Futures At All Time High On Evergrande Reprieve Despite Intel, Snapchat Collapse

S&P 500 futures traded to within 2 points of their September all time high, rising 0.12% to 4547, just shy of their 4549.5 record after China’s Evergrande unexpectedly made a last minute coupon payment, averting an imminent weekend default and boosting risk sentiment. But while spoos were up, Nasdaq futures edged -0.18% lower after Intel warned of lower profit margins, while Snap crashed 22%, leading declines among social media firms after flagging a hit to digital advertising from privacy changes by Apple. Intel plunged 10% in premarket trading as it missed third-quarter sales expectations, while its Chief Executive pointed to shortage of other chips holding back sales of the company’s flagship processors. 10Y yields dropped 2bps, the dollar slumped and bitcoin traded above $63,000. Fed Chair Powell is scheduled to speak at 11am ET.

The Chinese property giant’s bond-coupon payment has boosted sentiment because it reduces risks to the broader financial system, according to Pierre Veyret, technical analyst at ActivTrades. “However, this optimistic trading mood may be short-lived as investors’ biggest concern remains inflation,” he said. “Traders will listen intently to Jerome Powell today as the Fed chairman is expected to give more clues about monetary policy.”

Not everything was roses, however, and Facebook fell 3.7%, while Twitter lost 4.1% after Snap said privacy changes by Apple on iOS devices hurt the company’s ability to target and measure its digital advertising Snap plunged 20.9% on the news and cast doubts over quarterly reports next week from Facebook and Twitter, social media firms that rely heavily on advertising revenue.

Meanwhile supply chain worries, inflationary pressures and labor shortages have been at the center of third-quarter earnings season, with analysts expecting S&P 500 earnings to rise 33.7% year-on-year, according to Refinitiv data. Some analysts, however, said such worries will only have a temporary impact on earnings from mega-cap technology and communications companies this reporting season.

“Intel also produced less than stellar results. Shorting big-tech has been a good way to lose money in the past two years, and I expect only a temporary aberration,” wrote Jeffrey Halley, senior market analyst, Asia Pacific at OANDA in a client note. Elsewhere, Apple rose 0.2%. Other giga tech stocks including Tesla, Microsoft and Netflix also rose, limiting declines on Nasdaq 100 e-minis. Here are some more premarket movers:

- Mattel (MAT US) rose 6.7% after the firm known for its Barbie and Fisher-Price toys lifted its full-year guidance amid a sales rebound, even as it grapples with a global logistics crunch ahead of Christmas.

- Digital World Acquisition (DWAC US) jumped 67% after more than quadrupling on Thursday after news that the blank-check company would merge with former President Donald Trump’s media firm.

- Phunware (PHUN US) soared 288% as the company, which runs a mobile enterprise cloud platform, is plugged by retail traders on Reddit.

- Whirlpool (WHR US) fell 2% as the maker of refrigerators reported sales that fell short of Wall Street’s estimates, citing supply chain woes.

Investors were more upbeat about Europe, where consumer and tech companies led a 0.6% gain for the Stoxx 600 Index which headed for a third week of gains with cosmetics maker L’Oreal SA jumping more than 6% after reporting sales that were significantly higher than analysts expected. Euro Stoxx 50 and CAC gain over 1%, FTSE 100 and IBEX lag but hold in the green. Tech, household & personal goods and auto names are the strongest sectors. On the downside, French carmaker Renault SA and London Stock Exchange Group Plc were the latest companies to report supply-chain challenges. Here are some of the biggest European movers today:

- L’Oreal shares rise as much as 6.8% after its 3Q sales beat impresses analysts, with Citi praising the French beauty-product maker’s capacity to re-balance growth between different geographies at a time of worry over China. The stock posted its biggest gain in almost a year.

- Essity shares are the biggest gainers in the OMX Stockholm 30 large cap index after 3Q EPS beat consensus by 10%, with Jefferies citing lower financing costs as among reasons for the improved earnings.

- Thule shares rise as much as 6.7%, most since July 21, after the company reported earnings for the third quarter.

- Klepierre shares gain as much as 4.8%, hitting the highest since Sept. 30, after the French mall owner boosted its net current cash flow per share view amid an ongoing recovery in its markets and stronger-than- expected rent collection.

- Wise shares fell as much as 5.4% after co-founder Taavet Hinrikus sold a stake worth GBP81.5m in the digital-payments provider to invest in early-stage businesses.

- Boliden shares declined as much as 6.1%, most since May 2020, after 3Q earnings missed estimates.

- London Stock Exchange declines as much as 4.2% following third-quarter earnings, with Citi (neutral) describing the revenue mix as “marginally disappointing” amid underperformance in the data and analytics division.

- Shares in holding company Lifco fell as much as 8% after reporting disappointing sales numbers in its dental business, missing Kepler Cheuvreux’s revenue estimates by 18%.

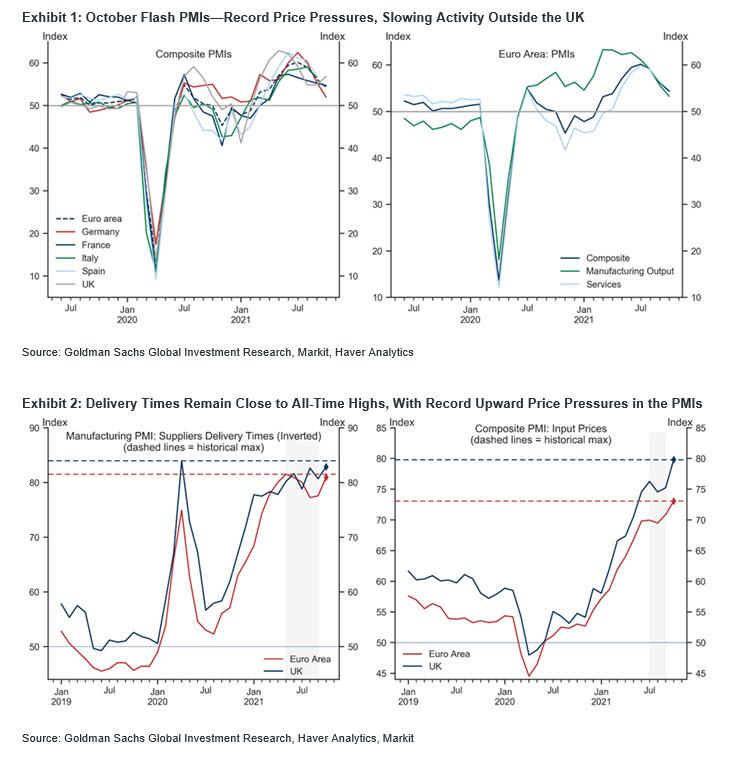

European stocks ignored the latest warning print from the continent’s PMIs, where the composite flash PMI declined by 1.9pt to 54.3 in October—well below consensus expectations—continuing the moderation from its July high. The area-wide softening was primarily led by Germany, although sequential momentum slowed elsewhere too. In the UK, on the heels of a succession of downside surprises, the composite PMI surprised significantly to the upside for the first time since May. Supply-side constraints continue to exert upward price pressures, with both input and output prices rising further and reaching new all-time highs across most of Europe.

- Euro Area Composite PMI (October, Flash): 54.3, GS 54.9, consensus 55.2, last 56.2.

- Euro Area Manufacturing PMI (October, Flash): 58.5, GS 57.1, consensus 57.1, last 58.6.

- Euro Area Services PMI (October, Flash): 54.7, GS 54.8, consensus 55.4, last 56.4.

- Germany Composite PMI (October, Flash): 52.0, GS 54.5, consensus 54.3, last 55.5.

- France Composite PMI (October, Flash): 54.7, GS 54.3, consensus 54.7, last 55.3.

- UK Composite PMI (October, Flash): 56.8, GS 53.6, consensus 54.0, last 54.9.

Earlier in the session, Asian equities climbed, led by China, as signs that Beijing may be easing its property policies and a bond interest payment by Evergrande boosted sentiment. The MSCI Asia Pacific Index rose 0.2%, on track to take its weekly advance to almost 1%. Chinese real estate stocks, including Seazen Group and Sunac China, were among the top gainers Friday, after Beijing called for support for first-home purchases, adding to recent official rhetoric on property market stability. China Evergrande Group pulled back from the brink of default by paying a bond coupon before this weekend’s deadline. The payment “brings some near-term reprieve ahead of its official default deadline and presents a more positive scenario than what many will have expect,” said Jun Rong Yeap, a market strategist at IG Asia Pte. The Asian measure was also bolstered by tech shares, including Japan’s Tokyo Electron and Tencent, while the Hang Seng Tech Index capped a 6.9% rise for the week in its biggest climb since August. The gains in the sector offset declines for mining shares as coal futures in China extended a price collapse to more than 20% in three days. Unlike in the U.S., where stocks are trading at a record high, Asian shares have been mixed in recent weeks as traders try to assess the impact on earnings of inflation, supply chain constraints and China’s growth slowdown. Falling earnings growth forecasts, combined with rising inflation expectations, are continuing to cast “a stagnation shadow over markets,” Kerry Craig, a global markets strategist at JPMorgan Asset Management, said in a note.

In rates, Treasuries resumed flattening with long-end yields richer by more than 2bp on the day, while 2-year yield breached 0.46% for the first time since March 2020, extending its third straight weekly increase. 2-year yields topped at 0.464% while 10-year retreated from Thursday’s five-month high 1.70% to ~1.685%, remaining higher on the week; 2s10s is flatter by 2.5bp, 5s30s by ~1bp. In 10-year sector bunds cheapen by 3.5bp vs Treasuries as German yield climbs to highest since May; EUR 5y5y inflation swap exceeds 2% for the first time since 2014. In Europe, yield curves were mixed: Germany bear-flattened with 10-year yields ~2bps cheaper near -0.07%.

Meanwhile, measures of inflation expectations continue to print new highs with EUR 5y5y inflation swaps hitting 2%, the highest since 2014, and U.K. 10y breakevens printing at a 25-year high.

In FX, AUD and NZD top the G-10 scoreboard. The Bloomberg dollar index Index fell and the greenback traded weaker against all its Group-of-10 peers apart from the pound; risk-sensitive Scandinavian and Antipodean currencies led gains. The pound inched lower after U.K retail sales fell unexpectedly for a fifth month as consumer confidence plunged, adding to evidence that the economic recovery is losing momentum. The cost of hedging against inflation in the U.K. over the next decade rose to the highest level in 25 years amid mounting concern over price pressures building in the economy. The Aussie dollar climbed as positive sentiment was boosted by the news about Evergrande Group’s bond payment; it had earlier fallen to a session low after the central bank announced an unscheduled bond-purchase operation to defend its yield target. The yen held steady following two days of gains as a rally in Treasuries narrows yield differentials between Japan and the U.S.

In commodities, crude futures recover off Asia’s worst levels, settling around the middle of this week’s trading range. WTI is 0.5% higher near $82.90, Brent regains a $85-handle. Spot gold adds ~$10 to trade near $1,792/oz. Most base metals trade well with LME nickel and zinc outperforming.

Looking at the day ahead, the main data highlight will be the aforementioned flash PMIs from around the world, on top of UK retail sales for September. From central banks, Fed Chair Powell will be speaking, in addition to the Fed’s Daly and the ECB’s Villeroy. Earnings releases will include Honeywell and American Express.

Market Snapshot

- S&P 500 futures little changed at 4,538.75

- STOXX Europe 600 up 0.4% to 471.82

- MXAP up 0.2% to 200.16

- MXAPJ up 0.2% to 661.40

- Nikkei up 0.3% to 28,804.85

- Topix little changed at 2,002.23

- Hang Seng Index up 0.4% to 26,126.93

- Shanghai Composite down 0.3% to 3,582.60

- Sensex down 0.2% to 60,775.00

- Australia S&P/ASX 200 little changed at 7,415.48

- Kospi little changed at 3,006.16

- Brent Futures up 0.2% to $84.81/bbl

- Gold spot up 0.5% to $1,792.58

- U.S. Dollar Index down 0.18% to 93.60

- Euro up 0.2% to $1.1645

Top Overnight News from Bloomberg

- The Bank of England will likely defy investors’ expectations of a sudden interest-rate increase next month because it rarely shifts policy in such dramatic fashion, according to three former senior officials.

- The ECB will supercharge its regular bond-buying program before pandemic purchases run out in March, according to economists surveyed by Bloomberg.

- Euro-area businesses are reporting a sharp slowdown in activity caused by an aggravating global supply squeeze that’s also producing record inflation. French manufacturing output declined at the steepest pace since coronavirus lockdowns were in place last year, while growth momentum deteriorated sharply in Germany, purchasing managers report. Private-sector activity in the euro area slowed to the weakest since April, though it remained above a pre-pandemic average.

- China continued to pull back on government spending in the third quarter even as the economy slowed, with the cautious fiscal policy reflecting the desire to deleverage and improve public finances.

- President Joe Biden said the U.S. was committed to defending Taiwan from a Chinese attack, in some of his strongest comments yet as the administration faces calls to clarify its stance on the democratically ruled island.

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets traded with a positive bias but with gains capped following the temperamental mood on Wall St amid mixed earnings results and although a late tailwind heading into the close lifted the S&P 500 to a record high and contributed to the outperformance of the NDX, futures were then pressured after hours as shares in Intel and Snap slumped post-earnings with the latter down as much as 25% on soft guidance which subsequently weighed on tech heavyweights including social media stocks such as Facebook and Twitter. ASX 200 (Unch.) was subdued amid weakness in mining names and financials but with downside cushioned after the recent reopening in Melbourne and with the RBA also conducting unscheduled purchases to defend the yield target for the first time since February. Nikkei 225 (+0.3%) recovered from opening losses with risk appetite at the whim of a choppy currency and with some encouragement heading into the easing of restrictions in Tokyo and Osaka from Monday. News headlines also provided a catalyst for individual stocks including Nissan which was subdued after it cut planned output by 30% through to November and with Toshiba pressured as merger talks between affiliate Kioxia and Western Digital stalled, while SoftBank enjoyed mild gains after a 13.5% increase in WeWork shares on its debut following a SPAC merger. Hang Seng (+0.4%) and Shanghai Comp. (-0.3%) traded, initially, with tentative gains after another respectable liquidity injection by the PBoC and news of Evergrande making the USD-bond interest payment to avert a default ahead of tomorrow’s grace period deadline. This lifted shares in Evergrande with attention now turning to another grace period deadline for next Friday, although regulatory concerns lingered after the PBoC stated that China will continue separating operations of banking, securities and insurance businesses, as well as signed an MOU with the HKMA on fintech supervision and cooperation in the Greater Bay area. Finally, 10yr JGBs were lower on spillover selling following a resumption a resumption of the curve flattening stateside where T-note futures tested the 130.00 level to the downside amid inflationary concerns and large supply from AerCap which launched the second largest IG dollar bond issuance so far this year. In addition, the gains in Japanese stocks and absence of BoJ purchases in the market today added to the lacklustre demand for JGBs, while today also saw the RBA announce unscheduled purchases valued at AUD 1bln to defend the yield target for the first time since February, although the impact on yields was only brief.

Top Asian News

- Tencent Blames WeChat Access for Search Engines on Loophole

- JPM’s Yang Joins Primas Asset Management’s Credit Trading Team

- Gold Rises on Weaker Dollar to Head for Second Weekly Gain

- Interest Payment Made; Junk Bonds Rally: Evergrande Update

A choppy start to the session has seen European equities extend on opening gains (Stoxx 600 +0.8%) with the Stoxx 600 on course to see the week out relatively unchanged. After a marginally positive lead from Asia, European stocks picked up after the cash open with little in the way of clear catalysts for the surge. Macro focus for the region has fallen on flash PMI readings for October which painted a mixed picture for the Eurozone economy as the EZ-wide services metric fell short of expectations whilst manufacturing exceeded forecasts. Despite printing north of the 50-mark, commentary from IHS Markit was relatively downbeat, noting that “After strong second and third quarter expansions, GDP growth is looking much weaker by comparison in the fourth quarter.” Stateside, futures are mixed with the ES relatively flat whilst the NQ (-0.3%) lags after shares in Intel and Snap slumped post-earnings with the latter down as much as 25% on soft guidance which subsequently weighed on tech heavyweights including social media stocks such as Facebook (-4% pre-market) and Twitter (-4.5% pre-market). Elsewhere in the US, traders are awaiting further updates in Capitol Hill, however, moderate Democrat Senator Manchin has already tempered expectations for a deal being reached by today’s goal set by Senate Majority Leader Schumer. Back to Europe, sectors are mostly firmer with outperformance in Personal & Household Goods following earnings from L’Oreal (+6.2%) who sit at the stop of the Stoxx 600 after Q3 earnings saw revenues exceed expectations. To the downside, Telecom names are lagging amid losses in Ericsson (-3.1%) after the DoJ stated that the Co. breached obligations under a Deferred Prosecution Agreement. Elsewhere, Vivendi (+3.1%) is another notable gainer in the region as Q3 earnings exceeded analyst estimates. LSE (-3.3%) sits at the foot of the FTSE 100 post-Q3 results, whilst IHG (-3.5%) is another laggard in the index post-earnings as the Co.’s fragile recovery continues.

Top European News

- U.K.-France Power Cable Has Unplanned Halt: National Grid

- Banks Prepare to Fight Basel Over Carbon Derivatives Rule

- Wise Slumps After Founder Hinrikus Offloads $112 Million Stake

- London Stock Exchange Says Supply Chains to Delay Tech Spend

In FX, the Greenback has topped out yet again, and partly in tandem with US Treasury yields following their latest ramp up, but also against the backdrop of improved risk appetite that emerged during APAC hours when reports that China’s Evergrande made an overdue interest payment helped to lift sentiment after a late tech-led downturn on Wall Street. The index may also have lost momentum on technical grounds following a minor extension to 93.792, but still not enough impetus to reach 94.000 or test a couple of resistance levels standing in the way of the nearest round number (Fib resistance at 93.884 and 21 DMA that comes in at 93.948 today compared to 93.917 on Thursday), and a fade just shy of yesterday’s best before the aforementioned drift back down to meander between a narrow 93.789-598 corridor. Ahead, Markit’s flash PMIs and a trio of Fed speakers including Williams, Daly and chair Powell feature on Friday’s agenda alongside today’s batch of earnings.

- AUD/NZD/CAD – Honours remain pretty even down under as the Aussie and Kiwi both take advantage of the constructive market tone that is weighing on their US counterpart, while assessing specifics such as RBA Governor Lowe reiterating no target rate for Aud/Usd, but the Bank having to intervene in defence of the 0.1% 3 year yield target for the first time in 8 months overnight in wake of upbeat preliminary PMIs. Meanwhile, NZ suffered another record number of new COVID-19 cases to justify PM Adern’s resolve to keep restrictions tight until 90% of the population have been vaccinated and keep Nzd/Usd capped under 0.7200 in mild contrast to Aud/Usd hovering just above 0.7500. Elsewhere, some traction for the Loonie in the run up to Canadian retail sales from a rebound in WTI to retest Usd 83/brl from recent sub-Usd 81 lows, as Usd/Cad retreats towards the bottom of a 1.2375-30 range.

- EUR/CHF/GBP/JPY – All marginally firmer or flat against the Dollar, but the Euro easing back into a lower band beneath 1.1650 and not really helped by conflicting flash PMIs or decent option expiry interest from 1.1610-00 (1.4 bn) that could exert a gravitational pull into the NY cut. The Franc is keeping afloat of 0.9300, but under 0.9250, the Pound has bounced to probe 1.3800 on the back of considerably stronger than expected UK prelim PMIs that have offset poor retail sales data and could persuade more of the BoE’s MPC to tilt hawkishly in November, especially after the new chief economist said the upcoming meeting is live and policy verdict finely balanced. Conversely, the BoJ is widely tipped to maintain accommodation next week and as forecast Japanese inflation readings will do little to change perceptions, putting greater emphasis on the Outlook Report for updated growth and core CPI projections and leaving the Yen tethered around 114.00 in the meantime.

- SCANDI/EM – The Sek and Nok are on a firm footing circa 9.9800 and 9.7000 against the Eur respectively, and the former may be acknowledging an upbeat Riksbank business survey, while the latter piggy-backs Brent’s recovery that is also underpinning the Rub in the run up to the CBR and anticipated 25 bp hike. The Cnh and Cny are back in the ascendency with extra PBoC liquidity and Evergrande evading a grace period deadline by one day to compensate for ongoing default risk at its main Hengda unit, but the Try is still trying in vain to stop the rot following Thursday’s shock 200 bp CBRT blanket rate cuts and has been down to almost 9.6600 vs the Usd.

In commodities, WTI and Brent are marginally firmer this morning though reside within overnight ranges and have been grinding higher for the duration of the European session in-spite of the lack of newsflow generally and for the complex. Currently, the benchmarks are firmer by circa USD 0.40/bbl respectively and reside just off best levels which saw a brief recapture of the USD 83/bbl and USD 85/bbl handles. Given the lack of updates, the complex remains attentive to COVID-19 concerns where officials out of China reiterated language issues yesterday about curbing unnecessary travel around Beijing following cases being reported in the region. Elsewhere, yesterday’s remarks from Putin continue to draw focus around OPEC+ increasing output more than agreed and once again reiterating that Russia can lift gas supplies to Europe; but, as of yet, there is no update on the situation. Finally, the morning’s European earnings were devoid of energy names, but updated Renault guidance is noteworthy on the fuel-demand front as the Co. cut its market forecast to Europe and anticipates a FY21 global vehicle loss of circa 500k units due to component shortages. Moving to metals, spot gold and silver are firmer but have been fairly steady throughout the session perhaps aided by the softer dollar while elevated yields are perhaps capping any upside. Base metals remain buoyed though LME copper continues to wane off the closely watched 10k mark.

US Event Calendar

- 9:45am: Oct. Markit US Composite PMI, prior 55.0

- 9:45am: Oct. Markit US Services PMI, est. 55.2, prior 54.9

- 9:45am: Oct. Markit US Manufacturing PMI, est. 60.5, prior 60.7

- 10am: Fed’s Daly Discusses the Fed and Climate Change Risk

- 11am: Powell Takes Part in a Policy Panel Discussion

DB’s Jim Reid concludes the overnight wrap

Hopefully today is my last Friday ever on crutches but with two likely knee replacements to come in the next few years I suspect not! 6 days to go until the 6 weeks of no weight bearing is over. I’m counting down the hours. Tomorrow I’ll be hobbling to London to see “Frozen: The Musical”. I’ve almost had to remortgage the house for 5 tickets. There is no discount for children which is a great business model if you can get away with it. Actually given the target audience there should be a discount for adults as I can think of better ways of spending a Saturday afternoon.

The weekends have recently been the place where the Bank of England shocks the market into pricing in imminent rate hikes. Well to give us all a break they’ve gone a couple of days early this week with new chief economist Huw Pill last night telling the FT that the November meeting was “live” and that with inflation was likely to rise “close to or even slightly above 5 per cent” early next year, which for a central bank with a 2% inflation target, is “a very uncomfortable place to be”. Having said that, he did add that “maybe there’s a bit too much excitement in the focus on rates right now” and also talked about how the transitory nature of inflation meant there was no need to go into a restrictive stance. So the market will probably firm up November hike probabilities today but may think 1-2 year pricing is a little aggressive for the moment. However, it’s been a volatile ride in short sterling contracts of late so we will see. Ultimately the BoE will be a hostage to events. If inflation remains stubbornly high they may have to become more hawkish as 2022 progresses.

This interview capped the end of a day with another selloff in sovereign bond markets as investors continued to ratchet up their expectations of future price growth. In fact by the close of trade, the 5yr US inflation breakeven had risen +10.0bps to 2.91%, and this morning they’re up another +3.5bps to 2.95%, which takes them to their highest level in the 20 years that TIPS have traded. 10y breakevens closed up +4.7bps at 2.65%, their highest level since 2011. Bear in mind that at the depths of the initial Covid crisis back in 2020, the 5yr measure fell to an intraday low of just 0.11%, so in the space of just over 18 months investors have gone from expecting borderline deflation over the next 5 years to a rate some way above the Fed’s target.

Those moves weren’t just confined to the US however, as longer-term inflation expectations moved higher in Europe too. The 10yr German breakeven rose +5.4bps to a post-2013 high of 1.87%, and its Italian counterpart hit a post-2011 high of 1.78%. And what’s noticeable as well is that these higher inflation expectations aren’t simply concentrated for the next few years of the time horizon, since the 5y5y inflation swaps that look at expectations for the five year period starting in five years’ time have also seen substantial increases. Most strikingly of all, the Euro Area 5y5y inflation swap is now at 1.95%, which puts it almost at the ECB’s 2% inflation target for the first time since 2014.

The global increase in inflation compensation drove nominal yields higher, with the yield on 10yr US Treasuries up +4.4bps yesterday to a 6-month high of 1.70%, as investors are now pricing in an initial hike from the Fed by the time of their July 2022 meeting. And in Europe there was a similar selloff, with yields on 10yr bunds (+2.4bps), OATs (+2.1bps) and BTPs (+2.7bps) all moving higher too. Interestingly though, the slide in sovereign bonds thanks to higher inflation compensation came in spite of the fact that commodity prices slid across the board, with energy, metal and agricultural prices all shifting lower, albeit in many cases from multi-year highs. Both Brent Crude (-1.41%) and WTI (-1.63%) oil prices fell by more than -1% for the first time in over two weeks, whilst the industrial bellwether of copper (-3.72%) had its worst daily performance since June.

Even with high inflation remaining on the agenda, US equities proved resilient with the S&P 500 (+0.30%) posting a 7th consecutive advance to hit an all-time high for the first time in 7 weeks. Consumer discretionary and retail stocks were the clear outperformer, in line with the broader reflationary sentiment. Other indices forged ahead too, with the NASDAQ (+0.62%) moving to just -1.04% beneath its own all-time record, whilst the FANG+ index (+1.11%) of megacap tech stocks climbed to a fresh record as well. In Europe the major indices were weaker with the STOXX 600 retreating ever so slightly, by -0.08%, but it still remains only -1.29% beneath its August record.

Looking ahead, the main theme today will be the release of the flash PMIs from around the world, which will give us an initial indication of how various economies have fared through the start of Q4. Obviously one of the biggest themes has been supply-chain disruptions throughout the world, so it’ll be interesting to see how these surface, but the composite PMIs over recent months had already been indicating slowing growth momentum across the major economies. Our European economists are expecting there’ll be a further decline in the Euro Area composite PMI to 55.1. Overnight we’ve already had some of those numbers out of Asia, which have showed a recovery from their September levels. Indeed, the Japanese service PMI rose to 50.7 (vs. 47.8 in Sep), which is the first 50+ reading since January 2020 before the pandemic began, whilst the composite PMI also moved back into expansionary territory at 50.7 for the first time since April. In Australia there was also a move back into expansion, with their composite PMI rising to 52.2 (vs. 46.0 in Sep), the first 50+ reading since June.

Elsewhere in Asia, equity markets have followed the US higher, with the Hang Seng (+0.92%), CSI (+0.87%), Hang Seng (+0.42%), KOSPI (+0.27%) and Shanghai Composite (+0.09%) all in the green. That also comes as Japan’s nationwide CPI reading moved up to +0.2% on a year-on-year basis, in line with expectations, which is the first time so far this year that annual price growth has been positive. In other news, we learnt from the state-backed Securities Times newspaper that Evergrande has avoided a default by making an $83.5m interest payment on a bond whose 30-day grace period was going to end this weekend. Separately, the state TV network CCTV said that 4 Covid cases had been reported in Beijing and an official said that they would be testing 34,700 people in a neighbourhood linked to those cases. Looking forward, equity futures are pointing to a somewhat slower start in the US, with those on the S&P 500 down -0.08%.

Turning to the pandemic, global cases have continued to shift higher in recent days, and here in the UK we had over 50k new cases reported yesterday for the first time since mid-July. New areas are moving to toughen up restrictions, with Moscow moving beyond the nationwide measures in Russia to close most shops and businesses from October 28 to November 7. In better news however, we got confirmation from Pfizer and BioNTech that their booster shot was 95.6% effective against symptomatic Covid in a trial of over 10,000 people.

Finally, there was some decent economic data on the US labour market, with the number of initial jobless claims in the week through October 16 coming in at 290k (vs. 297k expected). That’s the lowest they’ve been since the pandemic began and also sends the 4-week average down to a post-pandemic low of 319.75k. Alongside that, the continuing claims for the week through October 9 came down to 2.481m (vs. 2.548m expected). Otherwise, September’s existing home sales rose to an annualised rate of 6.29m (vs. 6.10m expected), and the Philadelphia Fed’s business outlook survey fell to 23.8 (vs. 25.0 expected).

To the day ahead now, and the main data highlight will be the aforementioned flash PMIs from around the world, on top of UK retail sales for September. From central banks, Fed Chair Powell will be speaking, in addition to the Fed’s Daly and the ECB’s Villeroy. Earnings releases will include Honeywell and American Express.

Tyler Durden

Fri, 10/22/2021 – 08:07![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com