The Fed Has Enabled The Biggest Perpetual Frat Party Of All Time

Authored by Sven Henrich via NorthmanTrader.com,

I trust nobody was surprised by the big market rally last week. After all we’re all joyful attendees of a big frat party, indeed one could argue the biggest perpetual frat party of all time where the hosts are offering an infinite free supply of booze, coke and hookers. And fear not, once the party goers tire just a little, the supply will be once again upped to keep the party going.

The February correction advertised already what was coming: Intervention to calm fear of rising yields as I highlighted on March 2. As tech sold off even harder during the first week of March the technicals also flashed buy the dip, the reasons I highlighted publicly on March 5:

Quick market update: pic.twitter.com/RBJTiIwzkM

— Sven Henrich (@NorthmanTrader) March 5, 2021

And naturally this week the forces of intervention appeased in full force:

This week in markets:

1. Fed extends PPP liquidity facility

2. Congress passes $1.9 trillion stimulus package

3. ECB accelerates bond buying

4. Nothing else mattered pic.twitter.com/RyKqVSYv9X— Sven Henrich (@NorthmanTrader) March 12, 2021

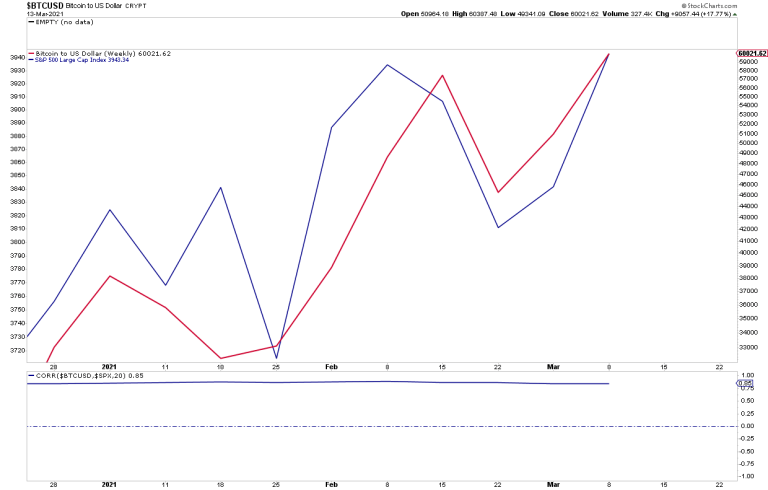

The result: New all time highs in key indices such as $DJIA, $SPX and $RUT with other asset classes such as Bitcoin joined at the hip:

Yes, Bitcoin is much more volatile than the broader market but in terms of directional up and down flow it is showing a high correlation in 2021 in particular.

The global liquidity frat party has crept into asset classes far and wide. Bitcoin is an expression of this as capital is trying to find superior return with all kinds of justifying narratives.

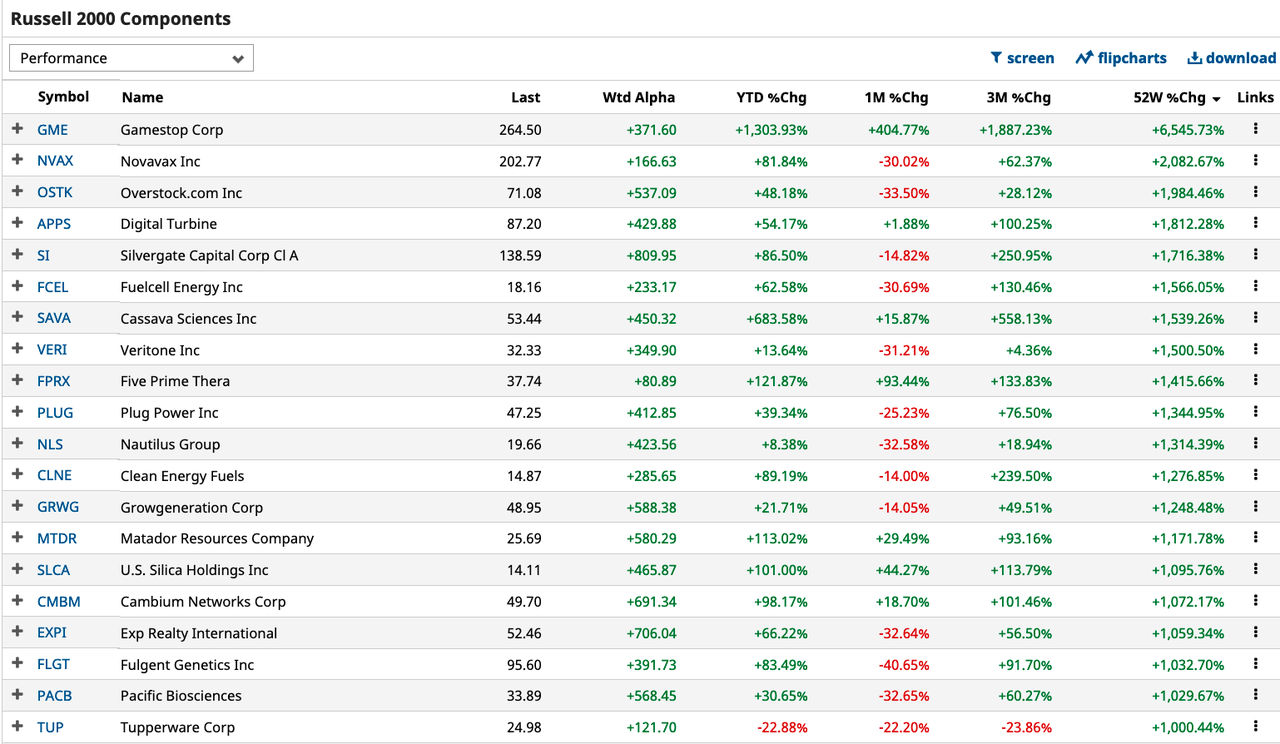

Bitcoin is up over 1,000% over the past year. Many claim it is an expression of a store of value in the face of relentless central bank intervention and fiat currency printing. But if superior returns is self validating evidence of such a store of value argument the same could be said and more so about a number of small cap stocks that have seen 1000% returns in the past year, some even with much higher returns to show for:

While I’ll leave the Bitcoin discussion for another future article I for now submit that the argument can be made it’s all part of the same trade: Historic free liquidity pumped into the frat party.

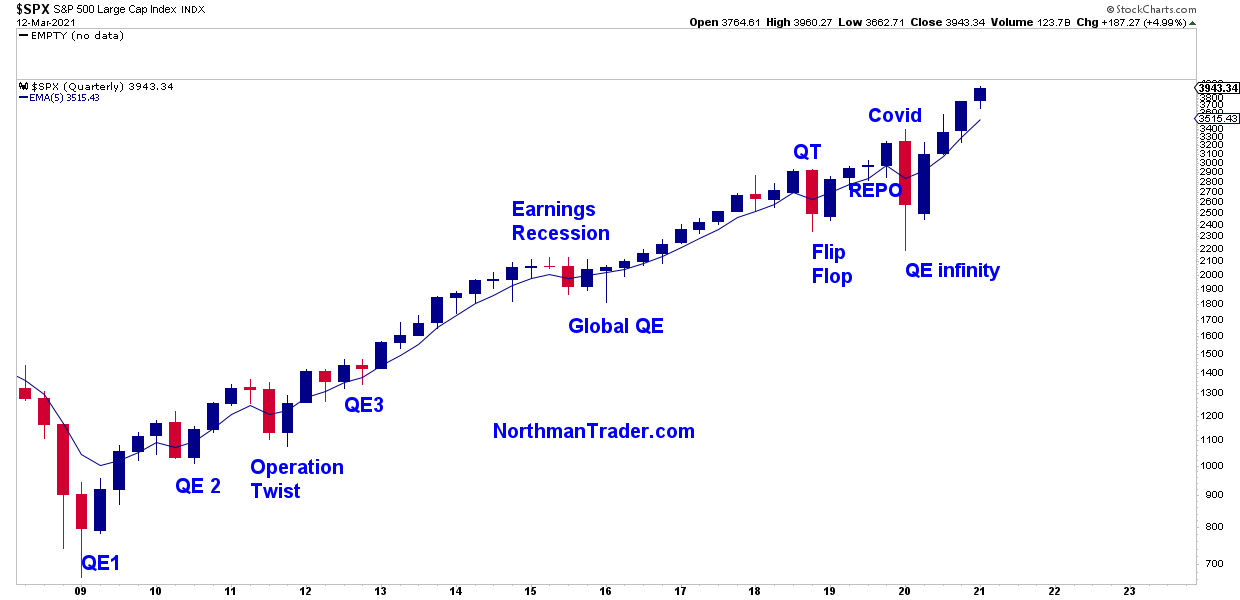

This frat party has been ongoing since 2009 and interventions have been predominant on any sign of trouble as expressed with downside in markets. See any quarterly red candle in markets and the frat party supply begins anew:

But note the party requires ever more supply to keep it going.

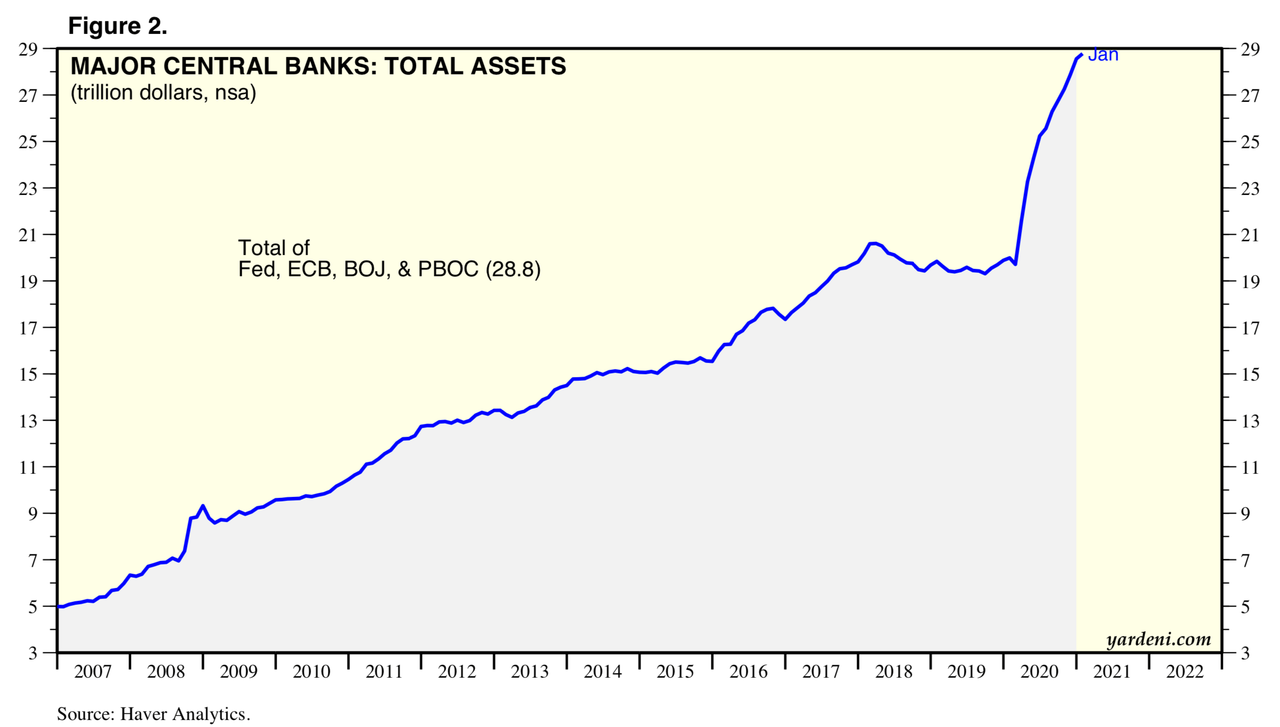

The obvious form of course being central bank interventions the likes we have never seen before:

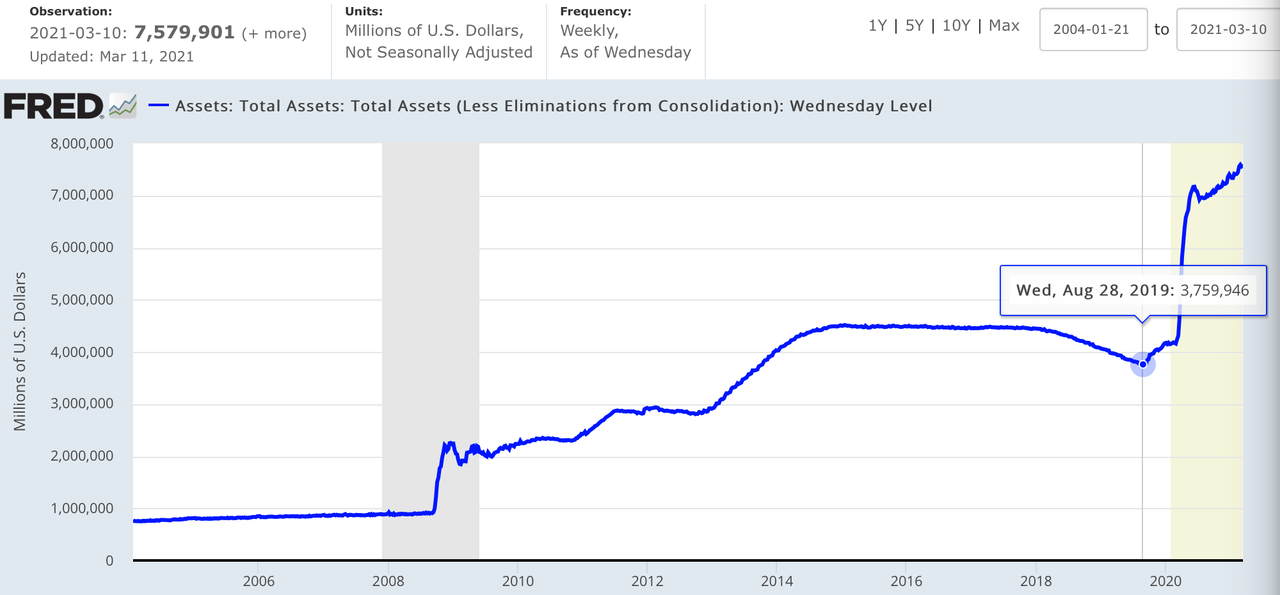

A cumulative party injection of $24 trillion since 2007 by just 4 central banks with nearly $10 trillion in the past year alone.

Indeed the Fed has now doubled its balance sheet since the temporary and rather marginal effort to reduce it came to a sudden end 19 months ago:

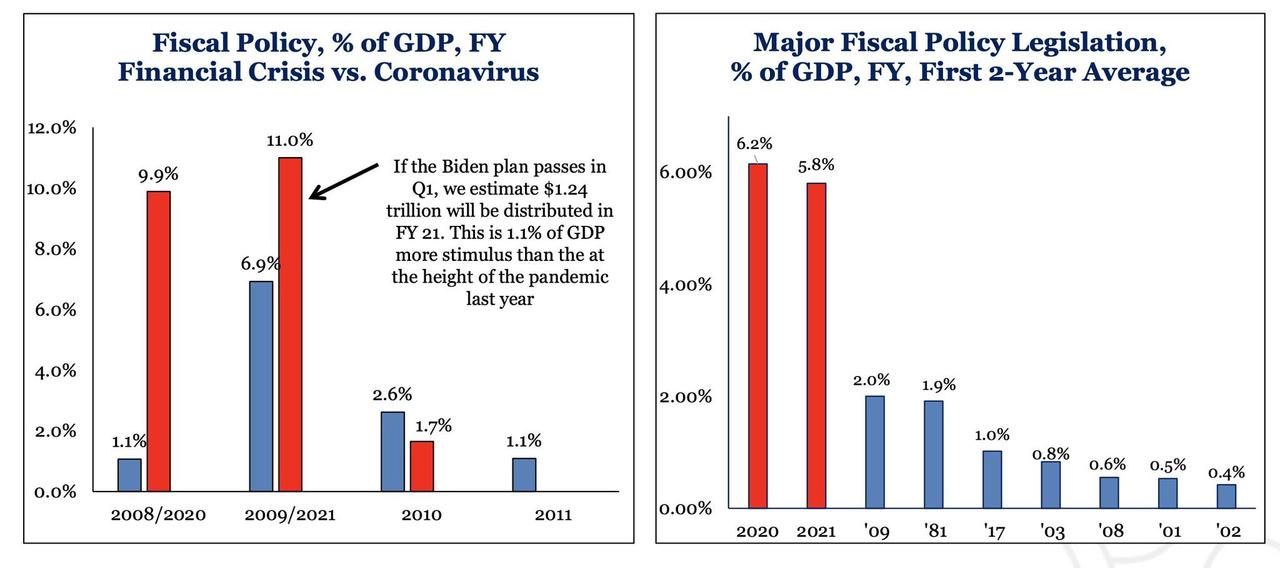

And now of course we see the fiscal side joining going on a spending spree that dwarfs even the one of the great financial crisis:

This latest, third installment of stimulus money not even really pretending to be targeted. Free money for all even those that don’t really need it. Even people that never lost their jobs or loss in income get stimulus checks not only for themselves but for their children as well at a time when household wealth has never been higher.

And record household wealth is no surprise as equity valuations are higher than ever seemingly heading toward 3 deviations above the historic mean:

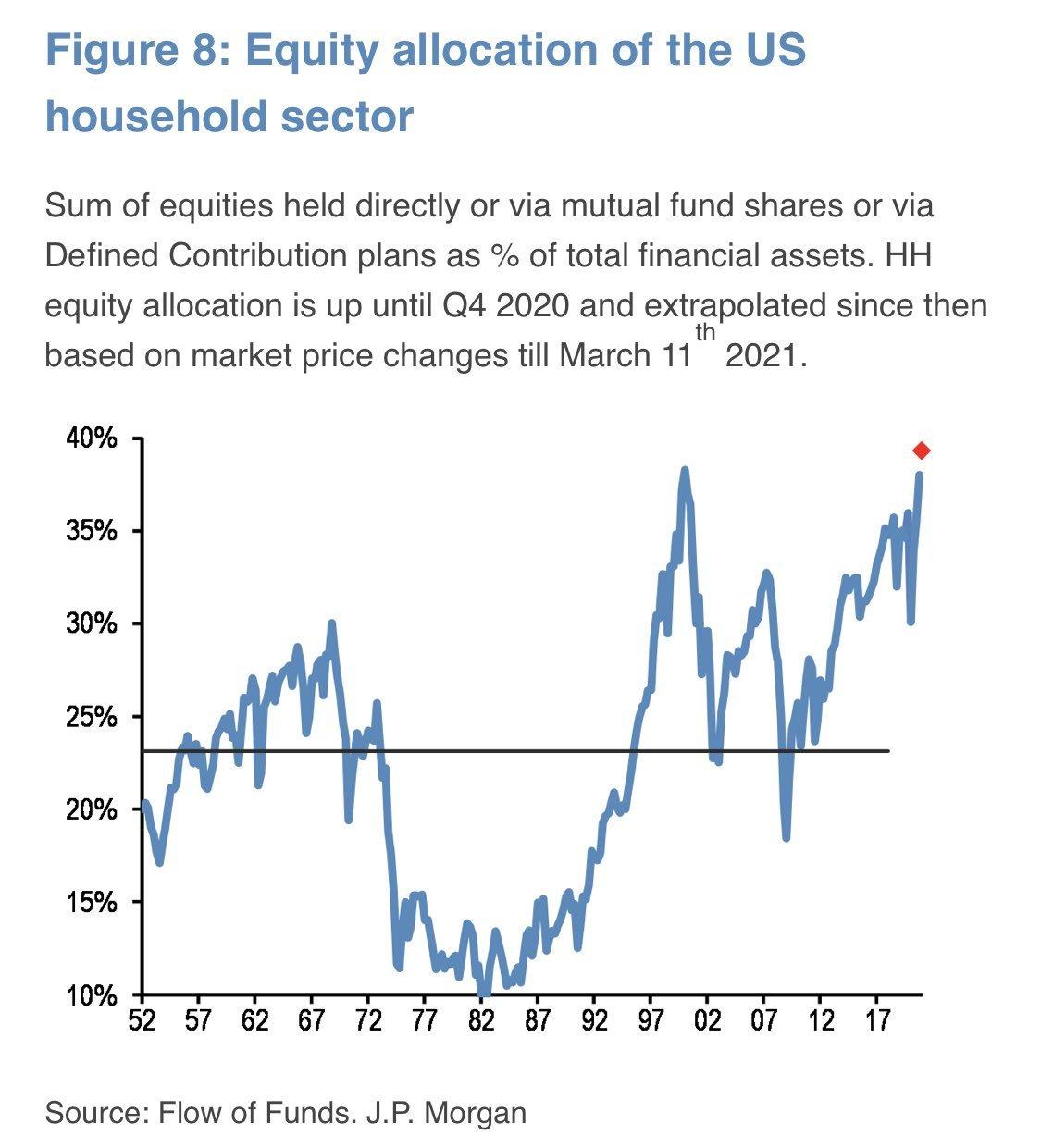

With equity allocations approaching the year 2000 peak:

Yes even stock holders who benefitted from rising asset prices get stimulus checks too. What a cool frat party. Expending wealth inequality is now a group effort for don’t kid yourself: $1,400 stimulus checks are just that for a single person, but the cumulative effect will once again benefit disproportionately those who own the asset classes.

GDP estimates for 2021 keep being raised as we are witnessing the biggest recovery free money can buy. Yet not even the largest GDP growth figures in 55 years will stop central bankers from injecting more liquidity. They know they can’t stop, they can’t even hint at stopping. Hence Christine Lagarde felt compelled to accelerate ECB bond purchases this week in response to rising yields, which she called a threat to the economic recovery.

Irony is dead:

We injected so much liquidity causing yields to rise faster than we expected which threatens the viability of our risk free rate valuation balloon hence our best course of action is to add even more liquidity at a faster pace.

We are from the @ECB & we are here to help.

— Sven Henrich (@NorthmanTrader) March 12, 2021

Yes, the bond market is sending a signal of rebellion raising the prospect that the long presumed dead consequences of all these interventions could be making their presence felt. It’s been said that too much of a good thing can be a bad thing. I submit there has been no scientific process by which central bankers and politicians globally have decided what the right amount of liquidity is to support the recovery. Rather I submit it’s been and continues to be way too much and it’s distorting everything and a sudden velocity driven bond market in the form of accelerated rising yields is indeed a clear and present danger to the enormous debt and valuation construct that has been unfolding:

For the free money party was based on one key premise: Low rates which justified the notions of TINA (there is no alternative) and the ability to finance all the new debt consequence free.

So yes, the pressure to intervene continues and the Fed is on the hook this coming week. The latest interventions this week enough for markets to ignore the latest spike to new highs in yields for now. Yet the bond beast remains angry and demands appeasing.

And so the Fed and other central banks are boxed in the trap of their own making. Markets are approaching this week with not only the highest valuations and equity allocations in history but also with dramatic chart extensions the extent of which we have never seen before in some cases, small caps being one such example:

Yes, 1,000%-6,500% share appreciations bring about consequences in index charts. With small cap index prices sitting a record 15% above their quarterly Bollinger band and a 10MA quarterly oscillator sitting at an all time high disconnect of nearly 40% there simply is zero room for error.

Especially in context with tech sending a historic warning sign:

Interesting times. pic.twitter.com/VVj4T9wbnP

— Sven Henrich (@NorthmanTrader) March 6, 2021

For the past 12 years central banks have intervened at any sign of market trouble, now the market demands feeding even at all time highs for the state of market faith in central bank intervention is so absolute it expects not only a constant supply of its drugs, but now expects new interventions in the form of yield control to continue to propel it to further highs.

The problem with all this should be self apparent: We are rapidly approaching the point of peak liquidity. We are unlikely to see such a forceful combination of both monetary and fiscal stimulus again. On the political front the ability to push a 4th stimulus package through is running against a key reality clock: The next Congressional election in less than 2 years. It may give Democrats enough time to push through a new stimulus package and/or infrastructure plan but given the composition of its own caucus the party may find the next package much harder to push through compared to this week’s stimulus package, especially since the deficit this year is now on pace for a record $4 trillion following last year $3.1 trillion during Republican control. That’s $7.1 trillion in new debt in 2 years in case if anyone’s counting.

Central banks, while still on a constant printing and low rates train will increasingly find themselves confronted with an obvious dichotomy: Why are you still printing with 5-7% GDP growth while the economy is increasingly overheating? You asked for fiscal stimulus now you have it. You asked for inflation. It’s coming in a big way and the bond market is telling you so. The larger message: After 12 years of non stop boozing and partying a major headache is coming.

And one of these headaches will come in the form of comps that can’t be repeated. Following the sugar high growth figures of 2021/2022 the economy will once again slow, earnings growth figures will once again slow. And this is the time central bankers will want to finally raise rates? When the economies are slowing? When higher yields brought about the very inflation they sought to bring about in the first place make the sustainability of historic debt loads highly questionable.

The eventual solution: More booze, coke, and hookers of course. Because the party must go on for there is zero evidence, none, zilch, that markets and the economy can maintain any sort of positive trajectory on their own, without intervention.

And with the latest combination of both fiscal and monastery intervention the ability to reduce intervention is becoming ever more diminished. With 3 stimulus checks under their belt in just 12 months we now have a larger population that is quickly becoming accustomed to free government money handouts. Socialism happens fast. Policy makers may find that expectations are easier set than ended.

This coming week then will come at an interesting time: Can new highs be sustained with the help of an again accommodative Fed, or will these new highs fail, perhaps driven by a disappointed bond market sending yields even higher setting up for a potential double top in the most one way oriented market in sentiment, valuation technical disconnects and equity allocations in history?

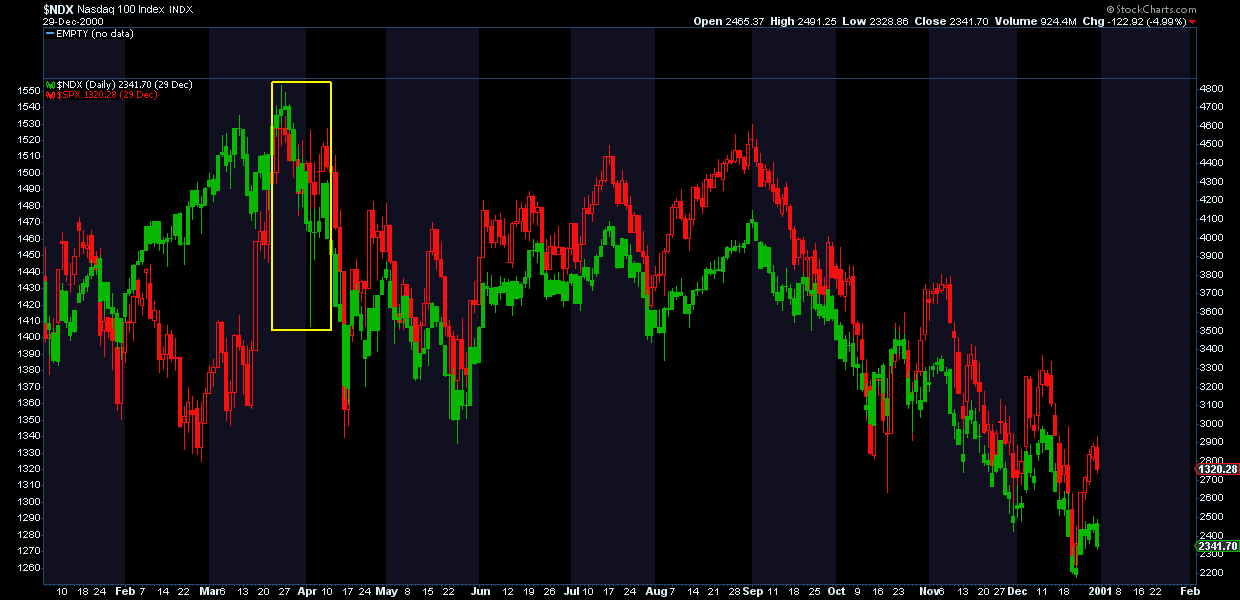

Lest not forget that the last time we saw tech suddenly correcting and seeing a weaker bounce for lower highs was precisely during that infamous March 21 years ago:

Back then when tech failed to make new highs the bubble had burst, only for it to take participants months to realize it as the ensuing market chop continued into September of that year. And as in 2000 it may take months after the fact to realize the bubble has burst.

Tune in for Jay Powell’s press conference on Wednesday for a hint at whether the party continues or whether it’s time for a major hangover.

Tyler Durden

Sun, 03/14/2021 – 13:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com