Jamie Dimon’s View Of Economic Reality Is Still Delusional

Authored by Lance Roberts via RealInvestmentAdvice.com,

“This is the most prosperous economy the world has ever seen and it’s going to be a very prosperous economy for the next 100 years.” – Jamie Dimon

That’s what the head of JP Morgan Chase told viewers in a recent “60-Minutes” interview.

“The consumer, which is 70% of the U.S. economy, is quite strong. Confidence is very high. Their balance sheets are in great shape. And you see that the strength of the American consumer is driving the American economy and the global economy. And while business slowed down, my current view is that, no, it just was a slowdown, not a petering out.” – Jamie Dimon

If you’re in the top 1-2% of income earners, like Jamie, I am sure it feels that way.

For everyone else, not so much.

This isn’t the first time that I have discussed Dimon’s distorted views, and just as we discussed then, even just marginally scratching the surface on the economy and the “household balance sheet,” reveals an uglier truth.

The Most Prosperous Economy

Let’s start with the “most prosperous economy in the world” claim.

As we recently discussed in “Socialism Rises,”

“How did a country which was once the shining beacon of ‘capitalism’ become a country on the brink of ‘socialism?’

Changes like these don’t happen in a vacuum. It is the result of years of a burgeoning divide between the wealthy and everyone else. It is also a function of a 40-year process of capitalism morphing an entire population into ‘debt slaves’ to sustain economic prosperity.

It is a myth that the economy has grown by roughly 5% since 1980. In reality, economic growth rates have been on a steady decline over the past 40 years, which has been supported by a massive push into deficit spending by consumers.”

With the slowest average annual growth rate in history, it is hard to suggest the economy has been the best it has ever been.

However, if an economy is truly prosperous it should benefit the majority of economic participants, which brings us to claim about “household balance sheet” health.

For Billionaires, The Grass Is Always Green

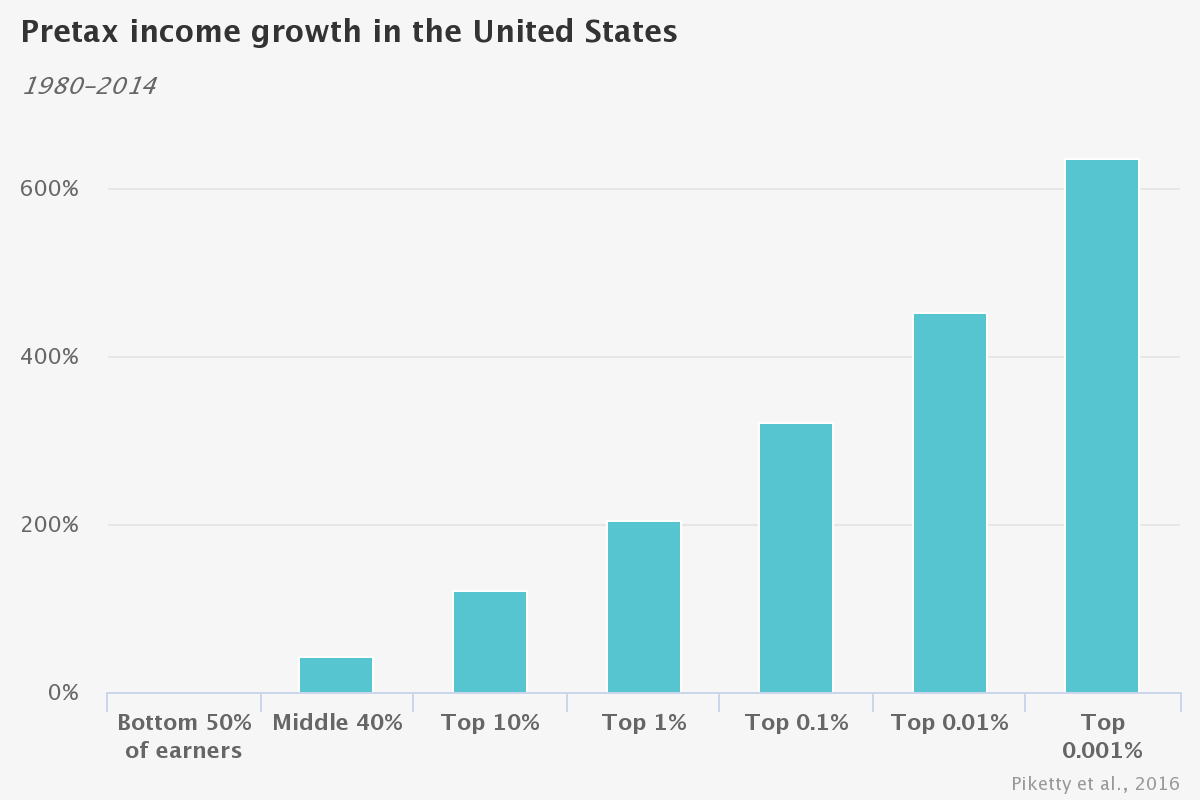

If you are in the upper 20% of income earners, not to mention the top .01% like Mr. Dimon, I am quite sure the “economic grass is very green.” If you are in the bottom 80%, the “view” is more akin to a “dirt lot.” Since 1980, as noted by a recent study from Chicago Booth Review, the wealth gap has progressively gotten worse.

“The data set reveals since 1980 a ‘sharp divergence in the growth experienced by the bottom 50 percent versus the rest of the economy,’ the researchers write. The average pretax income of the bottom 50 percent of US adults has stagnated since 1980, while the share of income of US adults in the bottom half of the distribution collapsed from 20 percent in 1980 to 12 percent in 2014. In a mirror-image move, the top 1 percent commanded 12 percent of income in 1980 but 20 percent in 2014. The top 1 percent of US adults now earns on average 81 times more than the bottom 50 percent of adults; in 1981, they earned 27 times what the lower half earned.“

The issue is the other 80% are just struggling to get by as recently discussed in the Wall Street Journal:

“The American middle class is falling deeper into debt to maintain a middle-class lifestyle.

Cars, college, houses and medical care have become steadily more costly, but incomes have been largely stagnant for two decades, despite a recent uptick. Filling the gap between earning and spending is an explosion of finance into nearly every corner of the consumer economy.

Consumer debt, not counting mortgages, has climbed to $4 trillion—higher than it has ever been even after adjusting for inflation. Mortgage debt slid after the financial crisis a decade ago but is rebounding.” – WSJ

The ability to simply “maintain a certain standard of living” has become problematic for many, which forces them further into debt.

“The debt surge is partly by design, a byproduct of low borrowing costs the Federal Reserve engineered after the financial crisis to get the economy moving. It has reshaped both borrowers and lenders. Consumers increasingly need it, companies increasingly can’t sell their goods without it, and the economy, which counts on consumer spending for more than two-thirds of GDP, would struggle without a plentiful supply of credit.” – WSJ

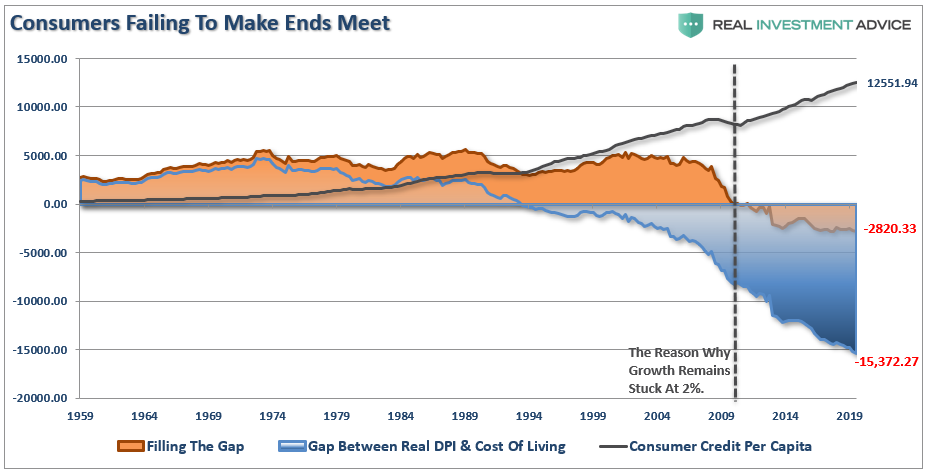

I show the “gap” between the “standard of living” and real disposable incomes below. Beginning in 1990, incomes alone were no longer able to meet the standard of living, so consumers turned to debt to fill the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $2600 annual deficit that cannot be filled. (Note: this deficit accrues every year which is why consumer credit keeps hitting new records.)

But this is where it gets interesting.

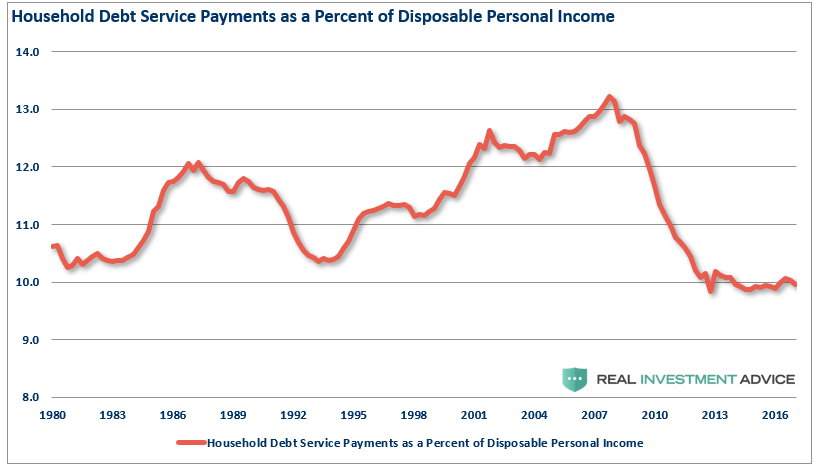

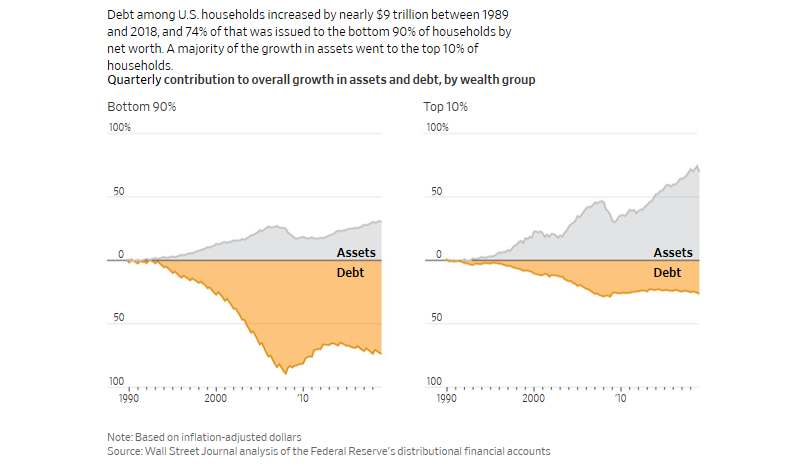

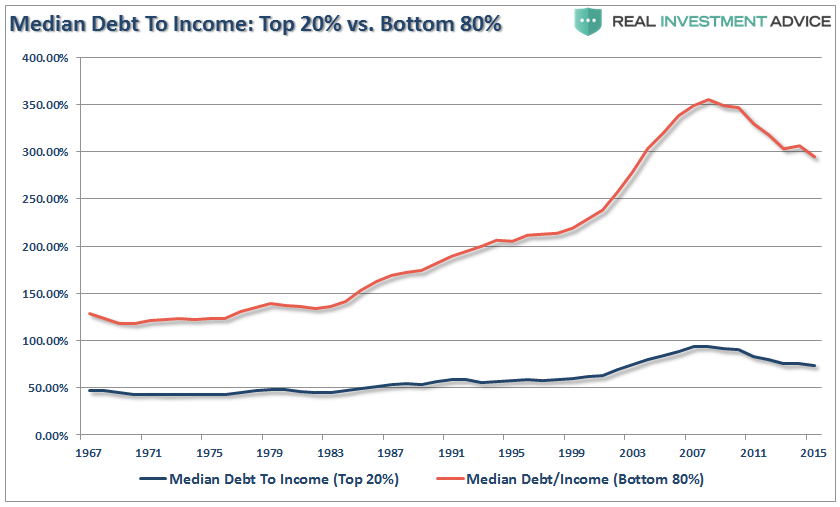

Mr. Dimon claims the “household balance sheet” is in great shape. However, this suggestion, which has been repeated by much of the mainstream media, is based on the following chart.

The problem with the chart is that it is an illusion created by the skew in disposable incomes by the top 20% of income earners, needless to say, the top 5%. The Wall Street Journal exposed this issue in their recent analysis.

“Median household income in the U.S. was $61,372 at the end of 2017, according to the Census Bureau. When inflation is taken into account, that is just above the 1999 level. Without adjusting for inflation, over the three decades through 2017, incomes are up 135%.” – WSJ

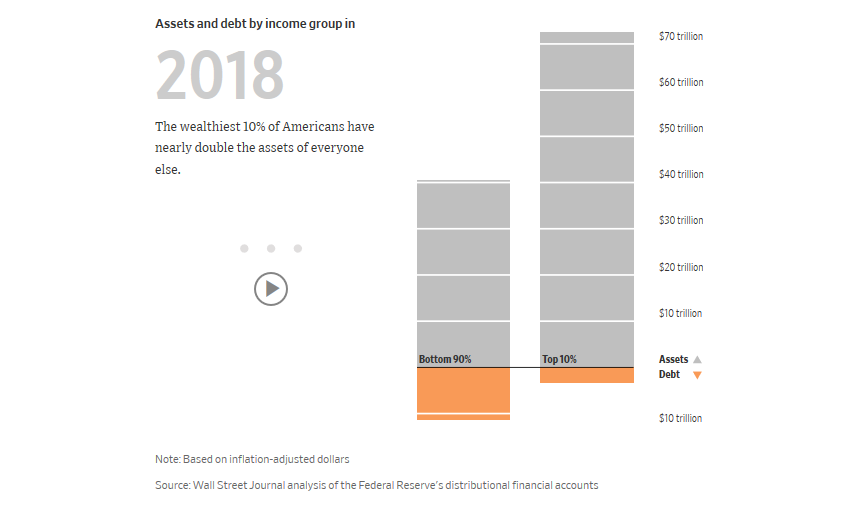

“The median net worth of households in the middle 20% of income rose 4% in inflation-adjusted terms to $81,900 between 1989 and 2016, the latest available data. For households in the top 20%, median net worth more than doubled to $811,860. And for the top 1%, the increase was 178% to $11,206,000.

Put differently, the value of assets for all U.S. households increased from 1989 through 2016 by an inflation-adjusted $58 trillion. A third of the gain—$19 trillion—went to the wealthiest 1%, according to a Journal analysis of Fed data.

‘On the surface things look pretty good, but if you dig a little deeper you see different subpopulations are not performing as well,’ said Cris deRitis, deputy chief economist at Moody’s Analytics.” – WSJ

With this understanding, we need to recalibrate the “debt to income” chart above to adjust for the bottom 80% of income earnings versus those in the top 20%. Clearly, the “household balance sheet” is not nearly as healthy as Mr. Dimon suggests.

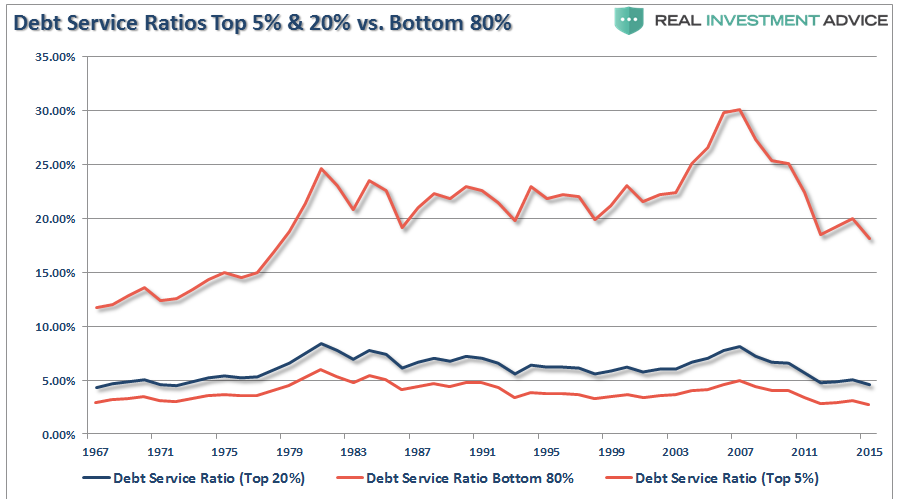

Of course, the only saving grace for many American households is that artificially low interest rates have reduced the average debt service levels. Unfortunately, those in the bottom 80% are still having a large chunk of their median disposable income eaten up by debt payments. This reduces discretionary spending capacity even further.

The problem is quite clear. With interest rates already at historic lows, the consumer already heavily leveraged, and wage growth stagnant, the capability to increase consumption to foster higher rates of economic growth is limited.

With respect to those who say “the debt doesn’t matter,” I respectfully argue that you looking at a very skewed view of the world driven by those at the top.

Mr. Dimon’s Last Call

What Mr. Dimon tends to forget is that it was the U.S. taxpayer who bailed out the financial system, him included, following the financial crisis. Despite massive fraud in the major banks related to the mortgage crisis, only small penalties were paid for their criminal acts, and no one went to jail. The top 5-banks which were 40% of the banking system prior to the financial crisis, became 60% afterwards. Through it all, Mr. Dimon became substantially wealthier, while the American population suffered the consequences.

Yes, “this is the greatest economy ever” if you are at the top of heap.

With household debt, corporate debt, and government debt now at records, the next crisis will once again require taxpayers to bail it out. Since it was Mr. Dimon’s bank that lent the money to zombie companies, households again which can’t afford it, and took on excessive risks in financial assets, he will gladly accept the next bailout while taxpayers suffer the fallout.

For the top 20% of the population that have money actually invested, or directly benefit from surging asset prices, like Mr. Dimon, life is great. However, for the vast majority of American’s, the job competition is high, wages growth is stagnant, and making “ends meet” is a daily challenge.

While Mr. Dimon’s view of America is certainly uplifting, it is delusional. But of course, give any person a billion dollars and they will likely become just as detached from economic realities.

Does America have “greatest hand ever dealt.”

The data certainly doesn’t suggest such. However, that can change.

We just have to stop hoping that we can magically cure a debt problem by adding more debt, and then shuffling it between Central Banks.

But then again, such a statement is also delusional.

Tyler Durden

Thu, 12/05/2019 – 09:44

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com