Fed Starts To Wind-Down Secondary Corporate Credit Bailout Fund

The Fed’s first-ever foray into directly bailing out the corporate bond market will apparently come to a final close in the next few months (they hope).

The vehicle, known as the Secondary Market Corporate Credit Facility, or SMCCF, holds about $13.7 billion in already-outstanding corporate bonds.

The SMCCF ceased operations on December 31, 2020.

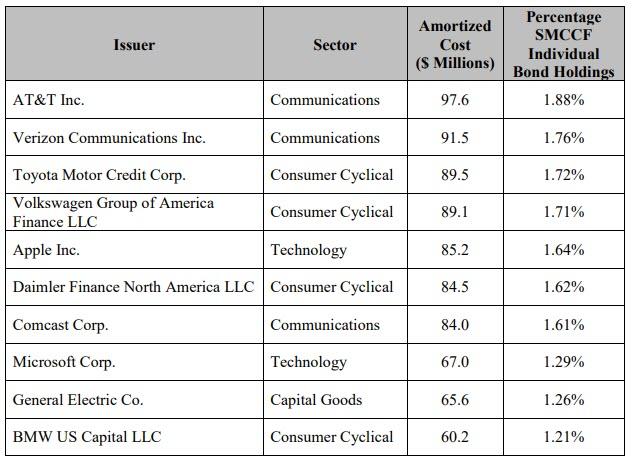

$5.21 billion of bonds from individual companies including Whirlpool, Walmart, and Visa (as of April 30, 2021, 45 bonds matured, 112 had been redeemed early, and 1,204 bonds remain outstanding in the SMCCF).

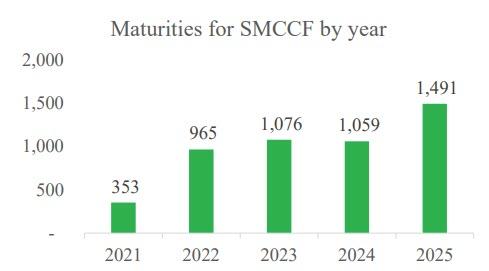

Approximately half of the bonds in the SMCCF will mature by the end of 2023. As seen in the chart below, while most bonds will mature in 2025, bond maturities are spread out fairly evenly among the five years that bonds are due.

In addition, it held $8.56 billion of exchange-traded funds that hold corporate debt, such as the Vanguard Short-Term Corporate Bond ETF.

Across the ETFs and individual bonds, AT&T, Verizon, and Toyota had the biggest positions…

The NY Times reports that a Fed official said the central bank expects to complete by the end of the year.

The Federal Reserve Board on Wednesday announced plans to begin winding down the portfolio of the Secondary Market Corporate Credit Facility (SMCCF), a temporary emergency lending facility that closed on December 31st, 2020. The SMCCF proved vital in restoring market functioning last year, supporting the availability of credit for large employers, and bolstering employment through the COVID-19 pandemic.

SMCCF portfolio sales will be gradual and orderly, and will aim to minimize the potential for any adverse impact on market functioning by taking into account daily liquidity and trading conditions for exchange traded funds and corporate bonds. The Federal Reserve Bank of New York, which manages the operations of the SMCCF, will announce additional details soon and before sales begin.

The SMCCF was established with the approval of the Treasury Secretary and equity provided by the Treasury Department under the CARES Act.

We have one simple question – what happens when they start to sell and spreads blow out amid zero liquidity?

The Fed’s decision comes as speculation grows over when The Fed will start thinking about thinking about tapering its massive bond-buying bonanza of liquidity?

Why don’t you wind down ZIRP and QE which were “temporary emergency” policies from 13 years ago?

— EndTheFed.org (@EndTheFed_org) June 2, 2021

For now, there is no real reaction in bond ETFs…

Tyler Durden

Wed, 06/02/2021 – 16:52![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com