2020-2022 Versus 1929-1932

Authored by Alasdair Macleod via GoldMoney.com,

Current levels of equity markets are not only divorced from their underlying economic and business realities but are repeating the madness of crowds that led to the Wall Street crash of 1929—1932. The obvious difference is in the money: gold-backed dollars then compared with unbacked fiat today.

We can now begin to see how markets and monetary events are likely to develop in the coming months and this article provides a rough sketch of them. Obviously, the financial asset bubble will be burst by rising interest rates, the consequence of rising prices for consumer essentials. Fiat currencies will then embark on a path towards worthlessness because the monetary authorities around the world will redouble their efforts to prevent interest rates rising, bond yields rising with them, and equity values from collapsing; all by sacrificing their currencies.

The ghost of Irving Fisher’s debt-deflation theory will soon be uppermost in central bankers’ minds, preventing them from following anything other than a radically inflationary course regardless of the consequences.

Current views that tapering must be initiated to manage the situation miss the point. More QE and even direct purchases of bonds and equities are what will happen, policies that will certainly fail.

Anyone seeking to survive these unfolding conditions will be well advised to put aside some sound money – physical gold and silver.

Introduction

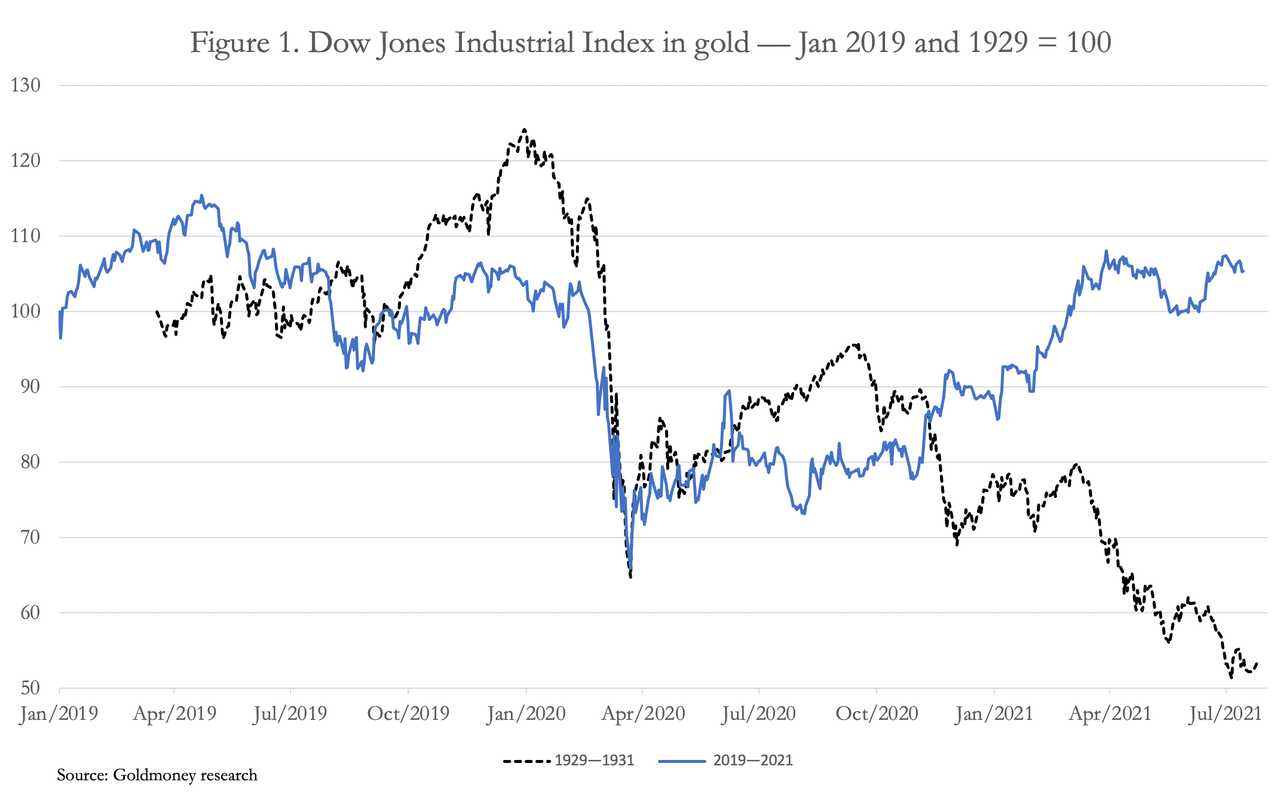

In the past I have compared the current market situation with 1929, when the US stockmarket suffered a major collapse that October. With memories short today, many will have even forgotten that between 12 February and 23 March last year the Dow Jones Industrial Index fell 38.4% top to bottom in less than six weeks, paralleling the 66% fall between 4 September and 13 November 1929 on an eerily similar timescale. Figure 1 shows the Dow of ninety years ago superimposed on top of that of today, shifted so that November 1929 coincides with March last year.

The principal difference is in the money. For this reason, Figure 1 adjusts today’s Dow by the gold price. In 1929-33, no such adjustment was required since the dollar was on a freely exchangeable gold standard at $20.67 to the ounce. But adjusting it by the gold price today tells us that measured in sound money the Dow peaked in April 2019. And following the initial rally after the crash in March 2020, a rise in the gold price has not been sufficient to suppress the Dow on a gold adjusted basis.

There are two possibilities: either the mid-bear market rally in the US stockmarket is lasting much longer than that between November 1929 and 21 April 1930, or the rise in the gold price has not yet been enough to counter the effect of monetary inflation. We can all have views on which is true. But one thing is certain: given zero interest rates, gathering price inflation and therefore the prospect of rising interest rates, evolving factors driving markets can only be strongly negative. When it comes this time round the fall in the Dow will almost certainly be catastrophic both in gold and nominal dollar terms. And the difference from 1929—32 is the massive expansion of money and credit that has been feeding into inflated financial assets.

As the background to stockmarket trends, there is enough circumstantial evidence for us to assume that the world is on the brink of a major financial catastrophe. The list of negatives is growing. It started with the US repo market blow-up in September 2019, followed by the Dow losing 35% in nominal points between 10 February and 23 March 2020 (as pointed out above) before the Fed stepped in to rescue the stock market by cutting the funds rate to the zero bound and reinstating QE to the unprecedented extent of $120bn every month, along with several other market-enhancing measures. They worked. At least, that is, if you ignore the costs and consequences.

Long before those mad-March days of last year, the Fed had been in crisis management mode — in fact ever since the Lehman failure. Backed by the goodwill of markets, whose participants still wish to avoid disaster as least as much as the Fed, the Fed succeeded. It prevented the excesses in residential property financing in the late 2000s from turning into a more general rout. But the cost has been a wobbly highwire act ever since, with investors observing central banks threatening at times with losing their precarious balance and falling into a yawning chasm of financial chaos.

With an investment establishment still wishing to believe in gravity-defying factors, such as good old fundamentals and the human right to let others to pay the price for their own follies, economic reality has been completely smothered. The Fed’s prestigitation has been achieved by printing money, increasing its balance sheet from $847bn the month that Lehman failed to $6,042bn today, an increase of over six times.

The Fed got away with its “extraordinary measures” in the wake of the Lehman crisis and along with the other major central banks found that through their careful management several succeeding crises were averted. And when covid came along and the world went into lockdown, the acceleration of monetary inflation to pay for it all was the obvious solution because its principal effect — rising prices — was under control.

Well, that’s not quite true beyond the purely statistical sense. It is more truthful to say the CPI statistic had been tamed to the point of irrelevance. Proof of this statistical legerdemain is there for anyone who cares to look for it, because the eximious John Williams of Shadowstats.com continues to produce the unexpurgated 1980 version, stripped naked from the subsequent adjustments in method deployed by the Bureau of Labor Statistics, all of which just happen to adjust price increases out of their inflation numbers. Williams’s estimates of price inflation, typically in the five to ten per cent range for the last ten years but now well above that, were confirmed by the Chapwood index, before covid stopped its statistical collection.

While Wall Street has been making whoopee on the back of increased money and credit, Main Street has been suffering. The only offset has been the availability of artificially cheapened finance. The liar loans of the noughties may not be back in actuality, but they certainly are in spirit as an artificial lifestyle support.

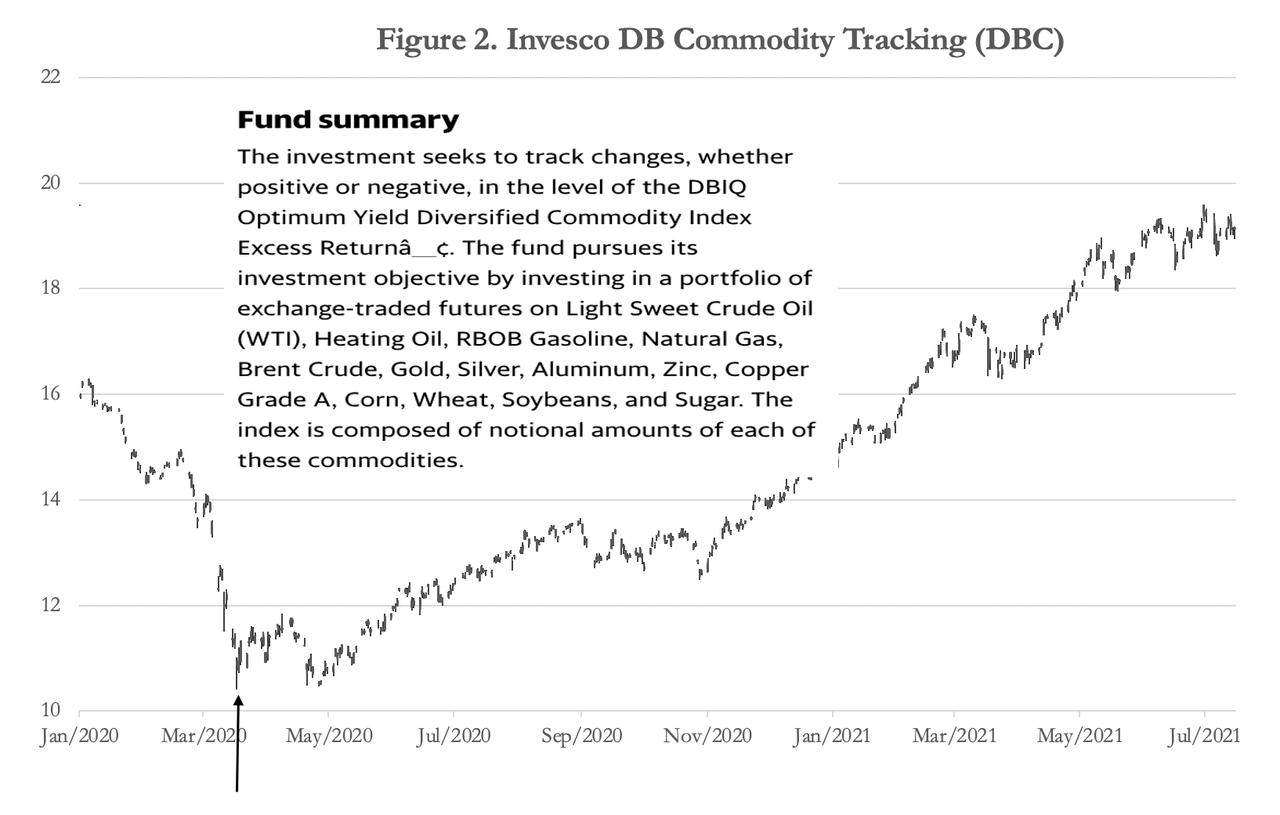

But the lesson for the bulls is that the days of claiming that inflation is confined to 2% or so are ending. The near doubling of the Fed’s monetary base from the time of the repo crisis in September 2019 has also seen an explosion in commodity prices. Figure 2 illustrates the point, with the up arrow showing the point where commodity prices turned higher, taking their cue from the precise moment of the Fed’s abandonment of all monetary restraint.

As well as rising commodity prices, Covid messed up global logistics, which still won’t be sorted until sometime next year, according to the experts. There is no leeway in inventories, due to the ubiquity of just-in-time product management. And as if to rub salt in these wounds, encouraged by more generous benefits the unemployed have become unexpectedly workshy.

The result is a material post-lockdown abyss between spending, all financed by expanding government deficits, and the availability of goods and services. Prices are not only rising due to all these factors but will continue to do so. But central banks are claiming price rises are only transitory and by next year supply chains will be working again, the balances between production and consumption will normalise and we will be back to its goal-sought 2% price inflation. But even Keynesian high priests are now warning price rises are likely to be sticky at the least, and as for the MMT crowd (remember them?) they have gone to ground.

Those of us who have taken the trouble to study the theories of money and credit know that the future is devolving into one of two choices for the authorities. The first is to continue with the policies of extend and pretend and watch the dollar and every other fiat currency suffer in terms of their purchasing power. Alternatively, central banks and governments must refuse to inflate the quantity of money any further and cut their spending to the bone. And they must permit both banks and businesses, when they fail, to do so.

Unfortunately, central banks only have a mandate for the former, and cannot stand back and let private sector actors sort it all out.

The Fed’s fast-approaching dilemma

We can be sure that, privately, growing numbers of the Fed’s FOMC realise it was a mistake to turn a blind eye to the inflation problem. And in the UK, Andy Haldane is leaving his post as chief economist to the Bank of England, while going on the record saying in effect that inflation is the elephant in the room. Lord Mervyn King, ex-Governor of the BoE was instrumental in a House of Lords report criticising the Bank’s inflationary QE policies.

The problem fast approaching all major central banks is that a rise in interest rates will be brought forward by their misjudgement on price inflation, a development which will directly challenge the policy of deploying QE to support financial markets and sustain confidence in the economy. And with the end of zero official interest rates, to continue support for financial assets requires an increase in quantitative easing to compensate. In other words, the money being fed to investing institutions will have to be supplemented to prevent risk assets falling in value.

There are two ways in which this can be attempted by the Fed. The first is to simply increase QE from the current $120bn every month, and the second is for the Fed, the US Treasury, or the Exchange Stabilisation Fund to supplement existing QE by investing directly into corporate bonds and equities to support prices. In other words, the inflationary policy of supporting asset prices by inflationary means will need to be dramatically accelerated, not tapered as commonly supposed.

Either way, the outcome is now set in stone. Further adjustments to monetary policy will only change the timing. But the only alternative, as noted above, is for central banks to withdraw and leave markets to their own devices. It is the dilemma that John Law faced in 1720, when he needed to accelerate the printing of money to buy shares in his Mississippi venture, which were being sold when calls were due by those who were either unable or reluctant to pay them. He believed that interest rates could be suppressed by flooding markets with money. Richard Cantillon disagreed (see more about Cantillon below).

The rate at which Law was forced to inflate in an attempt to keep interest rates suppressed and to keep the Mississippi bubble bubbling ended up destroying his unbacked livres’ purchasing power.

That the Fed faces the same problem will rapidly become apparent when it drags its heels in raising interest rates to protect the dollar. And the Fed is not alone. All the major central banks, with the notable exception of the Peoples Bank of China, have been pursuing the same policy of rigging markets in financial assets to maintain confidence in them by inflating their currencies. Therefore it is a mistake to simply look at exchange rates.

No market nor any currency can escape the destruction of what will then become unavoidable. A limitless acceleration of the money supply to stop interest rate expectations from collapsing financial markets will simply raise expectations of yet higher interest rates to come. And after stock markets begin to implode, the greater loss will then be seen in the purchasing power of fiat currencies.

Ever since the Fed decided that supporting markets was an economic priority, which was even publicly admitted as a policy objective by Alan Greenspan when he was Fed Chairman, this eventual outcome became a certainty.

Waypoints on the journey to currency collapse

When a market bubble bursts, nothing can stop the subsequent destruction. We must now look at how this descent into a vicious bear market is likely to unfold. The first truism to point out is that the losses will be exacerbated by a collapsing medium of exchange, and we should dismiss hopes, at least at the outset, that at some point bonds and equities will find a level where true value exists because, in the absence of fiat money being convincingly backed by gold there will be nothing to measure final values by.

We shall start by considering the factors raised by a collapsing currency. The process is already underway, as shown by Figure 2 above, which pinpointed the turnaround in commodity prices to March 2020, when the Fed went all-in on monetary inflation.

There is good reason to suggest that the current situation is dissimilar from the European inflations following the First World War. Unlike the conditions when various European currencies collapsed in the 1920s, there is no medium of exchange other than state fiat currencies. There was no doubt that in Germany, for example, the boom in exports which led to the availability of dollars and other currencies more stable than the paper mark slowed down the decline in purchasing power of the paper mark at least until the spring of 1923. It was only then that the German population collectively realised that the paper mark was worthless.

It is one thing to gradually destroy a currency’s purchasing power through its inflationary expansion. Since the Nixon shock, this has been the case, with the dollar losing all but 3% of its purchasing power measured in gold over the course of fifty years. The loss through the expansion of M3 broad money at 97.2% confirms the figure. But when the destructive path of global monetary inflation becomes patently obvious, the broad relationship between the expansion of money and credit and the currency’s purchasing power breaks down. It then becomes a matter of the speed with which the wider public educates itself to the inflationary facts.

The deployment of QE makes the John Law experience three centuries ago more relevant to the current situation than the better documented paper mark inflation. In examining the empirical evidence, we should consider two elements separately. First, the Mississippi company’s share price peaked at just over 10,000 livres in January 1720, falling to about 4,500 livres by the following September. But having weakened somewhat on the foreign exchanges in 1719, livres measured against the English pound sterling remained relatively stable at 30 to the pound until May, before the rate rose to about 110 at the beginning of September. It then became worthless on the foreign exchanges in London and Amsterdam.

The time taken for the livre to be publicly rejected as a medium of exchange was approximately a month less than the final collapse of the paper mark. While we have no idea how long a global rejection of fiat currencies might take today, the John Law experience suggests that financial asset values will begin to collapse ahead of the currencies in which they are priced. And the sense behind this timing is that after an initial collapse in asset values, monetary expansion will then be ramped up in response.

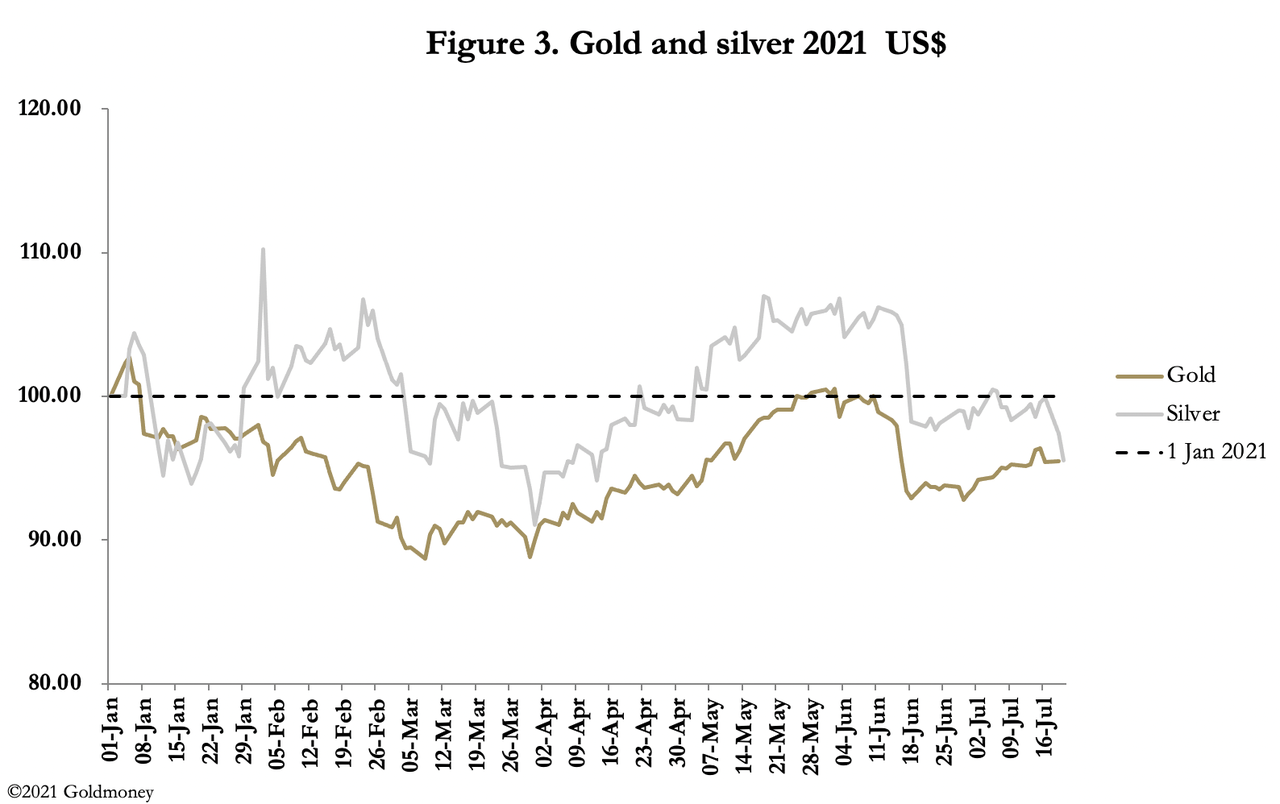

With today’s potential currency collapse being a global affair, we cannot measure the effect on asset values in any currency, but only in sound money. Throughout history sound money has been gold, which is why Figure 1 at the head of this article is relevant. And as Figure 3 below shows, having backed off from higher levels the gold price has been stable so far this year, with both gold and silver down a modiest 4.5%.

Could this equate to the livre’s relative stability in the first half of 1720 before its collapse? We should resist overinterpretation, but it seems very likely that when fiat currencies are dramatically overissued to support failing financial asset values, it will be reflected in a sharply rising gold price.

Reflecting currencies’ loss of purchasing power, further rises in commodity prices plus supply chain and scarce labour factors are all set to increase consumer prices significantly. The initial inflation effect on production costs will lead to cash flow difficulties for businesses, restricting output of goods and services even further. And as falling output leads to lower job security and rising unemployment, rising prices will be accentuated for essentials because spending will be increasingly focused upon them.

The contradictions of neo-Keynesian monetary policies will become fully exposed. On one hand, price inflation will be causing genuine hardship on Main Street, which suggests that interest rates should be allowed to rise to stabilise the currency. And on the other, rising insolvencies because of the diversion of cash flow to finance the consequences of inflation suggests they should be eased. But for dollars interest rates are already at the zero bound.

There is little doubt that in defiance of all common sense and empirical evidence FOMC members and their counterparts in other central banks will naturally opt for continued monetary easing and even plan for the introduction of price controls.

Fisher’s debt deflation theory

Clearly, the consequences of debauching currencies produce specific problems. Collapsing asset values produce others, and it is time to revisit the relationship between gross overborrowing and a fall in the price levels for collateral. Either disorder on its own need not be a disaster, but the combination is catastrophic. Furthermore, Irving Fisher’s analysis did much to inform economic and monetary policies following the depression in the 1930s, so will almost certainly become relevant for policy decisions again.

There were three key elements in Fisher’s thesis: grossly overextended balance sheets, a fall in the price level and very high interest rates. For today’s conditions, we must modify it slightly by amending the price level to apply to financial assets, though priced in gold it will also apply to consumer prices. And we must also note that interest rates are the nominal rates that apply to the currencies in which banks render their accounts.

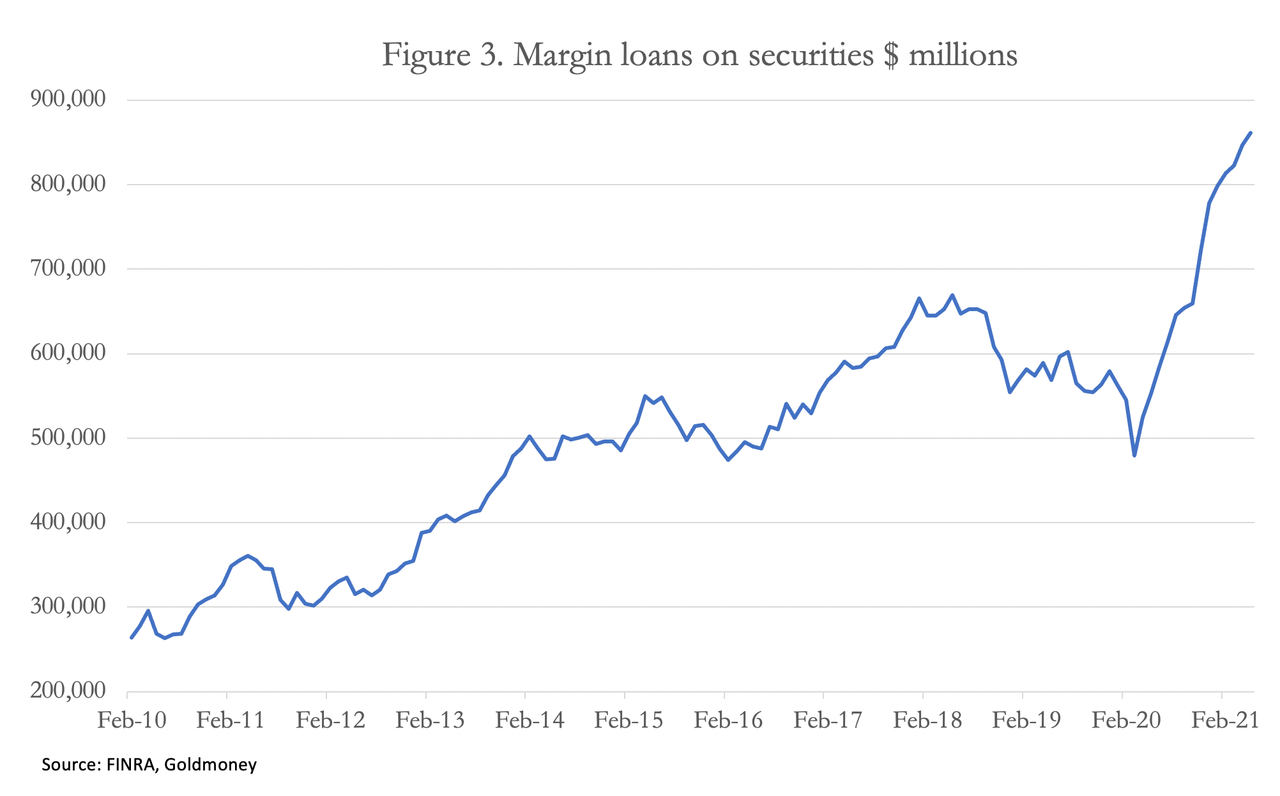

In its early stages, at least, we are considering Fisher’s debt-deflation theory as it applies to financial assets. In a stockmarket rout, falling collateral values will initially affect those who have borrowed to buy stocks. And as Figure 3 shows, this borrowing is at eye-watering levels, consistent with an extreme bubble. In a stockmarket slump, this will translate into sudden selling pressure from margin calls.

Next is portfolio allocation in US securities by foreigners, which according to the US Treasury’s TIC figures stood at $12.941 trillion in May. This is part of their total exposure across all securities and in bank deposits, $24.916 trillion and $6.552 respectively, totalling $31.468 trillion. From these figures we can see that as our John Law experience progresses, nearly $13 trillion in foreign-owned equities will be potentially for sale, bearing in mind that the first investments sold in any bear market are non-core foreign holdings — which is what US equities are to foreign investors.

US holders of foreign equities total a similar $11.69 trillion, so US selling of foreign equities will ensure that asset price deflation in US markets will be exported internationally.

Only now can we really test the relationship between gross overborrowing and a fall in financial asset values because they form the basis of collateralised lending. The Fed’s H.8 release Table 2 gives us clues where collateral liquidation is likely to have the greatest impact. Of bank credit totalling $15.632 trillion, only $2.468 trillion (15.8%) is in commercial and industrial loans. The greater exposure is in property ($4.644 trillion, 29.7%). It is in these two sectors that the collateral liquidation will occur.

Today’s US banking system appears to be less exposed to a debt-deflation crisis than the 1930s, which led to the failure of thousands of banks. Nevertheless, it is bad enough on the face of it to require the whole banking system to be rescued in the event of a debt-deflation crisis.

The consequences of a developing banking crisis are likely to accelerate a tendency by non-financial actors to precautionally reduce their bank balances. Acquiring physical banknotes has been rendered impractical by developments in the industry. The risk is that a race is likely to develop between the rate at which the purchasing power of bank deposit balances declines and the prices of individual assets and goods increase, further heightened by sellers of goods reluctant to accept increases in their bank balances. Instead of the crack-up boom being fuelled by cash payments delayed by the lack of available cash, the convenience of electronic payments suggest that the fall in purchasing power for fiat currencies will be considerably more rapid.

Learning from Cantillon

When Destiny with men for pieces plays, as individuals we are powerless to stop events. Even those notionally in charge can do nothing. And given that Fate is now in charge of events, it will be everyone for him or herself. But we can take some empirical guidance.

In 1714—1717, Richard Cantillon learned his trade as a banker in Paris working for his elder cousin Richard, the Chevalier Cantillon. He saw through Law’s pre-Keynesian schemes for what they were worth. Accordingly, he made two distinct fortunes from them. He loaned money to others to buy shares in Law’s scheme, sold them immediately without telling the borrowers and almost certainly looked very foolish for a while. But he successfully sued for repayment of nearly all his loans after Law’s bubble collapsed and he also pocketed the considerable proceeds of the share sales. His second and larger fortune was made by predicting the collapse of Law’s livre, selling as many as he could on the foreign exchanges in London and Amsterdam. The lessons for us today are that when the bubble bursts not to own financial assets, and then to dispose of unsound money.

The safest course of action is always the simplest, and we are not all unscrupulous bankers like Cantillon anyway. The equivalent of disposing of livres for sterling and Dutch florins is simply to acquire enough physical gold and silver to ride the inevitable monetary and economic crisis out.

Summary and conclusion

We can begin to see parallels between the 1929-32 financial crisis, but there are significant differences. The obvious one is monetary, with the Dow being priced in gold ninety years ago, while today it is pure fiat. But priced in gold, we can see from Figure 1 that today’s adjusted Dow peaked in April 2019.

The experience of the earlier financial crisis ninety years ago and its economic effects led to the gradual abandonment of sound money and the adoption of today’s policies informed by neo-Keynesian inflationism. It has ended up with central banks, led by the Fed, directing monetary policy to create a sustained wealth effect through asset price inflation. This policy was first admitted by Alan Greenspan, and accelerated by every crisis since —most notably, by Ben Bernanke dealing with the Lehman failure.

It has been a long trip, but thanks to a similar crisis in France three centuries ago we can begin to discern the likely outcome of current monetary policies. Combined with cyclical pressures repeating the market valuation excesses seen in 1929, central banks have also caused an inflation of prices which is now beyond their control. Interest rates are bound to rise and soon, something that is already being strongly resisted. The conditions for a collapse in financial assets are falling into place and we can be in no doubt that the monetary authorities will do anything to prevent it. It is either that or they stand back and let free markets sort things out for themselves, for which they have no mandate.

When it comes, the order is likely to be first an asset value crisis leading to attempted widespread liquidation. It will be rapidly followed by a currency collapse as panicked authorities try to sustain asset values. At least that is the logic we can now discern, confirmed by the empirical evidence from the John Law experience. The only security in these conditions, as French citizens discovered, was the possession of specie, that is metallic money — gold and silver bars and coins.

Tyler Durden

Sat, 07/24/2021 – 11:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com