Eurozone Yield Spreads Blow Out, It’s Another Crisis For Greece And Italy

Authored by Mike Shedlock via MishTalk.com,

Once again, the ECB has a crisis on its hands as 10-year bond rates in peripheral Europe widen relative to Germany.

Average Bond Interest Rates Through April from Europa, May 2022 is the current yield on 2022-06-06

ECB Policymakers Will Ask Lagarde to Be Tough on Fragmentation

Widening spreads have the ECB alarmed. The Bloomberg article ECB Policymakers Will Ask Lagarde to Be Tough on Fragmentation is what inspired this post.

European Central Bank policymakers will this week ask President Christine Lagarde to use stronger language to signal that fragmentation won’t be allowed to happen and the borrowing costs of more vulnerable countries like Italy and Spain will be contained, according to people familiar with the matter.

Lagarde has said many times the central bank won’t allow financial conditions across the euro area to diverge significantly and is ready to do whatever is needed to avoid it.

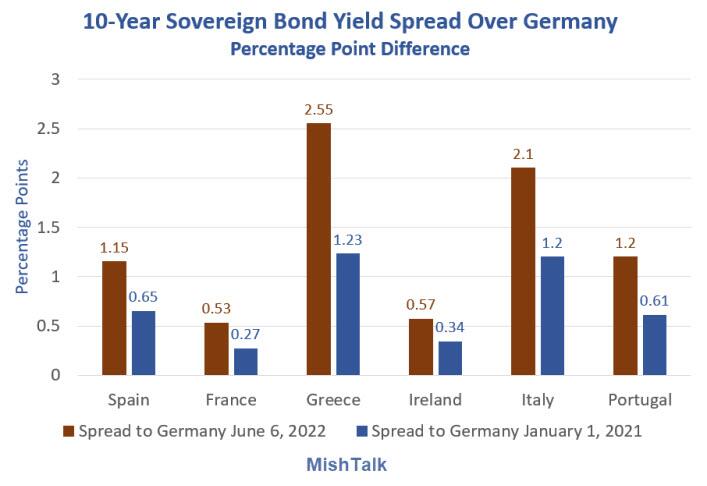

10-Year Sovereign Bond Spread Over Germany

10-Year Sovereign Bond Spread Over Germany Mish Calculation

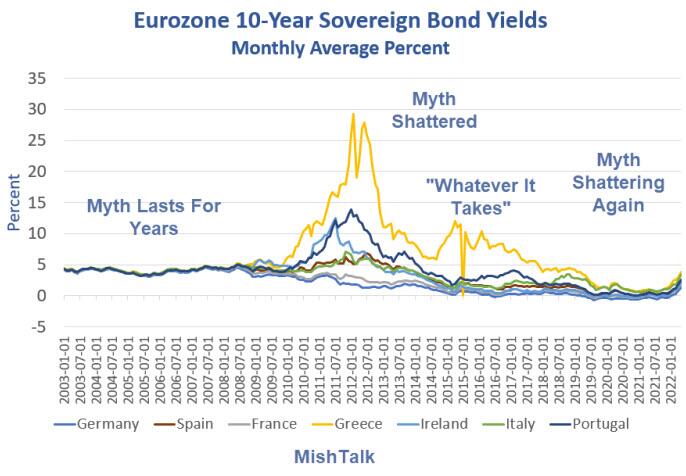

Eurozone 10-Year Sovereign Bond Yields Long Term

Long Term Average Bond Interest Rates Through April from Europa Through April 2022

The Big Myth

The big Eurozone myth is that all Eurozone sovereign debt has no risk. If it did, and that myth lasted for years, the yield on all Eurozone sovereign bonds would be the same.

In 2015, when Greece 10-year bonds exploded to nearly 30 percent, then ECB president Mario Draghi (now Italy’s Prime Minister) gave a speech announcing “We will do whatever it takes to save the Euro, and believe me it will be enough.”

After the announcement yield spreads plunged.

Q: What did Draghi do?

A: Nothing!

Seriously, the ECB did nothing. The threat alone was somehow sufficient. Draghi restored faith in peripheral debt.

Lagarde has said many times the central bank won’t allow financial conditions across the euro area to diverge significantly and is ready to do whatever is needed to avoid it.

The Eurozone gets another test doesn’t it?

Fundamental Flaw

The Euro itself is fundamentally flawed.

There is no one interest rate policy that makes sense for Greece, Spain, Italy, and Germany.

The sovereign debt risk is not the same and anyone with an ounce of common sense understands that.

Quantitative Tightening?

To control spreads this time, I suspect the ECB will have to buy every bond of Greece, Spain, Italy, and Portugal.

That is not compatible with Quantitative Tightening or rising yields.

What a Hoot!

For the second time ECB presidents have to come to the rescue of Greece, Spain, Italy, and Portugal.

I am positive that another “We will do whatever it takes” announcement without doing anything will NOT suffice.

Controlling spreads is going to be damn hard to pull off with the ECB’s interest rate at -0.50 percent and rising and quantitative tightening allegedly in the works.

Another Eurozone sovereign debt crisis is brewing and few see it.

Biden Plans to Pay Down National Debt, Tackle Inflation

Meanwhile, back in the USA, my June 3 “Hoot of the Day” was Biden Plans to Pay Down National Debt, Tackle Inflation

End of the 40-Year Bull in Debt and a “Global Depression” Threat

The bull market in bonds is over, and with that Danielle DiMartino Booth see a “Global Depression” Threat

Click on the link for an excellent video.

* * *

Tyler Durden

Wed, 06/08/2022 – 06:30

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com