“There Is No Real Place To Hide If You Are A Portfolio Manager”

By Ven Ram, Bloomberg Markets Live Commentator and analyst

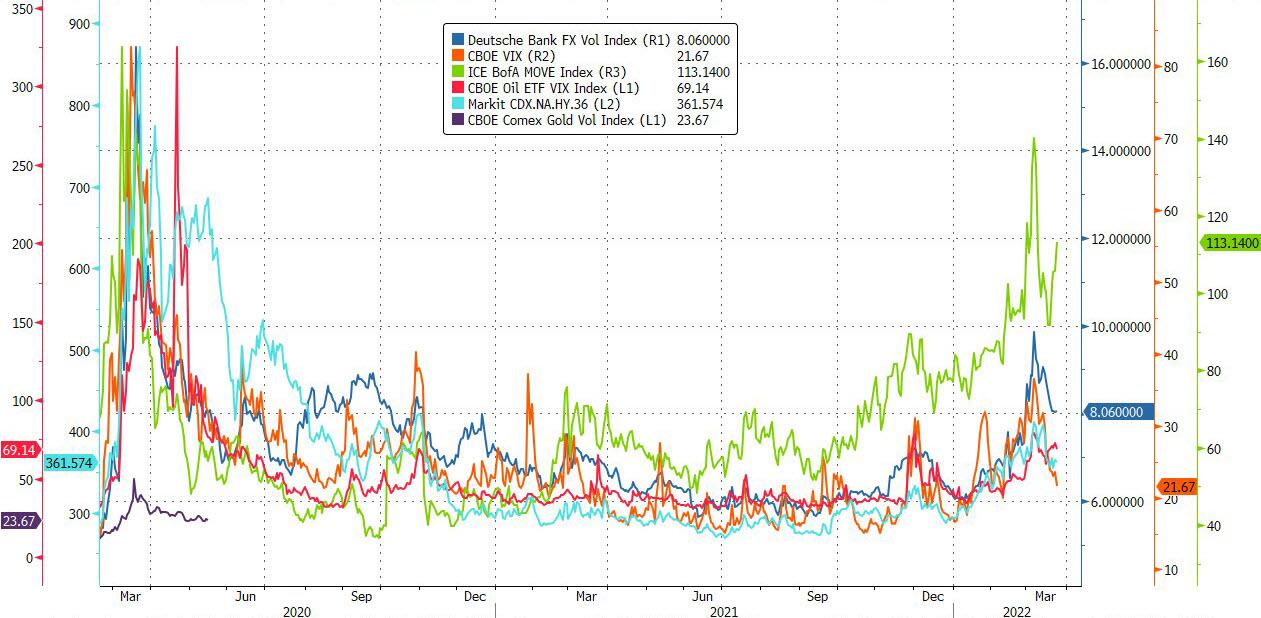

Market Volatility? Count Yourself in if You Know Intrinsic Value

And so the “world couldn’t be a better place” stock rally of the past week showed signs of flagging overnight, with some incredulity setting in. But bonds obliged, with yields trending lower, and commodities whistled a merry tune too.

Today the story could be different, and tomorrow it may be a new variation. In other words, the constant among the markets’ variables isn’t quite clear yet. Yesterday notwithstanding, Treasuries haven’t been so off-color in decades. Stocks can change their mind on a whim and currency overlays may have performed even if the underlying asset didn’t do so well, depending on your pick. In other words, there is no real place to hide if you are a portfolio manager. Still, going long cash isn’t really an option given the corrosive power of inflation and what that would mean for real returns. And in any case, cash is only a small — even if elastic — component of the whole make-up.

But such volatility also brings with it opportunity. All you had to do in the past three years was to go long pretty much any asset — or even anything that may not truly be called an asset — and wait for the tooth fairy to do the rest. With such fairy tales having come to an end, it’s now the time for true alpha-seekers. The best among them have an edge in this kind of market, where everyone knows the price of an asset but few really know its intrinsic value.

In other words, these are the people who intuitively know what a dollar bill is worth, blindfolded. That one skill is enough to conquer the world, and that’s what Warren Buffett has shown us. Just the other day, when stocks were running up, up and away, Berkshire Hathaway announced its purchase of Alleghany Corp. I couldn’t help but immediately look at the price the conglomerate had paid. An earnings yield of almost 9% and a price-to-book of just 1.26x, did you say? To be fair, I wasn’t sure whether it was Buffett himself who saw the deal through or one of his new fund managers, but the purchase shows Berkshire is still sticking to its value knitting.

So volatility is not to be feared, but to be embraced. In financial markets, risk is often defined as volatility. The more astute fund managers have a simpler, more earthy way of defining it: risk comes from not knowing what you are doing. But for those who do know their abacus well, there has never been a better time in a long, long while.

Tyler Durden

Thu, 03/24/2022 – 17:40

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com