Cracks In The World Economy Are Starting To Show

Submitted by QTR’s Fringe Finance

Friend of Fringe Finance Lawrence Lepard released his most recent investor letter this week, with his updated take on the monetary miasma spreading across the globe.

For those that missed it, Larry also talked with me on my podcast just days ago. I believe him to truly be one of the muted voices that the investing community would be better off for considering. He’s the type of voice that gets little coverage in the mainstream media, which, in my opinion, makes him someone worth listening to twice as closely.

Larry was kind enough to allow me to share his thoughts heading into Q4 2022. The letter has been edited ever-so-slightly for formatting, grammar and visuals.

This is Part 1 of his letter. Part 2 can be found here.

In the third quarter, virtually all asset classes went for a roller coaster ride – a sharp bear market rally in July and August, followed by a vicious sell off in September as the Fed continued its Hawkish tone at Jackson Hole in late August and then raised the Fed Funds rate in September to 3.00-3.25%. Recall that as recently as February 2022 Fed Funds was at 0.0-0.25%.

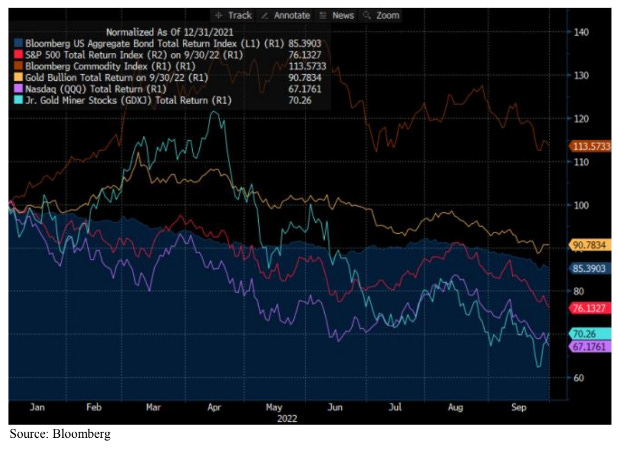

Year to date through 9/30/22, the S&P 500 and Nasdaq are down -24% and – 33%, respectively. Gold and Gold Miners (GDXJ) are down -9% and -30% year to date, respectively. Bloomberg’s US Aggregate Bond Index is down -15%. Only the Bloomberg Commodity Index (broad commodities like oil that are benefiting from inflation) is up year to date (+13.5%).

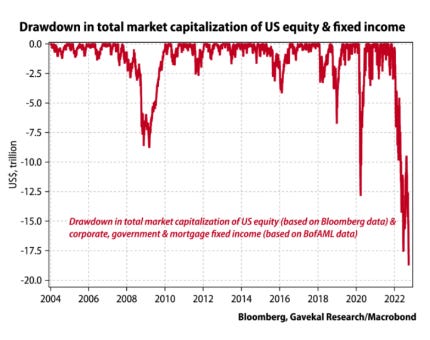

The Fed’s hawkishness has caused an enormous amount of wealth destruction. As the chart below shows, US stocks and bonds have created a drawdown of $18 Trillion in the US equity and fixed income markets, far worse than 2008 and 2020’s market value destruction. Yet, despite this the Fed maintains that a “soft landing” is still attainable in this downturn. We believe this “soft landing” will be about as accurate as their prior contention that “inflation is transitory”.

CENTRAL BANK HAWKS

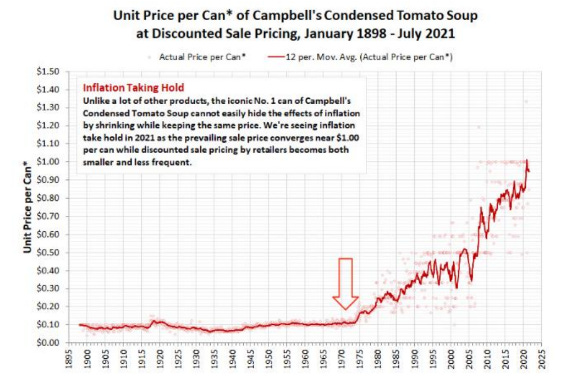

Throughout the 20th century, bouts of inflation tended to be modest (with the exception of short periods where externalities drove much higher inflation – e.g., WWII or Vietnam). However, once the pure fiat economy emerged post 1971, inflation and credit cycles became more the norm with a periodic crisis about every decade. Notice in the chart below how rapid the price of a can of Campbell’s Soup inflated once we went off the gold standard (see arrow at 1971).

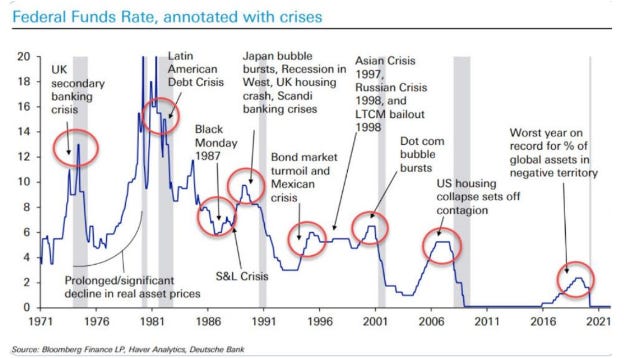

With inflation, growing fiscal deficits and the Fed’s increasing intervention in controlling interest rates and money supply, various crises often popped up as the chart below shows.

Notice how the Fed Funds Rate (blue line) would be increased by the Fed, only to lead to a unique crisis. Note further, how at each crisis, the Fed was forced to rapidly lower rates and come to the rescue.

Well, we are on our way to the Fed creating the next major crisis. Throughout 2022, the Fed has yet again, tried to fight inflation (mind you, inflation largely of their own making – even when accounting for Covid supply chain issues and the Ukraine War). The Fed has been as aggressive as they were in the late 1970s in raising rates this year and reducing the money supply.

FRAGILE, LEVERED WORLD

A levered global economy is a fragile system when the cost of debt begins to increase, and particularly sensitive to aggressive rate moves like the Fed has been conducting. Many just assume that “things will be fine; rates can rise and the Fed can solve inflation like it did in the 1970s.”

However, the world is far more leveraged than in the 1970s. Global Debt/GDP is 2.5x larger than in the 1970s (see chart below). As a subset of that, the US has a Federal Debt/GDP level of 130% vs. only 30% in the 1970s. Financing costs matter a lot in an economy that has accumulated such a huge debt load over the past 40-50 years.

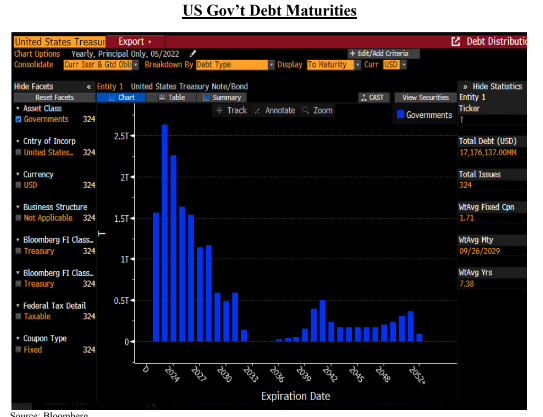

Moreover, the maturity profile picture of US Government debt is not pretty. The chart below depicts the US Treasury bond maturities. Notice how the vast majority of the outstanding US Treasury bonds mature in the next 4 years.

Former Treasury Secretary Mnuchin tried to extend the duration, but alas there was scant demand for long term US Treasuries. Now, yes – it’s easy to conclude that the US will easily refinance that debt. But what if rates are a lot higher given a lack of buyer interest? Or if Japan sells their $1.2 Trillion + of US Treasuries they hold? Or US Fiscal Deficits balloon further which requires even more treasury debt issuance?

Leverage is dangerous like a grenade. Particularly, when US interest rates spike as shown below. The extremely rapid increase in the interest rate on the US 2 year Treasury bonds is going to wreak havoc on the US Treasury’s interest expense, which in turn will have a huge impact on the US Federal budget.

It is important to understand the math associated with higher US Government interest rates. With over $31T of debt, the US Government budget is at great risk of running unsupportable deficits if interest rates continue to increase. In the fiscal year ended 9/30/22, the US Federal Government incurred interest expense of $392B. Today, on a going forward, run-rate basis, the Treasury has interest expenses of $672B annualized. If rates continue to increase to say an average of 4%, interest expense would be $1.2T, and 5% would imply $1.6T. The latter number is almost $1.0T larger than our current run rate.

Granted, this math assumes all the debt rolls over instantly, however, the average duration on the Treasury debt is around 3 years, so higher rates will impact interest expenses very shortly.

Get 50% off: If you enjoy this article, would like to support my work and have the means, I would love to have you as a subscriber and can offer you 50% off for life: Get 50% off forever

US FEDERAL BUDGET DEFICITS ARE ABOUT TO BALOON BIGGER

Presently, the Congressional Budget Office (CBO) is projecting a $1.0T Federal deficit in 2022. However, this number is distorted for several reasons. First, Federal tax receipts in 2022 were almost $600B above trend line due to capital gains taxes collected from stock market investors in a raging bull market that did not end until 2021 (capital gains taxes were paid in April 2022). Second, Social Security, which represents $1.2T of annual spending is about to get a 8.7% COLA adjustment upward, so the cost will increase by $104B. Third, the President just forgave over $400B of Student Debt (it is unclear if this will flow through the budget, but it should). Fourth the Congress has passed several bills including an infrastructure bill and an inflation protection act.

Each will add hundreds of billions to the deficit. And finally, the economy is slowing down rapidly following the Fed’s rate hikes. In past downturns (2000, and 2008) tax receipts have fallen between 8 and 15% and social expenditures have increased by similar percentages. We foresee a Federal Budget Deficit that will easily approach or exceed $2.0T in the 2023 fiscal year. All of this spending will need to be paid for by issuing new debt. So pro forma one year from now, the Government will be paying interest on at least $33T of Treasury debt.

We also know that historically gold has performed best when Government deficits are large and growing. We do not believe the market understands what a deficit problem the US is about to encounter. When it becomes more apparent that the US has a Fiscal and Debt servicing problem and that interest costs are making it worse, then the demand for US Treasury securities will fall. This in turn will lead to higher interest rates. Ultimately, we believe the Fed will be forced into Yield Curve Control (YCC) because they will do the same math and determine that the US Treasury is unable to carry the higher interest burden. However, recall that YCC can only be accomplished by growing the Fed balance sheet to issue new debt (QE) which is used to purchase old debt. This would constitute a pivot and would be wildly inflationary.

CRACKS IN THE WORLD ECONOMY ARE BEGINNING TO EMERGE

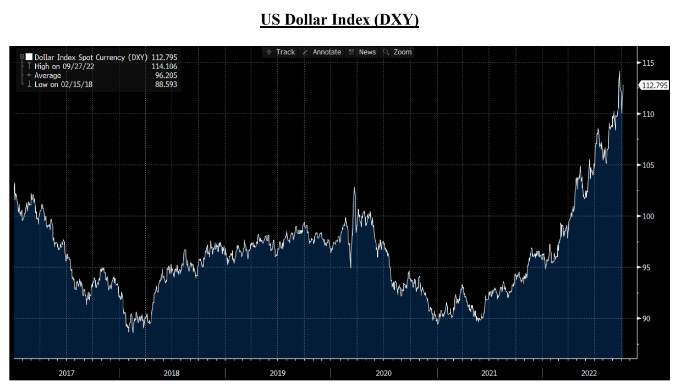

Despite the fact that the US fiscal situation is getting worse, the Fed’s aggressive tightening actions have led to exceptional relative strength in the US Dollar. This strength has hurt countries all over the world as they pay a higher price for dollar based imports (~80% of global trade is priced in dollars – think oil, steel, copper, fertilizer etc.) and on any dollar denominated debt.

We are already beginning to see major economic cracks emerge as a result of this aggressive Fed tightening and its impact on the dollar.

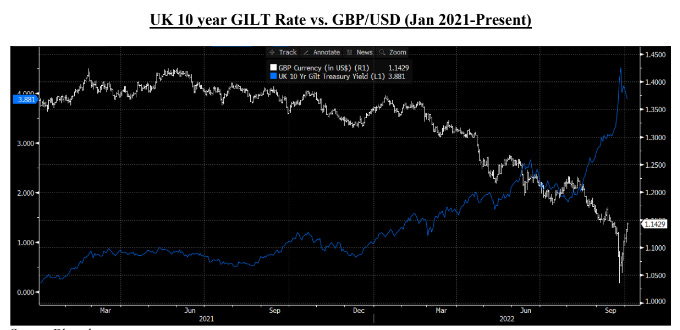

Great Britain, in particular, is a good preview of how a crisis can unfold as interest costs impact a bond market. A new Prime Minister in the UK made a policy error (arguably) by promising tax cuts and increased social spending to cap the costs of higher electricity for businesses and citizens. The UK bond and currency markets did not like this very much. As you can see in the chart below the Great British Pound (GBP) began to depreciate rapidly (white line in chart below). Simultaneously, interest rates in the UK began to increase quite rapidly (blue line in chart below). What had started out as trends during 2021 and the first half of 2022 turned into routs.

In turn, this left UK Pension Funds with massive mark to market losses as their interest rate and currency hedges were reeling and their bond holdings were declining in value.

The resulting Bloomberg Headline read: BOE Pledges Unlimited Bond Buying to Avert Imminent Gilts Crash

On September 28th, the Bank of England was forced to come in with a £65bn assistance package to buy bonds from Pension funds. Kerrin Rosenberg, a UK Pension expert said, “If there was no intervention today, gilt yields could have gone up to 7-8% from 4.5% this morning an in that situation around 90% of UK pension funds would have run out of collateral,” Another UK banker said “the leverage unwind in UK gilts came close to triggering a Lehman moment.”

This episode serves as a preview of what will become writ large in terms of a WSDC (World Sovereign Debt Crisis). Central Banks will be forced to avert crises by going right back to printing money and buying bonds via Quantitative Easing (QE).

This UK Sovereign debt and currency crisis, which then led to a Pension crisis is a major issue that may be the big grenade that sets off our next major crisis. In essence – a summary of what UK Pensions have done is:

-

They were desperate for yield to be able to fund future pension payments`

-

Over 2/3 of UK Pension Funds entered into a scheme called LDI (liability-driven investment strategy). In LDI, the funds lever up with only small amounts of equity and invest in derivatives to enhance their returns.

-

It’s similar to what many US funds have done called Risk Parity – whereby funds desperate for yield in their 60/40 stock/bond portfolios, and thinking bond prices are stable, lever up their bond portfolio to get even greater yield

-

In both LDI and Risk Parity, that works fine, until the underlying asset (bonds) lose value rapidly in a rising rate environment. Then, the fund’s leverage bites them badly and margin calls ensue.

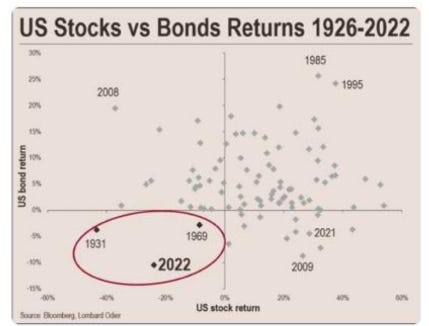

JP Morgan estimates that mark to market losses on derivatives linked to LDI could be over GBP125 billion. (6% of UK GDP). But now, assume this environment where both global stocks and bonds continue to decline together – this can ripple to the Risk Parity funds too. Indeed, as the chart below shows, it is rare for stocks AND bonds to decline at the same time:

Furthermore, there is a fascinating historical record associated with the two prior instances. Both were precedent to a revaluing of currencies versus gold. In the 1931 example the declines in stocks and bonds led to Roosevelt’s devaluation of the dollar in 1934 (a 70% devaluation versus gold) and in the 1969 example it was only two years before the US was forced to abandon the Gold Standard in the Nixon shock1. What will happen this time? Suffice it to say, we believe this is truly going to be historic.

Beyond the UK, cracks are beginning to emerge even in the massive $20 Trillion+ US Treasury market (something that has rarely ever been seen before). Last Wednesday October 12, Yellen addressed US Treasury market liquidity concerns and the possible need for the US Treasury itself to provide liquidity to that market (the irony, given the Treasury has deficits yet plans to use even more borrowed money to provide liquidity!)

Part 2 of Larry’s letter can be read here.

About Larry Lepard

Larry manages the EMA GARP Fund, a Boston based investment management firm. Their strategy is focused on providing “Monetary Debasement Insurance”. He has 38 years experience and an MBA from Harvard Business School. On Twitter he is @LawrenceLepard Managing Partner and, via email, he is [email protected]

Disclaimer: QTR is long various gold and silver miners and have both long and short exposure to the market through equities and derivatives. I have no position in Larry’s funds. Larry is a subscriber to Fringe Finance and has been on my podcast. The excerpts from Larry’s letter, above, shall not be construed as an offer to sell, or the solicitation of an offer to sell, any securities or services. Any such offering may only be made at the time a qualified investor receives from EMA formal materials describing an offering plus related subscription documentation. There is no guarantee the Fund’s investment strategy will be successful. Investing involves risk, and an investment in the Fund could lose money. The strategy is also subject to the following risks: Currency Risk, Non-US Investment Risks, Issuer Specific Risk.

Tyler Durden

Fri, 10/21/2022 – 08:16

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com