Europe’s Depleted Gas Storage Might Not Get Refilled Ahead Of Next Winter

Europe may have trouble replenishing its natural gas storage facilities by next winter as storage levels are at decade lows.

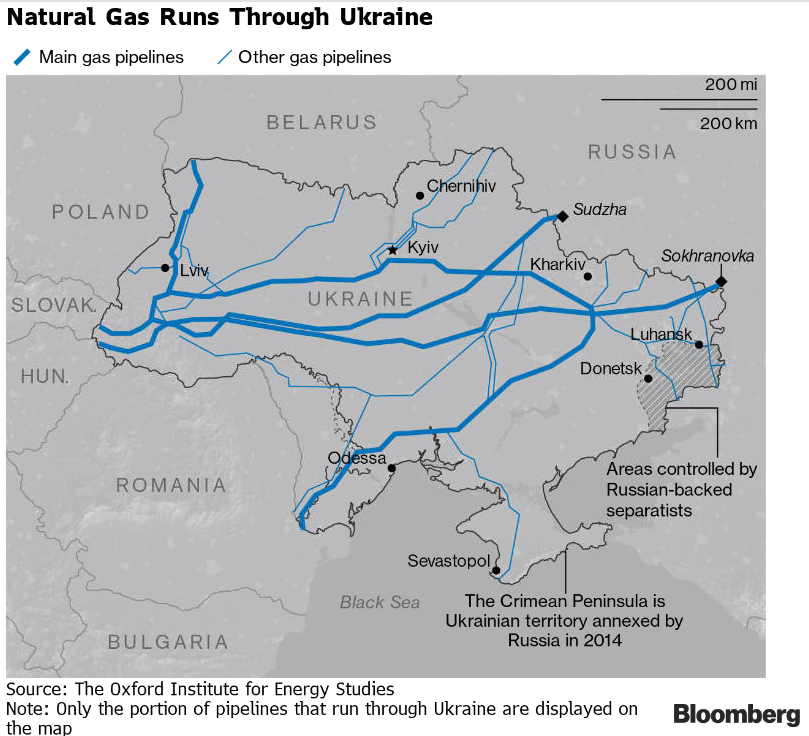

Russia, which supplies one-third of Europe’s natgas needs, has said delivery of gas through vast networks of pipelines will continue.

On Monday, Russia’s gas producer Gazprom published a statement warning there will be “serious challenges” in replenishing European gas storage facilities for next winter considering “such significant gas volumes” are needed and never has this happened ahead of the summer months.

Gazprom said there could be daily restrictions on injections because of the technological capacities of the pipeline infrastructure. Then there’s also the risk of damage to pipelines that transit gas from Russia through Ukraine. On top of this, European markets will be competing with increasing demand from Asian markets.

Bloomberg data shows that German underground storages “are depleted” by 70.6%, while French ones are 77.1%. Gas withdrawal from European storage lasts until late March and, in some cases, early April. Gas injections begin shortly after to resupply the continent for the summer months and ahead of next winter. However, since storage levels are at decade-low levels, filling up ahead of next winter could be a challenge.

Then there’s the risk of Russia limiting natgas flows to Europe in retaliation for a raft of fresh sanctions that froze Russian central bank assets, and some Russian banks were removed from the SWIFT financial messaging system, which has caused utter chaos in Russian markets on Monday, especially in FX markets.

Wood Mackenzie analyst Kateryna Filippenko told Reuters, “Europe might have to pull every lever to keep the lights on – reducing gas burn and cranking up mothballed nuclear and coal plants; maximizing indigenous gas production and pipeline imports.”

Filippenko said there would be temporary fixes, leaving Europe with “perilously low storage volumes” going into winter, adding that energy prices “could be higher than 2021/22”.

Kaushal Ramesh, an analyst at Rystad Energy, also agreed with Filippenko: “End-2022 and going into 2023 may see prices closer to the 2021 winter and could be higher.”

Although the European benchmark, Dutch gas prices, are below December’s record highs, prices did jump 60% on Thursday after Moscow invaded Ukraine.

Higher energy prices have rippled through the economy and resulted in a massive surge of power prices that have crushed households across Europe. Governments in the region are spending billions of euros shielding consumers from soaring power prices.

“Rising commodities prices will further fuel already high levels of inflation, putting Western central banks between a rock and a hard place,” said Teeuwe Mevissen, senior market economist at Rabobank.

“Raising interest rates will increase the chance of hurting the pace of economic recovery, not raising rates might lead to increased inflation expectations and might still lead to a deflationary environment because of lower purchase power putting pressure on spending power and, therefore, demand,” said Mevissen.

The good news so far is that “western nations have excluded Russian commodity exports from sanctions,” said Mark Haefele, chief investment officer for global wealth management at UBS Group AG.

“But positions are shifting fast, and Western nations have already begun implementing measures that seemed unlikely a few days ago, and the White House has stated that energy sanctions are on the table,” Haefele said.

Even though Gazprom continues to pump gas into the energy crisis-stricken continent, there are genuine risks that supply disruptions could be seen or at least pipeline capacity into Europe might not be able to inject enough gas to refill supplies ahead of next winter, which could very well result in higher energy prices.

Tyler Durden

Tue, 03/01/2022 – 04:15

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com