France Has Repatriated All Its Monetary Gold

By Jan Nieuwenhuijs of Gainesville Coins

The central bank of France has covertly repatriated 221 tonnes of gold between 2013 and 2016. Since then, all its monetary gold is stored in La Souterraine in Paris. Repatriating all gold is related to France’s aim to revamp Paris as a gold trading center.

Introduction to the Gold Repatriation Trend

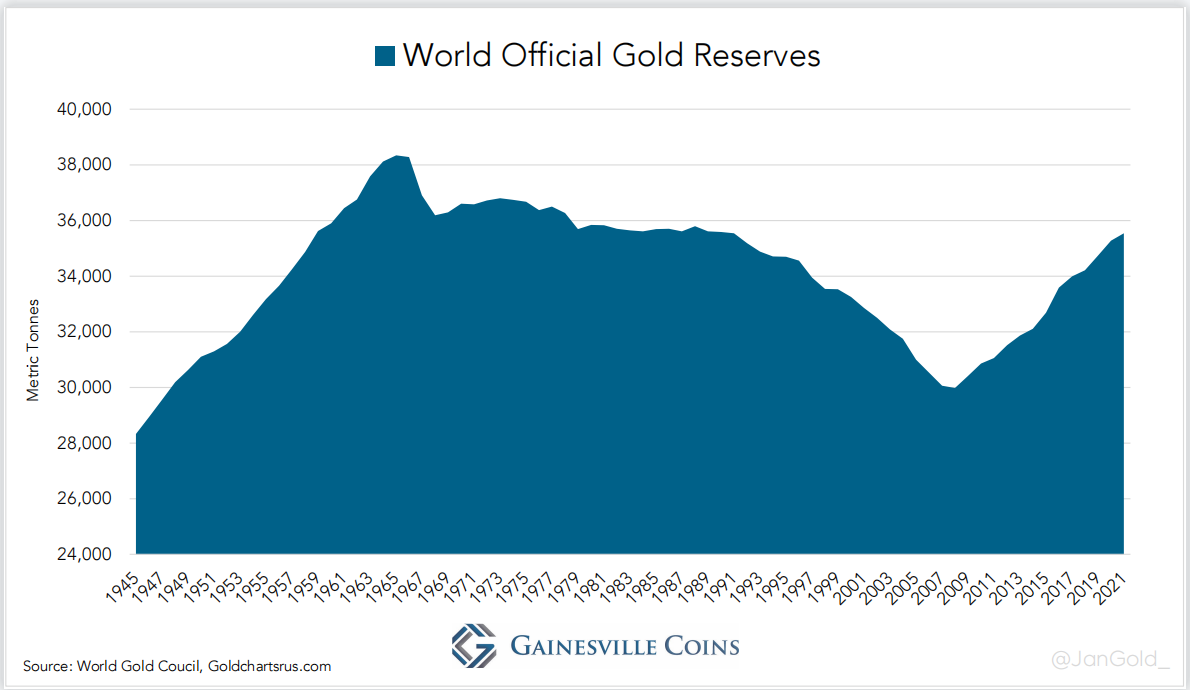

Gold’s role in international finance and geopolitics has changed dramatically since 2008. The Great Financial Crisis reminded central banks of radical uncertainty and the humbling aspect of risk. Instead of net sellers, central banks have turned into net buyers of gold, steadily purchasing more than 400 tonnes a year.

Most European central banks own relatively more gold than their Asian peers. Thus, some European governments haven’t bought additional metal but have instead reassessed their gold policy.

In 2013 the German central bank was the first to announce it would repatriate gold from the Banque de France (BdF, “Bank of France”) and the Federal Reserve Bank of New York. Eventually it would have 50% of its gold stored in Germany. The other half would be left in New York and London. According to the German central bank their gold policy serves three objectives: cost efficiency, security, and liquidity.

Cost efficiency has to do with storage costs at different locations. Security is about the safety of vaults and in which country the vaults are located. How much is a country willing to store abroad? Liquidity involves holding bars in liquid marketplaces such as London, i.e., to efficiently swap metal for foreign exchange in times of emergency.

After Germany, other countries such as the Netherlands and Austria followed by repatriating monetary gold. There has been no official news from France.

When France Repatriated Its Gold

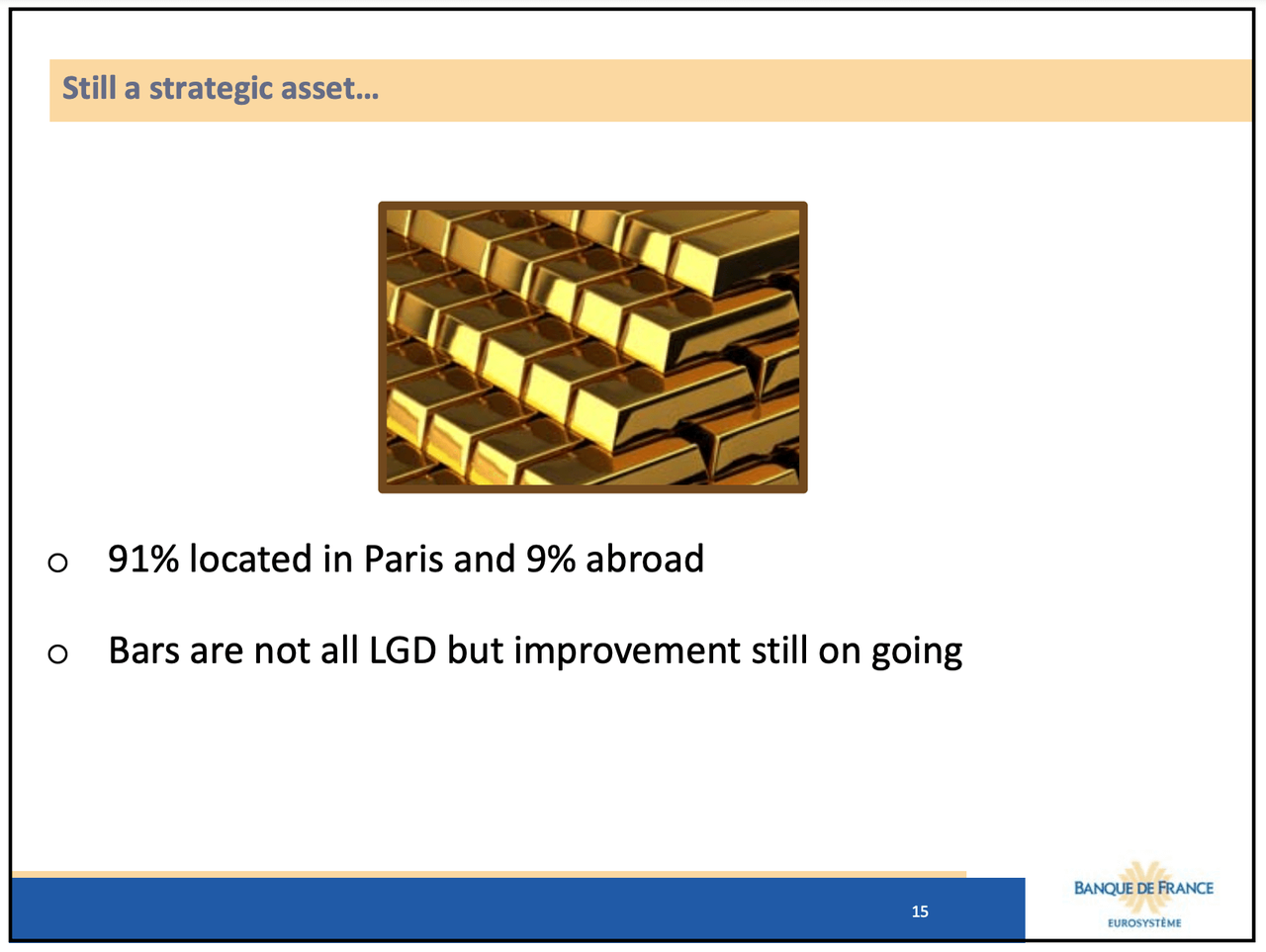

At the London Bullion Market Association (LBMA) conference in 2013, one of the keynote speakers was BdF’s Director of Market Operations, Alexandre Gautier. On slide 15 of his presentation we can see BdF stored 91% of its 2,435 tonnes in Paris at the time, and 9% “abroad.”

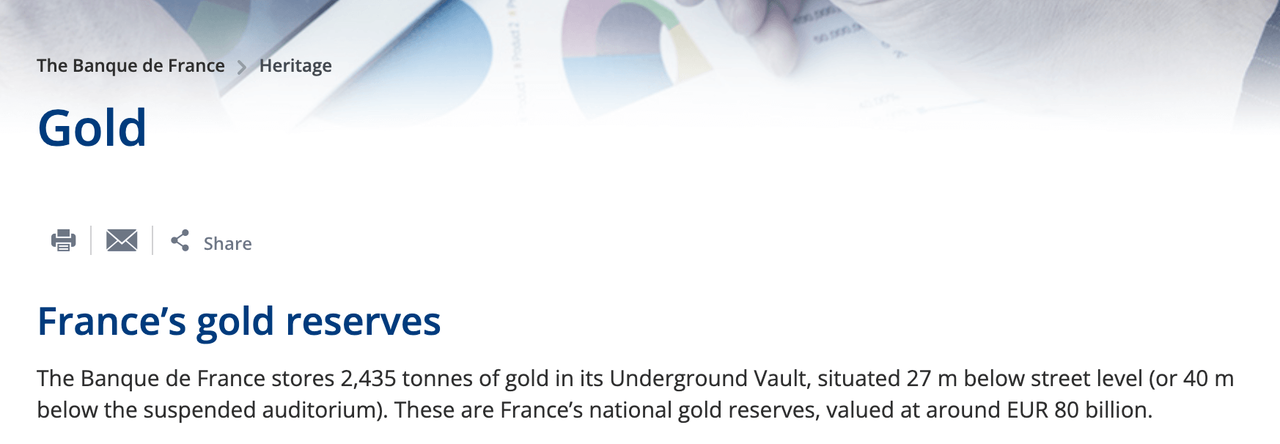

Currently, we can read on BdF’s website that all its gold is stored in its own vault in Paris. The gold stored abroad must have been repatriated after 2013. Knowing exactly when is impossible. For one, because BdF doesn’t respond to emails regarding this subject. Second, BdF employees that answer the phone don’t speak English.

The first snapshot taken by the Way Back Machine of the above BdF webpage, though, is from October 6, 2017. And at the bottom of that snapshot, it reads: “Updated on: 12/08/2016.” BdF thus first disclosed that all its gold is in Paris by late 2016. Therefore, BdF must have repatriated 221 tonnes (9% of 2,435 tonnes) sometime between 2013 and 2016.

Quite likely France repatriated from the UK. In the 1960s France was the most vocal critic of the United States, which was printing much more dollars relative to the gold they had backing those dollars. France aggressively converted dollars into gold and pressed for a reform of the international monetary system. Any of the French gold stored in a liquid marketplace abroad after Bretton Woods was likely in London.

Reviving Paris as a Gold Trading Center

In 2018, BdF’s Second Deputy Governor, Sylvie Goulard, published an article in the LBMA’s magazine the Alchemist: “Banque de France and Gold: Past and Future.” Goulard praises Paris as one of the main gold trading hubs, next to London and New York, during the gold standard. And “the financial crisis [in 2008] acted as a wake-up call for gold,” she writes, which “proved to be an opportunity for gold and for the Banque de France.”

She shares that since 2009 BdF has been upgrading all its monetary gold to LBMA Good Delivery standards. In the modern Western gold wholesale market centered in London all bars meet the same criteria—LBMA Good Delivery—to ease trading. Any bars that don’t adhere to this standard will trade at a discount, which can increase during a crisis.

{kind=link}

The central bank of France has made sure all its gold can be deployed in the wholesale market, if it desires to do so. Additionally, Goulard writes:

“As well as upgrading its stock, the Banque de France is taking various other steps to ensure it meets LBMA criteria. All large bars are weighed on electronic scales which allow the Banque to check that the weight meets the LBMA standards for accounting purposes. The renovation of the historical vaults housing the gold reserves [in Paris] has nearly been completed: the floor will be able to support heavy forklift trucks, and intermediary shelves have been inserted between the existing shelves to ensure the gold is only stacked five bars high, making handling easier. Other storage facilities will be available soon: either strong rooms for storing bare bars on shelves or large vaults to store sealed pallets, facilitate handling, transportation and auditing. By the end of the year, a new IT system will be in place to improve our ability to respond to market operation needs and other custody services.

“Building on its long experience in managing its gold reserves, in 2012, the Banque de France began to extend its range of gold services to reserve managers. In addition to offering custody of physical gold in its vault in Paris, the Banque de France can buy and sell gold on the spot markets for its institutional customers, using its execution expertise. It can also offer gold swaps either for the purpose of using gold as collateral for deposits, which has been happening more and more since the Basel III framework recognised gold as eligible collateral, or for the purpose of raising foreign currency cash against gold. Finally, foreign central banks can engage in gold lease transactions with the Banque de France as principal, in order to increase the return on their gold holdings without increasing their counterparty risk.

“While these gold investment services have until now only been offered from London, it recently became possible for the Banque de France to offer them also from Paris, thanks to a partnership with a large commercial bank that is active in the gold market. As a result, with the improvements in the Banque de France’s vaults, and the innovations in its service offering, Paris could gradually re-emerge as a key marketplace for gold.”

After Goulard’s article was published it became clear that JP Morgan has an account at BdF. Through bullion banks BdF is better connected to the greater gold market.

{kind=link}

Foreign central banks that store gold in Paris are offered services such as trading, lending and swapping gold. From an industry insider I have heard that in recent years central banks have swapped U.S. dollars for gold at the BdF. Occasionally, the gold swap rate was higher than the U.S. dollar interest rate. Holding gold—for as long as the swap is agreed—incurs no counterparty risk.

Some analysts surmise that turning Paris into a new gold trading center is primarily due to Brexit. Surely, the Brexit vote on June 23, 2016, has strengthened BdF’s ambitions to develop a local gold market, but these ambitions were born long before the U.K. decided to leave the E.U.

As Goulard mentions, BdF started upgrading its metal in 2009, and “in 2012, the Banque de France began to extend its range of gold services to reserve managers.” It’s possible, though, that BdF doubled down on its ambitions by repatriating its metal from London shortly after the Brexit vote.

However it may be, France’s central bank saw huge potential for gold right after 2008. Based on Goulard’s article my assessment is that BdF expects gold’s role in the financial system will increase. Why else upgrade all the French gold, overhaul the vault, set up a new IT system, and develop a full set of trading services for foreign central banks in Paris?

Tyler Durden

Sun, 04/17/2022 – 08:10

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com