Rabobank: Don’t Dilly Dalio On The Way

By Michael Every of Rabobank

And don’t dilly Dalio on the way

“My old man, said be a [insert team name] fan; and I said, ‘I disagree, you’re a nasty person, and not in a relationship’” is the safe-for-work version of the classic British football-terrace song. The tune is of an original 1919 music hall number ‘And don’t dilly dally on the way’, which is about (“abaaat”) the hardships of working-class life. Indeed, the easier-to-understand-for-foreigners version, not the one my grandad sang to me, goes like this:

My old man said “Foller the van; and don’t dilly dally on the way”.

Off went the van wiv me ‘ome packed in it; I walked behind wiv me old cock linnet.

But I dillied and dallied, dallied and I dillied; Lost me way and don’t know where to roam.

Who’ll put you up when you’ve lost your bedstead; And you can’t find your way ‘ome?

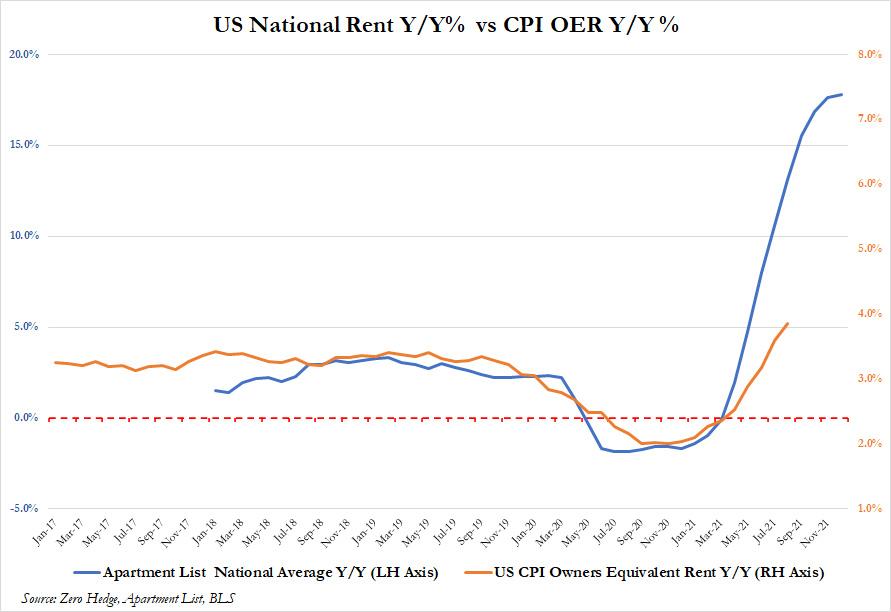

This song came to my mind as headline US CPI hit 7% y/y, the highest since 1982, and core CPI hit 5.5%. Moreover, when you look at the composition of the report, it is far higher for many than is being reported. The Owners’ Equivalent Rent component that makes up a huge chunk of the total index was up just 3.8% y/y at a time when Apartment List, with a mere 5m datapoints to draw from, suggests rents are actually up nearly 18% y/y, while CoreLogic said back in September rents were up 10.2% y/y. If anything like the Apartment List data were captured –which of course they won’t be– then headline CPI would be nearly 10% y/y.

The very beige Fed Beige Book will be seized on by optimists clinging to the view that 2022 will be like 2021, and “inflation will come down again in H2”. After all, it mentioned shortages somewhat less than in recent months, even as China shuts down again, port backlogs are longer, and Twitter suggests many shelves are barer. It also mentioned that pay continues to rise briskly, as do benefits in kind. Yes, this is playing catch-up; but it is also playing ketchup….pat, nothing, pat, nothing, pat, nothing…splurge. On one hand, that could be wage inflation into a supply-constrained US economy; or it could be a supply of goods into a demand-constrained economy. Either way, it isn’t a gradual decline back to a nice median 2% CPI forecast, sorry.

As such, governments are nervous. Quinnipiac has President Biden on 33% approval and 53% disapproval; CNN has 33% saying they trust him and 67% saying they don’t. These are numbers that political, and then policy, earthquakes are made of. There are even mutterings that Hillary Clinton might run again in 2024, while we can already assume Trump will: 2016 redux for markets to savour! You don’t want to hear what the British working class are singing about PM Boris in nightclubs or at darts matches, but he’s about as popular as Prince Andrew right now. Indeed, the Spectator sums up what even the right-of-center middle class now think of “BYO BoJo” apparently unable to recognize, or admit, he attended a 2021 boozy party of 100 people in Downing Street’s garden right after telling voters they could only meet one other person in theirs.

And if politicians are nervous, try central banks. Fed Chair Powell’s recent attempt to say he understands the pain of those hit by inflation he didn’t predict, and he’s a “diamond geezer” really, was about as believable as Dick Van Dyke’s Cawk-knee act in ‘Mary Poppins’ (which he gave an official apology for in 2017: we are still awaiting reparations). Further, when Powell says he can sort it out (“sortitaaat”) for said inflation-sufferers, he is as convincing as Keanu Reeves in ‘Dracula’, whose Mockney was by far the most diabolical thing in the whole film.

The same level of authenticity was evident in this week’s eulogy of China’s ‘common prosperity’ by Wall St’s instant-coffee table intellectual Ray Dalio. Wealth gaps need to be narrowed, says the billionaire; otherwise the US “empire” is over, added the US-based billionaire betting on both sides in what he claims is a battle for global hegemony. He’s completely right about the US; but he’s wrong that China is much better off in that regard, which is why they are embracing common prosperity! What Dalio also misses is that China is not seeing a shift to higher taxation or wealth redistribution, apart from pinpoint pounces on social media influencers and celebrities. Indeed, Beijing stresses that’s a route they don’t want to go down, and nor is embracing more state welfare spending.

This makes it unclear how the wealth gap *can* be narrowed except via more upmarket mercantilism, asset prices collapses (“houses are for living in, not speculation” is Beijing sentiment that would win LOTS of votes in the US and UK), or ‘donations’ to social causes. As such, Dalio is free to donate parts of his fortune to the state, like Chinese billionaires. He is free to avoid the “barbaric” growth of private capital by making bad investments and watching wealth gaps narrow that way: “This time next year, Rodney, we’ll [only] be millionaires.” And he is free to prioritize strategic capital investment in the US, not China, to help shift to upmarket mercantilism. But I bet he dilly Dalios on the way, and then dilly doesn’t.

This underlines a point I have been making for longer than some billionaires have been eulogizing China. All we hear in market media replete with ads for designer lifestyle goods today is the urgent need to narrow income and wealth gaps. What we never hear are any concrete solutions that don’t cause the same market media to hyperventilate and say “No, not that!”

It’s always no to taxation of the rich (because socialism); no to state spending (because socialism and inflation); no to pay rises (because inflation); no to asset price collapses (because markets and ads for designer lifestyle goods); no to breaking up monopolies (because rigged markets); and no to any form of protectionism (because markets and long supply chains in firms running ads for designer lifestyle goods). None of the key policy levers can be pulled for any serious length of time, or at all.

And yet now is apparently the right time to pull the rate hikes, QE tapering, and then QT levers, while reassuring markets that asset prices won’t go down, and saying that this will help the working class pay the rent. “Pull the other one. it’s got bells on,” as they mutter in working class London while serving drinks on trays to billionaires publicly worrying about wealth gaps. “Who’ll put you up when you’ve lost your bedstead; And you can’t find your way ‘ome?”

Meanwhile, the key Moscow/NATO meeting ended yesterday with the former saying the situation was “very dangerous” and the way forward was unclear. Some report that the only obstacle to a way forward for Russia in one respect is the warmer-than-normal weather: until the ground freezes hard, their tanks can’t roll even if Putin wants them to. (Ironic, given global warming was supposed to start wars, according to the Pentagon.) Will Vlad dilly dally for much longer?

* * *

Today is light on data, apart from US PPI and initial claims, but is heavy on big picture themes, far-too-early 2022 calls, and instant-coffee table intellectualism

Tyler Durden

Thu, 01/13/2022 – 10:05

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com