Nomura Warns Of Relief-Rally ‘Squeeze’ Into OpEx From Massive Rise In “Fuel For A Melt-Up”

Hopeful signs of a lowering in tensions on the border of Ukraine have sparked a ‘risk-on’ push higher in markets, which will now likely prompt significant Equities “squeeze” flows from the Options space and covering from dynamic hedgers.

Add to the news that Putin is pulling back the fact that China injected a net 100B Yuan into the banking system via the MLF, sending CSI 300 +1.1%, as a further signal of liquidity- and credit- pumping after January’s already all-time record $626B of new Yuan loans offered showed the extent that which Chinese authorities are willing to go to stifle the economic- and market- crunch in the country.

All this combined to a strong session as cash-trading begins and as Nomura’s Charlie McElligott warns, “virtuous” second-order Greeks look set to take-over and further accelerate the spot rally / vol compression into expiration.

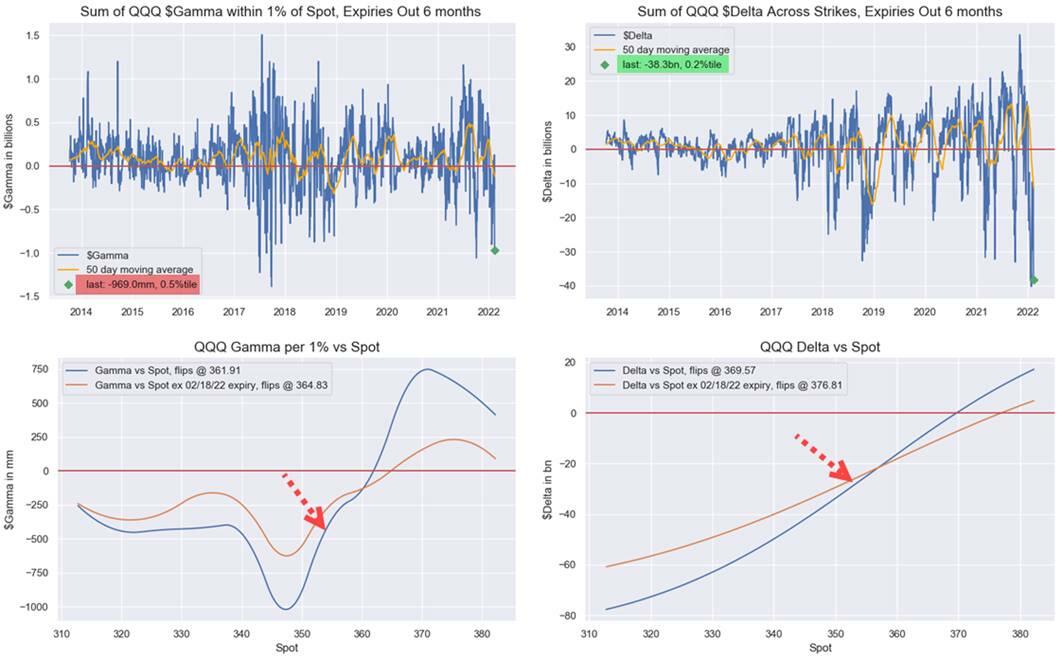

On the Index Options side, the Gamma run-off this week is going to be substantial (SPX -35%, QQQ -41%, IWM -53%), with the majority of it in downside Puts—which could accelerate “trade up” into expiration (although this potentially then leaves us vulnerable next week, depending upon what clients choose to do with hedges btwn now and expiration– i.e. whether they “roll”)

-

Vanna impact from the current gap-lower in iVol (spot VIX currently -6 vols from yday’s highs after the Russian “de-escalation” headlines) will accelerate Dealer covering of “short hedges” in futures as Puts decay / Delta moves toward zero as we rally away from downside strikes (while too, lower iVol will see Gamma get LONGER as a further stabilizer)

-

Additional Charm impact via short-dated option proximity to imminent expiration from increasingly OTM Puts which Dealers are short to clients—leading to additional “covering” impulse of futures “short hedges” on the approach

$Delta Rank (extreme “Short” as fuel for melt-up):

- SPX / SPY -$427.2B, 2.0%ile

- QQQ -$38.3B, 0.2%ile

- IWM -$15.4B, 1.0%ile

$Gamma Rank (“accelerant” flows which will chase moves in both directions):

- SPX / SPY -$8.6B, 6.8%ile

- QQQ -$969.0mm, 0.5%ile

- IWM -$243.3mm, 13.3%ile

$Gamma drops for Op-Ex (large unclenching—but this time from such extensive “downside” hedging):

- SPX / SPY -35%

- QQQ -41%

- IWM -53%

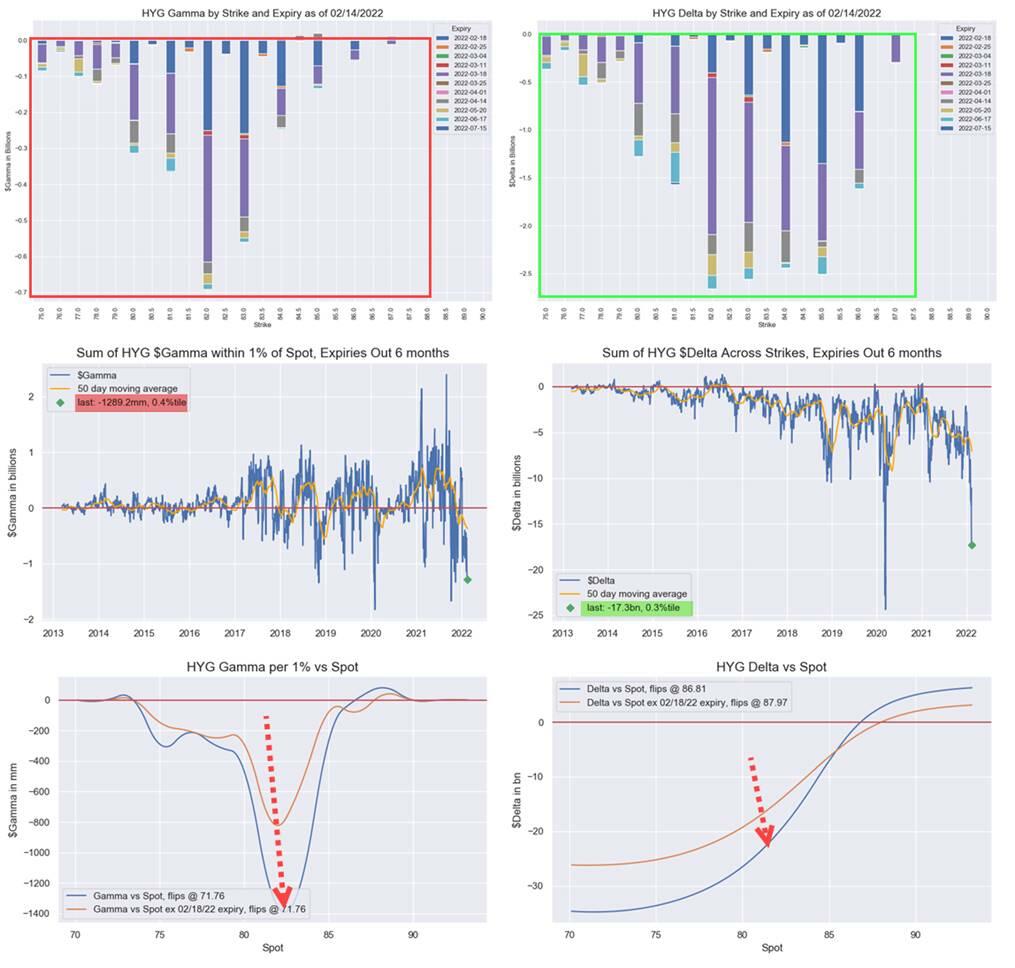

The Nomura strategist adds that it’s not just Equities product Vol position in the “cross-hairs” – we have seen absolutely incredible demand for Credit (HYG / high yield) hedging here and away as Spread product is a known “loser” with tighter FCI and negative impacts of QT “crowding-out” from Fixed-Income investors…and Dealers are MASSIVELY “Short Gamma with EXTREME Short Delta,” with 38% of the Gamma running-off Friday, setting this one up to be extra spicy

This is particularly interesting too because we also see “Corporate Credit” (spread WIDENING) as the large NEGATIVE macro factor price catalyst for SPX and the second worst for Nasdaq per Quant Insight…meaning a substantial RALLY here in HYG could add additional gasoline to further “sling-shot” an Equities mechanical rally.

And finally, the notional short base is substantial, particularly in “macro” ETF at 98.3%ile…

which will likely elicit further “buy to cover” fuel.

So unless we see a serious pushback from US officials to deny the headlines that Putin is pulling back, the market – at least into OpEx – has significant potential from positioning, greeks, and macro-hedges to melt-up.

Tyler Durden

Tue, 02/15/2022 – 10:06

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com