Hyped-Inflation Versus The Coming Global Demographic Vortex

Most Central Banks are increasingly convinced high inflation rates might not be so transient after all. Which is why the tightening cycle has now begun. It’s worth reminding oneself that secular demographics are set to reach maximum deflationary pressure in the decade ahead. This is in stark contrast to the 1970s when demographic trends underpinned the then inflationary surge.

But amid the current inflation panic, Eric Basmajian of EPB Research reminds us that the demographic headwinds facing the major economies are intensifying (especially with people dropping out of the workforce). His great charts show deflation pressures are intense.

In the long-term, demographics will be a big shock to Central Banks hopes of higher inflation rates.

The Global Demographic Vortex

Executive Summary

-

All major economies are suffering from aging demographics.

-

An economy gets a boost from the 25-54-year-old age cohort and suffers a drag from the 65+-year-old age cohort.

-

Older populations are correlated to lower real growth and lower inflation.

-

With major economies already stuck at the zero-bound, fiscal and monetary authorities will have to contemplate negative interest rates or continued debt-financed fiscal spending.

-

Both options will not reverse economic gravity and erode the standard of living over time.

A rising tide lifts all boats. An economy receives a significant boost through the prime-age (25-54) population as this cohort has the highest rate of income and consumption. Prime-age workers buy more homes, vehicles, and durable goods, helping to boost production and employment.

Conversely, an economy feels a drag as older demographics (65+) comprise a larger share of the total population, particularly as modern economies are structured through heavy transfer payments in traditional retirement years. The older population rapidly slows consumption, downsizes home size, and is more able to leave the labor force, supported through Medicare and Social Security, at least in the United States.

The next 10-15 years will bring a significant demographic drag, not only in Japan, the poster-child for an aging population, but also in Europe, the United Kingdom, China, and the United States.

The global demographic vortex will act as a vacuum, sucking resources from the prime-age workers through taxation or debt-financed transfers, forcing central banks to hold rates at the zero-bound or quickly return after another failed attempt to combat rising inflation.

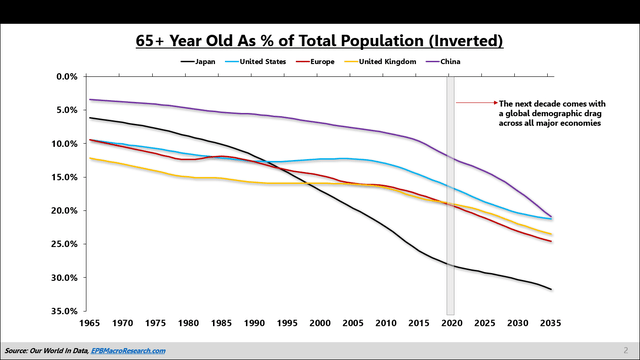

Demographic Drag

Charted below, we can see the aging population across major economies of the world. The 65+-year-old group as a percentage of the total population is rising (charted inversely) in the five largest economies.

Aging Demographics In All Major Economies:

Source: Our World In Data, EPB Macro Research

Despite popular opinion, Japan is not the only country that is suffering a demographic drag, and in fact, over the next ten years, the major economies of the world will mirror the problems that plagued Japan over the previous decades.

Aging Demographics In All Major Economies:

Source: Our World In Data, EPB Macro Research

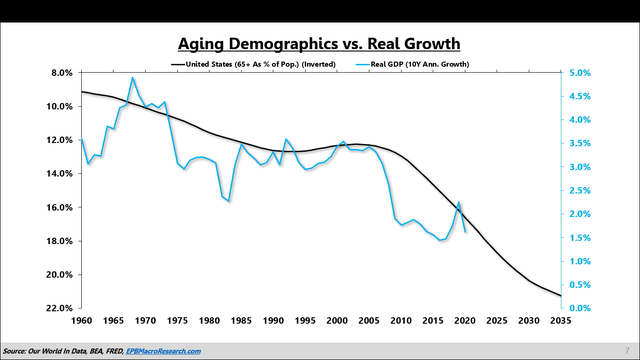

Many investors and economic analysts acknowledge aging demographics and the negative impact on growth and inflation but are relatively flippant about the importance. Like the analogy of a frog in boiling water, demographics have been impacting every major economy, contributing to sub-par economic growth over the last ten years, with investors and analysts offering dozens of explanations other than the most obvious and forceful economic fundamental.

The chart below shows the 10-year annualized rate of real GDP growth for the United States [blue] and the old-age population as a percentage of the total, graphed inversely [black].

Aging Demographics vs. Real GDP Growth:

Source: Our World In Data, BEA, FRED, EPB Macro Research

The demographic drag will not impact economic growth month to month or even year to year. Still, if you are willing to take a longer view, demographics are the most reliable economic fundamental impacting real growth, inflation, and thus, central bank policy and interest rates across the entire Treasury curve.

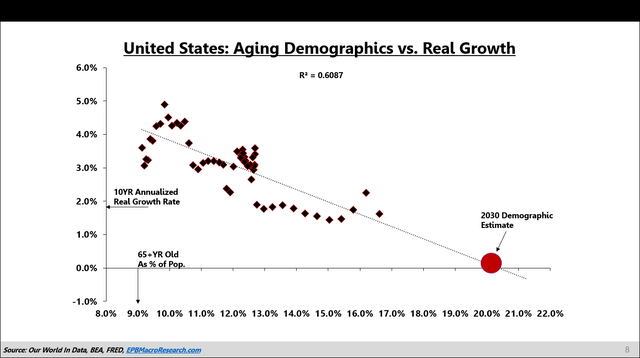

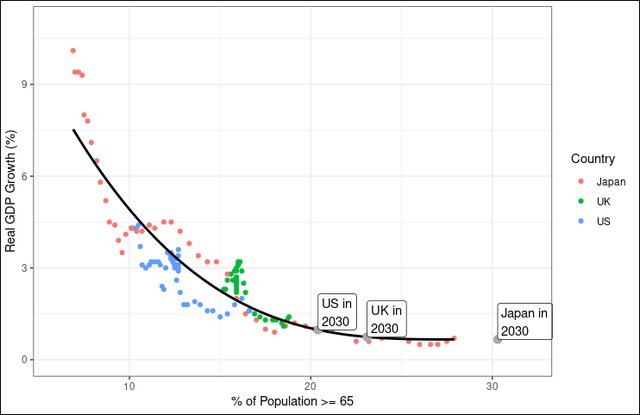

The relationship below shows the old-age population on the X-axis and the 10-year annualized rate of real growth on the Y-axis. The 2030 demographic estimate highlights how we should very much expect real economic growth to converge to 0% by the end of the decade.

Real Growth Will Converge To Zero:

Source: Our World In Data, BEA, FRED, EPB Macro Research

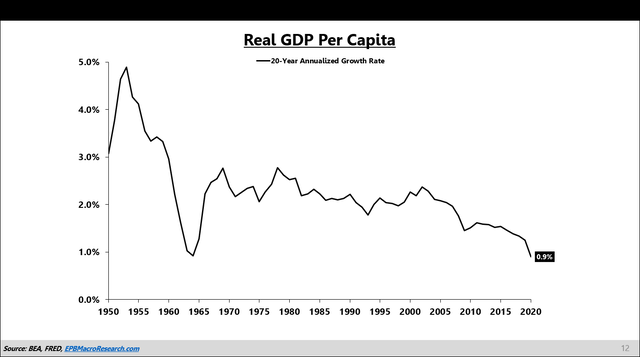

While this may sound extreme, investors that are more familiar with the long-term analysis at EPB Macro Research know that real GDP per capita growth is already rapidly converging towards zero despite unlimited central bank support and fiscal transfers.

Real GDP Per Capita: 20-Year Annualized Growth

Source: BEA, EPB Macro Research

As economic growth converges towards zero, the linear relationship between demographics and growth starts to level off. With the help of statistician Ian Fellows, we can plot the relationship between real GDP growth and the old-age population in Japan, the UK, and the United States.

Real Growth Will Converge To Zero:

Source: Our World In Data, BEA, FRED, Ian Fellows, EPB Macro Research

Aging demographics plaguing all five major economies of the world will suck real economic growth down towards zero, forcing central banks to the zero-bound if not already there and through the zero-bound for those willing to further the experiment of negative interest rates.

The recent surge in supply-side inflation is causing panic among global central banks, putting rate hikes back into the near-term equation. As with the last several attempts to “normalize” policy, there will be a quick U-turn back towards the zero-bound as economic gravity continues to pull the real growth rate to zero.

Demographics & Inflation

Demographics is also the most influential factor for inflation if you are willing to accept a longer time frame.

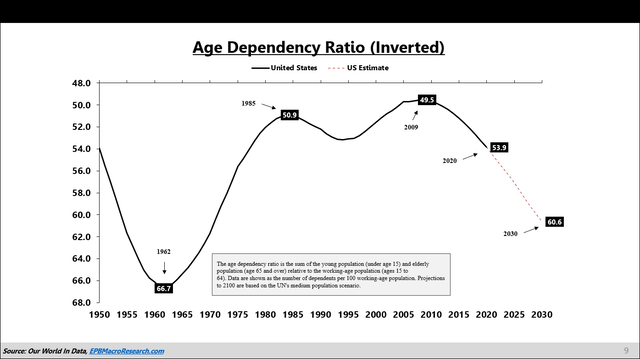

The age-dependency ratio is a measure that relates the “dependents” in the population to the working-age population.

The population 15-years and younger depend on parents for support, and the population 65-years and older, based on the way we have structured our system, also depends on the working-age population to produce goods, work, and generate income support retirement programs.

As a result, the age-dependency ratio graphed inversely in the chart below measures how much pressure there is on the working-age population to divert resources towards the young and old.

As the line is moving higher in the chart below, the working-age population is widening relative to the dependent population, creating robust economic conditions.

United States: Age Dependency Ratio

Source: Our World In Data, EPB Macro Research

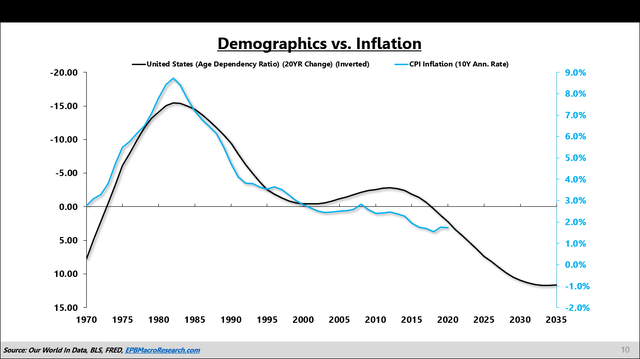

Particularly today, with inflation that resembles the 1970s, investors and analysts frantically remember what caused the 1970s inflation and the similarities to the current situation.

In reality, the situation today is much different as the 1970s inflation can be almost entirely explained by a demographic boom.

After the war, there was a “baby boom.” Fast forward 20 years, and those babies are now entering the prime-age cohort, ready to work, consume and produce. From 1960-1985, the United States experienced some of the most positive demographics the country has ever seen.

If we take the 20-year rolling change in the age-dependency ratio and plot it against the long-term (10Y) rate of inflation, we can see that almost all of the long-term inflation trends can be explained through demographics and a widening or contracting share of the working-age population.

United States: Change In Age Dependency Ratio Vs. Inflation

Source: Our World In Data, BLS, FRED, EPB Macro Research

Investors and analysts ignore demographics despite the clear relationships proving population trends to be the most reliable and forceful determinant of economic conditions.

Summary

Over the last ten years, sub-par economic growth and lackluster rates of inflation have confused policymakers and investors. A global demographic drag is at the heart of the problem.

The next decade will come with a global demographic drag that is far more intense than the last ten years across all major economies, not just Japan.

The rate of real economic growth will continue to slowly grind towards 0% and pull the long-term rate of inflation with it.

Fiscal policy will try and paper over this lost demand, aided by a close relationship with the central bank. Still, this debt-based strategy will only compound the problem, leaving the economy without any lasting growth and a rising debt burden, adding even more pressure to the global economy than the demographic drag alone.

Central banks will once again try an exercise of removing accommodation and raising interest rates to combat severe supply-side inflation, only to find that the structural economy is too weak, and a quick U-turn back towards the zero-floor will come if you are willing to take the multi-year view.

Debt-based fiscal spending will create short-term boosts to growth and inflation but with diminishing efficacy and increasing unintended consequences.

The long-term investor should be mindful of these trends and align their portfolio with assets that can survive another low-growth decade. Defensive assets like long-duration Treasury bonds are still effective at low levels of interest rates and one part of a diversified portfolio.

Some equities will benefit from low or no growth, particularly the companies that do have legitimate growth as growth that investors can find will continue to trade at a premium.

Companies that are sensitive to the real economy and aggregate economic growth will not benefit, so the overall equity market will become increasingly narrow in the decade ahead.

* * *

If you’re interested in regular updates on the shorter-term cyclical trends in both growth and inflation, consider our monthly report. If you’re interested in quarterly updates on the longer-term structural trends in both growth and inflation, consider our quarterly presentation. If you’d like access to both offerings, please contact me for a bundled rate.

Tyler Durden

Fri, 11/19/2021 – 19:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com