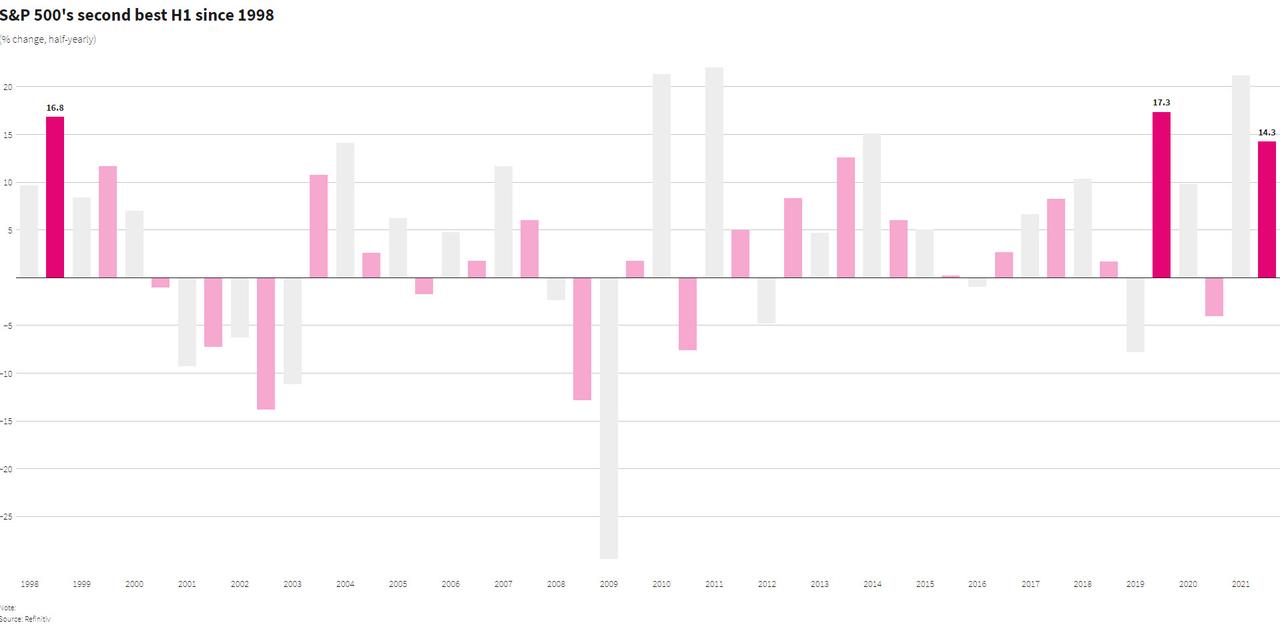

Shaky Futures Close Out Second Best First Half Since 1998

US stock index futures treaded water after rebounding from session lows on the last day of the quarter, one day after the S&P 500 and the Nasdaq closed at record levels, as rising renewed lockdown risks from the delta coronavirus strain overshadowed confidence in the global economic recovery. The S&P 500 has climbed about 14.3% in the first half of the year and is set for its second best first-half performance since 1998…

… with energy, financials, real estate and communication services stocks notching the best performance at the sectoral level. The S&P growth index which houses mega-cap FAAMG names has jumped nearly 11.9% this quarter, outperforming its value peer and narrowing the gap for the year-to-date performance.

At 715 a.m. ET, Dow e-minis were down 54 points, or 0.16%, S&P 500 e-minis were down 1.5 points, or 0.04%, and Nasdaq 100 e-minis were down 16.75 points, or 0.12%.

Wednesday’s cautious turn follows strong data from the US and Europe that show surging confidence in the economic recovery. That according to Bloomberg, suggests markets remain finely balanced between hopes for an imminent return to normal and fears that runaway inflation or Covid variants could derail the rebound.

Shares of Micron Technology, which is expected to post quarterly results after markets close, rose 1.0% as they headed for their fourth straight monthly decline. Here are some of the biggest U.S. movers today:

- Altimmune (ALT) plunges 38% in premarket trading after the company said after the close it will discontinue its Covid-19 vaccine trials. Analysts lowered their price targets while seeing the move as the right choice to refocus the company’s efforts on ongoing obesity and liver programs.

- Software stocks Exela Technologies (XELAU) and Powerbridge Technologies (PBTS) surge 54% and 25% respectively with the two stocks being touted on Reddit.

- Kiromic BioPharma (KRBP) sinks 24% after announcing it priced 8 million shares of its common stock at a public offering price at $5 per share, with gross proceeds reaching $40 million.

- Vertex Energy (VTNR) gains as much as 49% in premarket trading after Clean Harbors (CLH) agreed to buy some of the company’s assets for $140 million.

- Cryptocurrency-exposed stocks are falling in premarket trading Wednesday as Bitcoin drops back below $35,000 following a three-day rally: Riot Blockchain -3.6%, Marathon Digital -2.8%, Coinbase -0.4%, Ebang -1.9%, Ault -2.9%; Other crypto-exposed stocks: Tesla -0.4%, Silvergate Capital -0.5%, Square -0.5%

“The environment in Q3 should still be supportive for risky assets, though fear of bouts of persistent inflation could alter this scenario,” Sebastien Galy, senior macro strategist at Nordea Investment Funds SA, wrote in a note. “We expect to see bouts of volatility from this.”

European shares slumped with the Stoxx 600 dropping -0.6% after sliding more than 1% earlier with cyclical stocks bearing the brunt of losses. Airlines struggled as fears of the more contagious Delta variant continue to spur tourism curbs in the region. The Stoxx 600 Automobiles & Parts Index dropped as much as 2.8%, the steepest intraday decline since May 19, and is the day’s worst-performing subgroup on the wider European gauge; the SXAP is trading at the lowest level since May 26. Worst performers include: Volkswagen -3.4% and its controlling shareholder Porsche Automobil Holding SE -4.7%, Valeo -3.4%, Faurecia -2.8%, Renault -2.7%, BMW -2.5%. Here are some of the biggest European movers today:

- GrandVision shares surged as much as 14% after EssilorLuxotticasaid it will close its EU7.3b acquisition of the Dutch eyewear retailer at the agreed-upon price, confounding investors who had expected the buyer to seek a discount following an arbitration ruling.

- Solutions 30 shares jumped as much as 17% after shareholders voted to approve the Luxembourg- based technology-services company’s 2020 financial accounts, which its auditor Ernst & Young had refused to certify.

- Indivior Plc shares rose as much as 11% after the company raised its full year 2021 guidance. Stifel said the upgrade to Sublocade guidance reflects the waning impact of Covid-19 on holding back growth of the product.

- Vallourec shares gained as much as 6.9% after Jefferies upgrades the stock, saying co.’s financial restructuring has addressed concerns over its balance sheet and there remains upside risks to 2021 Ebitda guidance.

- The Stoxx 600 Automobiles & Parts Index dropped as much as 2.8%, the steepest intraday decline since May 19, and is the day’s worst-performing subgroup on the wider European gauge; the SXAP is trading at the lowest level since May 26.

- Worst performers include: Volkswagen -3.4% and its controlling shareholder Porsche Automobil Holding SE -4.7%, Valeo -3.4%, Faurecia -2.8%, Renault -2.7%, BMW -2.5%

- Safilo Group shares plummeted as much as 17% in Milan trading, the steepest intraday

Asian stocks erased an early gain on Wednesday while still set to cap their longest quarterly winning streak since 2007. Chinese stocks advanced after manufacturing data suggested the economy’s recovery is stabilizing at a solid pace, and the tech-heavy ChiNext Index climbed 2.1% to a six-year high on gains in EV battery maker CATL. Notable gains were also seen in Singapore and Taiwan, while benchmarks slipped in Hong Kong and Japan. Technology stocks were the biggest boosts to the MSCI Asia Pacific Index, while a gauge of healthcare companies fell. The regional benchmark was on track for its fifth-straight quarterly gain, advancing 2.4% in April-June. That achievement comes in spite of mostly sideways trade in June as investors assess the sustainability of the more than 70% surge in the Asian stock gauge from last year’s pandemic low. Stocks rose early Wednesday after U.S. peers set a fresh record overnight and Moderna said its Covid-19 vaccine produced protective antibodies against the delta variant. “Optimism on the vaccine front to curb the delta variant may induce some relief for investors,” said Jun Rong Yeap, a market strategist at IG Asia. “That said, the vaccination progress in the region will have to see some significant pick-up in order to deal with the spreads. Otherwise, Covid-19 restrictions will remain the go-to option to curb the spreads, delivering some risks to the pace of economic recovery.”

Japanese stocks also fell as concerns over the delta variant of the virus damped investor sentiment despite Wall Street’s climb to a record. The Topix dropped for a second day, slipping 0.3% to 1,943.57 in Tokyo, while the Nikkei 225 declined 0.1% to 28,791.53. Sony Group Corp. contributed the most to the Topix’s loss. Today, 1,294 of 2,187 shares fell, while 783 rose; 25 of 33 sectors were lower, led by transportation equipment stocks. Terminal users can read more in our markets live blog. “With the delta variant infection outbreak occurring, it’s possible that reopen trade stocks — such as air transport and railway shares — will decline again,” said Norihiro Fujito, chief investment strategist at Mitsubishi UFJ Morgan Stanley Securities. “It’s possible that the delta variant spread could drag on Japan’s economic normalization into fall.” Japan’s government is planning to extend strong virus measures it has in place in Tokyo and other areas by two to four weeks to coincide with the early days of the Olympics, the Mainichi reported Monday. The Topix completed a 1.1% monthly gain, paring its loss for the quarter to 0.5%. The Nikkei 225 had a 0.2% loss for June, falling 1.3% for the quarter.

In rates, Treasuries rose as traders digested the latest Fed comments. On asset purchases, Thomas Barkin said Tuesday he wants to see much more U.S. labor market progress before slowing them, while Christopher Waller said economic performance warrants thinking about pulling back on some stimulus. Treasury yields are richer by 2bp-3bp from intermediates out to long-end of the curve, flattening 2s10s by 1bp, 5s30s by 0.5bp; bunds outperform by ~1bp in 10-year sector, flattening the German curve by a wider margin. Month-end extensions may provide additional support Wednesday, although no signs emerged during a lackluster Asia session. EGB outperformance comes amid June euro-area inflation ebb. In Europe, core fixed income curves bull flatten. Bunds richen ~3bps at the long end, outperforming gilts and Treasuries by 1-1.5bps. Peripheral spreads tighten to core, BTP rally out of well received auctions. The focal datapoint of U.S. session is June ADP employment change.

In FX, the Bloomberg Dollar Spot Index was a tad higher, rising a third day, and the greenback was mixed versus its Group-of-10 peers, though moves were confined to tight ranges; the euro hovered around $1.19. The pound was steady even after data showed the U.K. economy shrank more than expected in the first quarter, while fears lingered over the potential impact of the delta variant on the reopening schedule. The U.K.’s GDP declined 1.6% in the first quarter, slightly worse than the 1.5% previously reported. Still, the savings ratio rose to 19.9%, adding to a cash pile that is now powering a consumer boom. Australia’s dollar erased an Asia-session gain to touch a one-week low versus the greenback; sentiment remained vulnerable with half of the population under lockdown as the authorities try to contain outbreaks of the contagious Delta strain of the coronavirus; the kiwi also slipped, in tandem with the Aussie. The yen hovered around 110.50 per dollar and headed for a secondly monthly decline.

In commodities, crude futures reverse a modest dip to trade just shy of Asia’s best levels. WTI gained 0.6% to trade near $73.40, Brent stalls near $75. Spot gold trades off worst levels, down $3 near $1,758/oz. Most base metals are in the green: LME lead outperforms, gaining as much as 1.7%; aluminum underperformed. Bitcoin slipped to trade around $34,600.

Today we got the latest mortgage applications which dropped 6.7%, the biggest decline in 5 months. We also get the latest ADP Employment report, which is expected to show 600K new private payrolls. U.S. pending home sales data for May is at 10:00 a.m. Latest crude oil inventories are at 10:30 a.m. USDA quarterly crop stocks data is at 12:00 p.m. Atlanta Fed President Raphael Bostic and Richmond Fed President Tom Barkin speak later. Constellation Brands Inc., General Mills Inc. and Bed Bath & Beyond Inc. are among the companies reporting.

Market Snapshot

- S&P 500 futures down 0.26% to 4,271.00

- STOXX Europe 600 down 1.06% to 451.54

- MXAP down 0.1% to 208.30

- MXAPJ little changed at 700.87

- Nikkei little changed at 28,791.53

- Topix down 0.3% to 1,943.57

- Hang Seng Index down 0.6% to 28,827.95

- Shanghai Composite up 0.5% to 3,591.20

- Sensex up 0.2% to 52,664.79

- Australia S&P/ASX 200 up 0.2% to 7,313.02

- Kospi up 0.3% to 3,296.68

- Brent Futures up 0.29% to $74.98/bbl

- Gold spot down 0.16% to $1,758.44

- U.S. Dollar Index little changed at 92.13

- German 10Y yield fell 1.8 bps to -0.188%

- Euro little changed at $1.1892

Top Overnight News from Bloomberg

- Wagers on the spread between December 2022 and December 2024 Eurodollar futures — a play on how the rate hike cycle will evolve over that period — have surged in popularity this week. On Friday, Morgan Stanley strategists argued the spread could widen on both better- and worse-than-expected jobs data

- The Biden administration is developing an executive order directing agencies to strengthen oversight of industries that they perceive to be dominated by a small number of companies, a wide- ranging attempt to rein in big business power across the economy, according to people familiar with the plans, Dow Jones reports

- Euro-zone inflation cooled in June to temporarily ease concerns that the bloc’s economic reopening will fuel price growth, though economists expect the pressures to gather pace again in the second half of the year

- British households saved a fifth of their disposable income in the first quarter as the U.K. returned to lockdown, adding to a cash pile that is now powering a consumer boom

- New Bank of Japan board member Junko Nakagawa says it’s appropriate to continue with the bank’s current monetary stimulus

- The Swiss National Bank’s foreign exchange transactions totaled just 296 million francs ($321 million) in the first quarter, the smallest sum since the onset of the pandemic

- OPEC and its allies delayed preliminary talks between ministers by a day to allow more time for a compromise before a critical meeting on Thursday, according to two delegates

- Oil is heading for its best half since 2009 as the rebound from the pandemic boosts fuel consumption and tightens the market ahead of a key OPEC+ meeting that’s expected to lead to an increase in supply

Quick look at global markets courtesy of Newsquawk

Asian equity markets head into month-end mostly positive but with gains capped as the early momentum and attempt to improve upon the flat performance stateside, was tempered as participants digested a slew of data releases including the latest Chinese PMIs. Nonetheless, ASX 200 (+0.2%) was led higher by telecoms after Telstra announced the sale of a 49% stake in its towers business for AUD 2.8bln and with the index also propped up by strength in most commodity-related sectors aside from energy which suffers due to hefty losses in AGL Energy following its decision to demerge. Nikkei 225 (Unch.) failed to hold on to early gains with participants indecisive amid reports Japan is considering extending its quasi-virus emergency in Tokyo by 2-4 weeks and after disappointing Industrial Production data which showed the steepest contraction in a year, while the KOSPI (+0.3%) was also influenced by data with Industrial Production showing its largest growth in more than a decade despite actually missing forecasts. Hang Seng (-0.6%) and Shanghai Comp. (+0.5%) lacked firm direction following the Chinese PMI data in which the headline Manufacturing PMI topped estimates but showed slower growth in tandem with the softer Non-Manufacturing and Composite PMI readings. There were also reports that China’s leadership is straining to dial back its country’s chest-thumping “Wolf Warrior” approach to foreign policy on concerns it could undermine the country’s interests, while focus was also on IPO news with Didi pricing its US IPO at the top of the indicated USD 13-14/shr range ahead of today’s debut. Finally, 10yr JGBs were subdued heading into month-end with price action hampered by the lack of BoJ presence in the market and after the central bank also reduced its purchase intentions across three tranches for the July-September quarter.

Top Asian News

- Jimmy Lai’s Next Digital to Shut Down July 1 Amid China Pressure

- AIA Agrees to Buy China Post Life Stake for $1.9 Billion

- Married Couple Builds $2.2 Billion Fortune on Bubble Tea IPO

- Evergrande Meets One of China’s Three ‘Red Lines’ on Debt

European equities have adopted a more pronounced downside bias (Euro Stoxx 50 -0.9%) following a relatively mixed and directionless cash open – with fresh macro news flow also on the lighter side thus far on the final day of June, Q2, and H1. US equity futures have also succumbed to the losses seen across the pond, but with losses notably less pronounced. The NQ (-0.1%) is cushioned as bond yields are pressured, whilst the YM (-0.3%) and ES (-0.2%) fare better than the RTY (-0.5%). Back to Europe, sectors are now in the red across the board with the broader sectors portraying more of a defensive bias – with Healthcare, Telecoms, and Staples among the “better” performers. Delving deeper into the sectors, Oil & Gas (-1.5%) and Banks (-1.7%) reside among the laggards amid losses in the crude and yield complexes respectively – but Autos and Parts (-2.4%) are the marked underperformers amid the ongoing chip crunch weighing on production heading into earnings and delivery releases. On that note, Renault (-2.3%) announced plans to accelerate its EV strategy, with the launch of 10 new Battery EVs (BEVs) by 2025, whilst Volkswagen (-3.8%) is lagging, with reports yesterday suggesting that Ohio’s Supreme Court green-lighted the state’s attorney general to move forward with a lawsuit against the car maker over its “Dieselgate” scandal and manipulation of emissions-control systems. On the flip side, Unipol (+3.7%) shares remain supported by Investment vehicle Koru stating that it is mulling a 3.35% stake in the Co. via reverse accelerated book building and at a 6.6% premium to Tuesday’s closing price. Morrisons (+0.6%) meanwhile is kept afloat by the broader defensive flows alongside shareholder J O Hambro (2.9% stake) stating that CD&R must hike its bid from GBP 2.30/shr to GBP 2.70/shr if it wants the takeover to succeed. In terms of equity commentary, Barclays warns that risk appetite could wane heading into the summer lull, and spikes in real rates would be a key tail risk for the equity complex. “Yet we expect the bid for equities to continue, supported by earnings fundamentals, still high bond/cash positions, and buybacks.” The bank says. Barclays also suggests that some reflation trades were reset following last month’s FOMC meeting, with cyclicals reduced and value still appearing to be well-owned.

Top European News

- Ray-Ban Owner Goes Ahead With $8.7 Billion GrandVision Deal (2)

- Zaoui Brothers Join Europe’s Blank-Check Rush With Odyssey SPAC

- Macquarie Targets U.K. Rental Housing With $1.4 Billion Launch

- Russia Conducted Cyber Attack on German Banking System: Bild

In FX, the Greenback has slipped back from Tuesday’s highs, but remains underpinned awaiting any late or final month end rebalancing flows that may apply some downside pressure around the end of the European session and/or over the NY close. However, the Dollar continues to resist the bulk of June 30’s negative signals via various bank models in the interim, and from a macro perspective will be looking towards ADP for direction along with pointers for Friday’s NFP release after the first of today’s four scheduled Fed speakers, the Chicago PMI as a proxy for tomorrow’s manufacturing ISM and then US housing data again. In index terms, 92.00 is still proving to be pivotal and the range thus far is 92.162-91.998 vs 92.194-91.852 yesterday, with one basket component in particular keeping the DXY capped. Usd/Sek is trading down near 12.0300 and Eur/Sek around 10.1200 amidst few signs of disappointment over Sweden’s Euro defeat at the knock-out stage last night, as SEB signals a strong Krona buying requirement against the Buck especially.

- CHF – At the other end of the G10 spectrum and hardly helped by a significantly weaker than forecast Swiss KOF leading indicator or investor sentiment, the Franc is floundering and striving to contain losses under 0.9200 vs the Greenback and sub-1.0950 against the Euro, regardless of the country’s Finance Minister lowering the estimated cost of pandemic debt relief to Chf 25 bn from Chf 30 bn.

- NZD/CAD/AUD – Very little respite for the non-US Dollars, and a marked downturn in broad risk sentiment as the month, quarter and half year draws to a close is also weighing on the Kiwi, Loonie and Aussie. Indeed, Nzd/Usd is now eyeing and relying on support circa 0.6975 to arrest a slide following a mixed NBNZ business survey overnight, while Usd/Cad has scaled 1.2400 before Canadian monthly GDP and PPI updates, and Aud/Usd is probing 0.7500 to the downside in wake of Chinese NBS PMIs that revealed a sub-consensus services print and the CBA flagging latest lockdowns as a reason why the RBA could be less inclined to halve the pace of bond purchases at next week’s policy meeting.

- GBP/EUR/JPY – All narrowly mixed vs their US peer, but Sterling unable to regain 1.3850+ status with any real conviction or pull away from 0.8600 against the Euro in the manner that England did at Wembley when facing Germany to reach the Quarter Finals. Meanwhile, 1.1900 continues to act as the focal point for the Euro vs the Buck and 110.50 is keeping the Yen tethered with hefty option expiry interest at the strike (1.9 bn) and either side (1.6 bn from 110.25-20 and 1.5 bn from 110.70-75), irrespective Japanese ip falling over twice as much as expected in May on the m/m basis.

In commodities, WTI and Brent front-month futures are choppy as the complex attempts to balance broader market sentiment with OPEC and Iranian developments. WTI and Brent hit session lows of USD 72.82/bbl (vs high 73.61/bbl) and USD 73.93 (vs high 74.80/bbl) respectively in a move that coincided with declines across equities, whilst a base was found in conjunction with reports that Iranian nuclear talks have been postponed to an unspecified date – suggesting a smaller likelihood of Iranian oil returning to the market in the initially expected time frame. Elsewhere, the OPEC JTC on Tuesday did not provide a recommendation for ministers to consider. The JTC signalled uncertainty about the spread of COVID variants and the speed of vaccine rollouts. It also said that it is monitoring sovereign debt levels, inflation rates, and central bank actions. In fitting with the June MOMR, the JTC expects a rebound in oil demand and strong growth in H2. All-in-all, the technical committee reviewed a range of scenarios and aligned their base case with the June MOMR. Sources suggested Moscow and Riyadh have different views regarding the pace at which oil should be brought back to the market, with the latter favouring a more gradual approach. The Kuwaiti oil minister suggested the group is cautious about raising output amid challenges. The OPEC, JMMC, and OPEC+ meetings are all slated for Thursday at 12:00BST, 15:30BST and 17:00BEST respectively. The JMMC meeting was pushed back with some citing Russian Deputy PM Novak’s calendar, although sources suggested it is to allow for more time to negotiate a compromise (newsquawk’s updated primer is available here). Turning to metals, spot gold and silver are flat within tight ranges and near yesterday’s lows around the USD 1,750/oz and USD 26.75/oz respectively awaiting tomorrow’s US ISM Manufacturing and Friday’s US jobs report. In terms of base metals, LME copper is modestly firmer but in the grander scheme, the red metal is consolidating near recent lows. Dalian iron ore futures fell over 3%, with traders citing China’s continued crackdown whilst the regions Official PMIs also underwhelmed

US Event Calendar

- 7am: June MBA Mortgage Applications, prior 2.1%

- 8:15am: June ADP Employment Change, est. 600,000, prior 978,000

- 9:45am: June MNI Chicago PMI, est. 70.0, prior 75.2

- 10am: May Pending Home Sales YoY, prior 53.5%; Pending Home Sales (MoM), est. -1.0%, prior -4.4%

Tyler Durden

Wed, 06/30/2021 – 07:48![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com