Oil Spreads Are Trading At Historically Unrealizable Levels

Authored by Brynne Kelly via Cornerstone Global Commodities,

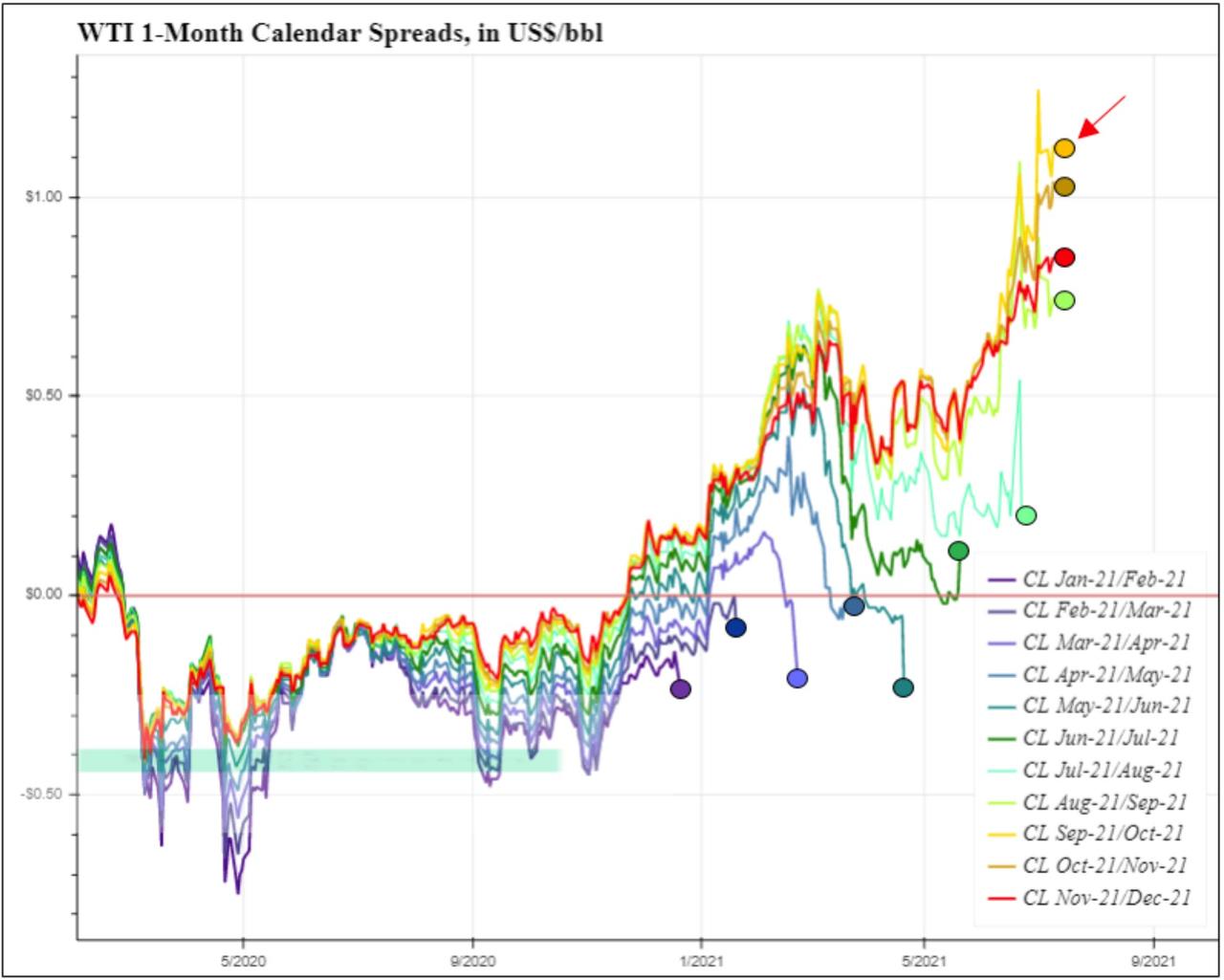

Outright oil prices have continued to rally this year as economies recover from impaired pandemic levels, however calendar spreads have been unable to realize their bullish intent. In fact, calendar spread structures have continued to disappoint into expiration.

In some respects this is less about a failure of the front-month contract heading into expiration and more about a handing-off of strength to the next contract, which narrows the front spread into expiration.

The close-knit nature of 1-month spreads relative to moves in flat price may not reveal a useful pattern. Towards that end, when we lengthen our spread analysis to incorporate more time into the picture (6 or 12 month spreads vs 1 month spreads), the pattern becomes more visible. The pattern being that bullish sentiment is portrayed through calendar spreads until expiration. In both cases (the Dec/Dec 12 month spread and the Dec/June/Dec front vs back condor spread) are prone to follow market sentiment and rally along with flat price only to fail as expiration approaches.

At the moment, both of these spreads are approaching levels that have been UNREALIZABLE in the past.

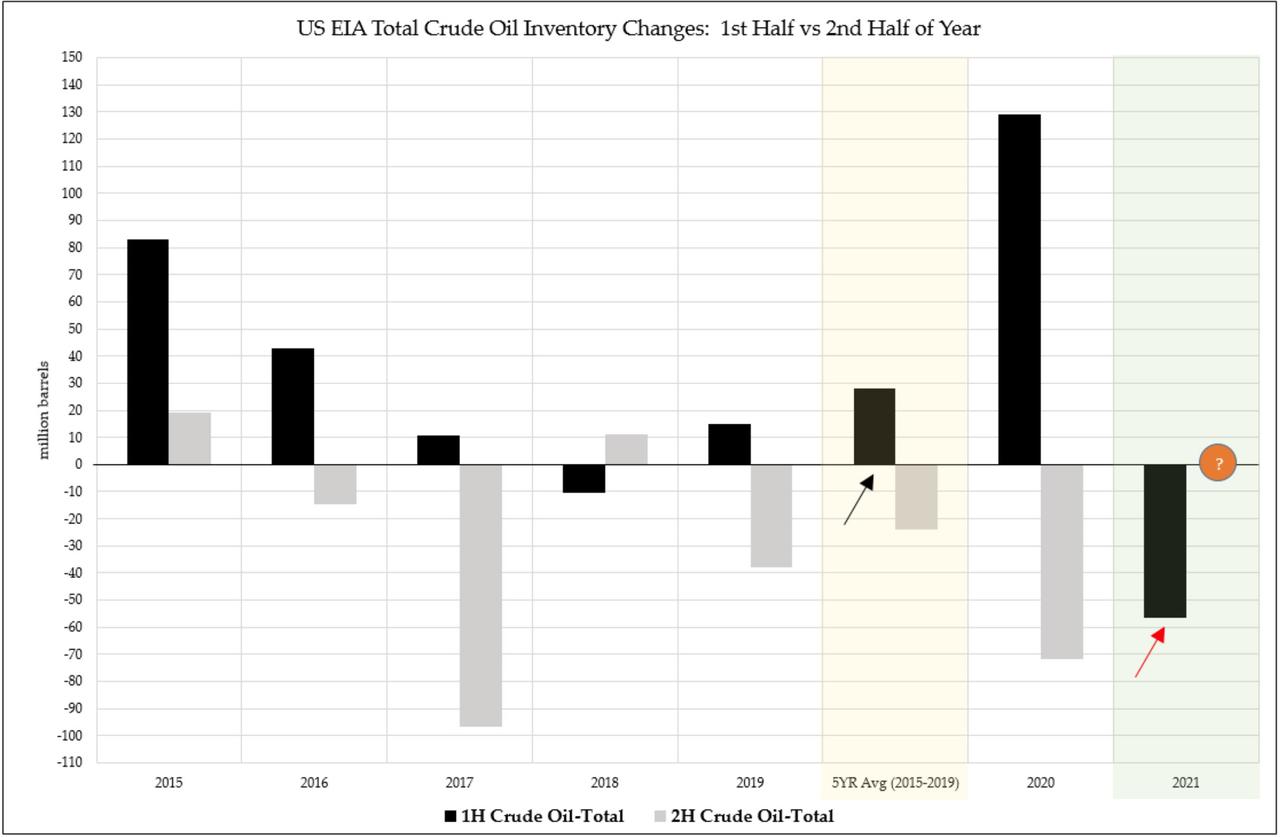

What does this mean going forward?? Are we likely to see spreads break historical records to the upside before pulling back into expiration, or will we finally realize historical highs in backwardation? To unpack this we start with inventories. First we break the year down in to the first half versus the second half and then compare the changes in these 2 periods over time and also against their 5-year average (ex 2020), highlighted in yellow below.

Futures backwardation has induced significant US inventory drawdowns this year, which essentially means we are borrowing barrels from the future (taking barrels out of inventory today in hopes they can be paid back at lower levels in the future). The result being that oil inventory draws for the first half of 2021 were larger than any in recent history. In fact, since 2015 there has only been one other year when the first half of the year posted a net draw in crude oil inventory and that was in 2018 (black bars below = first 6 months of the year, grey bars = last 6 months of the year). Given the magnitude of the build we saw in 2020, we are still a long way off from matching 1H 2020 builds with 1H 2021 draws, but it IS a break in the overall pattern.

The second half of the calendar year is generally known for draws in oil inventories, although not as definitively as the first half is known for builds (grey bars above). Yet, in none of the years since 2015 has oil drawn in the first half AND the second half of the year. Even in 2020, when we had massive builds in the first half of the year, the second half of the year saw inventories decline.

Given the shape of WTI calendar spreads, and the performance of spreads to date, futures spreads are currently registering levels that should continue to entice storage draws and reach their peak in the Sep/Oct spread (gold line, shown earlier above).

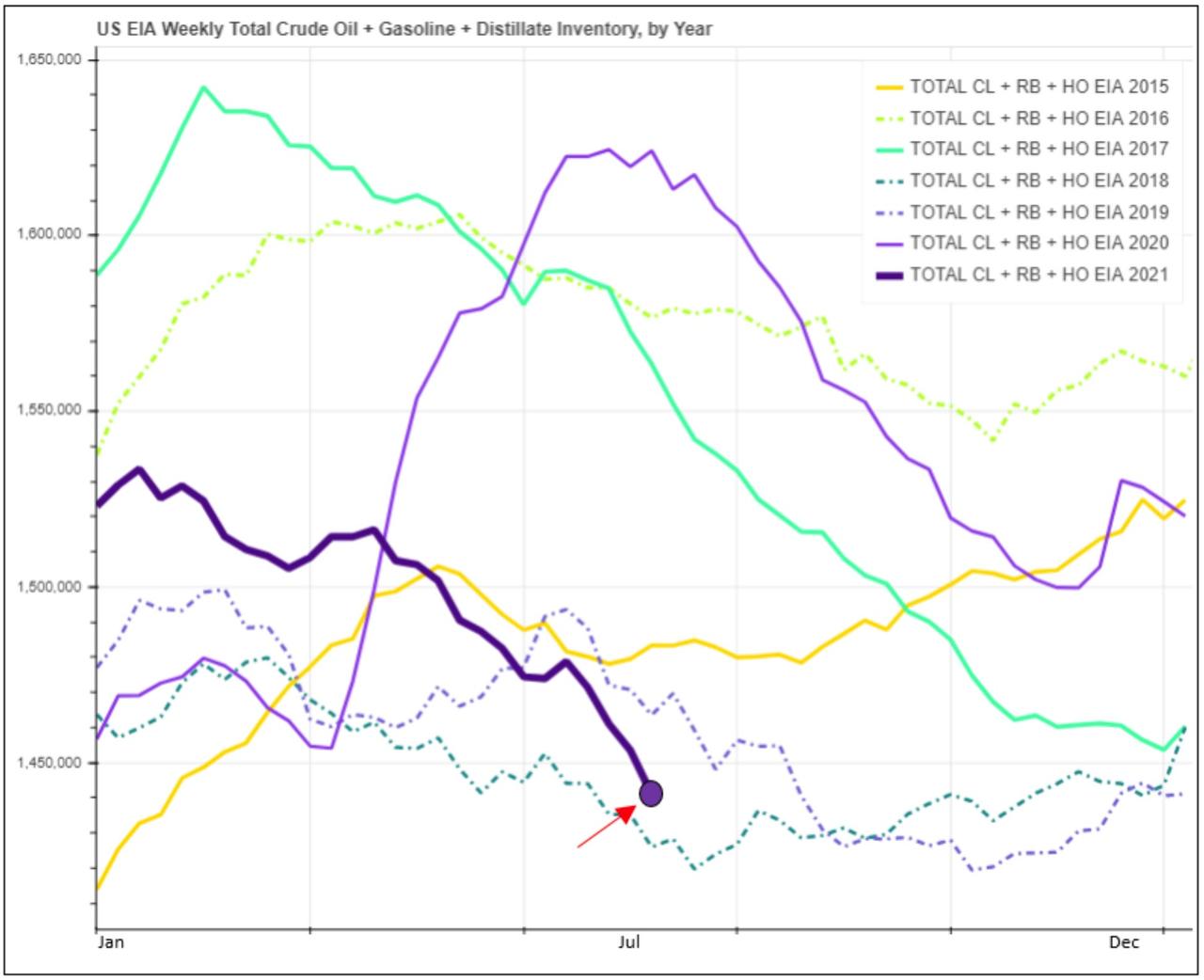

The result of all of this is the lowest US crude oil inventory (plus SPR) since 2015 (dark purple line below). To continue to draw down oil inventory in the second half of the year – from here – would no doubt be supportive.

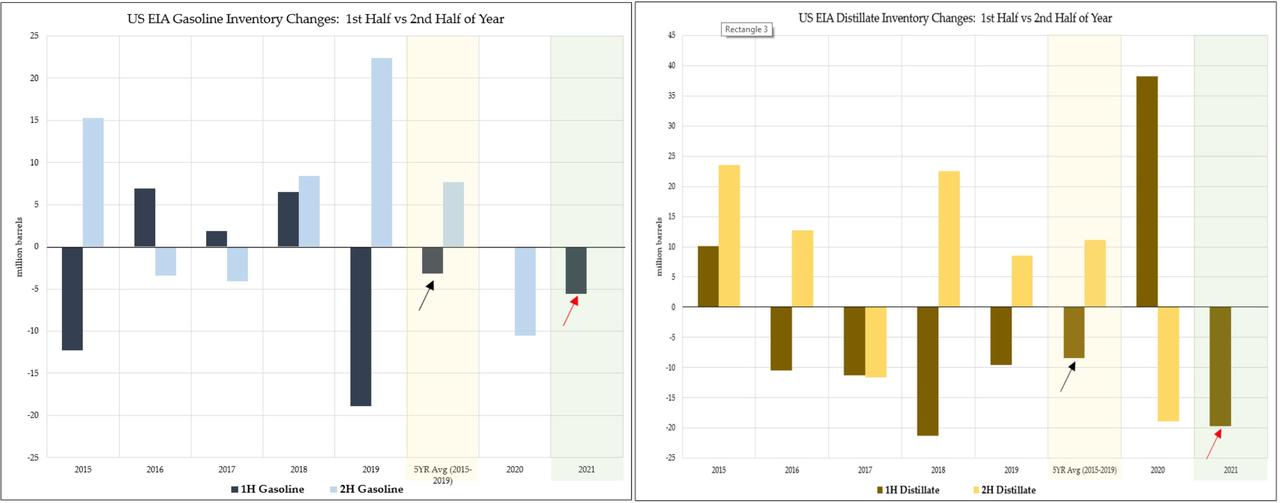

In contrast, gasoline and distillate inventory changes this year have not only mimicked their 5-year average changes (of inventory reductions) in the first half of 2021 but also exceeded them (although neither is an outlier in 2021 the way the crude oil is).

Regardless, total combined inventory levels (crude oil + gasoline + distillate) are low by recent historical standards, sitting just slightly above 2018 levels.

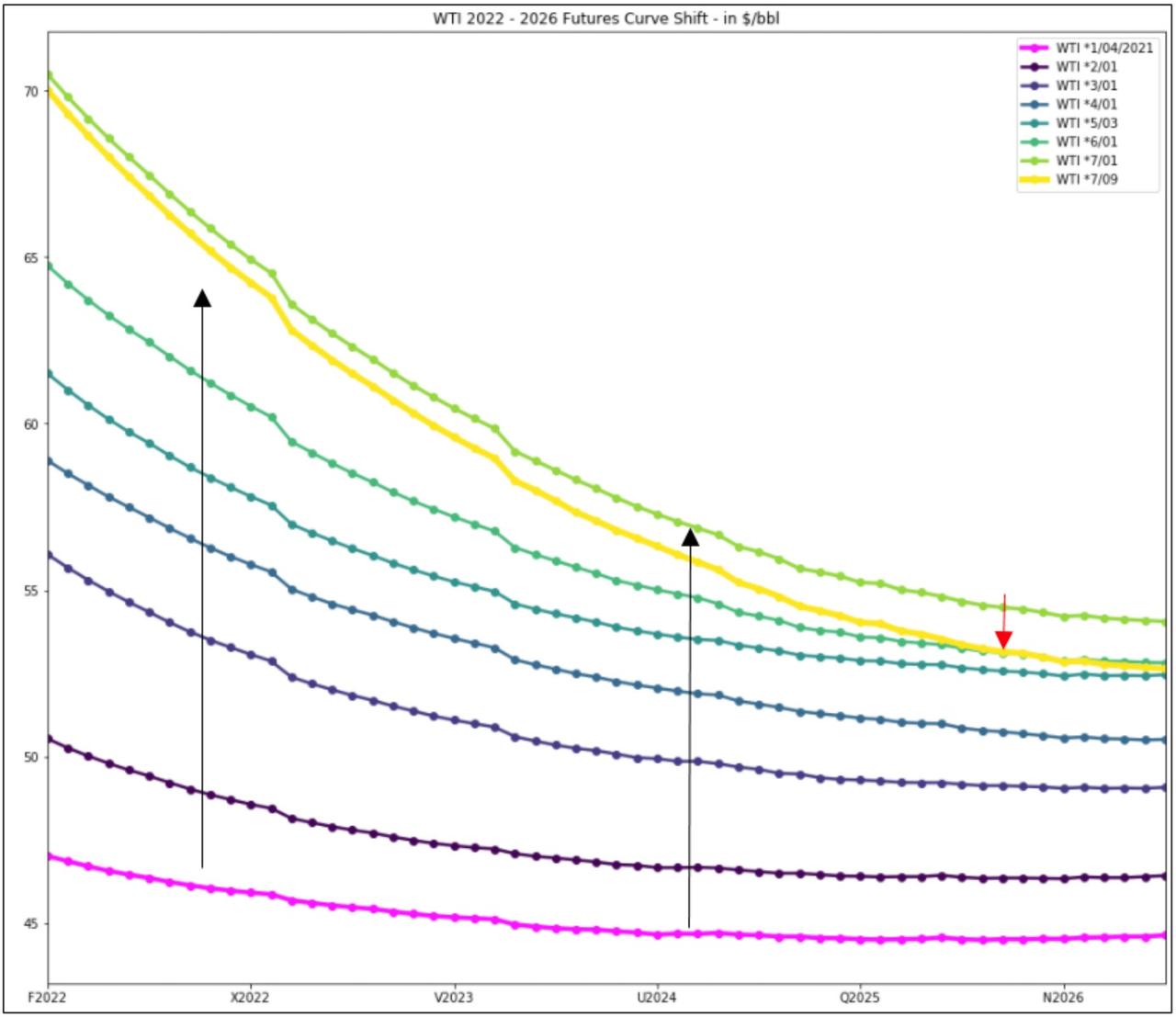

So, what is stopping us from continuing to move higher? It could be the selling showed up in July in the back of the curve, causing it to lose ground to the front of the curve and push calendar spreads higher.

This is evident through the lens of the futures curve shape below. The entire curve had been shifting higher through the end of June and then the back began losing ground to the front in July (yellow line = 7/09/21 CME futures settlements).

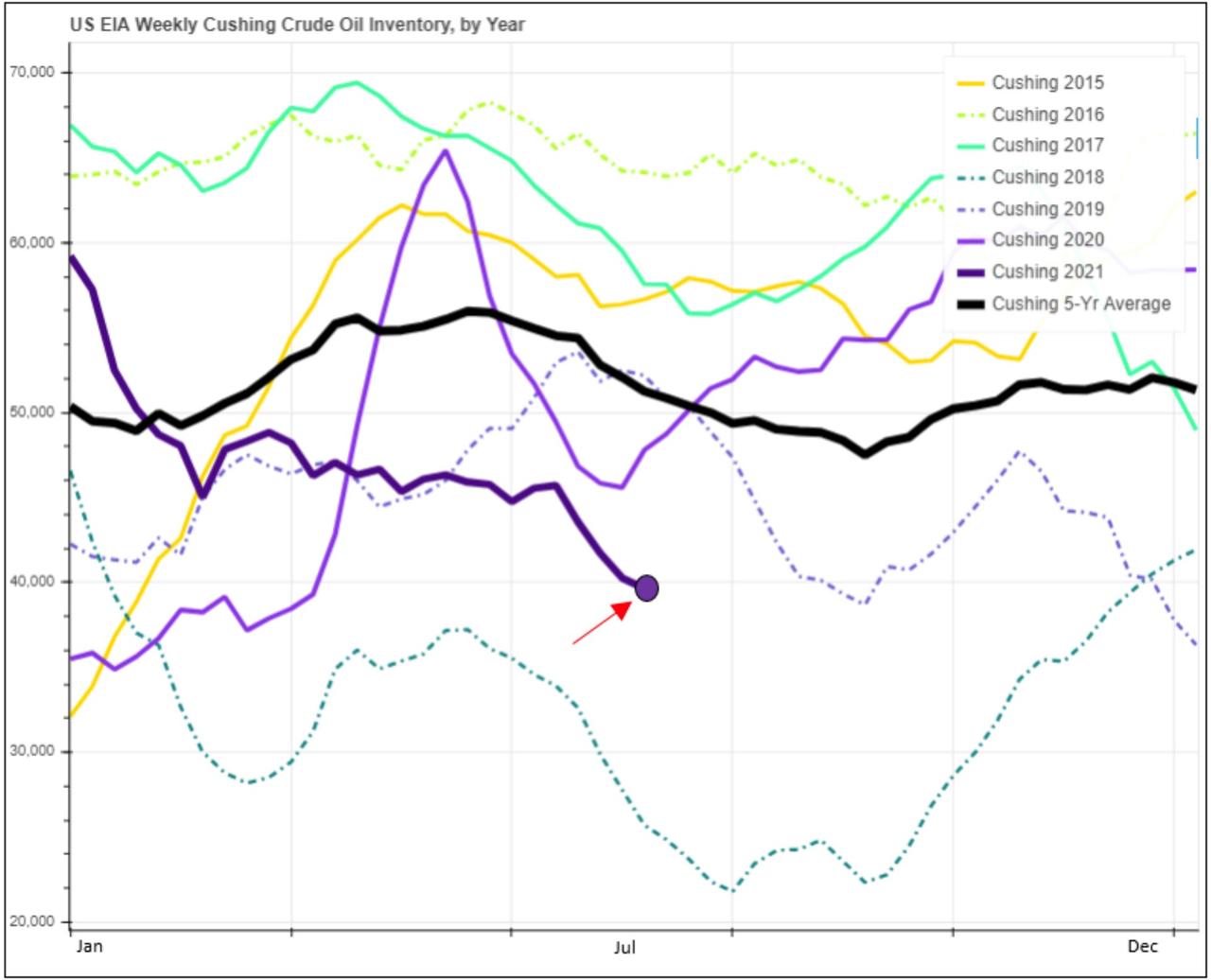

For all the press that Cushing inventories receive weekly, their story is not quite as interesting. Using the same yearly comparison we used for total inventories above, there is still some room to the downside for Cushing inventories before they dip below 2018 levels.

Using the inventory and spread picture from above, it’s clear that we have now reached the point where inventory levels could become problematic. It’s clear that the current pace of inventory draws cannot be sustained. Inventory draws are a result of non-normal backwardation. We are currently witnessing non-normal backwardation. Should the trend of draws continue from here through the second half of the year, the set-up for higher prices is intact.

Tyler Durden

Mon, 07/12/2021 – 05:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com