Money supply growth rose slightly in November, rising above October’s twenty-one-month low. Even with November’s rise, though, money supply growth remains far below the unprecedented highs experienced during much of the past two years. During thirteen months between April 2020 and April 2021, money supply growth in the United States often climbed above 35 percent, well above even the “high” levels experienced from 2009 to 2013. As money supply growth returns to “normal,” however, this may point to recessionary pressures in the near future.

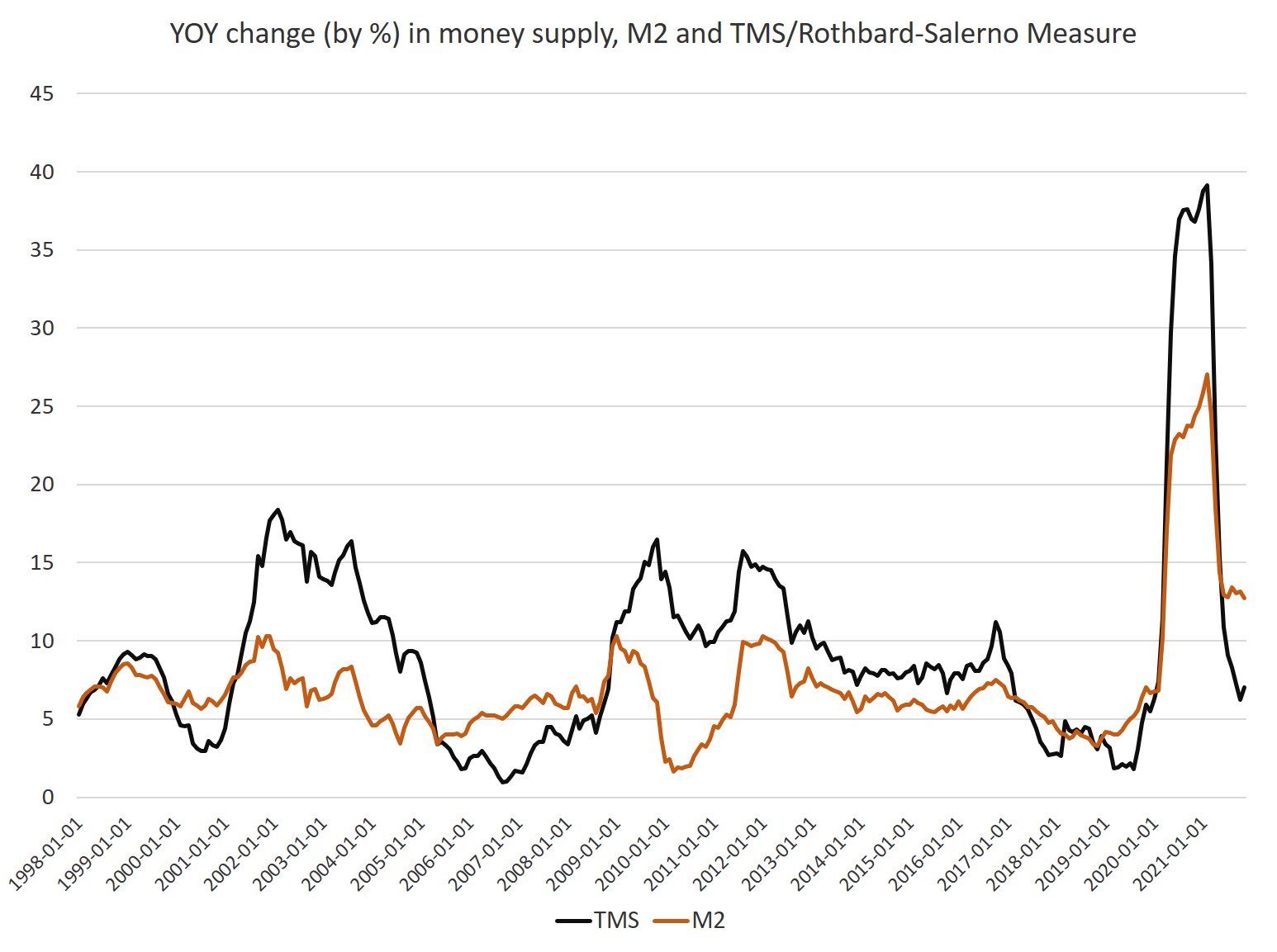

During November 2021, year-over-year (YOY) growth in the money supply was at 7.0 percent. That’s up from October’s rate of 6.2 percent, and down from the November 2020 rate of 36.8 percent. Growth peaked in February 2021 at 39.1 percent.

Historically, the growth rates during most of 2020, and through April of 2021, were much higher than anything we’d seen during previous cycles, with the 1970s being the only period that comes close.

The money supply metric used here—the “true” or Rothbard-Salerno money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. The Mises Institute now offers regular updates on this metric and its growth. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits and retail money funds).

M2 growth rates have been largely stable for the past sixth month, with the growth rate in November falling slightly to 12.7 percent. That’s down slightly from October’s growth rate of 12.5 percent. November’s rate was well down from November 2020’s rate of 24.4 percent. M2 growth peaked at a new high of 27.0 percent during February 2021.

Money supply growth can often be a helpful measure of economic activity, and an indicator of coming recessions. During periods of economic boom, money supply tends to grow quickly as commercial banks make more loans. Recessions, on the other hand, tend to be preceded by periods of slowing rates of money supply growth. However, money supply growth tends to begin growing again before the onset of recession. As recession nears, the TMS growth rate typically climbs and becomes larger than the M2 growth rate. This occurred in the early months of the 2002 and the 2009 crises. A similar pattern appeared before the 2020 recession. Money-supply growth fell throughout much of 2019, and the economy appeared headed toward recession. However, the “lockdowns” and stay-at-home orders of the covid panic accelerated this process and ensured a sizable drop in economic activity. Massive stimulus then pushed money-supply growth up to record levels.

Fed Stimulus and Declining Loan Growth

Money supply growth was fueled in part by enormous amounts of deficit spending that occurred throughout 2020 and 2021. This led to the “need” for large amounts of monetization by the Federal Reserve. (This was needed to keep interest on the national debt low.) Indeed, as federal deficit spending grew throughout 2020, Fed purchases of government bonds increased substantially as well. Since June of 2021, however, federal spending has fallen well below its earlier peaks levels. This has allowed the Fed to scale back its monthly asset purchases, and the growth in Federal Reserve assets has been slowing—although there are still no plans at the Fed to actually decrease total assets:

Moreover, year-over-year growth in commercial loans has been negative since March of 2021, further putting downward pressure on money-supply growth. Commercial and industrial loans in the US were down, year over year, 7.9 percent in November, and have been in negative territory since April of 2021.

Another factor in declining growth rates is declining totals in Treasury deposits at the Fed. These totals are factored into the TMS money supply measure—but not with M2—and this total has declined from $1.7 trillion in July 2020 to $133 billion in November.

Overall, such a sizable drop in TMS growth in recent months continues to point toward a weakening economy. As commercial banks make fewer loans, they create less new money. And as the Federal reserve buy fewer assets, it creates less new money to do so. That’s good for price inflation, but a drop in new money can be a big problem for zombie companies, and bubble industries that rely on a constant influx of new money.

The Mises Institute exists to promote teaching and research in the Austrian school of economics, and individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. These great thinkers developed praxeology, a deductive science of human action based on premises known with certainty to be true, and this is what we teach and advocate. Our scholarly work is founded in Misesian praxeology, and in self-conscious opposition to the mathematical modeling and hypothesis-testing that has created so much confusion in neoclassical economics. Visit https://mises.org