The Debt Ceiling Non-Crisis & Why Rates Will Fall

Authored by Lance Roberts via RealInvestmentAdvice.com,

The financial media is rife with misinformation on the debt ceiling and the jump in interest rates. However, a review of history shows that not only is the “debt-ceiling” issue a non-crisis, but the recent rise in rates is likely an opportunity to buy bonds.

Let’s start with the media scare tactics over the debt ceiling:

-

If Congress doesn’t raise the debt ceiling, the Treasury will run out of money.

-

The U.S. will default on its debt.

-

The markets and economy will crash.

While there is a grain of truth behind these statements, they are largely false. However, for the media, a manufactured crisis should never be allowed to go to waste. To wit:

“As Washington teeters closer to a possible government shutdown at midnight Thursday, here’s why the status of the nation’s debt ceiling may ignite more worry in financial markets.

Sept. 30 marks the end of the federal government’s fiscal year, and the deadline for Congress to pass a funding measure. The debt ceiling, which is the amount of money lawmakers authorize the Treasury Department to borrow, must be suspended or raised by Oct. 18, according to Treasury Secretary Janet Yellen, or the U.S. likely will default on its debt.“ – MarketWatch

CBS took the “fear-mongering” to a whole new level with this statement:

“The U.S. economy could plunge into another recession this fall if Congress fails to lift the debt ceiling and the nation is unable to pay its obligations, according to an analysis by Moody’s Analytics chief economist Mark Zandi. The fallout would wipe out as many as 6 million jobs and erase $15 trillion in household wealth, he estimated in a report.”

While a remarkable statement to get “clicks,” even a cursory review of history suggests the hyperbole falls well short of reality.

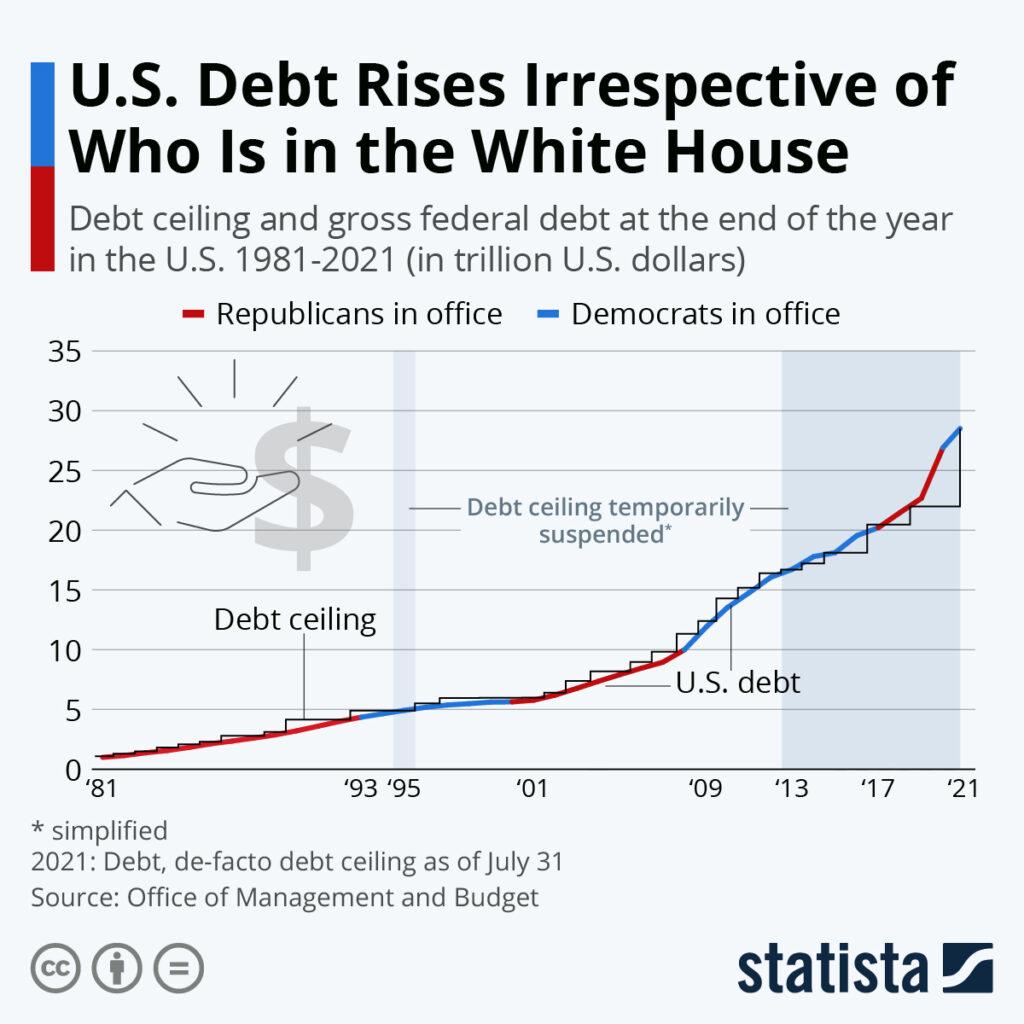

Both Parties Equally Responsible For Lifting The Debt Ceiling

Let’s start with an explanation of the “debt ceiling.”

“The debt ceiling is the legal limit on the total amount of federal debt the government can accrue. The limit applies to almost all federal debt, including the roughly $22.3 trillion of debt held by the public and the roughly $6.2 trillion the government owes itself as a result of borrowing from various government accounts, like the Social Security and Medicare trust funds. As a result, the debt continues to rise due to both annual budget deficits financed by borrowing from the public and from trust fund surpluses, which are invested in Treasury bills with the promise to be repaid later with interest.” – CRFB

The entire purpose for establishing a debt ceiling was to place a “credit limit” on the Government. In a responsible Government, as the debt ceiling approaches, members of Congress should begin discussing budget cuts, spending reductions, or revenue increases. The goal, logically, is to keep the country in a “surplus” position over time.

In 1980, that all changed, and seven administrations and four decades later, Government debt surged, deficits exploded, and the debt ceiling rose 78 times. (49 times under Republicans and 29 times under Democrats.)

Has The U.S. Ever Defaulted On Its Debt?

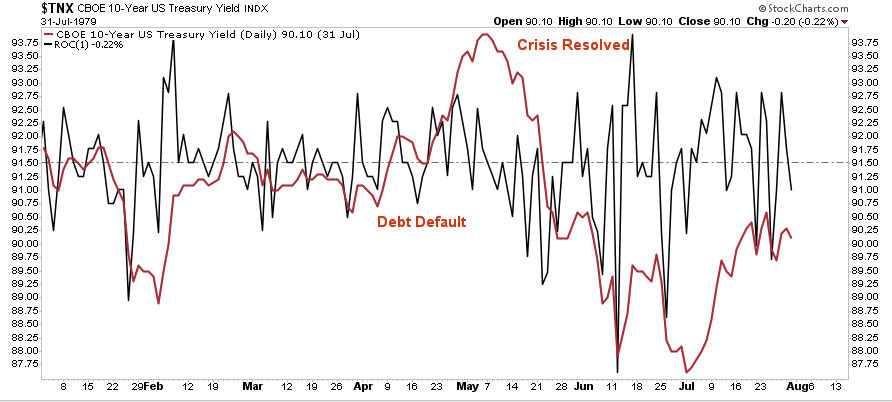

“Investors in T-bills maturing April 26, 1979, got told that the U.S. Treasury could not make its payments on maturing securities to individual investors. The Treasury was also late in redeeming T-bills which become due on May 3 and May 10, 1979. The Treasury blamed this delay on the failure of Congress to act in a timely fashion on the debt ceiling legislation in April. Also, an unanticipated failure of word processing equipment used to prepare check schedules contributed to the delay.” – The Financial Review

What the mainstream media missed, because “fear-mongering” attracts readers, is there are two types of default. The first is an actual default where the borrower cannot pay its debts due to a lack of capital.

The second is a “technical default.” In 1979, as noted, the Treasury was hung up over a “debt ceiling debate” and could not make interest payments. There was little worry by lenders over the safety or security of their capital. They knew that when the U.S. resolved the “technical issues,” the Government would make its payments.

Such is the “crisis” bond investors currently face.

-

Could there be a short-term delay in making interest payments? Absolutely.

-

Is there any risk of a default on the payment of interest or principal on outstanding Treasury bonds? Absolutely not.

As shown, 10-year rates did spike shortly over the initial concerns of the default. However, as soon as bondholders realized there was no continuing threat, they began to buy bonds at a discount to the previous value. Over the next couple of months, rates fell as sanity returned to the bond market. (Later that year, rates would rise again over legitimate concerns of the oil crisis.)

The Democrats Have All The Power To Solve The Problem

Despite all of the media narrative we noted previously; the Democrats did not need ANY Republican votes to:

-

LIft the debt ceiling

-

Fund the Government via “Continuing Resolution,” or “C.R.”

-

Pass the $3.5 Trillion spending bill.

The Democrats did what we expected on Thursday and passed a “clean Continuing Resolution” to fund the government until December 3rd.

U.S. House, in 254-175 vote, OKed the Senate-passed continuing resolution (“CR”) to extend government funding to Dec. 3 and avert a partial shutdown. Also includes billions for disaster aid and Afghan evacuation & resettlement. Biden’s signature next.

D 220-0, R 34-175

— Greg Giroux (@greggiroux) September 30, 2021

The problem for the Democrats in separating the Continuing Resolution from the debt ceiling is they lost any leverage to force a bipartisan debt vote to suspend the debt limit. Such puts the Democrats in a precarious position. With no bipartisan support, the Democrats will own the entirety of the debt increases in the upcoming mid-term elections. Such could be very problematic for representatives from more moderate “purple” states like Virginia and Georgia. As a result, even progressive Democrats are pushing back on Biden and Pelosi’s “runaway” spending plans.

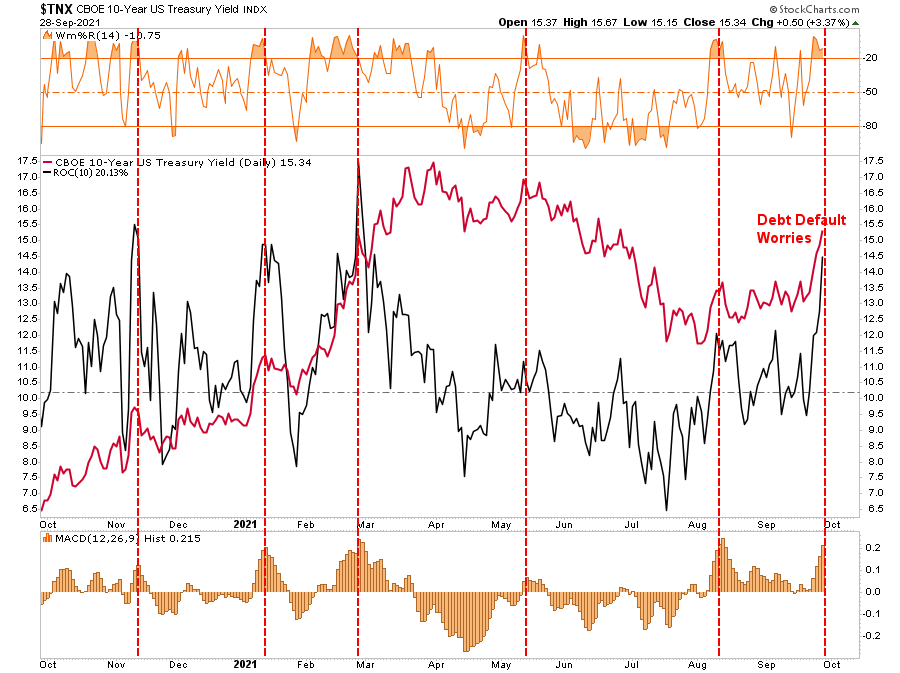

As noted above, it is not surprising to see Treasury yields rising once again. However, the current rate of change in rates is not historically dramatic and well within the context of what one would expect.

Debt Ceiling Crisis Redux

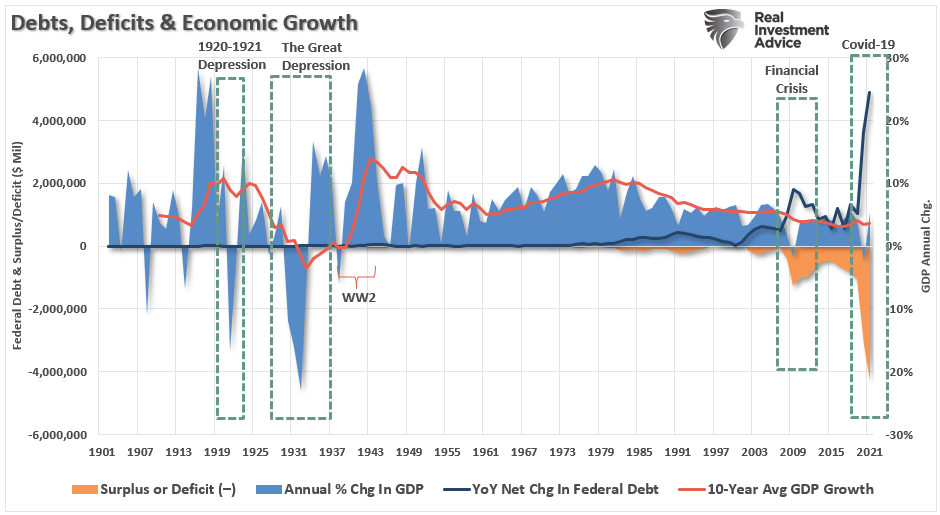

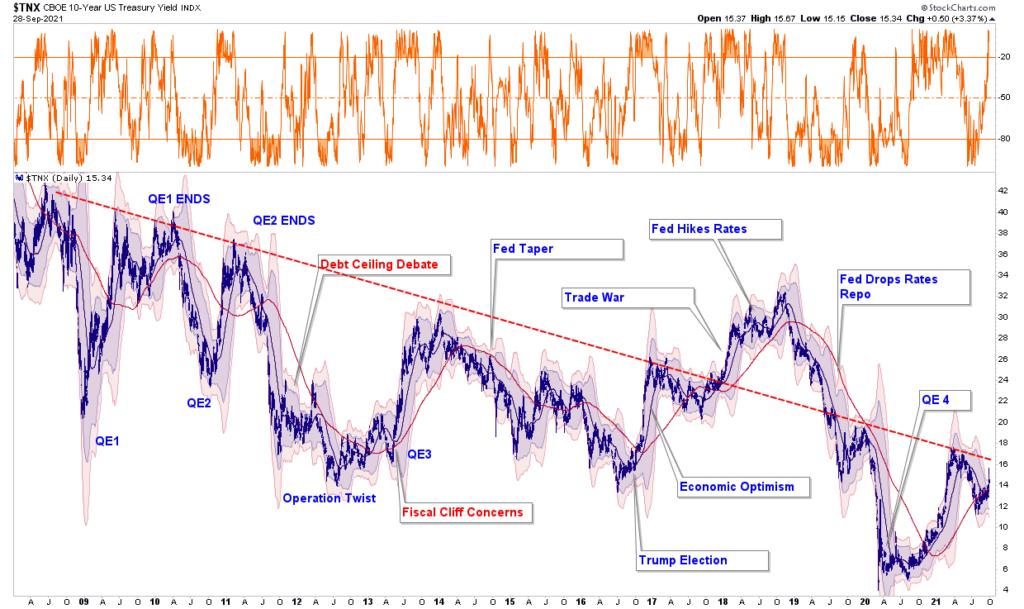

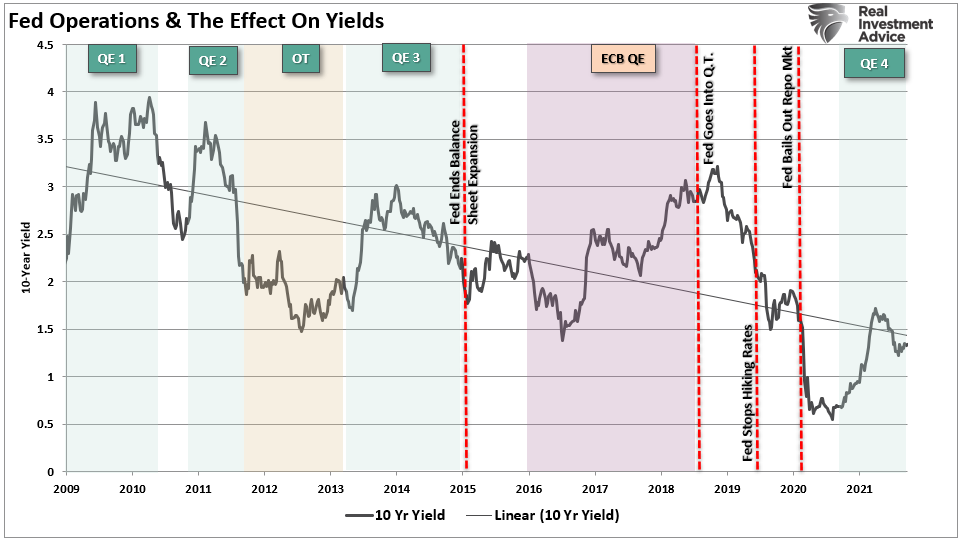

As Congress lifts the debt ceiling for the 79th time, the runaway spending and deficit increases continue to accelerate. The consequence of increasing debts and deficits is evident in the declining economic growth rates over the past 40-years.

During the last 12-years, a debt ceiling fight is an annual event between policymakers. The most prominent of which was in 2011 that led to a comprise to cut $1 trillion in spending. At that time, Ben Bernake launched the third round of Quantitative Easing to compensate for what was feared to be a “fiscal cliff” in 2013. Such was due to spending cuts getting automatically imposed.

As shown, rates spiked during the “debt ceiling crisis” as concerns over default rose. Subsequently, rates fell to new lows as deficits surged and economic growth slowed. Rates initially jumped over concerns of spending cuts, but the massive amount of QE injected into the system fueled stocks into overdrive, and yields collapsed.

Why Now Is Likely A Great Bond Buying Opportunity

There are several vital points evident from reviewing history.

-

While politicians talk a tough game, the current debate over the debt ceiling is nothing more than political posturing.

-

The media is a primary source of misinformation over the debt ceiling and potential outcomes.

-

Bond investors should be welcoming the debt ceiling debate as an opportunity to buy bonds at cheaper prices with higher yields.

Are there currently risks to the bond market that investors should be concerned about near term? Yes. The current spike in inflation will likely last longer than expected due to the break of supply lines. Furthermore, rates tend to rise when the Fed begins to discuss “tapering” their bond purchases as they are doing now.

However, both of these issues will resolve themselves going forward. Eventually, the supply chain disruption will mend, and inflation will decline as supply comes back online.

More importantly, when the Fed does begin the process of “tapering” their bond purchases, yields historically fall as investor’s “risk-preference” shifts from “risk-on” to “risk-off.”

As if always the case with investing, timing, as they say, is everything.

Such is why, with interest rates at more extreme overbought levels, we are looking for our next opportunity to add duration to our bond portfolios. Moreover, with the equity market grossly overvalued, we suspect that bonds will provide a chunk of our capital gains over the next couple of years.

There is little upside to the equity market. However, when the next recession approaches, yields will once again likely approach zero.

Got bonds?

Tyler Durden

Fri, 10/01/2021 – 15:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com