Is A Volatility Storm Coming?

Authored by Patrick Hill via RealInvestmentAdvice.com,

“Volatility often refers to the amount of uncertainty or risk related to the size of changes in a security’s value. A higher volatility means that a security’s value can potentially be spread out over a larger range of values. This means that the price of the security can change dramatically over a short time period in either direction.” – Investopedia

Federal Reserve Bond Tapering & Interest Rate Hikes Reduce Liquidity

Federal Reserve liquidity injections have bailed out the economy and equity markets for the last 18 months. And as a result, the bailout created a relatively low volatility environment for equity and bond markets. Will the announced withdrawal of Fed injections of $120B per month set up the monetary system for higher volatility? We see major economic forces combining in the intermediate future to create a possible ‘volatility storm’ driving valuations down. These economic forces include:

-

Fed tapering

-

Interest rate hikes

-

Inflation

-

Labor wage increases.

One of these macro factors is a challenge for monetary policymakers to mitigate damage to the financial system. But, a combination of these factors already building may overwhelm the monetary system. Further, markets are at historic high valuations today. But, market weaknesses and structure, along with valuations may create optimal conditions for a volatility storm.

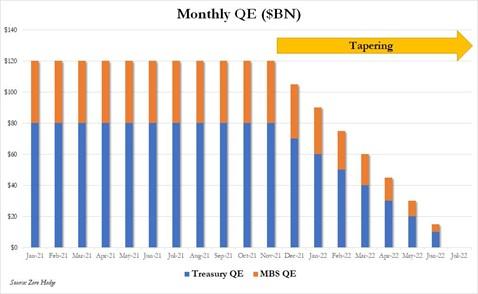

Taper Is Coming

In September, the minutes of the September Federal Open Market Committee meeting noted that most participants agreed that tapering of treasury and mortgage bond purchases should begin in December, but analysts expect a formal announcement at the November Fed meeting. Accordingly, here is a forecast of how the projected tapering may occur into mid – June 2022.

Sources: Zero Hedge, Real Investment Advice – 10/15/21

The financial markets enjoyed about $2.16T in liquidity injections resulting in a low volatility monetary environment for the S&P 500 to bull market from a March 2020 low of 2191 to 4471. The impact of tapering is both real and psychological. However, some analysts argue that the real reduction in bond purchases will have a minimal effect on bond markets. Others note that while the actual withdrawal of treasury bond purchases in the $21.9T treasury market is small, the psychological aspects of tapering are significant. Investors will feel the Federal Reserve is not ‘covering their downside risk’ anymore.

Some economists see an increase in volatility due to the end of bond purchases and increasing interest rates. On Fox News, October 17th, Mohammed El-Erian, Chief Economic Advisor at Allianz SE, said he sees increased volatility in the future.

“I worry…that this wonderful world we’ve been living in of low volatility, everything going up, may come to a stop with higher volatility. If I were an investor, I would recognize that I’m riding a huge liquidity wave thanks to the Fed, but I would remember that waves tend to break at some point, so I would be very attentive.”

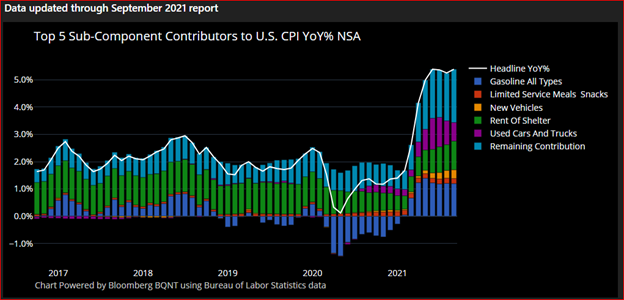

Inflation Surges to Decade Highs

The Consumer Price Index, CPI has moved above 5% on a year-over-year basis and it continues to rise. Housing rent prices are up by 17.9%, according to the Case – Shiller housing September index. Rent increases lead owner equivalent rent housing costs by five months based on a model by Macrobond and Nordea. This means that the 14% jump in existing home prices YoY is likely to extend into next year. Below is a chart of the CPI since 2017 and major components such as housing and gasoline.

Sources: Bloomberg, Bureau of Labor Statistics – 10/13/21

The record prices of key commodities continue to drive the price of manufactured goods higher. Oil prices settled at $85 per barrel, a three-year high on October 15th. Aluminum prices have increased by 40% in the last year. The metal price hit a 13 year high on the London Metal Exchange on October 15th as well. Copper prices surged by12% in the last week to the highest price since May 12th with a 74 year low in inventories. Demand for primary metals has soared due to power generation demand and the shift to green power infrastructure systems. If passed, the $1T Bipartisan Infrastructure Bill agreed upon in Congress will likely keep commodities prices high for a couple of years.

China Boosting Demand

Plus, China continues to make considerable investments in manufacturing and power generation projects keeping global demand high for commodities. Container shipping of commodities adds to their price. Container shipping rates from Shanghai to Los Angeles have increased by ten times in the last year. Computer chip shortages continue with the highest delays on record in chip shipments for September and auto manufacturers have reduced production on some models by 10 – 20% reducing car inventories at dealers and supporting high new and used car prices. Mitigating the surge in inflation would be declining consumer sentiment and buying, plus a possible slowdown in the global economy. Yet, wages may continue to climb, causing businesses to respond with price increases.

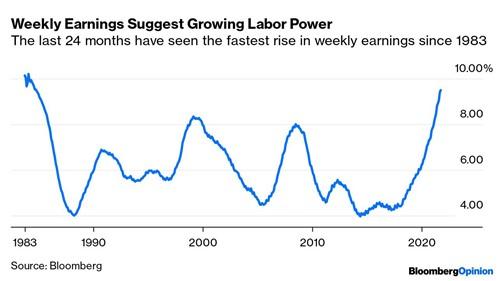

Increased Wages Drive Demand Inflation

Increases in wages will possibly sustain demand. Weekly earnings have soared to almost 10%. This chart shows weekly earnings back to 1983, the last time earnings increased at this high level.

Source: Bloomberg – 10/12/21

Worker earnings increases continue to be driven by a labor shortage. There are 4.3M jobs left to fill since the labor force participation rate high of February 2020. Critical factors in many jobs not being filled include: 3.6M retirees not returning to the labor force, lower-wage hospitality workers into higher-paying warehouse and delivery jobs, and 2.5M workers staying at home to care for Covid-19 relatives. The Wall Street Journal reports on October 14th the labor participation rate is at 61.6% versus 63.3% in February 2020. As a result, the labor force participation rate continues to be below pre-pandemic levels.

Sources: Labor Department, The Wall Street Journal – 10/14/21

Labor Shortages Aren’t Helping

The National Federation of Independent Businesses recently reported that their Hard Jobs to Fill indicator shows that wages are likely to continue to soar. The following chart shows how the labor shortage is fueling a rise in wages.

Sources: NFIB, The Daily Shot 10/12/21

In many industries, the labor shortage is forcing employers to hire key employees away from competitors. Accordingly, employers report in tight markets such as software programming offering 20% hire-on bonuses. The restaurant industry’s average wage now stands above $15 per hour to attract workers in this 400% yearly worker churn sector. Further, recruiters report that some workers seeing a tight labor market are evaluating work-life balance choices. Also, drop-out workers in some cases are taking vacations, pursuing hobbies, or just taking a break. Remote work-from-home options will continue to create tighter labor conditions for the foreseeable future. A September Wall Street Journal survey of 52 economists showed that 42% expect the economy to not recover to pre-pandemic workforce levels for years to come.

Next, let’s look at how weaknesses in the market can provide clues on a gathering volatility storm.

Monthly, Weekly Time Frames Show Bearish Market Direction

Brett Freeze, principal at Global Technical Analysis (GTA), uses a unique set of time frames matched with trend models to identify support and resistance levels. Markets behave in different ways based on different time periods and participants. For example, institutional investors tend to make long-term investments quarterly. GTA analysis reports on quarterly, monthly, weekly, and daily trends. The following chart shows ES futures contract prices are below Monthly and Weekly Trends. The model notes a one period or two-period move as below trend. When ES future prices make three consecutive period moves, a trend is indicated for that timeframe.

Source: Brett Freeze, Global Technical Analysis – 10/15/21

Note: PQH = Previous Quarter High, PQL = Previous Quarter Low, PMH = Previous Month High, PML = Previous Month Low, PWH = Previous Weekly High, PML = Previous Weekly Low, PDH = Previous Daily High, PDL = Previous Daily Low

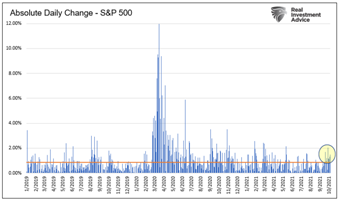

Realized Volatility Is Relatively Low, Yet Implied Volatility Is Rising

Realized volatility is the change in price between the daily closes of a stock, ETF, or financial instrument. The following chart from Lance Roberts and CNBC shows how price changes in the S&P 500 have been above average but are still within a 2% daily range since the March 2020 SPX lows.

Source: Real Investment Advice – 10/6/21

Realized volatility shows how market participants are actually driving market price swings by direct trading. The limited movement of realized volatility obscures the impact of implied volatility of markets.

Implied Volatility

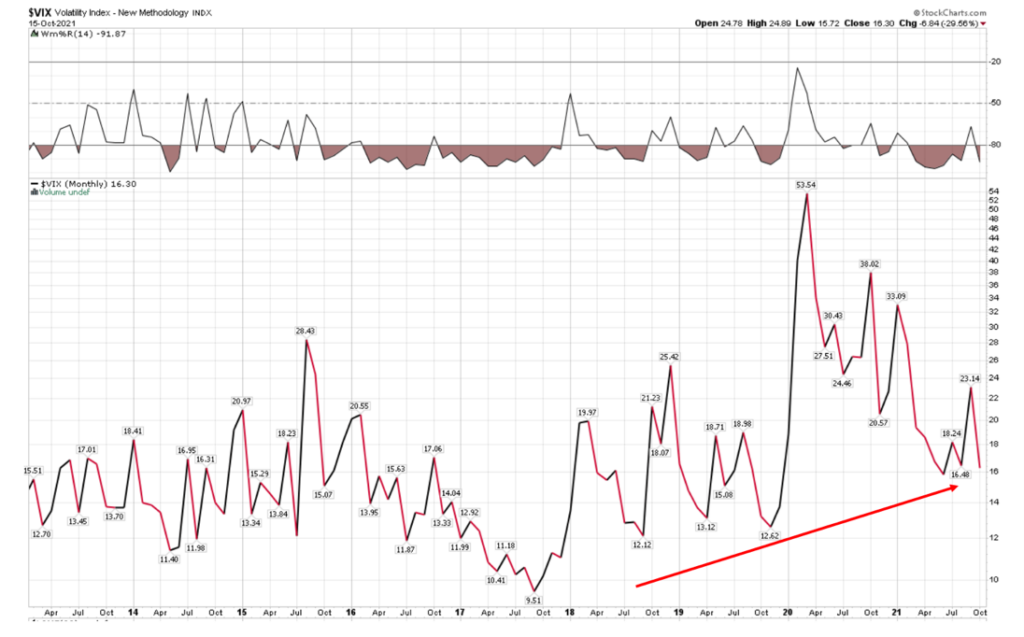

Implied volatility is the range of prices based on speculation of where a price may be for underlying security or index at a specific date. Overall implied volatility has been climbing the past few years. The Volatility Index (VIX) is an indicator of implied volatility. The Chicago Board Options Exchange developed the VIX as a real-time index representing market expectations for the relative strength of near-term price changes of the S&P 500 index (SPX). It is calculated based on the ratio of puts (an option to sell underlying security) to calls (an option to buy underlying security) for near-term (30 days or less) options contracts.

VIX – Bullish or Bearish?

The lower the VIX index and the more calls to puts is considered bullish. Conversely, the more puts to calls driving and higher VIX is deemed to be bearish. The VIX uses put and call options set at specific strike price levels that traders speculate the SPX maybe, not the actual SPX index value. The VIX is one gauge of market sentiment on the direction of prices for the SPX. Over the past several years, the baseline VIX has been climbing as the SPX has rallied. Higher lows indicate growing anxiety about high valuations. The following monthly chart shows the VIX levels since 2014 with higher lows (red arrow) as it spikes at market lows like March 2020.

Source: Patrick Hill – 10/16/21

The VIX reached a low of 9.51 in 2017 and today stands at 16.30 on October 15th as a rally continues. The VIX reached a high of 53.54 at the SPX March 2020 decline. It would seem with higher lows that a higher spike is possible. Daily options market volume as of September is higher than the volume of underlying stocks. This means that speculation on where the SPX level will be is overtaking market flows.

Options Levels Point to A Volatility Storm Zone – Below 4400

Options analysts note last week’s bounce in S&P 500 Index is likely due to traders selling put options at monthly expiration, which crushed implied volatility. The VIX indicator fell to 16.80 from 20. Dealers began setting up ‘short volatility positions and buying calls supporting the rise in market prices. SPX levels of open interest in puts and calls identify where there may be support or resistance to prices.

The following chart shows a gamma pivot point at 4400. Gamma is the rate of change of the delta or sensitivity of the option price to a $1 change in the underlying stock price. It measures the rate at which dealers must adjust their hedged positions. Positive gamma is above 4400, where there are more calls than puts and traders are net-long options. As a stock price goes up, the dealer sells the stock and buys it as it goes down. Dealers dampen price changes in a positive gamma environment.

Conversely, when a dealer is net short options, they must hedge by selling the stock as it goes down and buying the stock as price rises triggering increased volatility. Today, 4400 is the pivot point between positive and negative gamma. Below 4300, we added a Volatility Zone where a volatility storm may build. The chart shows total open interest with puts below the zero line and calls above, with current expiration darkly shaded.

Sources: SpotGamma.com and Patrick Hill – 10/15/21

Watch out Below 4400

Brent Kochuba, a co-founder of SpotGamma, notes likely increased volatility below 4400,

” We currently see fairly light put positions below 4400. This implies that traders may need to purchase put options on a break of 4400, which could in turn force options dealers to short futures. This could lead to dealers shorting into a down market, which increases volatility.”

We have located where the volatility storm may develop. But, what factors might trigger a storm?

Factors Triggering a Volatility Storm

The critical triggering events will be Federal Reserve tapering and interest rate increases planned for 2022. The financial markets depend on high levels of liquidity, so any reduction in liquidity could act as a catalyst for a volatility storm. Other factors that may magnify a liquidity crunch include:

-

The debt ceiling not being raised in December

-

Options hedgers overreach and can’t cover margin positions, triggering forced selling

-

Inflation roaring further ahead beyond the Fed’s ability to control it, so the market loses confidence in the Fed

-

The Fed raises interest rates higher and faster than the market expects

-

Consumers quit spending, causing retail sales to drop, corporations sales fall, and stock buybacks end that were sustaining high market valuations

-

The economy goes into a recession as GDP drops, employment falls, and corporate valuations fall

-

Any black swan event like the pandemic

Any volatility storm as markets decline is likely to force analysts to shift from valuing stocks based on market speculation to actual GAAP earnings (not stock buyback inflated EPS), fundamentals, and related unused valuation tools. The TINA – ‘there is no alternative’ trading phenomenon would be over. Investors will need to be mindful of the extreme volatility posed by a volatility storm. Accordingly, wild rallies and steep falls will require portfolio managers to sharpen their hedging and volatility strategies to maintain portfolio value.

Tyler Durden

Thu, 10/21/2021 – 08:04![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com