Tverberg: The World Has A Major Crude Oil Problem; Expect Conflict Ahead

Authored by Gail Tverberg via Our Finite World blog,

Media outlets tend to make it sound as if all our economic problems are temporary problems, related to Russia’s invasion of Ukraine. In fact, world crude oil production has been falling behind needed levels since 2019. This problem, by itself, encourages the world economy to contract in unexpected ways, including in the form of economic lockdowns and aggression between countries. This crude oil shortfall seems likely to become greater in the years ahead, pushing the world economy toward conflict and the elimination of inefficient players.

To me, crude oil production is of particular importance because this form of oil is especially useful. With refining, it can operate tractors used to cultivate crops, and it can operate trucks to bring food to stores to sell. With refining, it can be used to make jet fuel. It can also be refined to make fuel for earth moving equipment used in road building. In recent years, it has become common to publish “all liquids” amounts, which include liquid fuels such as ethanol and natural gas liquids. These fuels have uses when energy density is not important, but they do not operate the heavy machinery needed to maintain today’s economy.

In this post, I provide an overview of the crude oil situation as I see it. In my analysis, I utilize crude oil production data by the US Energy Information Agency (EIA) that has only recently become available for the full year of 2021. In some exhibits, I also make estimates for the first quarter of 2022 based on preliminary information for this period.

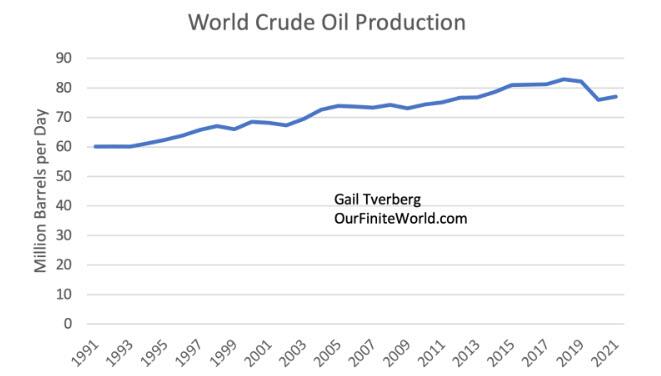

[1] World crude oil production grew marginally in 2021.

Figure 1. World crude oil production based on EIA international data through December 31, 2021.

Crude oil production for the year 2021 was a disappointment for those hoping that production would rapidly bounce back to at least the 2019 level. World crude oil production increased by 1.4% in 2021, to 77.0 million barrels per day, after a decrease of -7.5% in 2020. If we look back, we can see that the highest year of crude oil production was in 2018, not 2019. Oil production in 2021 was still 5.9 million barrels per day below the 2018 level.

With respect to the overall increase in crude oil production of 1.4% in 2021, OPEC helped bring this average up with an increase of 3.0% in 2021. Russia also helped, with an increase of 2.5%. The United States helped pull the world crude increase down, with a decrease in production of -1.1% in 2021. In Section [5], more information will be provided with respect to crude production for these groupings.

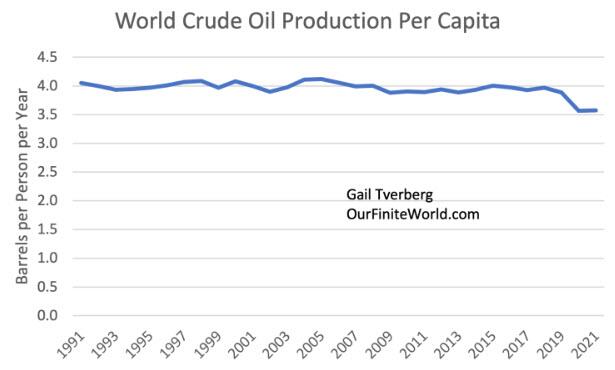

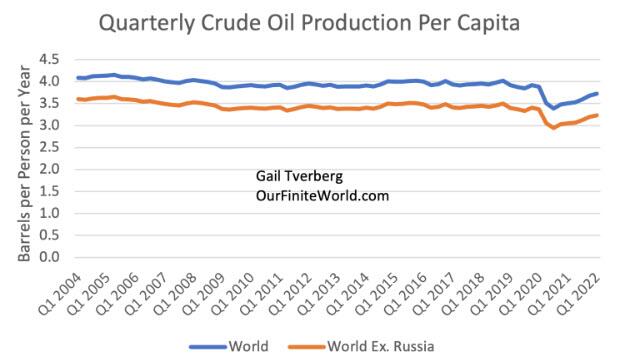

[2] The growth in world crude oil production shows an amazingly steady relationship to the growth in world population since 1991. The major exception is the decrease in consumption that took place in 2020, with the lockdowns that changed consumption patterns.

Figure 2. World per capita crude oil production based on EIA international data through December 31, 2021, together with UN 2019 population estimates. The UN’s estimated historical amounts were used through 2020; the “low growth” estimate was used for 2021.

Figure 2 indicates that, up through 2018, each person in the world consumed an average of around 4.0 barrels of crude oil. This equates to 168 US gallons or 636 liters of crude per year. Much of this crude is used by businesses and governments to produce the basic goods we expect from our economy, including food and roads.

A big downshift occurred in 2020 with the COVID lockdowns. Many people began working from home; international travel was scaled back. The reduction of these uses of oil helped bring down total world usage. Changes such as these explain the big dip in crude oil production (and consumption) in 2020, which continued into 2021.

Even in 2019, the world economy was starting to scale back. Beginning in early 2018, China banned the importation of many types of materials for recycling, and other countries soon followed suit. As a result, less oil was used for transporting materials across the ocean for recycling. (Subsidies for recycling were helping to pay for this oil.) Loss of recycling and other cutbacks (especially in China and India) led to fewer people in these countries being able to afford automobiles and smartphones. Lower production of these devices contributed to the lower use of crude oil.

{kind=link}

On Figure 2, there is a slight year-to-year variation in crude oil per capita. The single highest year over the time period shown is 2005, with 2004 not far behind. This was about the time many people think that conventional oil production “peaked,” reducing the availability of inexpensive-to-produce oil.

[3] Crude oil prices dropped dramatically when economies were shut in, beginning in March 2020. Prices began spiking the summer and fall of 2021, as the world economy attempted to open up. This pattern suggests that the real problem is tight crude oil supply when the economy is not artificially constrained by COVID restrictions.

Figure 3. Average weekly Brent oil price in chart prepared by EIA, through April 8, 2022. Amounts are not adjusted for inflation.

An analysis of price trends suggests that most of the recent spike in crude prices is due to the tightness of the crude oil supply, rather than the Ukraine conflict. The Brent oil price dropped to an average of $14.24 in the week ending April 24, 2020, not long after COVID restrictions were enacted. When the economy started to reopen, in the week ending July 2, 2021, the average price rose to $76.26. By the week ending January 28, 2022, the average price had risen to $90.22.

Russia invaded Ukraine on February 24, 2022. The Brent spot price on February 23, 2022, was $99.29. Brent prices briefly spiked higher, with weekly average prices rising as high as $123.60, for the week ending March 25, 2022. The current Brent oil price is about $107. If we compare the current price to the price the day before the invasion began, the price is only $8 higher. Even compared to the January 28 weekly average of $90.22, the current price is $17 higher.

Saying that the Ukraine invasion is causing the current high price is mostly a convenient excuse, suggesting that the high prices will suddenly disappear if this conflict disappears. The sad truth is that depletion is causing the cost of extraction to rise. Governments of oil exporting countries also need high prices to enable high taxes on exported oil. We are increasingly experiencing a conflict between the prices that the customers can afford and the prices that those doing the extraction require. In my view, most oil exporting countries need a price in excess of $120 per barrel to meet all of their needs, including reinvestment and taxes. Consumers would prefer oil prices under $50 per barrel to keep the price of food and transportation low.

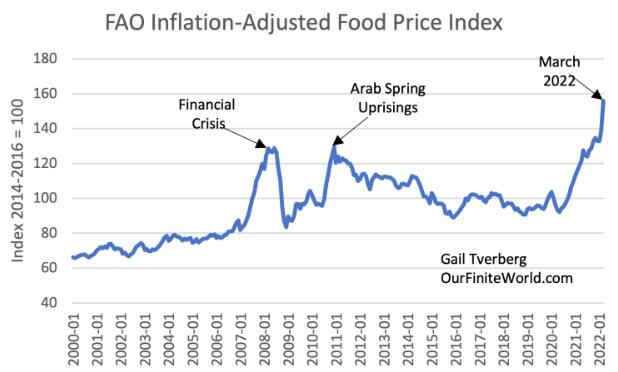

[4] Food prices tend to rise when oil prices are high because products made from crude oil are used in the production and transport of food.

History shows that bad things tend to happen when food prices are very high, including riots by unhappy citizens. This is a major reason that high oil prices tend to lead to conflict.

Figure 4. FAO inflation-adjusted monthly food price index. Source.

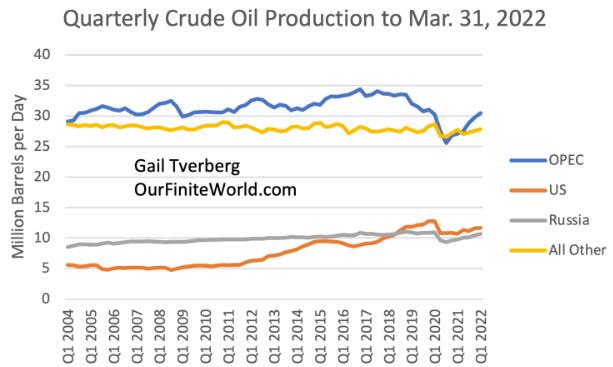

[5] Quarterly crude oil data suggests that few opportunities exist to raise crude oil production to the level needed for the world economy to operate at the level it operated at in 2018 or 2019.

Figure 5 shows quarterly world crude oil production broken down into four groupings: OPEC, US, Russia, and “All Other.”

Figure 5. Quarterly crude oil production through first quarter of 2022. Amounts through December 2021 are EIA international estimates. Increase in OPEC first quarter of 2022 production is estimated based on OPEC Monthly Oil Market Report, April 2022. US crude oil production for first quarter of 2022 estimated based on preliminary EIA indications. Russia and All Other production for first quarter of 2022 are estimated based on recent trends.

Figure 5 shows four very different patterns of past growth in crude oil supply. The All Other grouping is generally trending a bit downward in terms of quantity supplied. If world per capita crude oil production is to stay at least level, the total production of the other three groupings (OPEC, US, and Russia) needs to be rising to offset this decline. In fact, it needs to rise enough that overall crude production growth keeps up with population growth.

Russian Crude Oil Production

The data underlying Figure 5 shows that up until the COVID restrictions, Russia’s crude oil production was increasing by 1.4% per year between early 2005 and early 2020. During the same period, world population was increasing by about 1.2%. Thus, Russia’s oil production has been part of what has helped keep world crude production about level, on a per capita basis. Also, Russia seems to have made up most of its temporary decrease in production related to COVID restrictions by the first quarter of 2022.

US Crude Oil Production

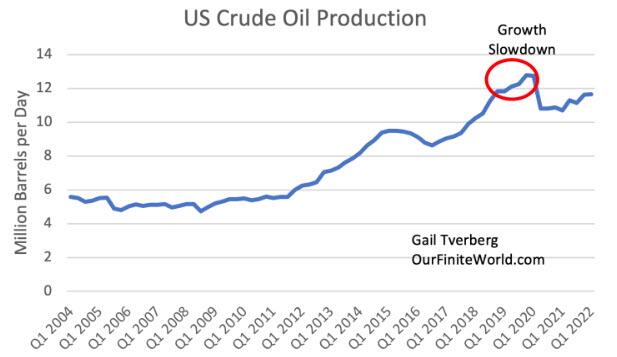

Growth in US crude oil production has been more of a “feast or famine” situation. This can be seen both in Figure 5 above and in Figure 6 below.

Figure 6. US crude oil production based on EIA data. First quarter of 2022 amount is estimated based on EIA weekly and monthly indications.

US crude oil production spurted up rapidly in the 2011 to 2014 period, when oil prices were high (Figure 3). When oil prices fell in late 2014, US crude production fell for about two years. US oil production began to rise again in late 2016, as oil prices rose again. By early 2019 (when oil prices were again lower), US crude oil growth began to slow down.

In early 2020, COVID lockdowns brought a 15% drop in crude oil production (considering quarterly production), most of which has not been made up. In fact, growth after the lockdowns has been slow, similar to the level of growth during the “growth slowdown” circled in Figure 6. We hear reports that the sweet spots in shale formations have largely been drilled. This leaves mostly high-cost areas left to drill. Also, investors would like better financial discipline. Ramping up greatly, and then cutting back, is no way to operate a successful company.

Thus, while growth in US crude oil production greatly supported world growth in crude oil production in the 2009 to 2018 period, it is impossible to see this pattern continuing. Getting crude oil production back up to the level of 12 million barrels a day where it was before the COVID restrictions would be extremely difficult. Further production growth, to support the growing needs of an expanding world population, is likely impossible.

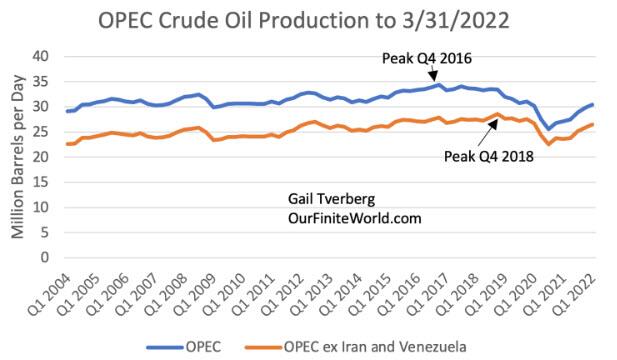

OPEC Crude Oil Production

Figure 7 shows EIA crude oil production estimates for the total group of countries that are now members of OPEC. It also shows crude oil production excluding the two countries which have recently been subject to sanctions: Iran and Venezuela.

Figure 7. OPEC crude oil production to December 31, 2021, based on EIA data. Estimates for first quarter of 2022 based on indications from OPEC Monthly Oil Market Report, April 2022.

If Iran and Venezuela are removed, OPEC’s long-term production is surprisingly “flat.” The “peak” period of production is the fourth quarter of 2018. The fourth quarter of 2018 was the time when the OPEC countries were producing as much oil as they could, to get their production quotas as high as possible after the planned cutbacks that took effect at the beginning of 2019.

Strangely, EIA data indicates that production didn’t fall very much for this group of countries (OPEC excluding Iran and Venezuela), starting in early 2019. The 2019 cutback seems mostly to have affected the production of Iran and Venezuela. It was only later, in the first three quarters of 2020, when COVID restrictions were affecting worldwide production, that crude oil production for OPEC excluding Iran and Venezuela fell by 4 million barrels per day. Production for this group then began to rise, leaving a shortfall of about 900,000 barrels a day, relative to where it had been before the 2020 lockdowns.

It seems to me that, at most, production for the group of OPEC countries excluding Iran and Venezuela can be ramped up by 900,000 barrels a day, and even this is “iffy.” Iraq is reported to be having difficulty with its production; it needs more investment, or its production will fall. Nigeria is past peak, and it is also having difficulty with its production. The high reported crude oil reserves are meaningless; the question is, “How much can these countries produce when it is required?” It doesn’t look like production can be ramped up very much. Furthermore, we cannot count on continued long-term growth in production from these countries, such as would be needed to keep pace with rising world population.

Figure 8. Crude oil production indications for Iran and Venezuela, based on EIA data through December 31, 2021. Change in oil production for first quarter of 2021 is estimated based on OPEC Monthly Oil Market Report, April 2022.

Figure 8 suggests that, indeed, Iran might be able to raise its production by perhaps 1.0 million barrels a day when sanctions are lifted.

Venezuela looks like a country whose crude oil production was already declining before sanctions were imposed. The cost of production there was likely far higher than the world oil price. Also, Venezuela has oil debts to China that it needs to repay. At most, we might expect that Venezuela’s production could be raised by 300,000 barrels per day in the absence of sanctions.

Putting the three estimates of amounts that crude oil production can perhaps be raised together, we have:

-

OPEC ex Iran and Venezuela: 900,000 bpd

-

Iran: 1,000,000 bpd

-

Venezuela: 300,000 bpd

-

Total: 2.2 million bpd

The shortfall of crude oil production in 2021, relative to 2018 production, was 5.9 million bpd, as mentioned in Section [1]. The 2.2 million barrels per day possibly available from this analysis gets us nowhere near the 2018 level. Furthermore, we have nowhere to go to obtain the rising crude oil production required to support the rising population with enough crude oil to supply food and industrial goods at today’s consumption level.

[6] Eliminating, or even reducing, Russia’s crude oil production is certain to have an adverse impact on the world economy.

Figure 9 shows the step-down in crude oil production that occurred in early 2020 and indicates that the world’s oil supply is having difficulty getting back up to pre-COVID levels. If Russia’s crude oil production were to be eliminated, it would make for another step-down of comparable magnitude. Major segments of the economy would likely need to be eliminated.

Figure 9. Quarterly crude oil production through first quarter of 2022 divided by world population estimates based on 2019 UN population estimates. Crude oil amounts through December 2021 are EIA estimates. Crude oil production estimates for first quarter 2022 are as described in the caption to Figure 5.

[7] When there isn’t enough crude oil to go around, the naive belief is that oil prices will rise and either more oil will be found, or substitutes will take its place. In fact, the result may be conflict and elimination of segments of the economy.

Our self-organizing economy will tend to adapt in its own way to inadequate crude oil supplies. Eventually, the economy may collapse completely, but before that happens, changes are likely to happen to try to preserve the “better functioning” parts of the economy. In this way, perhaps parts of the world economy can continue to function for a while longer while getting rid of less productive parts of the economy.

The following is a partial list of ways the economy might adapt:

-

Fighting may take place over the remaining crude oil supplies. This may be the underlying reason for the conflict between NATO and Russia, with respect to Ukraine.

-

COVID lockdowns indirectly reduce demand for crude oil. A person might wonder whether the current COVID lockdowns in China are partly aimed at preventing oil and other commodity prices from rising to absurd levels.

-

Some organizations may disappear from the world economy because of inadequate funding or lack of profitability.

-

Additional supply lines are likely to break, allowing fewer types of goods and services to be made.

-

The world economy may subdivide into multiple pieces, with each piece able to make a much more limited array of goods and services than is provided today. A shift toward the use of other currencies instead of the US dollar may be part of this shift.

-

World population may shrink for multiple reasons, including poor nutrition and epidemics.

-

The poor, the elderly and the disabled may be increasingly cut off from government programs, as total goods and services (including total food supplies) fall too low.

-

Europe could be cut off from Russian fossil fuel exports, leaving relatively more for the rest of the world.

[8] Countries that are major importers of crude oil and crude oil products would seem to be at significant risk of reduced supply if there is not enough crude oil to go around.

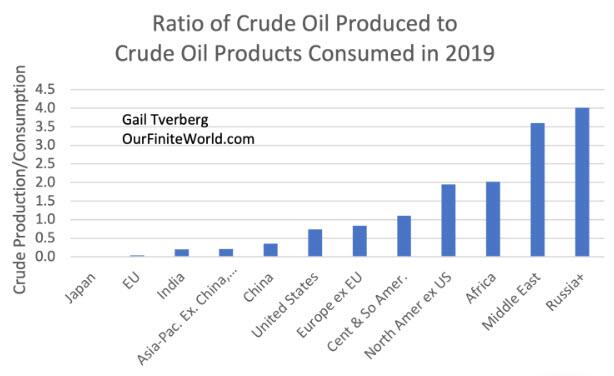

Figure 10 shows a rough estimate of the ratio of crude oil produced to crude oil products consumed in 2019, the last full year before the pandemic. On an “All Liquids” basis, the US ratio of crude oil production to consumption would appear higher than shown on Figure 10 because of its unusually high share of natural gas liquids, ethanol, and “refinery gain” in its liquids production. If these types of production are omitted, the US still seems to have a deficit in producing the crude oil it consumes.

Figure 10. Rough estimate of ratio of crude oil produce to the quantity of crude oil products consumed, based on “Crude oil production” and “Oil: Regional consumption – by product group” in BP’s 2021 Statistical Review of World Energy. Russia+ includes Russia plus the other countries in the Commonwealth of Independent States.

Perhaps all that is needed is the general idea. If inadequate crude oil is available, all of the countries at the left of Figure 10 are quite vulnerable because they are very dependent on imports. Russia and the Middle East are prime targets for countries that are desperate for crude oil.

[9] Conclusion: We are likely entering a period of conflict and confusion because of the way the world’s self-organizing economy behaves when there is an inadequate supply of crude oil.

The issue of how important crude oil is to the world economy has been left out of most textbooks for years. Instead, we were taught creative myths covering several topics:

-

Huge amounts of fossil fuels will be available in the future

-

Climate change is our worst problem

-

Wind and solar will save us

-

A fast transition to an all-electric economy is possible

-

Electric cars are the future

-

The economy will grow forever

Now we are running into a serious shortfall of crude oil. We can expect a new set of problems, including far more conflict. Wars are likely. Debt defaults are likely. Political parties will take increasingly divergent positions on how to work around current problems. News media will increasingly tell the narrative that their owners and advertisers want told, with little regard for the real situation.

About all we can do is enjoy each day we have and try not to be disturbed by the increasing conflict around us. It becomes clear that many of us will not live as long or well as we previously expected, regardless of savings or supposed government programs. There is no real way to fix this issue, except perhaps to make religion and the possibility of life after death more of a focus.

Tyler Durden

Sat, 04/30/2022 – 20:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com