Bond Market’s Historic Duration Ties Fed’s Hands

By Dan Wilchins, Bloomberg Markets Live reporter and commentator

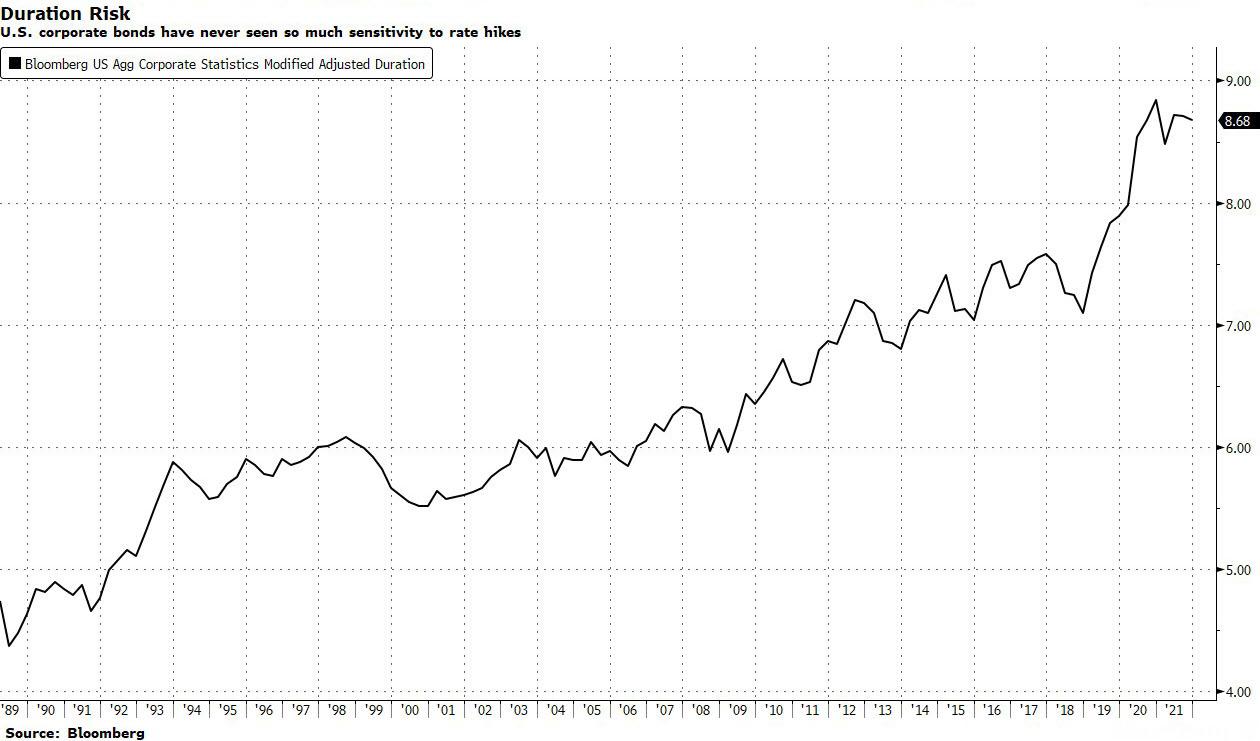

Bonds have never been so sensitive to rate changes, and the Federal Reserve may struggle to speed up tapering or raise rates much as a result.

The average duration, or price sensitivity to changes in rates, on a U.S. investment-grade corporate bond is close to all-time highs and spiked up from its level in 2019, according to Bloomberg index data. Same with Treasuries: the average duration is also near record highs.

When the Federal Reserve loosened the monetary spigots and made the extraordinary move to purchase corporate bonds last year, liquidity flooded capital markets and the cost of borrowing plummeted. Corporations took advantage and borrowed a record $1.75 trillion of investment-grade bonds, a third more than the previous peak.

While borrowers have been doing the right thing for themselves by locking in low yields for a long, long time, refinancing debt wherever possible, the flip side is that investors are holding more duration risk them ever. And that may come to haunt the markets if inflation doesn’t ease.

Whenever the Fed starts to tighten, bond prices could get slammed. Just look at what happened with 2013’s taper tantrum, except now duration is even longer, meaning price drops could be worse.

The potential for another taper tantrum may limit how aggressively the Fed chooses to tighten rates.

Tyler Durden

Wed, 11/17/2021 – 19:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com