure 1. The one graphic that rules them all.

Figure 2. “Largely peaceful protest” meme at its inception.

Putting ideas on paper is the best way to organize them in one place, and getting everything in one place is essential to understanding ideas as more than the gut reactions they often hide as.

~ Morgan Housel (@morganhousel), columnist on why we write

Every year I ponder not writing a review. One of the voices in my head was pleading with me, “Don’t write it. There is nothing to be gained.” A much louder voice that chimes in seconds before every major decision that I make, however, was saying, “Fuck it. Let’s do it.” Someday I may drop the mic but not yet. I personally benefit because my life’s experiences and observations—those wild moments and funny-assed one-liners—don’t get shoved down (or up) the memory hole. I get boluses of serotonin. Mike “Mish” Shedlock referred to 2019’s version as “Satirical, Comedic, Insulting…” as part of a thorough Collumoscopy.ref 1 To the guy who keeps emailing me urging me to clean it up so his daughters can read it, save your breath. They are either too young, which means they should be reading the Harry Potter series written by that transgender-bashing cis white billionaire, or probably have long since rounded the bases and are getting kinky with their boyfriends in ways that would curdle your blood. I also write this for Gerry (and his kids)…

Collum is a whiny moron…You would interview someone like that, a Trump-supporting climate denier…he’s a total idiot who needs to FOAD [fuck off and die]. He simply refuses to acknowledge facts…

~ Gerry Muller, my most audacious hate mailer, responding to Jim Kunstler for his audacity.

The title is a takeoff on the website entitled, “WTF Happened in 1971”, which uses 50 graphics to document that the world changed abruptly in 1971.ref 2 (The gold bugs know why.) It is undeniable that 2020 will be a year of abrupt change as well—a phase change so to speak—but to what future is unclear. We all squandered inordinate kilos of ATP trying to understand events in ways that would not make us happier people and for which an answer key eventually would be forthcoming.

We have to be very careful about how we spend our time…be very careful about not being manipulated into narrative after narrative….The Eye of Sauron is focused on climate, covid, and race. I’m not going to get caught up in it…Everything we get distracted onto we don’t make better.

~ Douglas Murray (@DouglasKMurray), author of The Madness of Crowds

This year posed challenges writing the damned thing, some common and others unique. Of course, I don’t have the luxury of casually surveying a year. Ya can’t be Toobin’ all day and patch it together in your spare time. Ya gotta Stephen-King the mother. Why not write it quarterly? Simple: it takes my beautiful mind that long to spot patterns in random noise and deconvolute the chorus of voices in my head. Also, nobody—and I mean nobody—in their right mind wants to rehash the events of 2020. The annual YIR is always about human folly, but how much folly is there when we’re all living in our basements (Joe)?

I tease Dave about his “Technical Analysis Wizardry,” because I want him to write a children’s book on charting. Still, I can’t deny that he often captures the market zeitgeist in one tweet.

~ Tony Greer (@TGMacro), TGMacro

Keeping it light was a Herculean task. I kept getting pulled by Lord Vader toward a revenge mindset, which I have curbed with only partial success. Epithet-rich allusions to baseball bats kept getting smuggled into the prose stemming from undiagnosed coprolalia, the acute swearing component of Tourette’s Syndrome. Some commenter after a podcast said (paraphrased), “This guy sure wants to put a hurt on a lot of people.” Indeed. The sense of frontier justice runs deep in the entire Collum clan. Horse thieves beware. I don’t need anger management; I need people to stop pissing me off. Ad hominem attacks are reserved for the total douche bags.

Writers are desperate people, and when they stop being desperate they stop being writers.

~ Charles Bukowski, American Poet

I was inadvertently ready for the pandemic in some odd ways. I love medieval history, had just finished a book on the Black Death in the fall of 2019, and was pondering immunology when Covid-19 struck. Ah, the first contention: I refuse to capitalize the whole thing because COVID-19 makes no sense linguistically—it’s not correct for an acronym or proper name—and using all caps is shouting and distracts from other attempts at emphasis. SHOULD I TYPE LIKE THIS? I don’t care what everybody else on the planet does. They are wrong. Screw ‘em. I appear to have gotten Covid-19 at birth; I have been tasteless and urged by friends and family to social distance since childhood. Obviously I should wax philosophically about the Covid-19, right? But what do you say to 350 million basement-dwelling bunker monkeys who are now expert epidemiologists and virologists with rock-solid opinions of what parts of the pandemic sucked the saltiest balls? I dedicate far less page space to the pandemic or the elections than you might expect.

It is so much better to tell the truth than to just shut up.

~ Douglas Murray (@DouglasKMurray), author of The Madness of Crowds

The YIR poses risk—possibly considerable risk—every year, but this year is special. No guff no glory I guess. There are a ton of social justice crazies (SJCs) out there. In the 65th year of my personal sitcom, the writers keep hurling absurdities to keep the series running, but I got canceled anyway. No, not by Covid-19 (unless this is The Sixth Sense) but by the diversity-industrial complex otherwise known as the Klan of the Kancel Kulture (KKK), virtuously broadcasting to the world that I am a seriously twisted bastard. It is hard to argue with that. However, if people in visible positions feel they cannot speak up right now, when will they speak up? On their deathbeds? If a 65-year-old tenured professor can’t express unpopular ideas, who can? A 9-to-5-er who could be fired in a heartbeat has no voice. I will keep spewing drivel because somebody has to do it.

Factoid: You cannot breathe with your tongue sticking out of your mouth.

Stuff your tongues back in your mouths you idiots. Of course you can. I have become increasingly aware that we are all looking through our own lens with an emerging plotline that is self-consistent with our own unique narrative. As described in The Social Dilemma, the narrative is shaped nefariously by ideologically dubious weasels in Silicon Valley running their MK-Ultra experiments on us through mass and social media. As I jam more pixelated pseudo-factoids into my noggin, doubts about their veracities are debilitating. How is it that smart blokes can peer at the same data and draw diametrically opposite conclusions? If I offered you $1000 to convince just one person—one person—that they were wrong about Russia collusion, the Biden laptop, election fraud, or the merits of sheltering, could you do it? Didn’t think so. Some of us must be, as Gerry would say, whiny morons who should simply FOAD, but we all have our truths that we will defend, Goddammit! This annual tome is, necessarily, the World According to Dave. At times it will sound narcissistic, but it’s not. [Editor’s note: yes it is.] It wanders through a range of topics in no way statistically weighted to their global importance but presented in a Michael-Lewis way sniffing out the story beneath the story. What my four regular readers would tell you is that I try to write about what others are not pondering. I don’t always find the rotting corpse, but I am attracted to foul odors.

Sturgeon’s Law: 90% of everything is crap

The Year in Review (YIR) is broken into two parts with individual sections hot-linked in the contents below. The whole beast can be downloaded as a single PDF here.

Contents

Part 1

Introduction

Contents

My Personal Year

Conspiracy Theories

Decade in Review

Investing

Gold

Wealth Creation

Valuations

Broken Markets

Bailouts

Healthcare

Link in Part 1

Part 2

Epilogue–Epstein

Epilogue-Climate Change

Rise of the Cancel Culture

The Tweet and Cancel

The Buffalo Shove: The Real Story

College Life

Political Correctness—Adult Division

Group Statements and Identity Science

Anatomy of the Riots

The Death of George Floyd

Covid-19: Just Opinions

Where to from Here?

Acknowledgments

Books

Links in Part 2

My Personal Year

How about ‘Batshit political views and how to succeed despite them?’

~ a colleague, when asked what topic I should present in a guest lecture

We all suffered from suffocating acedia—a melancholy specifically resulting from monastic isolation known only to ye olde linguists.ref 1 All things considered, I personally had it as good as you could ever hope, and none of us were sleeping in the London Tube at night to avoid the Luftwaffe. We sheltered with my 30-year-old youngest son Thomas and his main squeeze, got a lot of sun enjoying casual dinners and great chats, followed by a ritualistic dragging our asses through the grass after running out of toilet paper. But by mid-year there was a notable pall over the Shire, and orcs were spotted in the woods. One prays this is not a trilogy.

We are all biodegradable and progress through three stages of life: stud, dud, and thud. I thought getting old would take a while. I was wrong. You start life trying not to wet yourself and end life trying not to wet yourself. The middle is the fun part. The final days—pretty much gruel and drool I figure—will probably suck. While trying to avoid stage three, I put on 6 lbs sheltering but ripped off 26 lbs in the last 10 weeks (within 40 lbs of my crack weight.) You’ve gotta touch that bag before leading off again. I didn’t make it to the gym this year. That makes 15 in a row. I had a hernia fixed before the lockdown, still piss bladder stones every week or two (trying not to wet myself), came up negative on prostate cancer, make sound effects simply getting out of a chair, and learned how to cut my own hair. (The ears are easy, the back is quite a reach, and manscaping is unnerving.) We started with five dogs in the house and ended with six. The two visiting Boston Terriers inspired us to get Charlie. (Check out this video.ref 2) Charlie is great. It is nothing but Boston Terriers (and turtles) from here on.

I intend to retire at 70; the runway lights are in view. Much of the sand in the hourglass has fallen. It’s a little weird when you realize you are no longer building a career but trying not to crash land it. As a depreciating asset, your bucket list grows short as your fuck-it list expands. I occasionally read death-bed regrets: nobody ever worries about the bloat of their in-box.

Dave is the man who can rant better than anybody I’ve ever met.

~ Marty Bent (@MartyBent), Tales from the Crypt podcast

I did a lot of podcasts—some with encore performances—since my last Year in Review. They are listed unceremoniously as follows:

Chris Martenson (Peak Prosperity, @chrismartenson)ref 3

Jim Kunstler (Kunstlercast; @Jhkunstler)ref 4

Rick Sanchez (RT; @RickSanchezTV)ref 5

Chris Irons (Quoth the Raven; @QTRResearch)ref 6

Marty “Hodler King” Bent (Tales from the Crypt; @MartyBent)ref 7

Sam McCullough (end of Chain; @traders_insight)ref 8

Jason Burack (Wall St for Main St, @JasonEBurack)ref 9

Zach Abraham (KYR Radio; @KYRRadio)ref 10

Elijah Wood (Silver Doctors; @SilverDoctors)ref 11

Justin O’Connell (Gold Silver Bitcoin Podcast; @GldSlvBtc)ref 12

Anthony “Pomp” Pompliano (Morgan Creek Digital; @APompliano)ref 13

Ryan Ortega (Jelly Donut, @JellyDonutPod)ref 14

Thomas George (Grizzle; @thomasg_grizzle)ref 15

Kenneth Ameduri (Crush the Street)ref 16

Dan Ferris (Stansberry Research; @dferris1961)ref 17

Max Keiser and Stacey Herbert (Keiser Report; @staceyherbert and @maxkeiser)ref 18

Fergus Hodgson and Brien Lundin (Gold Newsletter Podcast; @GoldNewsletter)ref 19

Phil Kennedy (Kennedy Financial)ref 20

Phil Bak, CIO at Signal Advisors (@philbak1)ref 21

A bucket-list interview with Tony Greer (@TGMacro) on RealVision that had disappeared for months was found last year and officially posted this year.ref 22 (I actually suspect it had been censored by a former employee to protect their reputation.) I had a ball serving on a panel discussion at the 2020 New Orleans Investment Conference with Adam Taggart, Chris Martenson, and Dominic Frisby.ref 23 A quick search of Zerohedge shows 61 mentions over the years. That officially makes me a Tool of the Kremlin. (I haven’t run into The Donald nor Tulsi there yet). I found a webpage that professed to help you “Find out what the best investors are reading, writing, and saying” and was shocked to find my name on it. That ten minutes of fame has now rolled off the page to the Dark Web. My Keiser Report interview got translated to Spanish and was real haga clic en cebo.ref 24 I had a tweet make it into an elite medical journal, Stats:ref 25

A feature in Business Insider is too funny and too plot thickening to blow by here. (See “Broken Markets”.) The biggest downer in a year full of downers was being “canceled” by neo-Marxist SJCs. (See “Douche Bags”…no…sorry…“The Tweet”.) It was world-view changing and not pretty. The hinge-free left is a fountain of spew and vitriol. I usually put in a “Trigger Warning,” but if you are still reading you are either a bit of a perv or already building a case against me.

Conspiracy Theories

Are Conspiracy Theorists Epistemically Vicious?

Charles R. Pigden, sophist-douche bag

Hanlon’s razor says that you should never assume malice where incompetence will suffice. OK, but oftentimes it does not suffice. Collum’s razor says never be so narrow-minded that you refuse to believe men and women of wealth and power conspire. Those who do are probably happy not to swat those flies. Years ago I served on a PhD committee of Jim Rankin, a successful businessman from Dallas, who wrote a pretty damned interesting thesis on conspiracy theories.ref 1 There is scholarly work out there, and then there is Charles Pigden, Cass Sunstein (whose wife, Samantha Power, is a neocon), and Michael Shermer, all writing embarrassingly biased tripe that pays their mortgages. I say this every year: Stop declaring, “I am not a conspiracy theorist but…” and grow a pair. Embrace the label that horrifies you. Admit that the world is filled with sociopaths trying to screw us with complex plans. Use your fookin’ head and your gonads to stand up to the scoundrels.

A University of Chicago study estimated in 2014 that half of the American public consistently endorses at least one conspiracy theory. When they repeated the survey last November, the proportion had risen to 61%. The startling finding was echoed by a recent study from the University of Cambridge that found 60% of Britons are wedded to a false narrative.

A chemist at Cornell reports that a disturbing 39% of the American public are mushrooms—in the dark and fed horse manure.

Decade in Review

I love metaphors and similes. A particularly instructive one is Parker Brothers, Monopoly. The players all start with reasonable amounts of money. As the game proceeds, players collect $200 by simply passing Go and use this money to speculate on real estate. By the end of the game, only $500 bills are worth anything, the whole thing blows up, and most of the players end up destitute. I wonder why the originator of the game (Elizabeth Magie, not Charles Darrow) didn’t name it Inflation. In a twist of irony, an original game board sells for about $50,000.

~ Year in Review, 2010

I took a little time to thumb through a decade of YIRs to find sections that I am still proud of and seem to have withstood the test of time. Few have read all ten—Hi Mom!—but I know of fintwit legends who have. In some ways, I think the earlier YIRs were better because I was working at lower levels of the intellectual strata. To minimize repetition, I bypass ideas worth talking about. For example, I was writing about a disturbing change in the mood of society by 2011. Some of these sections are wiggy topics that stayed off radars and were stuffed down memory holes, but I still stand by them and think they retain appeal to the open-minded. In chronological order:

2002 Subprime Crisis prediction (republished in 2012): My best prediction.

Buffett Takes a Bath (2011): Pulling the curtain back on the Orifice of Omaha.

The Constitution and the Fourth Estate (2011): Early thoughts on the failure of media.

Paul Krugman’s Greatest Quotes (2013): This guy is just too funny.

Militarization of the Police and Civil Asset Forfeiture (2014): Police problems are not new.

Problems with the Roth IRA (talk given in Las Vegas in 2014): Consult your financial advisor.

Election (2016): My analysis of WTF Happened in 2016.

Price Gouging (2017): Why they are neither evil nor pervasive.

Antifa (2017): They’ve gotten worse.

Russiagate (2017): Baloney from the outset.

Las Vegas Shootings (2017): A seriously untold story.

Pension Crisis (2017 and 2018): The latter was reproduced verbatim by Solari.

Valuations (2018): Exhaustive look as a setup for this year’s writeup.

Syria (2018): Story of fake gas attacks before the media got it.

Kavanaugh versus Blasey-Ford (2018): The sub-surface details.

Skripal Poisonings (2018): Not what they appeared to be.

In Defense of Religion (2018): Through the lens of a pro-choice atheist.

Collum-An Autobiography (2019): In case you care to know.

Modern Monetary Theory (2019): From risk to reality in one year.

Climate Change (2019): Where science and politics collide (briefly mentioned in Part 2).

The Jeffrey Epstein Affair (2019): He ain’t dead (and briefly mentioned in part 2)

Investing

I finished 2020 with my total assets distributed 23% gold, 2% silver, 54% cash-like entities, 12% in real estate (my house, no mortgage), and 9% in a smattering of equities. The large cash prevents my returns from ever moving abruptly. I hope to put it to work someday. This year gold and silver returned a respectable 20% and 32%, respectively, although the fairly standard early-season rally began looking like a dead-ingot bounce by November. My overall accrual of wealth (ex-house appreciation) came in at 10.9% following 5.7% last year. Of course, it failed to keep up with Tesla, Moderna, and Bitcoin, but my crystal ball and Ouija board remain in the shop. (Note to self: pick up laptop.)

My best decade of the past four was from 01/01/00 through 12/31/09 with 13% annualized returns while the S&P made nothin’ (dividends included). Hold your applause. There is plenty of schadenfreude to go around. I missed the equity ramp from ’09–present. I am also not stupid; I sure wish I had caught that ramp. My reasoning behind the decision to sit it out (delineated in “Valuations”) was based on far superior reasoning to the completely vacuous reasoning in the 1990s that lavished me with wild returns including one year >100%. All you have is reasoning and luck. Those unsatisfied with decent returns are doomed to lose it all. “Easy come easy go” but Nick Carnot would disagree. I have enough to retire with inflation-adjusted zero-percent returns. I do, however, wish to leave some money to my kids, who are in a generation that will struggle to accrue wealth. I worked hard to bestow such privilege.

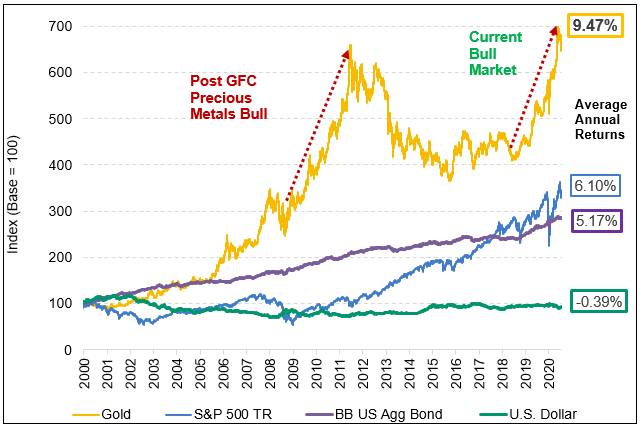

Figure 3. Two decades of gold versus equities (ex-dividends, taxes, fees, and inflation).

I’ve been a gold bug since 1999, chasing it down from 290 to 270, chasing it up from 300 to 450, and topping off the stash in 2016 in the 1200s after the swaffling by a cyclical bear market seemed to subside. It has served me well with a position that now is equivalent to six gross annual salaries. While the equity wankers thump their chests, the gold bugs quietly whooped their asses for two decades (Figure 3). JPM showed that gold beat the total returns of the S&P by 2% annualized. Gold even beat Buffett by a nose over the two decades.

Figure 4. Gold vs S&P capital gains for 2020 (ex-dividends, taxes, fees, and inflation).

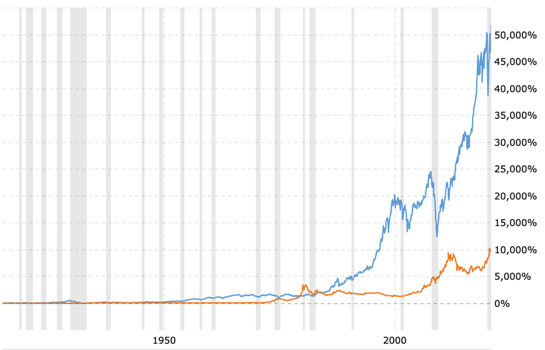

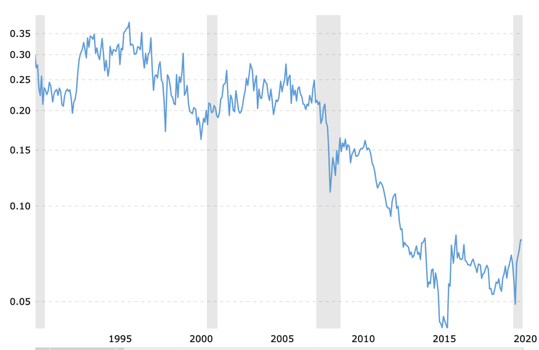

I am waaay more comfortable holding gold than the S&P 500, which has great momentum and horrid fundamentals (see “Valuations”). I’d love to replace the gold with productive assets someday but not yet. Graphics from a useful website Macrotrendsref 1 shows gold cannot win in the long term (Figure 5) but has returned a credible 8.4% since it started trading in the open market in 1973 after a half-century hiatus. You can win in the shorter term as shown by the S&P-to-gold ratio (Figure 6). The buy-of-the-century in 1999 was terrifying at the time but crystal clear in hindsight. It was that same S&P-gold ratio that kept me white-knuckling gold from 2013 forward; it never plumbed serious lows, leaving potentially more multiples of relative gains prospectively. I’m still waiting. I own no gold equities because the CEOs don’t seem to know how to make money, but you can see in Figure 7 why serious analysts are salivating.

Figure 5. Price of gold (yellow) relative to Dow (blue)

Figure 6. S&P-to-gold ratio

Figure 7. Philadelphia Gold and Silver Index (XAU) versus gold

People act like it’s a choice. Returning to the gold standard is the answer to a problem that leaves you no choice.

~ Grant Williams (@ttmygh), author of Things That Make You Go Hmmm…

There is a growing institutional bullishness for gold. Bank of America analysts noted that “as central banks and governments double their balance sheets and fiscal deficits, we up our 18-month gold target from $2000 to $3000/oz.” Goldman went bullish on gold while questioning the dollar’s reserve currency status, which is a sell signal to those who think they lie a lot. Buffett raised eyebrows when he sold his airline stocks, half of his Wells Fargo, and all of his Goldman shares (grabbed up on fire sale in ’09) while snarfing up a stake in Barrick Gold.ref 2 He has thrown more feces on the bugs over the years than a rhesus monkey.

The energy sector which has never, in nearly 100 years of data, performed so poorly relative to the index as it has over the past 12 months. These rubber bands are all about as stretched as they have ever been…it is time to get greedy on energy.

~ Jesse Felder (@jessefelder), author of The Felder Report

A bullish case can be made for various value sectors that include emerging markets, tobacco, and energy (see “Broken Markets”), but I am still thinking. Once I decide to enter one or more of these lurking opportunities, it will be quick and bold on a one-decision trade—I will marry it—and probably ride it till death do us part. I am not a trader, but stock toshingTM is risky in these crazy markets. [Note added in proof: I said, “Fuck it; let’s do it” and have started buying energy and precious metal equities.]

One of the smartest people I follow thinks the stock market is going to drop by 50%. I like David Collum a lot but this time he’s dead wrong. Another very bright financial investor named John Hussman believes not only that the Fed is powerless, he says the stock market is going to collapse by 67%. Both predictions are interesting but basically absurd. Those guys are way too optimistic.

~ Bob Moriarty, Founder of 321 Gold

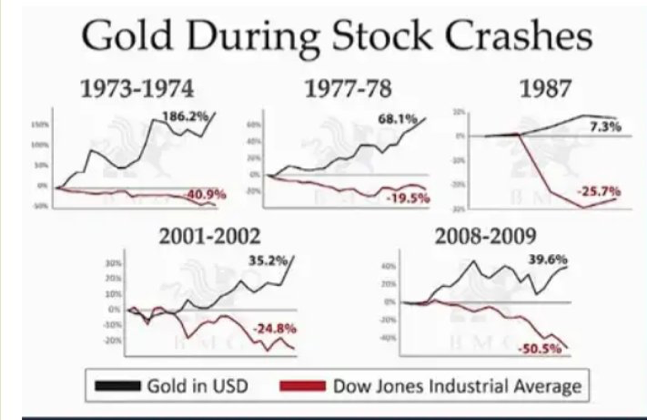

I have been making and will continue to make (see below) my annual case for a vicious secular bear market in equities and, quite possibly, bonds. But Dave (says one of the voices in my head): won’t investors sell anything not locked down, selling what they can not what they want? Yes, but look at gold in previous equity bear markets:

Gold

A tsunami of $8.5 trillion of Treasuries will be maturing by the end of 2021! Monetary stimulus will have to be astronomic to cover this. What a time to be a precious metals investor.

~ Otavio (Tavi) Costa (@TaviCosta), Crescat Capital

Chaos in the Comex. There was unusual turbulence underneath the surface of the gold market this year. Debates have raged for years about whether demand for physical gold would someday overwhelm the paper gold (futures) market. Many suspect the paper gold market is used to suppress the price of and demand for physical gold. GLD was introduced in 2004 as a convenient way to buy gold, but claims in the prospectus that HSBC actually holds physical gold seemed like a rehypothecated Leprachaun story to me. HSBC’s compiled rap sheet is also disquieting.ref 1 (I think HSBC is the reconstitution of BCCI.ref 2) The Comex trading platform where you roll contracts forward stipulates that you can take possession provided not too many others try to do so as well; they are 1% fractionally reserved of the metal.ref 3 Nooo problem! On a more humorous note, former Facebook founders and current bitcoin hodlers—the Winkelvoss twins—assured us that Elon Musk would soon swamp the globe with physical metal by mining it on the moon. There are many issues with this moonbat theory, not the least of which being that you are more likely to find swiss cheese than gold on the moon.ref 4

There is no price discovery in the market right now. If you need to borrow gold in the over-the-counter markets right now, you are going to pay a king’s ransom…There is plenty of gold in the market, but it’s not in the right places. Nobody can deliver the gold because we are forced to stay home.

~ Ole Hansen (@Ole_S_Hansen), Saxo Bank’s head of commodity strategy

Welp. The Comex started breaking records for demands of physical delivery while Covid-19 created sourcing problems.ref 5 Approximately 550 tons bled from the Comex, causing the price of gold futures and the spot price of gold to part ways pronto. HSBC is said to have been gutted for $200 million in one day by the “spreads” blowing out.ref 6 One could imagine, in the limit, the futures going to zero as traders realize they are unbacked promises. Not possible? Oil futures hit –$37 per barrel albeit for different reasons,ref 7 but that sure as hell wasn’t supposed to happen either. The futures-spot spread on the London Bullion Metals Exchange (LBMA) blew out with an ensuing mad scramble to change the rules as to what form of gold (bars versus bling) the delivery could be in.ref 8 The Comex and LBMA were joining forces to supply the metals by digging into their 400-ounce bars in the Bank of England that had not seen the light of day for decades.ref 9 Some may recall that the quality of those bars was questioned several years ago when somebody noticed they were “flaking”.ref 9 (Real gold doesn’t flake.) The LBMA publically stated that it “offered its support to CME Group to facilitate physical delivery in New York”, while the big banks were stepping on Comex trading limits. Retail buyers in Germany formed lines at gold stores after authorities dropped the amount they could purchase.ref 10 Some banks like ABN Amro said screw it and exited the whole game with big losses, which also forced their customers to liquidate their gold right when the banks needed it.ref 11 That was lucky for the banks, eh? Others profited through arbitrage by buying low abroad and selling high in the US. Some drew analogies to the 1968 gold rush when the London Gold Pool lost control of their price-fixing scheme.ref 12

The Central Banks are going to go into a new, non-conventional toolkit called debt monetization. They will lose control of the monetary base, and then we will go into a situation where, even with technology and with aging demographics in the industrialized world, we will be talking about inflation again. That might come in the next 18 to 24 months, and gold is going to skyrocket.

~ David “Rosie” Rosenberg (@EconguyRosie), Rosenberg Research & Assoc

Bank of America’s Global Commodities Research team suggested that maybe paper gold is no longer as important as it used to be,ref 13 which is synonymous with “nobody wants that paper crap anymore.” Seems that taking delivery plays the same role in commodities as a $500 cap on a $2 blackjack table. It precludes unlimited doubling-down speculation. That game may be over sooner than many thought possible. Meanwhile, the Russian central bank’s gold reserves grew by >5% in one month, becoming >20% of their total reserves.

The Fed may be forced to buy gold to maintain the appearance of responsibility for the world’s reserve currency….Global consumers are more familiar with gold than the banking system. Thus, this avenue of monetary expansion might finally lift the anchor on inflationary expectations and their associated spending habits.

~ Scott Minerd (@ScottMinerd), Global Chief Investment Officer, Guggenheim Partners

Fraud. What would the gold markets be without criminal activity? The Potemkin regulators are building a racketeering case against JPM for “spoofing” the markets, hoping to pry loose some hush money. Somebody may have duped the Chinese with 83 tons of fake gold.ref 14 Bank of Nova Scotia got fined for $127 million for metal price manipulation.ref 15 Based on the Collum Three Percent Rule, that means they made upwards of $4 billion en route to this surcharge. As usual, paying a big fine with no admission of criminal wrongdoing is paradoxical. Nobody went to jail. Nobody ever does.

Fiat money will be a passing fad in the long-term history of money…I’ve always found many commodities difficult to recommend on a buy and hold basis as most underperform inflation over the long run…Gold is definitely a fiat money hedge.

~ Jim Reid, Credit Strategist, Deutsche Bank

WTF Happened in 1971? A website with this title blew into view this year.ref 16 It shows over 50 financial plots of all shapes and sizes showing marked discontinuities in 1971. Several are shown below. Wow. WTF did happen in 1971? Nixon took us off the last vestiges of the gold standard.

Figure 1. WTF Happened in 1971?ref 16

We have gold because we cannot trust governments.

~ Herbert Hoover, President of the United States, 1928–32

Silver. A 32% gain in silver since my last YIR has more than a few sitting up and taking notice. It got entertaining when a rag-tag bunch of loons called the Robin Hodlers (see “Broken Markets”) put the silver ETF, SLV, on their buy list.ref 17 It rallied briefly but then gave that gain all back as is always the case when the amateurs get in the game. Silver dropped >15% in one day as the Robin Hodlers got chased back to the forest by the Sheriff of Price Discovery.ref 18 The Chaos at the Comex also included silver, causing some seriously upward movement. Goldman became overtly bullish silver citing solar panels as their motivation.ref 19 Beware: this is an old and possibly lame argument. Some say the enormous gold-silver ratio is bullish for silver, but this is only so if traders act on it. Others suggest the price is determined by investor preference for the stock (above ground supply) and flow (mined).ref 20 It leaves me feeling like a speculator. I have about two annual salaries committed to this hybrid precious-industrial metal but am not as convinced I understand it as I used to be. The inflation-adjusted price of silver is also not that inspiring in historical context (Figure 2).

Figure 2. Macrotrends charts do not make silver look cheap

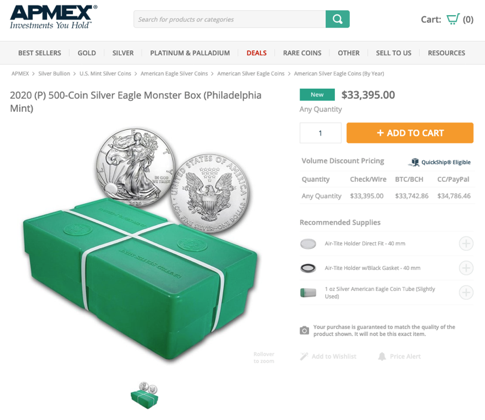

A quick scan of the uncontestably retail silver market on Ebay shows what the retail crowd is doing. High (30%) premiums on silver eagles suggest froth. Recently released Apmex silver eagles were said to be a limited edition. They sold for a nearly 200% premium. Lacking mint marks, the claim is that they can be identified by the notations on the unopened box. Let me get this right: we know what’s in the boxes only if we don’t open the boxes? Sounds like the refrigerator light paradox or beanie babies retaining value with the original tag.

Figure 3. Limited-edition silver eagles.

Wealth Creation

The more people who own little businesses of their own, the safer our country will be, and the better off its cities and towns; for the people who have a stake in their country and their community are its best citizens.

~ John Hancock, 1st and 3rd Governor of Massachusetts

I have been Toobin’ along for several years trying to understand the distinction between wealth creation, aggregation, and transfer. The shutdown of the much-ballyhooed service economy has inspired me to stroke the keyboard. What follows is a compilation of thoughts that are loosely stitched together in an attempt to drive economists completely nuts. It wanders a bit but serves as a preface to understanding post-modern markets.

During the Covid-19 shutdown, the Fed replaced lost wealth creation with wads of cash—an inflationary wealth redistribution. Meanwhile, the populace lived less ostentatiously akin to their ancestors of a century ago. We needed food, shelter, clothing, healthcare, and the internet (email, Zoom, and porn). Restaurant meals were replaced with the Joy of Cooking. Homemade bread was boss, resulting in a yeast and flour shortage. We cut our own hair and replaced excursions to Aruba with camping and hiking. Couples walked, jogged, and biked together. One can imagine younger couples may experience a baby boomlet in 2021. I ate meals on my deck and chatted deep into the evening with family.

What good was the consumer economy that tanked in our absence? What the hell is a “consumer” or “service” economy anyway? You eat what you kill. You have to produce it to consume it, no matter how much money lines your pantaloons. (Come on, man. Pantaloons?) If we provide services abroad, we pocket a few IOUs for later consumption. Trade deficits mean those other guys are pocketing the IOUs. If our trading partners are producing and we are consuming, we are getting poorer by pulling consumption forward via vender financing, and they are getting richer accruing chits. We will be working for them someday. Big trade deficits steer the US toward the Trouble with Triffin—Triffin’s Dilemma —which is the ultimate and supposedly unavoidable collapse of the reserve currency as delineated by Robert Triffin.ref 1

I was reading in the paper today that Congress wants to replace the dollar bill with a coin. They’ve already done it. It’s called a nickel.

~ Jay Leno

Inflation. What happened in the past when money creation substituted for wealth? The Romans hit the goldmines hard and discovered that increasing the gold supply inflated prices. Aggressive debasement of the metal content of their coins made it even worse. Unlike dicking around with their currency, building the Appian Way and aqueducts with an army of engineers masquerading as soldiers was real wealth creation; parts still exist to this day. The rise of the Renaissance and a massive rise in the Wealth of Nations following the Black Death is often ascribed to the increasingly sought-after peasants—the new middle class shaking off serfdom—being paid more. Maybe so, but there must have been a concurrent rise in per-capita productivity, which likely arose from the emergence of more free and open markets. Hundreds of millions of peasants, when left to their own devices, will innovate and create a lot more wealth than a few Kings busily molesting wenches and attacking their neighbors. It was, however, good to be King.

The Great Bullion Famineref 2 (whatever that is) of the 15th century was replaced by a pan-European boom when a 16th-century silver mine in Bohemia afforded oodles of silver and resulted in the introduction of the silver Thaler (from whence the term “dollar” derives).ref 3 Modern dogma suggesting the creation of money created wealth obscures the story of a temporary inflationary boom and the increasing divisibility of the currency promoting commerce. (We all know how hard it is to buy a fowl or a tankard of ale with a gold guilder.) While the discovery of the New World ultimately led to some serious wealth creation, the gold shipped to Spain by the conquistadors created nothing more than inflation, with the Spanish enjoying the perks of the Cantillon Effect—the benefit of being first in line before inflation appears in earnest. Discussions of the Cantillon Effect also underscore the aftershocks when the Spaniards failed to develop independent industry.ref 4 Modern era lottery winners are new-era Spaniards.

Lottery winners are more likely to go bankrupt within 3–5 years than the average American.

Robert Gordon argues a rise in real (inflation-adjusted) wages owing to fantastic gains in per-capita productivity actually caused (rather than was caused by) the great 20th-century expansion. (There’s more on Bob below.) Again, hundreds of millions of workers will revolutionize the world compared to a handful of robber barons with hot flappers in tow doing hostile takeovers of their competitors. Now we are witnessing a massive and growing wealth divide that is tearing the social fabric and undermining the statistically overwhelming contribution of 7.5 billion people who could innovate. The workers are once again filling the coffers of a few Kings (and Queens) with hot chicks in tow who are richer than Croesus in the Valley of Silicon. Mind you, I am not arguing for a wealth redistribution but instead that the Cantillon Effect is causing the distribution mechanisms to fail. Labor is battling capital for its share of the pie. Meanwhile, the capital keeps propagating like gerbils as if some asset mangling central bankers sequestered in the bowels of the system are printing the damned stuff without brrrreaks. This iatrogenic Monetary Munchhausen-by-Proxy Syndrome is also WTF Happened in 1971.ref 5

Capital needs to cost something for a dynamic economy to work.

~ Sheila Bair, former FDIC Chair

Just now, America is producing almost nothing except money, money in quantities that stupefy the imagination — trillions here, there, and everywhere.

~ Jim Kunstler

Increased per-capita productivity correlates with real wealth creation. All boats rise, some more than others. Keynes predicted that technology would shorten our work weeks to 15 hours—another one of his dubious theories kaput? (Sorry for the dig, Maynard. Shake it off.) Author David Graeber argues Keynes was correct and that the void is filled with what Dave called “bullshit jobs.”ref 6 Are we paying people to dig and then fill holes? I will try to pull this all together, but not yet.

If your lost job and income can be replaced by simply giving you government-issued checks, what were you doing that was so important?

GDP versus NDP. I once swapped emails with a prominent economist and Great Depression expert, Professor David Kennedy of Stanford.ref 7 (I have a point coming so hold your horses.) I submitted that the Great Depression was not ended by WWII but rather continued to the end of the war. The highly constrained personal consumption (rationing) was the blowoff bottom—the last drops of excess created in the 1920s wrung out of the system—that set us up for a surreal post-war boom. He suggested I was full of shit (paraphrased) by noting a 15% growth in GDP during the war and that the war-time hardship stories are overstated. With ten years of reflection, I am not yet giving up. To understand my point, I am going to offer an alternative metric for wealth creation.

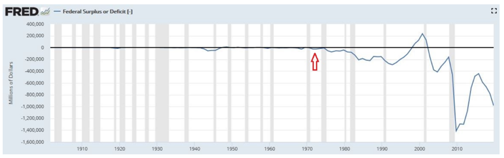

Everybody’s favorite measure of wealth creation, of course, is GDP (or GDP per capita), which is defined as

GDP = C + I + G + NX

C is personal consumption,

I is gross private domestic investment,

G is government purchases,

NX is net exports (exports minus imports)

We must use real (inflation-adjusted) GDP. Most agree that the inflation correction got all garbled up (juiced) by the Boskin Commission’s fudge factors that are necessary in theory but corrupted in practice.ref 8 Those weak-minded who think inflation is too damned low and are cooking their breakfast in a teaspoon over an open flame should pull themselves out of that pool of vomit and check out the Chapwood Index. It is a highly transparent measure of inflation in the 50 largest cities.ref 9

Figure 1. Chapwood inflation index.

Best I can tell, the creation of debt has not been subtracted from the GDP numbers either and, certainly, the correction for inflation is not at Chapwood-levels. According to the internet, if you subtract debt from GDP, we have had negative GDP for years. (We amassed gargantuan debt during WWII, which will be a component of my argument.)

Fun fact: My BHAG (estimate) of the global GDP at the time of Christ in 2020 dollars is $90 billion—a subsistence-level $300 per capita—compared with $80 trillion today ($10,000 per capita). Ergo, global per-capita GDP grew <0.2% per annum over two of the coolest millennia to date. Buying a global equity index fund spanning the growth of civilization would not have been that profitable.

Let me introduce what I think is a better metric of wealth creation called the Net Domestic Product, or NDP, defined as…

NDP = GDP – depreciation

NDP is one of the key gauges of economic growth reported by the Bureau of Economic Analysis (BEA).ref 10 If depreciation is low, NDP is high and vice versa. Investopedia says that a large GDP is good news whereas a high NDP indicates “economic stagnation.” As the macroprudential reasoning goes, it is during good times that you witness the replacement of the old with the new—balls-to-the-wall creative destruction. Failure to upgrade production facilities eventually decreases the country’s GDP. (Just ask those who lived through the 1970s in Pittsburgh.) Maybe so, but replacement cycles are expensive and can be fast. The really frothy ones smack of Bastiat’s Broken Window Fallacy: smashing and replacing windows juices the GDP without creating any wealth.

Let’s look at the underbelly of NDP. When those Romans constructed bridges, roads, and dwellings they created some serious wealth owing to profoundly slow depreciation. That is serious NDP because depreciation was near zero (NDP = GDP). At the micro-level, rapidly depreciating consumer goods stifle wealth accumulation (savings). Your house is full of crap with the life expectancy of a Clinton email server, none of which can be repaired. Replace your iPhone with each new model and watch what that does to your savings. Better yet, bulldoze your house every 20 years, build a better one, and tell me how that works out. In fact, the enormity of CSFs (Crap Storage Facilities) known as McMansions built with Chinese sheetrock and chincy hardware decay like scenes from Inception. I have previously called this accelerated replacement cycle—the high cost-per-use—a massive hidden inflation.ref 11

What does the service economy look like through the lens of NDP? The GDP contribution of a family night at the movies is equivalent to several Black & Decker power tools. The latter are labor-saving devices that last at least a few years (although not like those made 50 years ago). The family movie night depreciates in <3 hours (although the popcorn slathered with WD40 stays with you longer.) Two haircuts may last you two months whereas one pair of hair clippers can shave many heads, crotches, ears, backs, eyebrows, armpits, and dogs. A bioengineering degree from MIT depreciates considerably more slowly than a degree in grievance studies at Evergreen State College. The latter is a resume-destroying educational timeshare with a negative net worth in a job interview, which you will never get.

If you overuse one of the factors of production, such as debt capital, initially GDP will rise. You continue to overuse that factor of production, GDP flattens out; and if you continue to overuse that factor, GDP declines. More is not more — more is less.

~ Lacy Hunt, the legend from Hoisington Investment Management

Back to the debate about whether WWII ended the Great Depression. Admittedly, the war machine had lasting effects as new methods of mass production—Ford’s assembly line on steroids—evolved to crank one bomber per hour in a single plant. We also constructed transcontinental oil pipelines. Nonetheless, there is an offset because the War Machine was financed with debt, which is consumption pulled forward from subsequent decades. The product of the War Machine itself—bombs, planes, ships, and bullets—contributed massively to GDP but had inordinate depreciation rates (fractions of seconds in some cases). The utility of a bomb is truly ephemeral. The NDP on most of those armaments was a rounding error from zero. Let’s drive this home using a contemporary example: the $6 trillion spent on wars in the Middle East also contributed greatly to GDP but almost nothing to NDP. It would be nice to have that cash (or should I say productive labor) back, wouldn’t it? Accounting for debt pulled forward and rapid depreciation, did the WWII really bring us out of the Great Depression? In part yes, but only in part, and only in my opinion.

I think the technology answer has been provided to us by Dr. Robert Gordon at Northwestern. He said in our period of great growth from 1870 to 1970, we had transformative, revolutionary inventions…The technological changes today are more evolutionary, not revolutionary. The production function is one of the most fundamental relationships in all of economics, and it’s telling us we’re facing a period of difficult growth.

~ Lacy Hunt, the legend from Hoisington Investment Management

Inventions Past and Present. In a fabulous book, The Rise and Fall of Growth in America (see “Books”), Robert Gordon argues that the industrial revolution from 1870–1940 was a unique and not-to-be-repeated period of wealth creation. The period from 1940–1970 was OK, whereas the modern era is a mediocre stretch that was briefly interrupted by a technological spike from 1995–2005. (That’s when the porn showed up bigly.) Before you technophiles soil your thongs, Gordon is not alone. Robert Solow, winner of the Nobel Prize for Total Factor Productivity, TFP,ref 12 quipped that you can see the influence of computers everywhere but in the productivity numbers.ref 13 Admittedly, this was a few years back, but I am not alone in my frustration with the downsides of tech innovation. The Solow Paradox is defined as the “discrepancy between measures of investment in information technology and measures of output at the national level.” Tyler Cowen, in an essay The Great Stagnation, argues we are on a plateau.ref 14 Michael Hanlon makes the case that innovation has stalled since 1970 by surveying what we still can’t do.ref 15 Hey! We finally got a Dick Tracy watch! With 1970 as the approximate cut-off, the question should be repeated: “WTF Happened in 1971?”

We wanted flying cars; we got 140 characters.

~ Peter Thiel, venture capitalist

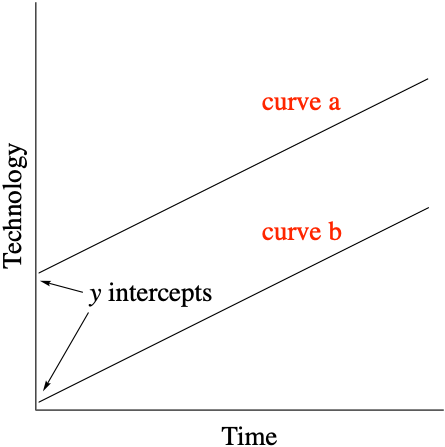

As a preamble to a discussion of transformational versus incremental wealth creation, let me resurrect a concept first presented to you in elementary school—the non-zero intercept. The utility of this construct came to me during an organic chemistry seminar in which somebody showed a fivefold influence on a cell wall property. It clicked: “That’s jack squat.” Fivefold to an organic chemist is <1.0 kcal/mol, the energetic cost of separating two water molecules from each other, and the dude was gonna build a fancy model around that? Now imagine a plot of the unitless and obtuse concept of technological change versus time (Figure 2). It would be noisy and should curve upward due to compounding, so let’s simplify it to a fault by linearizing everything. (I feel like an economist already.) The slope is the rate of technological change, and you want that puppy steep. Oh, yeah: Tesla baby! However, no advance is built on zero foundations. The non-zero intercept is the technology you creatively destroyed. The Gutenberg press was preceded by the quill. The quill would be a minuscule non-zero intercept best represented by curve b. The overall change represents unimaginable multiples off the original technology. Now imagine replacing manual typewriters with electric typewriters. That’s an incremental change—a BIG intercept, rendering the slope a rounding error (curve a at best). You may now have surmised that the seminar about cell walls had a non-trivial basal behavior without the additive—a large intercept—that left me underwhelmed. Biochemists, which I fondly refer to as “biowankers”, screw this pooch often, but we should still follow the science.

Figure 2. Technological change (slope) and creative destruction (y-intercept).

OK. I’m back. Not every invention is a Gutenberg press or electricity. New appliances riding on the backs of electrification—so-called “subsidiary” inventions—can be consequential. Most boomers probably have no idea that an enormous number of labor-saving devices became regular fixtures within the household just as their parents were creating the demon seed, you (pronounced “eewe”). Yay boomers! Now this will blow your circuits: Gordon says that the greatest decade for such subsidiary inventions was the 1930s—smack dab in the middle of the Great Depression. Bob argues that part of the Depression was labor getting pistol-whipped by capex (capital expenditures). Are we seeing a déjà vu as the Fed-funded digital world replaces people? Let’s ponder a few technological changes from the near and distant past to understand wealth creation. Ponder the slopes relative to the intercepts.

Ground transportation. We went from horse-drawn carriages to combustion-engine-powered vehicles, accruing hundreds of horse powers per vehicle in short order. Think cars, tractors, trucks, and bulldozers. In forty years, a horse had been replaced with a 1940s vintage Jaguar XK120 with a top end of 120 mph. Now I ask: 80 years later, what can you do with a Tesla that you couldn’t do with that vintage Jaguar XK120? Admittedly, a Tesla can do 250 mph on no road anywhere in the US. (Breedlove did 407 mph on the Bonneville Salt Flats in 1963.) A Tesla can go 300 miles on a single charge, but how far can it drive using the most efficient fuel source of them all, gas? I’m told Teslas are sooo cool to drive, but now I’ve gotta ask: Would you rather have sex, which is free or $20 on a bad day, or drive a Tesla? Thought so. I’m not done hammering Tesla by any means (see “Broken Markets”). How about replacing two horses with those 1912 hogs ridden by Mr. Harley and Mr. Davidson:

Communication. When the mail was replaced with telegraphs and eventually telephones, the time required to send a message across the country or around the world dropped from months to minutes and eventually to seconds. The Rothschilds had a fabulous currier system allowing them to trade assets on news from distant lands. “Quick. Sell those Waterloo munis.” The telegraph was a black swan that blew their business model out of the water. Now we have cell phones, which were brilliantly foreshadowed in 1960 by a must-see Arthur C. Clark videoref 16 and in 1926 by Tesla—the original Tesla:

When wireless is perfectly applied the whole earth will be a huge brain. We shall be able to communicate with one another instantly, irrespective of distance.

~ Nikola Tesla (@NickyT), 1926

Food Preservation. In prehistoric times, food preservation was via tribe members; you shared the kill. Drying meat to the point of inedibility and salting and pickling in clay crocks allowed for long-term storage. (The book Salt is a comprehensive treatise on the importance of salt to civilization that lives up to its sexy title.) Refrigerators, even as subsidiary inventions, were transformational for both shipping and storage. The next hundred years witnessed automatic ice makers. We recently put to pasture a 70-year-old Philco refrigerator that still worked. NDP was high the day they cranked out that beast. In 70 years, nobody will own a 70-year-old refrigerator that still works. Depreciation rates are very high.

Air Travel. The Wright brothers took us from commercially useless balloon-based flight (tiny intercept in Figure 2) to planes that were used militarily within a decade and crossing oceans within another. Orville Wright lived long enough to see jets in flight. Orville’s children witnessed jet-based commercial travel with the introduction of the Boeing 707 in the 1950s. Orville’s grandchildren now pay $50 bucks to get their bags looted of all valuables by TSA handlers. They do, however, get a free reach around at the security gate if their fake hip sets off the metal detector. (Hint to the old geezers with prosthetics: Identify as an old woman.) You can watch movies peering through your knees while you think about how nice a hot meal would be delivered by the stewardesses of yore.

Visual Arts. Photographs were the visual equivalents of the Gutenberg press and tape recorders the audio analogs. Movies and TV allowed you to see movements of tornadoes, elephants, and porn. (OK. That is the last porn allusion.) Decades later, you can watch anything you want on Netflix, but you can still only watch one show at a time. We had a rabbit-eared TV (in the cabin with the fridge) that got a single channel from Montreal. We were remarkably content, and those Club Super Sex commercials appearing after midnight were quite a treat. (That one doesn’t count.) Netflix is an incremental gain. I’ll give the internet serious transformational credit. It may be the Gutenberg Press 2.0 and is the source of Robert Gordon’s spike in wealth creation from 1995–2005. Google, despite its authoritarian leanings, is still seriously cool for looking up something in seconds that required weeks or months (if even possible) in the past. The subsidiary inventions are less inspired, just ask anybody who has wrestled with a website that is not Amazon’s.

True, social media is impressive. The internet gives us instant access to global knowledge. We are a more tolerant society, at least in theory. But Facebook is not the Hoover Dam, and Twitter is not the Panama Canal.

~ Victor Davis Hanson (@VDHanson), historian

Social Media. Facebook is unique. Given their business model of selling scraped data to corporate America, it seems to be a replacement for TV commercials and billboards. They may get me to buy a Saatva rather than a Tempurpedic mattress, but I am only buying one. To the extent they scrape data for nefarious reasons (as delineated in the books Surveillance Capitalism or Deleted), it is trivial to argue the modest intercept in Figure 2 is dwarfed by a steeply negative slope. Would society lose anything if Facebook disappeared? (Please take Mark with you.) And let us not forget the Solow Paradox.

Retail. OK, Professor Smarty Pants: what about Amazon? You can get anything from a single website in a day or two. Gordon reminds us that 100 years ago the Sears catalog let our great grandparents expand their purchasing beyond flour, beans, and nails from barrels in the general store to buying almost anything they wanted (including pre-fab houses). It took a few weeks, but, by comparison and over a century later, Amazon is incremental.

Highways. The movies give the Romans a bad rap. The Appian Way created by Roman engineers brought civilization to Europe (admittedly at the tips of Roman swords.) Lincoln initiated the Transcontinental Railway during the Civil War. Germany created the Autobahn, which inspired Eisenhower to create our interstate highway systems. These were government programs that created huge wealth. The last half of the 20th century witnessed the Big Dig, the Bridge to Nowhere, California’s unfinished rail systems, and interstate highways in Hawaii.

Plumbing. Running water via plumbing was developed millennia ago, but routine indoor plumbing in the early 20th century allowed homemakers to stop hauling 50–100 gallons of water a day in and out of the house. Throw in wiring and a phone, you have a modern household albeit 100 years ago.

Government. Herbert Hoover introduced the National Bureau of Standards (NBS), which allowed huge progress through interchangeable parts and mass production. (Hoover was a great president with a bad rep.) The boomer generation, by contrast, created the National Security Agency (NSA), which ushered in 50,000 bullshit TSA jobs in the US alone. Wouldn’t you like to get some of your civil liberties back?

Healthcare. Penicillin and its offspring introduced in the 1930s saved millions of lives. Most modern medicines are welcome additions but are more about maintenance than cure. (NB-Give a damned Nobel prize to the guy who invented Imodium in the 1960s.) Even cancer survival rates are rising slowly: you can see the non-zero intercepts.ref 17

Food Preparation. Gas and electric ranges at the turn of the century were big improvements over wood stoves and the hearth. Microwave ovens are incremental: you can make popcorn on a stovetop. Interesting factoid: possible kitchen applications of microwaves were discovered when some guy melted the chocolate bar in his pocket while whipping up a couple of Rocky Mountain oysters in his shorts.

Banking. The FDIC banking insurance in the 1930s represents the high-water mark for modern banking. You will have trouble convincing me that the bloated multinational banks of the present are anything but a monumental downward slide to the Gates of Hell. Banks used to be about matching lenders and borrowers—savings and loans—but are now systemically risky bucket shops with customers as prey. We’ll return to them in a bit.

Role of Energy. Maybe the perennial optimists will be right again, but those expecting that the 21st century’s growth will match or top that of the 20th century may be disappointed. Economists have noted that the ebbs and flows of modern economies correlate with energy consumption.ref 18 It is easy to see how tapping new and better energy sources have created profound changes through the millennia. Fire brought us out of the caves. Charcoal ushered in the Bronze and Iron age. In the ancient civilized world, the west was still on the cellulose standard while the Chinese were pumping natural gas out of the ground using bamboo pipes to boil seawater to get salt. The Highlanders started burning peat laced with dead Druid priests. The industrial revolution rode the back of the whaling industry for light—coal, and eventually oil…black gold…Texas tea. (Leviathan is a great treatise on the history of whaling on the growth of New England.) Each stage was powered by a better, more efficient fuel than its predecessor.

If stupid hippies hadn’t killed nuclear power, we’d have nuclear power plants, safer and cheaper than coal-fired plants, all over, and electric cars really would be zero emissions.

~ Penn Jillette, comedian

I once had dinner with Penn Jillette. Of course, the next push forward will be based on nuclear energy. Oh, but nooooo! We can’t do that! Although deaths in the US nuclear power industry are almost undetectable,ref 19 we are told, “one life is too many.” Forget about the death toll on Friday nights in the bars near the Texas oil fields. No siree, we are doing it with solar, wind, geothermal, and biomass, all displaying energy densities that are no match for a barrel of Saudi crude let alone a single nuclear reactor. Hey: maybe you could recycle that cooking oil from McDonalds to charge your Tesla. Alternative energies are unevenly generated, and they are also destabilizing to power grids when imported beyond a critical, and rather low, threshold.ref 20 Meanwhile, I’m told that second-generation nukes are so efficient as to leave essentially no toxic waste. We should rethink our aversion to nukes and do so fast.

The notion of wealth creation is foundational to the section on “Broken Markets.” Are the new era silicon-based industrial Goliaths really capable of creating wealth akin to their carbon-based predecessors? One last truly random and haunting thought: Civilization is, by definition, sandwiched between two ice ages. If nature ever shook the Etch-A-Sketch and zeroed out civilization, the post-apocalypse survivors would never regenerate modern society because they wouldn’t have the fossil fuels. We had one shot at building a sustainable industrial civilization. Let’s not blow it.

Valuations

[Investors] do not care about the movements in the price of the stock. Since their interest lies not in the sale of the stock but in the revenues secured through the dividends; the higher value of the shares forms only an imaginary enjoyment for them, arising from the reflection…that they could in truth obtain a high price if they were to sell their shares.

~ Joseph de la Vega, 17th-century businessman

The price you pay determines your rate of return.

~ Warren Buffett

Buffett noted in an iconic 1999 Fortune article that dropping interest rates are bullish.ref 1 The equity run starting in 1981 overlays perfectly with a four-decade bull market in bonds in which dropping rates were accompanied by greater profits and rising valuations. In a 60:40 portfolio, the rising price of bonds in the denominator drives the numerator and shifts enthusiastic investors to raise the percentage of equity exposure. (See Cash on the Sidelines.)ref 2 Treasuries are so overpriced now as to yield <2% nominal return per annum for thirty years. The only decision for a bond investor is how long you wish to get no yield. Jacking up the denominator of the 60:40 portfolio is nearing an end and the return from that denominator is a disastrous inflation-adjusted negative yield. The Fed, by contrast, starting with Alan Greenspan, missed that dropping part of Buffett’s thesis, often suggesting that low rates justify high equity valuations. This is called the ”Fed Model” and is tantamount to saying that the largest bond bubble in history justifies the largest equity bubble in history. Great model guys. I expect nothing less.

To say that low interest rates justify high valuations in stocks is also to say low interest rates justify low future returns in stocks. If one wishes to protect overvalued prices, one also has to accept meager long-term returns.

~ John Hussman (@hussmanjp), Hussman Funds

Historical Valuations. In 2018 I hit the valuation story as hard as I could, laying out 20 metrics all suggesting that the S&P 500 was at least twofold over historical valuations.ref 3 Figures 1–4 are just a few updates and new views. The Buffett Model—the S&P’s price-to-GDP ratio—is popular owing to its namesake. Figure 1 shows the stats of a market that is clearly muffin topping. Figure 2 is the more broadly-based Wilshire 5000 analog of the Buffett Indicator. You can see in all of them that the markets at the ’09 low were not deeply undervalued just because they had hurdled Earthward so dramatically, and the markets spent about a month below historical fair value. Pure greed kept my buying in check. There had to be more to go, but the Fed had other plans.

Figure 1. “Are markets priced for Destruction?” —Bloomberg

Figure 2. Wilshire 5000 versus GDP c/o Stephanie Pomboy of Market Mavens.

Figure 3. Market valuation versus GDP measured in trillions of dollars of market cap c/o Stephanie Pomboy of Market Mavens.

Valuation, I find, is a useless tool. If you base your investment decisions on valuation, you are never going to make money.

~ Mark Schmehl, Fidelity

Traders warn not to trade off valuations as a timing vehicle. As the risk soars new-era momentum traders are confident they can dine on Fibonacos and dips and be John Elway (leave at the top). They may skedaddle out the keyhole just in time, but somebody must own those assets all the way to the next secular bottom. Do ya feel lucky? Investors, by contrast, warn that price matters: the more you pay for a given asset the lower your returns. If you buy a Toyota Camry—a good, solid car—for $100,000 you’ll get hurt at the trade-in. The best investments are good assets in which low prices have wrung out the risk.ref 4 The great risk is scooping up assets of dubious quality when the party is raging. Investors should take note that Buffett has been paring his equity exposure including airlines, half of his Wells Fargo, all of his Goldman shares, and $5 billion of Apple, apparently turning Berkshire into a social conscience fund.ref 5

Figure 4. If we are more efficient technologically, why do we work so hard to buy the S&P?

Figures 1–4 show the markets have been above historical valuations since the mid-90s. To reiterate: there are many more.ref 2 One group of enterprising analysts treat rising valuations as a trendline and correct for it.ref 6 How novel. This is a long time to be above any mean. Must be a new paradigm. Maybe this is the demographics of the boomers pushing the markets up the Wall of Worry propelled by a Wall of Liquidity. I see the liquidity but not the worry. Years ago, Kudlow suggested social security should be put in the markets. That would have driven valuations up even higher, but Larry seemed to miss the niggling detail that it would not in any way create wealth or even generate GDP, only slice the pie into more pieces. Sounds fair to those who have no pie, but the collective gain would be zero. Ominously as the boomers liquidate their assets there is sparse evidence that the next generation will have the resources to put a bid under anything. We could witness 25 years of downward pressure provided Covid-19 doesn’t compress that timescale the hard way.

I understand people who bet on moral hazard. I understand people who bet on the Fed backstop. I don’t do it. I don’t think that’s a good way to invest…This notion that it doesn’t matter what happens to fundamentals…It doesn’t matter what happens to corporate earnings… It doesn’t matter what happens to economic growth… because The Fed will buy what I want to buy… that’s the mindset of the market right now….Why has the fed continuously conditioned markets to expect them to step in and repress any volatility? Isn’t it time to stop doing that because you end up not only undermining the system itself but you undermine the credibility of an institution that is critical to the well-being of this and future generations?

~ Mohamed El-Erian (@elerianm), former manager of Pimco

Current Valuations. OK. I documented the lofty valuations in 2018 but what about now? Equities have risen a smart 35% in the intervening two years. Even if we took a pass on the Covid-19 disaster, which I believe has exacted serious long-term damage, Buffett’s GDP denominator would have grown 5-6% at best. Let’s look at some granular details:

- Growth stocks are considered bottom-decile cheap when they are priced at six times sales and top-decile expensive at fifteen times sales. They were 23 times sales as of September without factoring in contributions from the Covid-19 recession.ref 7 A 75% price correction, provided it does no economic damage, will make them cheap again.

- In 2019 over 1500 CEOs took their booty and exited to “spend more time with their families.”ref 8 In January 2020, another 219 decided to cash in their chips. Insider selling was running high. What did they know?

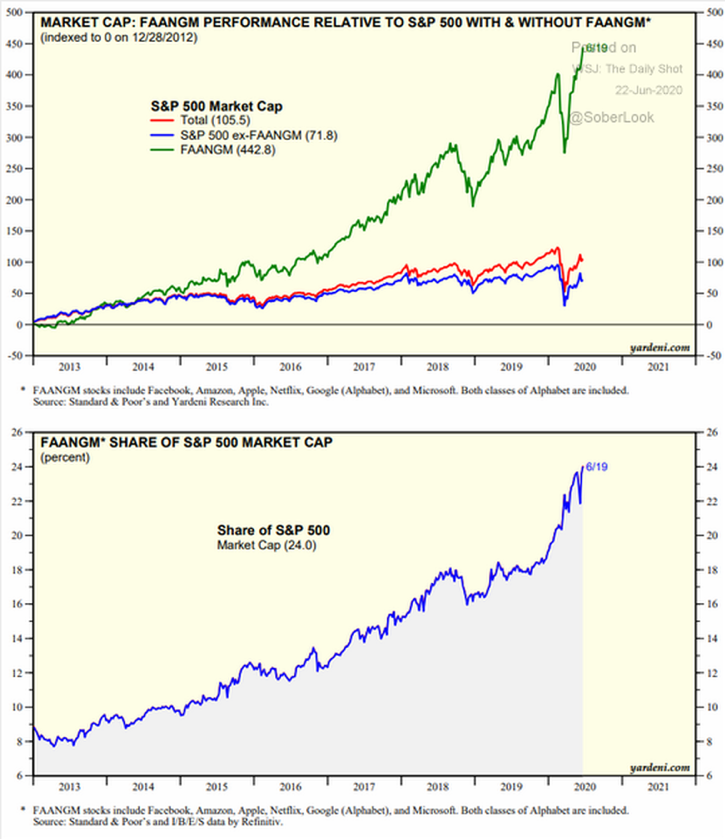

- The FAANGs have ridiculous valuations. These market Sherpas—Facebook, APPL, AMZN, NFLX, GOOG, with MSFT thrown in—have a combined market cap of >$8 trillion. They are the market. The S&P 500 is now the S&P 5. We’ll bang this drum hard in “Broken Markets.” I’m partial to using just MSFT, Apple, Google, and Amazon (MAGA).

- More companies are trading at over ten-times revenues than during the dot-com mania.ref 9

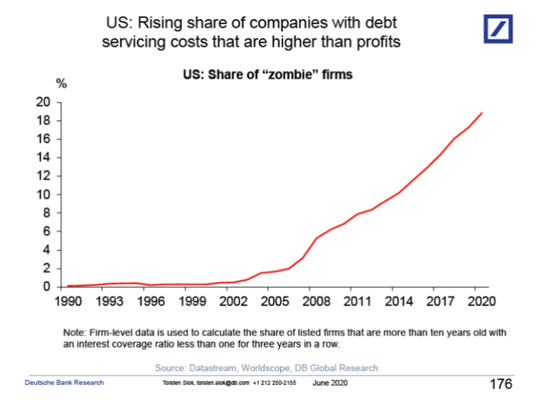

- Forty percent of publicly traded companies have negative net worths.ref 10 The percentage of zombie companies in the S&P—companies that are at least 10 years old and unable to pay interest on their debt without taking on more debt—is 14–18% depending on who you ask.ref 11 If your cash flow can’t cover the interest payments with rates at 5,000-year lows—I am not exaggerating—you are totally screwed. (I am exaggerating on that either.) In 1990, with interest rates near 10%, only 2% of the S&P were zombies.ref 10

- David Stockman notes the market’s “price-to-earnings ratio ranges between 52.1 times the earnings CEOs and CFOs certify on penalty of jail time ($65 per share) or 27 times the Wall Street brush-stroked and curated version ($125 per share), from which all asset write-offs, restructuring charges, and other one-timers/mistakes have been finessed out.”ref 13 (Notice how David specifies the importance of earnings that aren’t completely fabricated.)

The stock market has returned more than 125% since the 2007 peak, which is roughly 3x the growth in corporate sales and 5x more than GDP.

~ Lance Roberts (@LanceRoberts), chief Strategist RIA Advisors

From the legendary Jeremy Grantham…ref 12

This will end badly….I have been completely amazed. It is a rally without precedent…the only one in the history books that takes place against a background of undeniable economic problems…the market and the economy have never been more disconnected…the current P/E on the U.S. market is in the top 10% of its history… the U.S. economy, in contrast, is in its worst 10%, perhaps even the worst 1%…. This is apparently one of the most impressive mismatches in history…after a 10-year economic recovery, this would have been a perfectly normal time historically for a setback….And then the virus hit…bankruptcies have already started and by year-end thousands of them will arrive into a peak of already existing corporate debt…the history books are going to be very unkind to the bulls.

Realistic Expectations? What’s a reasonable guesstimate for investment returns over the long term? A gander at historical returns without accounting for valuation changes reveals that Wall Street hasn’t been completely truthful with us. The average nominal (non-inflation-adjusted) return for US stocks is about 5.5% annualized for 120 years and >6% in the post-war period.ref 14 Typical retirement plans assume a 7.5% nominal return. Polls show investors expect an outlandish 15% return on their equities over the next five years,ref 15 suggesting profound recency bias from the total return of 17% annualized ‘roid rage off the ’09 lows. They seem unaware that the last decade’s returns are trough-to-peak, a ridiculous one at that. Suze Orman spouts off about a Gen Z-ers putting $100 bucks a month into a Roth IRA and retiring as millionaires. Such a real return would require >11% return per annum—year after year—for 40 years.ref 16

Lowered Expectations. Earnings for a reconstructed inflation-adjusted S&P from 1870 to the present using Shiller’s numbers show a 15-fold gain (about 2.0% annualized). Funny how that is the same as the growth in the GDP over that same period. Go figure. Let’s tease out a few gems from Buffett’s iconic 1999 analysis, shall we?

Let’s say that GDP gets 3% real growth, which is pretty darn good…If you think the American public is going to make 12% a year in stocks, I think you have to say, for example, “Well, that’s because I expect GDP to grow at 10% a year, dividends to add two percentage points to returns, and interest rates to stay at a constant level.”…The absolute most that the owners of a business, in aggregate, can get out of it in the end—between now and Judgment Day—is what that business earns over time…[There are] frictional costs…the market maker’s spread, and commissions, and sales loads, and 12b-1 fees, and management fees, and custodial fees, and wrap fees, and even subscriptions to financial publications…investors are dissipating almost a third of everything that the FORTUNE 500 is earning for them …If I had to pick the most probable return, from appreciation and dividends combined, that investors in aggregate—repeat, aggregate—would earn in a world of constant interest rates, 2% inflation, and those ever hurtful frictional costs, it would be 6%. If you strip out the inflation component from this nominal return (which you would need to do however inflation fluctuates), that’s 4% in real terms. And if 4% is wrong, I believe that the percentage is just as likely to be less as more.

~ Warren Buffett, 1999 Fortune articleref 1

Thus, the Orifice of Omaha says 4% real return is it. Rob Arnot puts it at 3.1%.ref 17 Neither analysis appears to include taxes on the dividends and on nominal capital gains. (The authorities love inflation because they get to tax it.)

The Buffett Indicator…now yields a forecast of an average annual loss of nearly 8%, including dividends, over the coming decade.

~ Jesse Felder (@jessefelder), former hedge fund manager and author of the Felder Report

Expectations from Current Valuations. OK, Bub. We are way overvalued. I get it, but how do we get out of this metastable mess without having to put our affairs in order? It seems unavoidable that the mean regression will live up to its name. It will occur on no set timescale, but it is a gravitational pull—a force of nature. (Middle school arithmetic reminds us that you have to go through and spend time below the mean, but that is too ugly to ponder.)

We’re in the craziest monetary and fiscal mix in history. It’s so explosive, it defies imagination.

~ Paul Tudor Jones (@ptj_official), January 2020

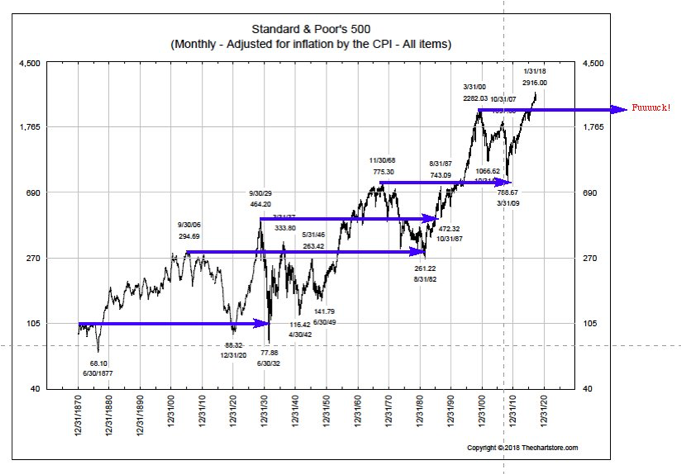

Two years ago I created a graphic showing how long it takes markets to regain their secular highs for the last (not first) time (Figure 5). Those arrows are 40–75 years long. From the old Bill Cosby comedy skit with God talking to Noah resisting building the ark: “Noah. How long can you tread water?”

Figure 5. I made this in 2018 and will keep posting it. (Background plot by Ron Greiss.) That longest blue arrow (1906–1981) is 75 years long. Howbowdah?

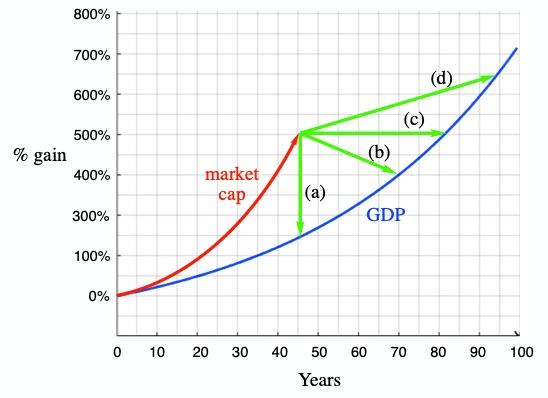

Regression to the Mean. I’ve tried to conceptualize a model for overvaluation and the unavoidable return to normal in Figure 6. Don’t get hung up on the units; it’s a spherical cow. The 2.0% real GDP growth compounded over the 20th centuryref 18 is approximated by the noiseless blue curve (y = 1.02x where x = 0–100 years). The red curve is the market tracking the GDP Buffett style but then departing into a mania—2x overvalued—by year 45. The math is identical for any metric of valuation. The choices for regression to the mean are illustrated with green arrows.

Figure 6. 2% growth in GDP (blue). Equity multiple expansion to 2x-overvalued occurs by year 45 (red). Regression to the mean (green) occurs by four paths: (a) crash (0 years, 50% correction); (b) secular bear (25 years, 16% correction); (c) treading water (35 years; 0% correction); (d) slow appreciation (50 years; 25% total gain).

- A market crash approximated by the vertical red arrow is optimal for a cash-rich bear looking for an entry point. That would be me. It would also turn the highly leveraged financial system into pink mist.

- Alternatively, curve c shows the markets treading water—moving horizontally—until they intersect with the GDP curve, which is monotonically growing at an uninterrupted 2% annualized rate. Investors will be treading water with zero real capital gains for 35 years, which is a rounding error the same as for your treasury portfolio. There are, however, dividends, but they are offset by taxes and fees.

- More realistically, markets will serve up a price–time combo platter and slowly drift lower while the GDP slowly grinds higher. Curve b, for example, shows a net 16% loss spread over 25 years. The inflation-adjusted 66% loss in S&P from 1967–81 was spread over the 14 years (see Figure 5).

- The Fed seems determined to follow the last path (curve d) in which the real capital gains angle upwards for eons. The boomers will have long-since gone to the light waiting 50 years for the regression to mean valuations accompanied by a 25% total gain (0.5% annualized). The Fed is charting this course by artificially and rather explicitly supporting asset prices. Unfortunately, they will fail because they actually suck at their jobs. This strategy in reality is simply generating loftier levels of overvaluation through a series of bubbles that become progressively more shock-sensitive and dangerous. It feels like the Fed is in the final stages of Tetris.

You can replace lost capital – but you can’t replace lost time.

~ Lance Roberts, batting 500