Will The Fed Bring Back That 70’s Show? Stay Tuned

Authored by Nicholas Baum via The Mises Institute,

Those who don’t learn from the past, as the old adage goes, are doomed to repeat it. Even in the realm of something as seemingly abstract and technical as economic policy, this saying holds true. Prices are soaring in all areas of consumption, from the grocery store aisle to the pump, with the United States experiencing its highest rate of inflation since 1981.

Yet this, in turn, brings up the question of what caused inflation to be even higher over forty years ago. The reason why inflation was so high back then is the same reason behind why we’re experiencing similar levels of it today. That is, an incredibly loose monetary policy employed by the Fed, often as the result of political pressures from the White House.

As we’ll see, however, history also provides a solution to the problem of inflation, but it will require a sense of bravery and resilience particularly in Fed Chairman Jay Powell in a manner that has not been seen in forty years, under then-Fed Chairman Paul Volcker.

Paul Volcker and The Great Inflation

If today’s inflation seems bad, consider the years between 1965 and 1982, a period when inflation averaged 6.7% a year and became so unbearable that the era became known as “The Great Inflation.” This nearly two-decade long spell of soaring prices was certainly the product of many factors, yet the first and most prominent undoubtedly being an excessively loose, and misguided, monetary policy.

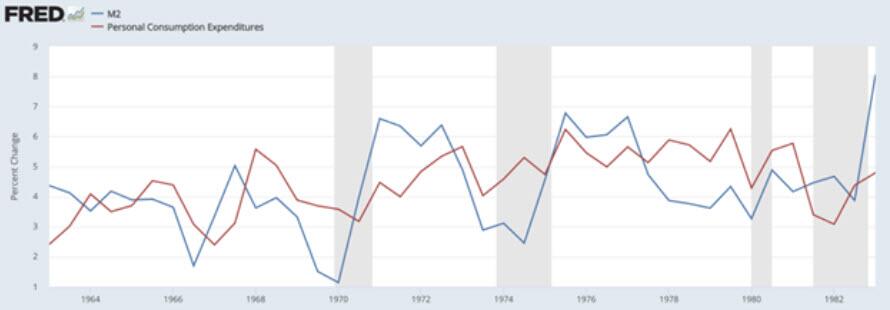

Consider the graph below, taken from the Federal Reserve Economic Database:

The blue line shows percent growth in the money supply while the red line shows the rate of inflation, measured every half-year. Clearly, there’s a general correlation where changes in inflation follow changes in the money supply. The correlation may not be very tight at times, but keep in mind that economists believe that it takes up to six months for inflation to reflect changes in the money supply.

Given this information, it’s clear that the Great Inflation was largely motivated by monetary policy, reflecting both the incompetence and flawed incentives of central banking. Take the beginning of the crisis for example; future Fed Chair Alan Greenspan writes:

In 1964, (President Lyndon B. Johnson) bullied the Federal Reserve into keeping interest rates as low as possible at the same time as delivering a powerful fiscal stimulus by signing tax cuts into law… the combination of tax cuts and low interest rates began to produce inflationary pressure.

Indeed, inflation grew from 4.77 percent annually between 1960 and 1963 to 7.82 percent from 1964 to the end of the decade, yet the outlook only worsened. The large spike in money supply growth starting around 1970 was largely due to President Richard Nixon’s similar tactics of pressuring the Fed into cutting interest rates, especially in the buildup to his re-election in 1972.

The Nixon tapes record several conversations of the President with then-Fed Chair Arthur Burns. These recordings include the President laughing about Burns’ claim that the Fed is independent and exclaiming that “(many elections) have been lost on the issue of unemployment. None has been lost on the issue of inflation.”

Matters were made worse when Nixon readied a series of anonymous leaks about the Fed, including plans to increase White House control over the central bank and even a false story that Burns wanted a pay raise when he actually suggested a pay cut.

Burns caved into this pressure. Interest rates fell from 9 percent at the start of 1970 to 3.8 percent by the first Presidential primary in March 1972, and the money supply grew at an average of 9.7 percent per year. Of course, while Nixon and Burns neglected it, inflation grew from 7.13 percent in 1970 to 10.6 percent in 1973.

As the 1970’s progressed, inflation worsened as it continued to mirror high money supply growth, as the graph confirms, with its height towards the end of the decade reflecting nervous incompetence at the Fed. By 1978, the Fed Chair was G. William Miller, widely regarded to be the worst Fed Chair in history, who barely moved interest rates and allowed money supply growth to continue around 8 percent annually while inflation reached around a staggering 11.5 percent during his tenure.

By the turn of the 1980’s, it had become evident that soaring inflation was both caused and continued by a loose monetary policy, and that something had to have been done to address the situation. Against this backdrop came the revolutionary Fed Chair Paul Volcker, who would provide the ultimate solution to the inflationary problem.

The solution, of course, was rather simple; raise interest rates and decrease the money supply.

This piece of Econ 101 logic was certainly known to Volcker’s predecessors at the Fed, but they simply couldn’t go through with it because of sheer political pressure to keep interest rates low.

The previous Fed Chairs, fearing for their jobs and the future of their agency, were essentially forced into neglecting inflation.

Soaring prices, of course, is a huge problem to the average voter, but as Nixon reminded Burns, many elections “have been lost on the issue of unemployment. None has been lost on the issue of inflation.”

Volcker resisted, however, and even as President Jimmy Carter publicly criticized his tight policy and President Ronald Raegan’s Chief of Staff James Baker privately pressured Volcker into giving up, the Fed Chair tightened interest rates from 10.94 percent at his arrival in August 1979 to an unprecedented 19 percent by the turn of 1981.

Volcker demonstrated a sense of bravery and commitment never before seen at the Fed, resisting political pressures and nerves to address rampant inflation. Consequently, inflation began its gradual decline, by some estimates reaching healthy levels of around 3 percent by 1983.

Jay Powell and Inflation Today

In the words of famed economist Milton Friedman, “Inflation is always and everywhere a monetary phenomenon.” What the brief history lesson of the US’s last encounter with high inflation shows is that the primary culprit behind soaring prices is the Fed itself, and not necessarily because Fed officials don’t care about inflation or don’t know how to fix it, but because they fear the political repercussions of addressing it.

All it took was one brave Fed Chairman, Paul Volcker, to finally put an end to the dilemma, but since then inflation has obviously reappeared. The Fed’s response to the brief recession triggered by government lockdowns saw the injection of over $4 trillion in additional money into the economy, and an almost 20 percent increase in the money supply in 2020 alone. High levels of inflation have, of course, followed this.

Now, it’s up to Fed Chair Jay Powell to right the wrongs of his leadership two years ago. Although the logic is simple, raising interest rates and choking inflation is no easy task, and Powell will certainly be on the receiving end of pressure both from Biden and Congress.

This makes the present moment all the more critical as the US faces the possibility of an inflation-induced recession. Jay Powell will need to replicate the bravery found in Paul Volcker forty years ago.

Tyler Durden

Fri, 07/29/2022 – 14:44

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com