As MBS Go “No Bid”, Veteran Mortgage Broker Warns ‘Nobody Is Prepared To Deal With Inflation’

Authored by Louis S Barnes via cherrycreekmortgage.com (emphasis ours),

During the last forty-four years, my days have begun and ended with the mortgage market. Four painful moments stand out. Today makes five. (There have been many more good days, but even the Fairy Godmother has her limits.)

Mortgages are covered poorly in financial press, as stocks and such are much more entertaining. Today’s events still unfolding will take days for good coverage. Freddie’s weekly survey will not discover today until next Thursday. But the MBS market is real-time, not like old, sleepy S&L days.

The CPI news this morning was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.” No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. Overnight the retail consequence has been a leap from roughly 5.50% to 6.00% for low-fee 30-fixed loans.

The physics of collisions… the second one does the harm. When your car hits a telephone pole, no problem. Then, after a slight lag, trouble comes when you hit the inside of your car. Same thing in football: helmet on helmet is all-okay… until your brain hits the inside of your skull.

The same physics govern housing collisions with mortgages. At the new year mortgages were still three-ish. In February, four. At the end of March, five. May, five-and-a-half. Historically, a two-percentage-point rise from cyclical trough has iced housing, the freeze underway a month ago. Now up by three points, and double January.

The pause in housing between the first collision and second is elongated because of human nature. Someone desperate to buy a house is still desperate, and modestly relieved to buy even at a higher price and rate so long as not forced into an unlimited auction. Now it’s time for Wile E. Coyote in his Acme sneakers, running off into thin air and all okay until he looks down.

Looking down… MBS are such a weird market that other markets have not processed what is happening. Stocks are down 2% today, but would be down a hell of a lot more if considering what a full-stop to housing will mean.

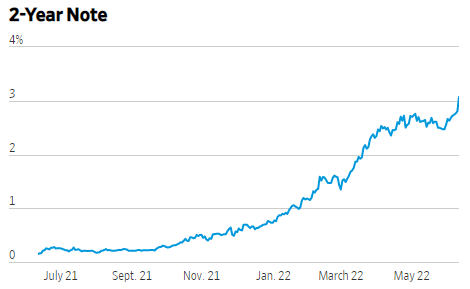

Another marker of MBS distress: the 10-year T-note had held 3.00% since April, the important top in 2012 and 2018. Trading 3.05% yesterday, now 3.20% — retail mortgages jumped triple that amount. The 10s/mortgages spread today is almost 300bps and double the 10s’ yield. Inconceivable. The Fed telltale 2-year T-note had held 2.70% since April, 2.85% yesterday, today 3.05% adding only one more .25% hike to the 2-cast, which is not enough to explain MBS overnight.

Today’s CPI Trigger. Markets were braced for a bad report, but not this. Overall CPI jumped 1.0% in May. Any thought of deceleration… ka-blooie. CPI 8.6% in the last year, accelerating under pressure from Ukraine energy dislocation. Many observers this morning say that the CPI news is so lousy that there is no point in looking at the details. Wrong. From the onset of Covid to Ukraine, our inflation problem was supply chain, mostly manufactured goods. Since Ukraine, it has shifted to energy.

Different elements of CPI have different weightings, which conceal the effect of energy in a crisis like this. In May the energy index within CPI… up 34.6% in May alone. In an event like this, the notion of excluding the high-volatility “core” is meaningless. Everything requires energy. The uppers and soles of your Nikes are fossil fuel. Food has its own Ukraine issue, but energy is the problem, from fuel to fertilizer.

Oil was $75/bbl pre-Ukraine, then held just above $100, now $120. Natural gas from normal $4-$5/mbtu… since Ukraine $9. The May increase in fuel oil, $16.9%. May utility natural gas, up 8% in the month. You can see component-by-component, month-by-month CPI here BLS Table A.

Those Other Four Moments…

-

1979, Saturday of Columbus Day Weekend, Paul Volcker announced that the Fed would allow the cost of money to float as high as necessary. Mortgages 11% on Friday, on Tuesday after the holiday 13%. However! That was 15 years into entrenched inflation, oil ten times as expensive in 1979 as 1972, and our economy just beginning energy conservation and new supply. All incomes ramped right along with inflation. The US economy was a “things” economy, with little overseas competition for union-heavy US labor.

-

1994, February… the cost of money coming out of recession 1.00%, by year-end 1994 to 5.25% — but in a disinflationary world, the cost of money was one-half the cycle peak four years before. 1994, February to May, mortgages from 7% to 9% — that magic two-point rise flattened housing, and the Fed had to cut in 1995 to dodge recession. The new mortgage peak, stabilizing near 8% was down from 11% in 1990, and we enjoyed a genuine and rare soft landing.

-

2007, July… you had to be deep in the mortgage racket to understand the first collision. Subprime and Jumbos went no-bid, and stayed there. The Fed was slow to understand the credit panic, began frantic cuts the following winter from 5.25% to 2.00%. But mortgages did not respond, stuck above 6.00%.

-

2008, July… the no-bid expanded to all mortgages, even government guaranteed. The 10-year T-note anticipating recession and worse fell to 3.50% while retail mortgages rose to 7.00%. That 350bps spread is the closest comparable to today’s 300bps.

Now What. At Thanksgiving 2008 the credit markets (all markets) were rescued by Ben Bernanke’s genius, announcing quantitative easing — buying enough MBS and Treasurys to unlock markets in which all had been afraid to buy.

Today… is it a coincidence that MBS have blown simultaneously with the Fed’s flip from QE buying to allowing runoff and threatening to sell? The weak break first. MBS are weird, and weird under stress is weak.

The Fed has had a plan, Powell becoming more concise each day: We will raise the cost of money until inflation comes under control. “It is our job to calibrate demand to supply.” A good, tidy, sorta mathematic way to proceed. But destruction of demand has limits, and this morning we hit one.

In today’s US, nobody is prepared to deal with inflation as it has developed in the last 90 days. Inflation can drop and even stabilize above the Fed’s target, but the world is only three months into finding alternate energy for Europe’s oil and gas imports from Russia. Including natural gas, something like 15% of the world’s energy supply has been dislocated.

Perhaps half will quickly be redirected. India and China are buying at a deep discount from Vladimir, which makes available much of the supply which those two used to buy elsewhere, Europe lining up. But Russian production is already suffering, a net and permanent loss. Alternate supplies require alternate delivery, gas especially tough — absent pipelines, all gas deliveries are dependent on scarce LNG ships and terminals. Coal normal, $50-$100/ton… today $395.

In this circumstance, the Fed’s demand destruction has all the wisdom of Xi’s zero-covid. In a rational world, if the party in power in DC were not encumbered by climateers, we would turn on the hose, take every step to unimpede production and delivery. Instead of threatening to tax windfall profits, we would offer incentive price guarantees to protect producers from the energy price drop certain to lie ahead. This is an energy problem, not some amorphous inflation amoeba.

Below the 10-year T-note in the last twenty years. In 2018 there were a few days with trades above 3.20%, so in theory 10s have not broken that critical support. Theories like that tend to last a few days. The Fed has to decide how much destruction it has in mind.

The 2-year T-note had been remarkably stable post-Ukraine, looking for the Fed to proceed quickly from today’s 1.00% to 2.75%. The chart is one year back, and at the moment cautious but unhinged:

Coal… under pressure since mid-2021, quadrupled from normal since Ukraine:

For further analysis on this, click here.

Tyler Durden

Sun, 06/12/2022 – 12:50

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com