Fed “Taper” Is Good News For The Bond Market

Authored by Lance Roberts via RealInvestmentAdvice.com,

Investors are fretting over the prospect of a “Fed Taper,” but history shows such will likely be good news for the bond market. Currently, it doesn’t seem that way, with rates rising post-announcement. As noted by CNBC:

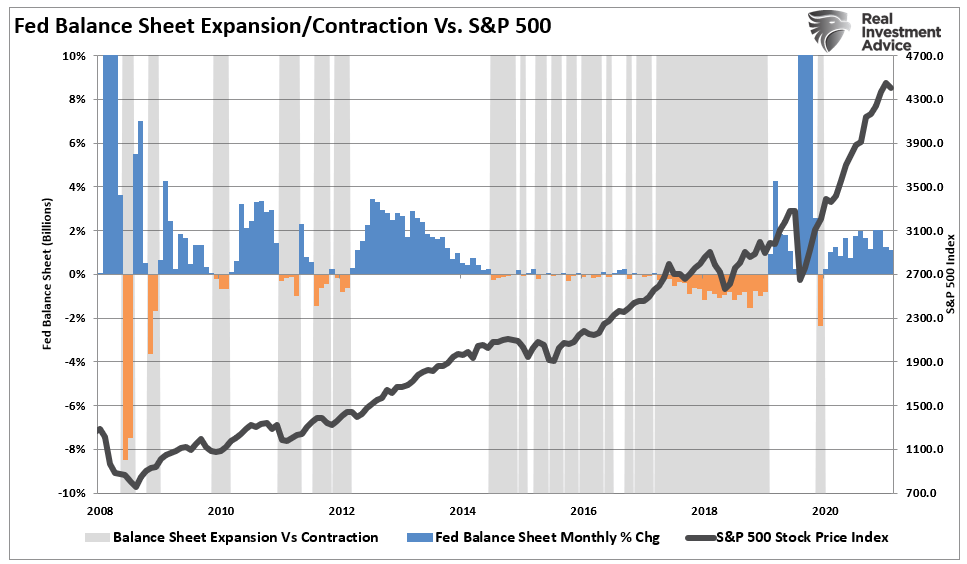

“While the Fed has gone into policy retreat before, it has never pulled back from such a dramatically accommodative position. For the past eighteen months, it bought at least $120 billion of bonds each month, Such provided unprecedented support to financial markets that it now will walk back.

The bond purchases have added more than $4 trillion to the Fed’s balance sheet which now stands at $8.5 trillion. Roughly, $7 trillion of which is the assets bought up through the Fed’s quantitative easing programs. The purchases helped keep interest rates low. Such provided support to markets that malfunctioned badly during the pandemic, and fueled a powerful run for the stock market.”

Previously, when the Fed began to taper their bond-buying programs, the market buckled as the “risk-on” trade reversed.

As was the case previously, Wall Street analysts quickly assumed that this time would be different despite the previous debacles.

“When Federal Reserve officials talked about pulling back on accommodative policies in 2013, anxious investors sent markets into a tizzy.

The opposite is happening now: The Fed signaled it started discussions of reducing bond-purchase programs. Investors, however, remain placid. The markets, in short, are taking everything in stride.” – WSJ

That is the case for now. Now let’s take a look at how the potential impact of the Fed’s announcement to taper may possibly be good news for the bond market.

Global Liquidity Is Slowing

While Wall Street is eternally optimistic, there are two problems with the view the Fed can cut liquidity without consequence.

To begin with, it isn’t just the Fed cutting liquidity. Liquidity globally, from both Central Banks and Governments, has started reversing heading into 2022.

*Global liquidity via central banks has already peaked and now in sharp decline ~ indicating world business conditions and growth to follow downwards

The rate of change is what matters – thus w/ liquidity in steep decline = increasing downside in economy (w/ a lag)

Deflationary pic.twitter.com/lbIeuvPGtC

— Adem Tumerkan (@RadicalAdem) September 23, 2021

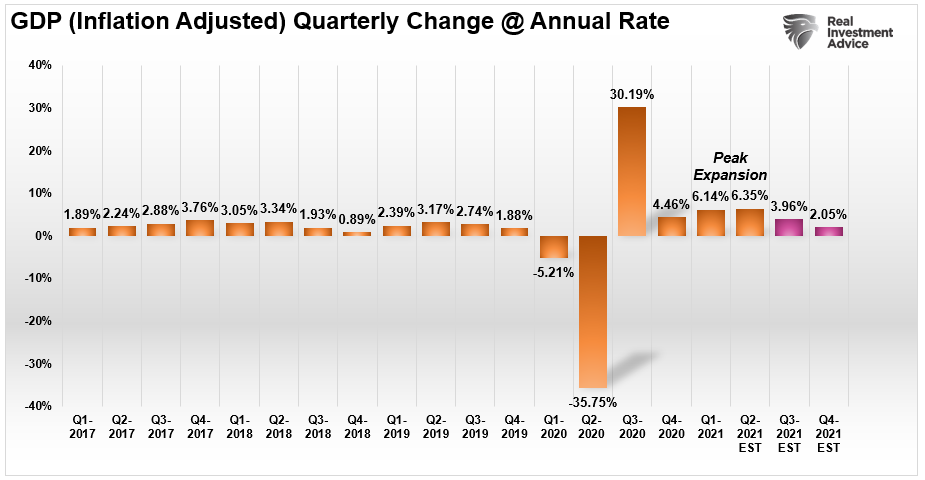

The hope, of course, is the economy is now strong enough to “stand on its own” without ongoing support. But, as discussed in “Reversion To The Mean,” economic growth is already falling well below expectations.

“Over the next few quarters, the year-over-year comparisons will become much more challenging. Q2-2021 will likely mark the peak of the economic recovery.“

During each previous QE cycle, as soon as the liquidity flows slowed or stopped, undesired outcomes were close by.

Awaken The Bond Bull

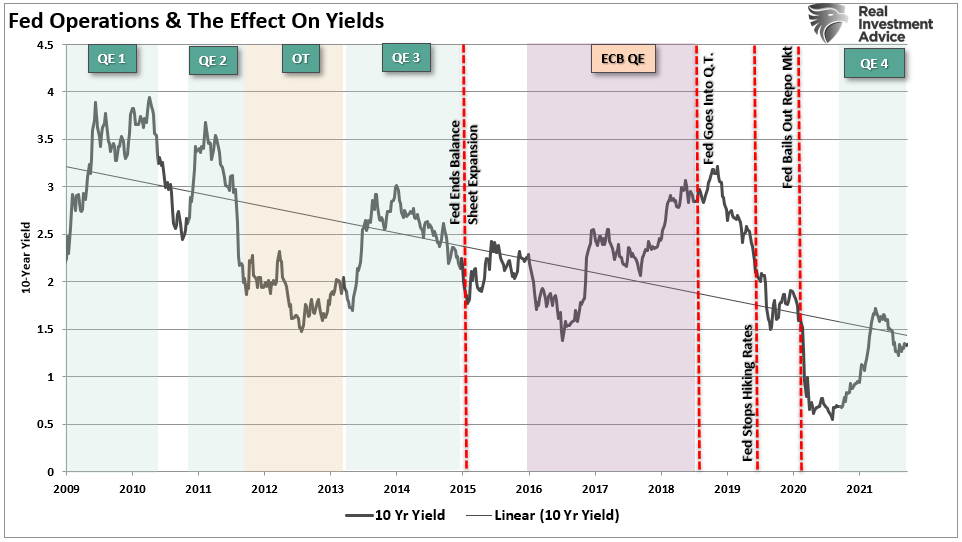

The recent “pop” in rates, when the Fed announced they will taper bond purchases, was not surprising. Such is the expectation if one of the primary sources of bond-buying is getting removed.

“In theory, tapering should lead to higher interest rates. By tapering its bond purchases, the Fed is increasing the supply that must get absorbed by the market. Such signals that policy is becoming less accommodative.” – Schwab

However, over the last decade, a reversal in Fed policy has repeatedly provided bond-buying opportunities. In the past, rates rose during QE programs as money rotated out of the “safety of bonds” back into equities (risk-on.).

When those programs ended, rates fell as investors reversed their risk preferences.

As the Fed begins tapers, investors’ risk preferences will change as liquidity wanes. There are three reasons such will be the case.

-

All interest rates are relative. With trillions in global debt globally sporting negative interest rates, the assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields in U.S. debt attracts flows of capital from countries with negative yields which push rates lower in the U.S.

-

The coming budget deficit balloon. Given the lack of fiscal policy controls, and promises of continued largesse, the budget deficit will swell beyond $4 Trillion in coming years. Such will require more government bond issuance to fund future expenditures.

-

Central Banks will continue to be a buyer of bonds to maintain market stability, but will become more aggressive buyers during each recession.”

With the current Administration and the Treasury pushing the idea of more government spending, the budget deficit is already rising, with economic growth running well below expectations. Such will foster more, not less, demand for bonds in the future and this is potentially good news for the bond market.

Bonds May Outperform

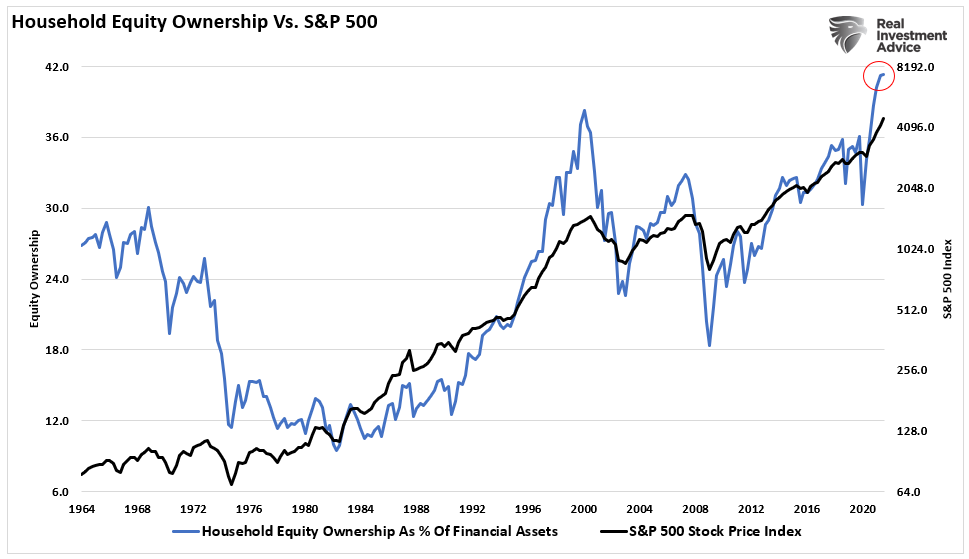

Here is the primary point. While market punditry continues to push a narrative that “stocks are the only game in town,” such will likely turn out to be poor advice. But that is the nature of a media-driven analysis with a lack of historical experience or perspective.

From many perspectives, the absolute risk of the heavy equity exposure in portfolios gets outweighed by the potential for further reward. The realization of “risk,” when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. Such is why we continue to acquire bonds on rallies in the markets to hedge against a future market dislocation.

In other words, we get paid to hedge risk, lower portfolio volatility, and protect capital. Bonds aren’t dead.In fact, they are likely going to be your best investment in the not too distant future.

In the short term, the market could surely rise further, especially if the Fed continues reinvesting the proceeds from their balance sheet. Such is a point I will not argue as investors are historically prone to chase returns until the very end. But over the intermediate to longer-term time frame, the consequences are entirely negative.

As my mom used to say:

“It’s all fun and games until someone gets their eye put out.”

Tyler Durden

Tue, 11/23/2021 – 06:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com