Fed Warns Of Negative Feedback Loop, Fragile Liquidity, And More Volatile Prices

Authored by Mike Shedlock via MIshTalk.com,

The Fed’s Financial Stability Report is a real hoot. Importantly the Fed fails to point a finger at itself…

Image clip from Fed’s Financial Stability Report

Please consider the Fed’s May 2022 Financial Stability Report

Pertinent Warnings

-

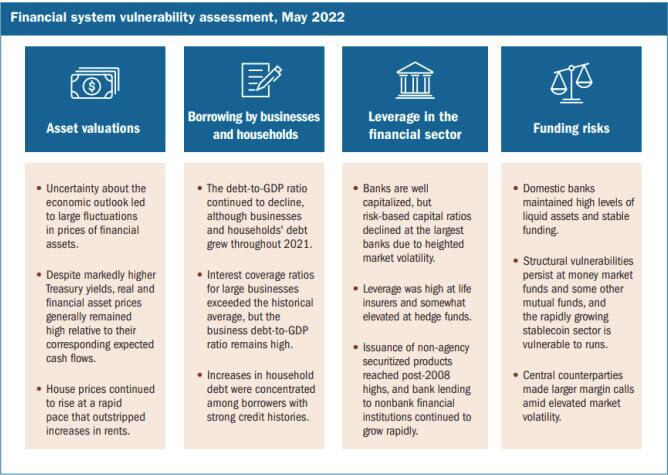

Despite markedly higher Treasury yields, real and financial asset prices generally remained high relative to their corresponding expected cash flows.

-

House prices continued to rise at a rapid pace that outstripped increases in rents.

-

Structural vulnerabilities persist at money market funds and some other mutual funds, and the rapidly growing stablecoin sector is vulnerable to runs.

-

Leverage was high at life insurers and somewhat elevated at hedge funds.

-

Central counterparties made larger margin calls amid elevated market volatility.

Q: Who was it that created the environment that made those conditions possible?

A: The Fed with help from three rounds of inappropriate fiscal stimulus

Notable Quotes

-

Prices of risky financial assets remained generally high compared with corresponding expected cash flows. Since November, house prices rose at a rapid rate and continued to outstrip increases in rents. Asset prices remain vulnerable to declines in response to negative shocks.

-

Rising inflation, supply chain disruptions, and ongoing geopolitical events might pose risks to the ability of some businesses and households to service their debts.

-

Some types of money market funds (MMFs) and stablecoins remain prone to runs, and many bond and bank loan mutual funds continue to be vulnerable to redemption risks.

-

Elevated market volatility associated with the Russian invasion of Ukraine has led to increased margin calls by central counterparties (CCPs), which in turn increased the demand for liquidity from a range of market participants.

-

According to some measures, market liquidity has declined since late 2021 in the markets for recently issued U.S. cash Treasury securities and for equity index futures.

-

While the recent deterioration in liquidity has not been as extreme as in some past episodes, the risk of a sudden significant deterioration appears higher than normal.

-

Since the Russian invasion of Ukraine, liquidity has been somewhat strained at times in oil futures markets, while markets for some other affected commodities have been subject to notable dysfunction.

-

It is difficult to predict periods of extreme market illiquidity.

-

Corporate bond valuations eased somewhat but remained high.

-

Farmland prices relative to rents remained elevated.

-

House prices continued to increase at a rapid pace, and price-to-rent ratios remained high relative to historical levels

-

A negative shock to house prices may hurt homeowners, but such a shock is unlikely to be amplified by the financial system.

-

Many small businesses could be adversely affected by rising costs. Increasing labor costs and prices for other inputs may reduce small firms’ earnings and their ability to service their loans.

-

Leverage remained low at banks and broker-dealers but high at life insurance companies and somewhat elevated at hedge funds.

-

Banks remained well capitalized.

-

Vulnerabilities of U.S. banks to the Russian invasion of Ukraine appear to be limited.

-

Leverage at life insurers remained near its highest level of the past two decades. Life insurers continued to invest heavily in corporate bonds, collateralized loan obligations (CLOs), and CRE debt, which leaves their capital positions vulnerable to sudden drops in the value of these risky assets.

-

Stablecoins are also vulnerable to runs, and the sector continues to grow rapidly.

-

The aggregate value of stablecoins—digital assets that are designed to maintain a stable value relative to a national currency or other reference assets—grew rapidly over the past year to more than $180 billion in March 2022. The stablecoin sector remained highly concentrated, with the three largest stablecoin issuers—Tether, USD Coin, and Binance USD—constituting more than 80 percent of the total market value.

-

Additionally, some crypto-assets—such as Bitcoin—have experienced extreme price volatility. Among other things, the EO directs the FSOC to issue a report on the financial stability risks and regulatory gaps posed by digital assets and include recommendations for addressing these risks.

-

Russia’s invasion of Ukraine and subsequent international sanctions disrupted global trade in commodities, leading to surging prices and heightened volatility in agriculture, energy, and metals markets . These markets include spot and forward markets for physical commodities as well as futures, options, and swaps markets that involve an array of financial intermediaries and infrastructures . Stresses in financial markets linked to commodities could disrupt the efficient production, processing, and transportation of commodities by interfering with the ability of commodity producers, consumers, and traders to lock in prices and hedge risks.

-

The risk of futures positions increased with higher volatility, even for participants whose combined physical and futures positions were perfectly hedged. The resulting higher initial margin requirements on exchange-traded futures meant that both short and long hedgers needed cash to post additional collateral.

-

Market liquidity, the ease of entering or exiting a position, diminished as trading became more costly for end users and as market makers pulled back to manage their own risks.

-

Russia’s ongoing war in Ukraine could affect U.S. financial stability through multiple channels.

-

A prolonged conflict, particularly if accompanied by severe and widespread commodity shortages, could lead to substantial volatility in commodity and financial markets, a downturn in economic activity concentrated in Europe, higher inflation and interest rates worldwide, and a broad pullback from risk-taking, transmitting stress to institutions that are exposed.

-

Elevated and persistent inflation combined with a sharp rise in rates could pose risks to the economy and the financial system.

-

Stresses in China, including in the real estate sector, could spill over to the United States.

-

Increased debt levels in many EMEs since the onset of the pandemic have made these economies more vulnerable to adverse shocks. More recently, higher food and energy prices have worsened the terms of trade for some EMEs—particularly commodity importers—and could exacerbate social and political stresses and trigger a downturn in investor risk sentiment and capital outflows.

Those points relate to inflation, asset valuations in general, housing risks, cryptocurrencies, commodities, China, Russia, and life insurers.

Negative Feedback Loop

Recently, depth in these markets has been lower than is typical even after taking into account the level of volatility, as shown for the oil market . This markedly low depth could indicate that liquidity providers are being particularly cautious, and liquidity may be more fragile than usual. Declining depth at times of rising uncertainty and volatility could result in a negative feedback loop, as lower liquidity in turn may cause prices to be more volatile.

No!

A Negative Feedback Loop is a stabilizing event.

Negative feedback (or balancing feedback) occurs when some function of the output of a system, process, or mechanism is fed back in a manner that tends to reduce the fluctuations in the output, whether caused by changes in the input or by other disturbances.

Whereas positive feedback tends to lead to instability via exponential growth, oscillation or chaotic behavior, negative feedback generally promotes stability. Negative feedback tends to promote a settling to equilibrium, and reduces the effects of perturbations. Negative feedback loops in which just the right amount of correction is applied with optimum timing can be very stable, accurate, and responsive.

Key Omission

Other than the feedback loop error, picked up and repeated in many places including the Financial Times, the report seemed shockingly candid except for one thing.

The Fed failed to point a finger at itself for the reckless buildup of stock prices, bond prices, house prices, crypto assets, and margin.

Don’t Worry, Janet Yellen Says the Financial System is Still Orderly

Meanwhile, as the report hints at one thing, Janet Yellen Says the Financial System is Still Orderly

Key question: How long will things remain orderly given the conditions and risks the Fed laid out?

* * *

Tyler Durden

Tue, 05/10/2022 – 15:10

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com