“The Worst Of All Worlds”: “Paralyzed” Fed Will Move “Too Slowly” To Raise Rates

Submitted by QTR’s Fringe Finance

This is Part 1 of an exclusive interview with Chris DeMuth, Jr., who founded Rangeley Capital, an event driven hedge fund in Connecticut.

Rangeley’s strategy is to invest in mispriced securities with limited downsides and corporate events that unlock shareholder value. He also hosts Sifting the World, Seeking Alpha’s SPAC and event driven research product. In his spare time, he climbs mountains.

QTR’s Note: Chris is one of the smartest people I’ve had the chance to meet during my tenure as an investor. He was one of the first people to ever take a phone call from me in the early 2010’s when I first started looking at the Questcor/Acthar scam. He was also one of the first people to be nice to me when I got my start on Seeking Alpha back about 10 years ago and is also widely respected by many people whose work I admire and follow.

All answers are opinion only and do not constitute investment recommendations.

Q: What do you see as potential outcomes for the Ukraine/Russia conflict in terms of the actual geopolitical volatility?

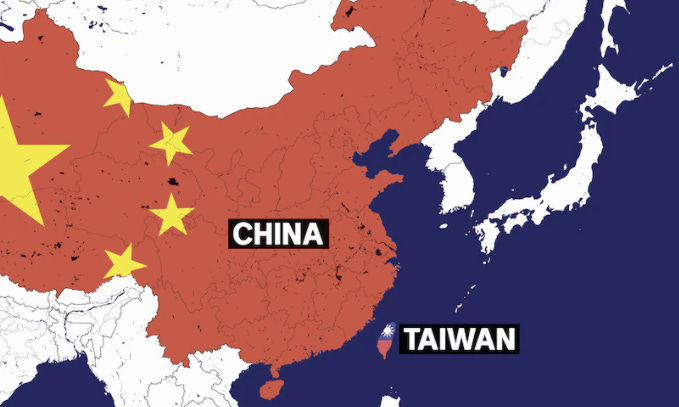

The potential outcome I’m most focused on is a spike in geopolitical volatility if this spreads to the Pacific. I am endlessly concerned about Ukraine for the sake of Ukraine, but where this could take the next big jump is if China invades Taiwan.

Additionally, Putin could be emboldened to strike the Baltic states and Poland.

It would not make a lot of sense for him to try, but so far his attack on Ukraine has been clumsy and irrationally executed, which broadens the scope for possible next moves to contemplate.

What do you see as outcomes for the market? Will Russian stocks ever trade again on U.S. exchanges?

The clearest, most mechanistic outcome for the market is on commodities from oil to wheat, driving up prices on already tight supply. Russian stocks could be permanently impaired if the current precarious balance of Putin’s aggression and his stable control of Russia continue.

But there are so many ways for things to change abruptly – the Russians could decisively win in a way that causes the west to make accommodations or Putin could be deposed causing the west to go from sanctions to aid in a abrupt pivot.

Do you think there’s a chance Russia just stops taking payment in anything other than rubles or gold?

Yes. They might have to. I expect there to be some manner of a default, probably in a way that allows them to keep doing business with their few residual trading partners.

Who do you think has all the leverage in this Russia Ukraine situation?

China. Russia has already committed most of their pre-positioned forces. The Ukrainians are already fighting like lions for their homeland. The west is already helping with the tools to sustain the Ukrainian fight and, if necessary, sustain it behind enemy lines for months or years to come.

So most of the direct and secondary players are committed. That leaves China. They could make or break Russia’s attack. They will certainly exact aggressive terms in return for whatever they commit.

What are the short, medium and long term implications going to be for U.S. stocks? Could we face an unprecedented era of discomfort, as I’ve predicted? What about for the U.S. dollar?

Prices down and volatility up over the short-term as investors refocus on systemic risk and rotate away from unprofitable tech towards owning real stuff.

Longer-term, the US might be seen as somewhat of a safe haven. We have been outperforming most international markets for a long time but this could really highlight the virtue of the rule of law and the precariousness of emerging markets.

The dollar is bad, but less bad than most of its alternatives, giving it kneejerk safe haven status in a pinch. But this could be the beginning of the end. Having reserve status and playing political games with a foreign power’s central bank is probably a game one can play only once.

If China coalesces around Russia, they could start a non-USD block that could expand over time, creating a multi-polar monetary system for the first time in over a century.

Do you think the Fed is going to be able to deal with inflation, underneath this whole mess?

No. I think they will fuck it all up.

OK, well, having said that, what’s your prediction for monetary policy this year given the new volatility?

They will be paralyzed and move too slowly, probably getting the worst of all worlds. This will be bad for the economy, but could also lead to dramatic political repercussions. The US administration has tried to claim otherwise out of some combination of duplicity and stupidity, but inflation is quite regressive.

Rich people can only spend so much on food and gas and basic staples; even filling up a G Wagon and flying in elk steaks from Wyoming costs a trivial percentage of income and wealth. But regular people, especially regular people on fixed incomes, are getting badly damaged.

They will be voting in November.

What do you see for energy prices going forward? Is the worst behind us?

I’m very long oil and gas, so I might rephrase that as “is the best behind us?” I don’t know. Can the ESG/renewable religion survive Russia’s invasion of Ukraine?

If it can, then the worst/best lies ahead. But if we are the slightest bit strategic, we can see that Putin’s leverage is nukes and energy and we can do something about energy today. Drill petrochemicals, mine coal, and fire up the nuclear plants. It will take time but an all-in effort to get our exploration and production to full speed will take the edge off over the longer-term.

The initial flails to cozy up to the Venezuelans and to reconstruct a sham deal with the Iranians appear unserious, but there’s still time to sweep aside red tape to get American energy production fired up.

The Europeans have done so badly on energy policy, that it leaves them the option of a quick, easy 180 degree pivot on essentially everything they’ve done to head in the right direction (especially on nuclear power).

I’m quite long uranium and see it as a clear beneficiary of any steps for the west to get serious on either energy independence or on the environment. Opposition is an elite aesthetic preference that we don’t have any time for anymore.

I wrote a couple days ago that I thought Russia and China could be looking to form a new economic system backed by gold. Thoughts on this idea?

It is a terrific idea. I won’t change teams or anything, but they’d get me at least pondering who my friends are and who my enemies are if they do something so sound.

Where in U.S. stocks are you looking now? Anything in tech you are daring to buy yet or do we have further to fall?

I like energy exposure with event driven kickers such as Amplify Energy (AMPY).

Someone dragged their anchor over our pipeline and the market thought we were the villains. I think we were the victims and have a claim. It could easily be worth twice what it cost today, especially after the spill liabilities are assigned (and, I think, we come out ahead).

Tech? Seems early, precarious, and scary to me at the moment. Virtually all of my tech exposure is via SPACs with a free put in the form of a redemption right for the cash in trust. I like speculating only when I get free do overs when I change my mind.

How do you handicap the risk for Chinese ADRs now that we’ve seen what has happened to Russian ones? Any bargains in Chinese ADRs you would touch?

Very very risky. I have had far more short ideas than long ideas among Chinese ADRs and the exceptions have generally not been happy ones. The structure has been good at shielding fraudsters from repercussions, their auditors have been largely complicit, and the whole process of Chinese companies listing in the US has largely been one of fleecing credulous foreigners.

At the risk of verging on masochism, I’ll mention that Nam Tai (NTP) is a hairy mess, but one with a price at $6 that has already priced in quite a lot of misery; it is down by almost half so far this year and this strong reaction looks to me to be an overreaction.

Anything else my readers should know about your current take on markets?

I just got back from summiting Kilimanjaro and tracking lions in the Serengeti. I had time to detach from the day-to-day aspects of work while my colleagues kept things going in my absence.

Upon return, I realized how eager I am to dive deep into research projects but also how futile my time was spent reactively chasing down explanations for hyper short-term stock price moves. They are mostly noise. They are sometimes efficient. But they are almost all ignorable. I just want to find very particular situations where we have an edge and to not force it if they don’t reveal themselves.

We can have a terrific year with just a couple each quarter. So I need to relax, do the work, and let opportunities come to me. I don’t need to have something to say about everything. It is easier to actually act smart if you’re willing to sound dumb, or at least not have a hot take on everything.

Price solves everything (well not fraud, but nearly everything). So if the market gets a good battering, there could be some fresh opportunities to put money to work. It is annoying to bid against price-insensitive enthusiasts for the same securities or companies, so it could be great to clear them out of the market for at least a while. I’m mildly net long here in the hope and expectation that we avoid WWIII, but also long potassium iodide as a hedge in case I’m wrong.

If you enjoyed this content, become a subscriber at QTR’s Fringe Finance.

My Disclaimer: I own CCJ and tons of gold, silver and oil and gas names. I may add any name mentioned in this article and sell any name mentioned in this piece at any time. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I get shit wrong a lot.

Chris DeMuth’s Disclaimer: Long uranium via SRUUF, AMPY, and NTP. Additional legal disclosures here for anyone really into that kind of thing; short version: think for yourself.

Tyler Durden

Thu, 03/17/2022 – 09:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com