99. Red. Balloons

By Michael Every of Rabobank

The focus for many in markets today is if the US S&P is going to truly slip into a bear market, a 20% decline from the peak. The NASDAQ is already there, of course.

What isn’t getting as many headlines is that US stocks are experiencing their worst start in 99 years(!) Recall all the nonsense about ‘The Roaring Twenties’? Well, we have the labor shortages in the aftermath of The Spanish Flu part, and the repeat of the awful Russia-Ukraine war, and fascism, and it appealing to some in the West sick of their own poor leadership, and what looks like the crash in asset prices, all of which sandwiched the fun ‘Great Gatsby’ part of the decade that markets prefer to focus on at Christmas theme parties.

In short, we see a sea of red in markets, and literally so in Ukraine, where President Zelenskiy states up to 100 soldiers are dying every day on his side alone.

So, is the worst behind us in markets? A just-released MLIV survey of 1,009 respondents shows the overall expectation is now for a further decline of 10% in the S&P from here: only 4% think the bottom is in; most think 3,500 is the line in the sand. In short, the ‘99’ red balloons are seen as likely to deflate further, or perhaps pop, before any floating by again.

Making that call is not my area as this is not an equity Daily. However, the fundamentals that led me to sneer at bullish ‘Roaring Twenties’ calls are still there to see, if only one wants to do so.

Inflation and geopolitical instability aren’t going to go away any time soon. Linking the two, as one should, a former German ambassador to Moscow tells @Tagesspiegel that President Putin is hoping his blockade of Ukraine’s grain supplies will lead to a migration crisis, with starving people then fleeing to Europe, that destabilizes the EU and pushes them to soften sanctions on Russia. Does he look wrong in that call when Germany, France, and Italy are already hardly hawkish? More pointedly, does the West have any answers to a hybrid warfare that weaponizes food, as in the past?

Meanwhile, as flagged last week, both developed and emerging markets are subsidising farmers and consumers. China just announced further subsidies of CNY10bn for its farmers, the latest (small) step to try to keep prices down, after going all in on coal production to keep energy costs low; and on a far larger scale ($26 billion), India will cut fuel levies and boost fertilizer subsidies, while offering other support to reduce the cost of living. While arguably needed in each individual country, looser fiscal policy overall in the face of a supply shock will keep inflation higher for longer. It arguably also makes it worse for those countries that cannot subsidise, and which are most likely to lead any migration crisis.

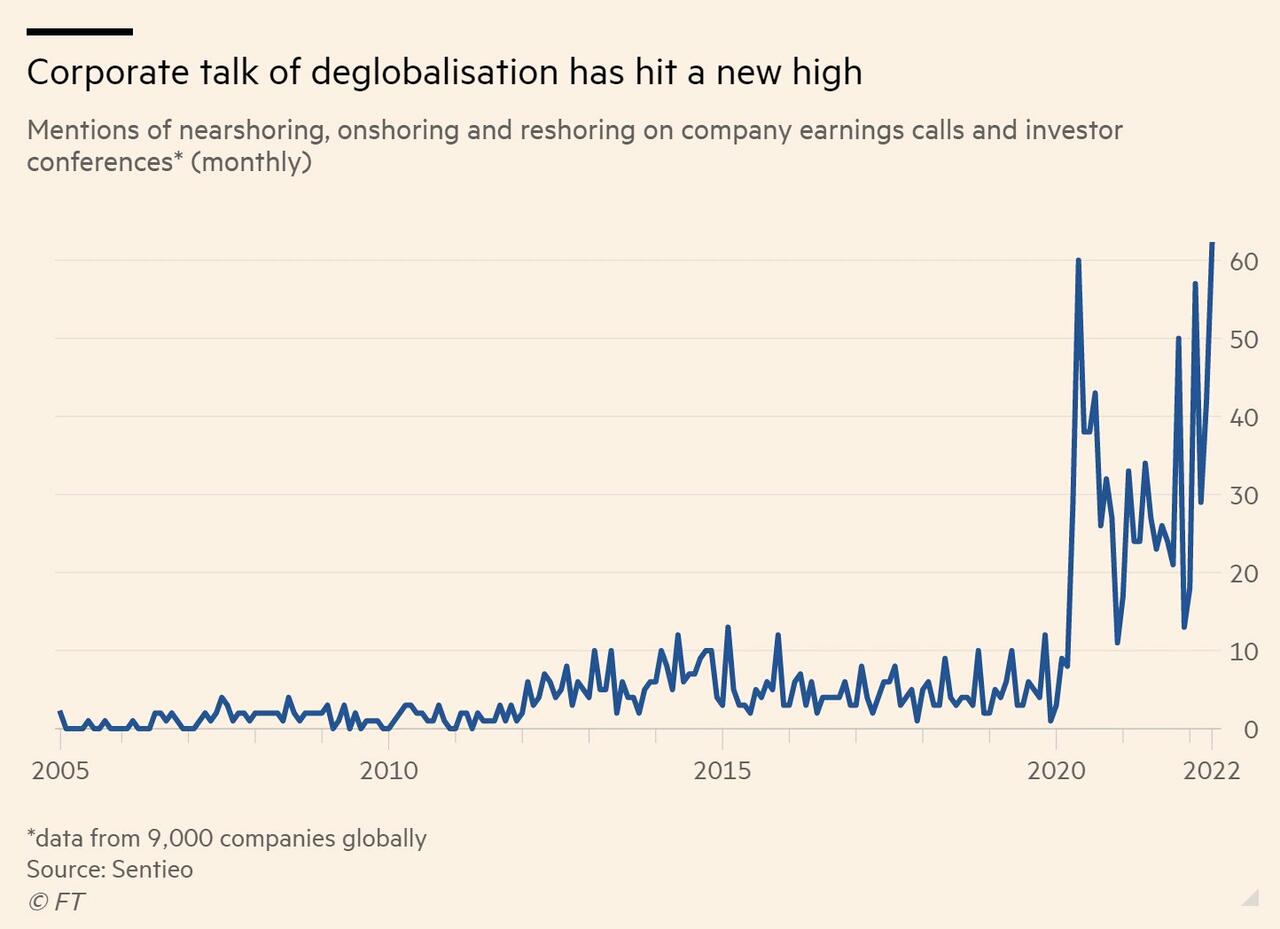

Meanwhile, the front page of the Financial Times today is ‘Business leaders warn that three-decade era of globalisation is ending’. The FT also shows mentions of ‘nearshoring’, ‘reshoring’, and ‘onshoring’ (not to mention friend-shoring) are running at an all-time high in company earnings calls and investor conferences.

As a bellwether, Apple just announced it will shift more iPhone production from China to India and Vietnam. Yes, it is finding it hard to shift the entire ecosystem of suppliers only China offers. The same is true in textiles, where there aren’t enough looms outside China, which are also made in China, and which it does not wish to sell to rivals. However, that just means entire ecosystems must move – and they will. In short, supply chain shocks are entrenched, and inflationary nearshoring *is* underway, even if it is with a ‘ketchup effect’, where we get nothing for ages and then too much. Of course, political leadership could shake the bottle.

Relatedly, US President Biden is in Asia. First, he will talk AUKUS with new Aussie PM Albanese. (Who is as wedded to it as his predecessor: he had to agree to it while in opposition before the US would agree to the deal as it’s a generational defense commitment, not something Boris Johnson might sign and then try to back out of.) Biden will also meet the Quad, as Japan –about to boost defense spending even further– talks about making AUKUS into JAUKUS, which would then only require India to make it JAUKUSI, a nuclear grouping that would roil the Pacific.

Not that China is not roiling the waters itself. Following its recent security deal with the Solomon Islands that some fear could lead to a Pacific naval base for the PLA Navy, Beijing is allegedly close to similar deals with Vanuatu and Kiribati. It’s almost as if there is a pattern… which I am sure Mr Market will explain is entirely benign and related to ‘opening-up’ and ‘reform’ and so the importance of not onshoring or nearshoring any key industries.

The US will today also launch its new Indo-Pacific Economic Strategy. This is somehow going to link its Asian defence umbrella with greater economic access to the US – without actually offering any greater economic access, as US politics is no longer pro free trade.

Many critics point out the geostrategic weakness of having no economic offer to match mighty military muscles. However, how much freer could US trade with the Pacific really get? Would a slight reduction in already low tariffs really make much difference to Asia ex-China exports? Isn’t relative US demand compared to China the most important element?

In which case, note that the US economy is likely to grow faster than China this year, with Bloomberg now downgrading its own expectation for the latter to just 2.0% y-o-y. All it took was sealing people into their homes in all its largest cities.

Yes, the new US Indo-Pacific will have less flesh on its bones than the Quad and AUKUS. Yet logic dictates friend-shoring might be a key part of it, even if that is both carrot and stick.

Linking many of the above supply-side developments, the US military is boasting on social media that it is now delivering baby formula to retailers and consumers, as FedEx also rushes it from Europe to the US too. Expect much, much more of this kind of thing ahead. And lots of money to be made from being on the right, not wrong, side of it.

This is all a lot for Davos to consider as it finally meets in person again this week, especially on top of Covid and Monkeypox. Oh, and higher interest rates, which also aren’t going away either.

PM Albanese won’t be thrilled to hear RBA’s Deputy Governor Kent say he thinks the neutral RBA rate is somewhere between 2% and 3%: but Labor doesn’t want to build an economy on the back of asset bubbles rather than productive investment and sustainable supply chains, does it?

To conclude, markets are focusing on the risks of further equity downside. Against once in a century bad performance, perhaps history and life away from Bloomberg screens might offer a better guide. However, while the real-world backdrop points to many losers ahead, that does not mean there are not also matching winners. Indeed, to avoid more ‘99’ and ‘red’, look for trial balloons as they float by. (Perhaps starting today in Asia and Davos?)

Tyler Durden

Mon, 05/23/2022 – 12:15

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com